BW Offshore Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

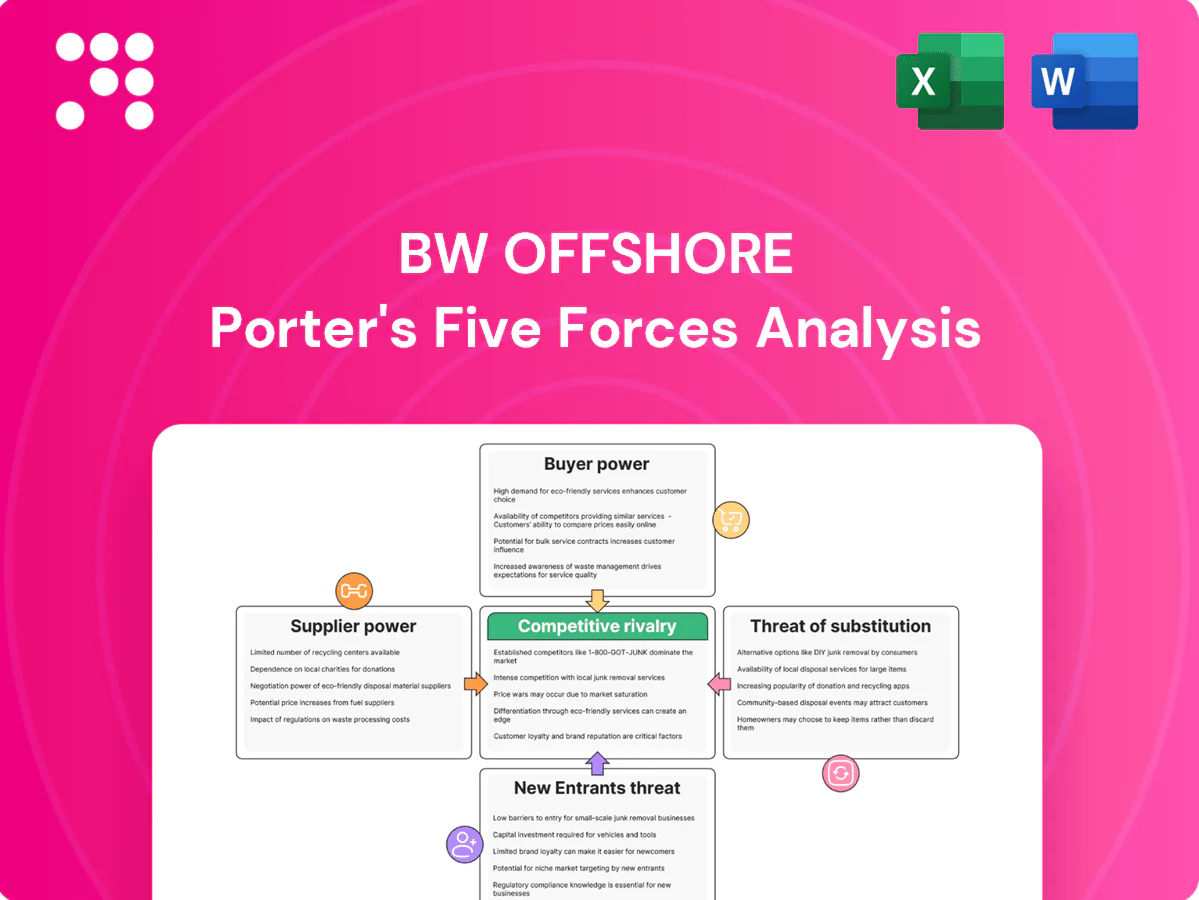

BW Offshore faces intense competitive rivalry, significant supplier and buyer pressures, and evolving threats from new entrants and substitutes—this snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable strategy insights for confident investment and planning.

Suppliers Bargaining Power

Concentrated qualified shipyards

Only about 4–6 Tier‑1 Asian yards (Samsung, Hyundai, Daewoo, Keppel, COSCO/Sembcorp) can build or convert large FPSOs to class and schedule, creating concentration risk. Limited yard slots push lead times to roughly 18–36 months during upcycles, giving yards pricing and scheduling leverage over BW Offshore. Dependency rises for complex hull conversions and integration scopes where specialized expertise is scarce. Diversifying yards and booking slots early partially offsets this supplier power.

Critical long-lead OEMs

Critical long-lead items such as turbomachinery, compressors, swivel stacks and subsea interface kits are sourced from few global OEMs (GE Vernova, Siemens Energy, MAN Energy Solutions), creating supplier concentration; lead times in 2024 commonly run 12–18 months. Design lock-in after frozen specs makes switching costly, so OEM delays or price hikes cascade into EPC schedules and liquidated damages exposure. Framework agreements and dual-qualifying packages mitigate but do not eliminate this supplier power.

Specialized marine services

Class societies such as DNV, ABS, Lloyds Register and Bureau Veritas, alongside mooring and turret specialists and offshore installation contractors, hold niche accreditation and safety expertise required by clients and regulators in 2024, granting them negotiation leverage. Peak market periods have tightened availability and pushed day rates higher. Multi-year partnerships and standardization of procedures help BW Offshore balance terms and secure capacity.

Commodity and logistics volatility

Steel, fuel and global logistics drove roughly 35% of FPSO capex/opex in 2024, and price or shipping shocks in 2024 have been sufficient to erode 5–15% of project margins post‑FID. Hedging and pass‑through clauses in lease and EPCI contracts lower exposure but do not fully shield against multi-month shipping constraints. Inventory planning and near‑shore staging cut schedule risk and margin volatility.

- 2024 steel/fuel/logistics ≈35% of cost stack

- Price/shipping shocks can cut 5–15% margins post‑FID

- Hedging/pass‑through help but not fully protective

- Inventory planning & near‑shore staging reduce schedule risk

Skilled labor and crewing

Experienced offshore crews and engineers remain scarce in 2024, with industry estimates pointing to a global seafarer/officer gap around 100,000 that tight cycles amplify; wage inflation and retention bonuses (reported up to ~15% in some basins 2023–24) boost manning agencies' bargaining power. Local content rules in Brazil and West Africa intensify basin-specific bottlenecks, while BW Offshore’s training pipelines and in-house crewing reduce external dependency.

- 2024 shortage ≈100,000 (industry estimate)

- Wage/bonus inflation up to ~15%

- In-house training lowers supplier leverage

Supply squeeze: 4–6, 12–18m leads cut FPSO margins

Only 4–6 Tier‑1 yards dominate FPSO builds (18–36m lead times) and OEMs (GE, Siemens, MAN) have 12–18m lead times in 2024, creating concentrated supplier power. Class societies and specialists command premiums during peaks. Steel/fuel/logistics ≈35% of cost; shocks cut 5–15% margins despite hedges and pass‑throughs.

| Item | 2024 metric | Impact |

|---|---|---|

| Tier‑1 yards | 4–6 | High leverage |

| OEM lead time | 12–18m | Schedule risk |

| Cost share | ≈35% | Margin exposure 5–15% |

What is included in the product

Concise Porter’s Five Forces appraisal tailored to BW Offshore, uncovering competitive intensity, buyer and supplier leverage, substitute threats, and entry barriers shaping its FPSO-focused profitability. Includes strategic implications for pricing, contract terms, and defensive moves against emerging offshore entrants and technology-driven substitutes.

One-sheet Porter's Five Forces for BW Offshore that distills competitive pressures into a customizable radar view for swift strategic decisions. Clean, no-code layout lets you tweak inputs, compare scenarios, and drop the chart straight into decks or reports.

Customers Bargaining Power

Few large IOC/NOC buyers

Global FPSO demand is concentrated among a few majors and NOCs (e.g., Petrobras, ADNOC, Petronas) that in 2024 drive procurement for a global fleet of roughly 200 FPSOs; they run competitive tenders that pressure lease rates and insist on tighter performance guarantees. Vendor lists and prequalification amplify buyer leverage, though long-term relationships and proven uptime can mitigate pricing pressure.

High pre-award optionality

Before FID buyers in 2024 retained high optionality—able to switch concepts, choose rival FPSO contractors, or defer sanction—strengthening price and term leverage. This forces BW Offshore, with a fleet of 9 FPSOs in 2024, to differentiate on schedule, reliability and bespoke financing solutions. Early engagement and FEED participation let BW shape specs and reduce apples-to-apples bidding, shortening decision cycles and protecting margins.

Switching costs mid-contract

Once an FPSO is contracted and integrated, switching suppliers typically incurs redeployment and re-configuration costs often exceeding $100 million and operational disruption risks, reducing buyer leverage during operations. Downtime can cost operators an estimated $1–5 million per day, further discouraging mid-contract changes. Renewal options and extension talks reopen pricing discussions, where BW Offshore’s strong uptime KPIs (commonly 98–99%+) and low emissions profiles command better renewal terms.

Local content and risk transfer

Buyers in 2024 increasingly insist on local content, stronger ESG performance and risk-sharing on schedule and carbon intensity, shifting costs and execution risk to contractors; meeting these conditions can secure awards but often compresses margins. Transparent allocation of risks and incentive-linked payments can rebalance outcomes and protect contractor returns.

- Buyers: local content + ESG + risk-share (2024)

- Impact: higher contractor costs, margin compression

- Mitigation: clear risk allocation, incentive mechanisms

Access to financing as a lever

Clients often prefer contractors who can bundle lease financing and project debt, using control over financing terms as a buyer negotiation lever; BW Offshore’s balance sheet strength and lender network allow it to absorb financing risk and push back on price concessions. Green or transition-linked financing further differentiates bids, attracting ESG-focused buyers and potentially lowering capital costs for BW Offshore.

- Bundle financing: strengthens bids

- Balance sheet: counters buyer leverage

- Green finance: ESG differentiation

Buyers steer ~200 FPSO tenders; switching costs >$100M

Buyers (Petrobras, ADNOC, Petronas) drive procurement for ~200 FPSOs in 2024, running competitive tenders that compress lease rates; BW Offshore (9 FPSOs) counters via uptime, schedule and financing. Pre-FID optionality strengthens buyer leverage, while in-contract switching costs (> $100M) and downtime ($1–5M/day) reduce it; ESG/local-content demands shift costs to contractors.

| Metric | 2024 | Impact |

|---|---|---|

| Global FPSOs | ~200 | Competitive tenders |

| BW fleet | 9 | Differentiation via uptime |

| Downtime cost | $1–5M/day | Discourages switching |

| Switching cost | >$100M | Locks suppliers |

Preview Before You Purchase

BW Offshore Porter's Five Forces Analysis

This preview shows the exact BW Offshore Porter's Five Forces Analysis you'll receive after purchase—fully formatted and ready to use. It contains the complete competitive assessment, key implications and actionable insights. No placeholders or samples; instant download on payment.

Go Beyond the Preview—Access the Full Strategic Report

BW Offshore faces intense competitive rivalry, significant supplier and buyer pressures, and evolving threats from new entrants and substitutes—this snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable strategy insights for confident investment and planning.

Suppliers Bargaining Power

Concentrated qualified shipyards

Only about 4–6 Tier‑1 Asian yards (Samsung, Hyundai, Daewoo, Keppel, COSCO/Sembcorp) can build or convert large FPSOs to class and schedule, creating concentration risk. Limited yard slots push lead times to roughly 18–36 months during upcycles, giving yards pricing and scheduling leverage over BW Offshore. Dependency rises for complex hull conversions and integration scopes where specialized expertise is scarce. Diversifying yards and booking slots early partially offsets this supplier power.

Critical long-lead OEMs

Critical long-lead items such as turbomachinery, compressors, swivel stacks and subsea interface kits are sourced from few global OEMs (GE Vernova, Siemens Energy, MAN Energy Solutions), creating supplier concentration; lead times in 2024 commonly run 12–18 months. Design lock-in after frozen specs makes switching costly, so OEM delays or price hikes cascade into EPC schedules and liquidated damages exposure. Framework agreements and dual-qualifying packages mitigate but do not eliminate this supplier power.

Specialized marine services

Class societies such as DNV, ABS, Lloyds Register and Bureau Veritas, alongside mooring and turret specialists and offshore installation contractors, hold niche accreditation and safety expertise required by clients and regulators in 2024, granting them negotiation leverage. Peak market periods have tightened availability and pushed day rates higher. Multi-year partnerships and standardization of procedures help BW Offshore balance terms and secure capacity.

Commodity and logistics volatility

Steel, fuel and global logistics drove roughly 35% of FPSO capex/opex in 2024, and price or shipping shocks in 2024 have been sufficient to erode 5–15% of project margins post‑FID. Hedging and pass‑through clauses in lease and EPCI contracts lower exposure but do not fully shield against multi-month shipping constraints. Inventory planning and near‑shore staging cut schedule risk and margin volatility.

- 2024 steel/fuel/logistics ≈35% of cost stack

- Price/shipping shocks can cut 5–15% margins post‑FID

- Hedging/pass‑through help but not fully protective

- Inventory planning & near‑shore staging reduce schedule risk

Skilled labor and crewing

Experienced offshore crews and engineers remain scarce in 2024, with industry estimates pointing to a global seafarer/officer gap around 100,000 that tight cycles amplify; wage inflation and retention bonuses (reported up to ~15% in some basins 2023–24) boost manning agencies' bargaining power. Local content rules in Brazil and West Africa intensify basin-specific bottlenecks, while BW Offshore’s training pipelines and in-house crewing reduce external dependency.

- 2024 shortage ≈100,000 (industry estimate)

- Wage/bonus inflation up to ~15%

- In-house training lowers supplier leverage

Supply squeeze: 4–6, 12–18m leads cut FPSO margins

Only 4–6 Tier‑1 yards dominate FPSO builds (18–36m lead times) and OEMs (GE, Siemens, MAN) have 12–18m lead times in 2024, creating concentrated supplier power. Class societies and specialists command premiums during peaks. Steel/fuel/logistics ≈35% of cost; shocks cut 5–15% margins despite hedges and pass‑throughs.

| Item | 2024 metric | Impact |

|---|---|---|

| Tier‑1 yards | 4–6 | High leverage |

| OEM lead time | 12–18m | Schedule risk |

| Cost share | ≈35% | Margin exposure 5–15% |

What is included in the product

Concise Porter’s Five Forces appraisal tailored to BW Offshore, uncovering competitive intensity, buyer and supplier leverage, substitute threats, and entry barriers shaping its FPSO-focused profitability. Includes strategic implications for pricing, contract terms, and defensive moves against emerging offshore entrants and technology-driven substitutes.

One-sheet Porter's Five Forces for BW Offshore that distills competitive pressures into a customizable radar view for swift strategic decisions. Clean, no-code layout lets you tweak inputs, compare scenarios, and drop the chart straight into decks or reports.

Customers Bargaining Power

Few large IOC/NOC buyers

Global FPSO demand is concentrated among a few majors and NOCs (e.g., Petrobras, ADNOC, Petronas) that in 2024 drive procurement for a global fleet of roughly 200 FPSOs; they run competitive tenders that pressure lease rates and insist on tighter performance guarantees. Vendor lists and prequalification amplify buyer leverage, though long-term relationships and proven uptime can mitigate pricing pressure.

High pre-award optionality

Before FID buyers in 2024 retained high optionality—able to switch concepts, choose rival FPSO contractors, or defer sanction—strengthening price and term leverage. This forces BW Offshore, with a fleet of 9 FPSOs in 2024, to differentiate on schedule, reliability and bespoke financing solutions. Early engagement and FEED participation let BW shape specs and reduce apples-to-apples bidding, shortening decision cycles and protecting margins.

Switching costs mid-contract

Once an FPSO is contracted and integrated, switching suppliers typically incurs redeployment and re-configuration costs often exceeding $100 million and operational disruption risks, reducing buyer leverage during operations. Downtime can cost operators an estimated $1–5 million per day, further discouraging mid-contract changes. Renewal options and extension talks reopen pricing discussions, where BW Offshore’s strong uptime KPIs (commonly 98–99%+) and low emissions profiles command better renewal terms.

Local content and risk transfer

Buyers in 2024 increasingly insist on local content, stronger ESG performance and risk-sharing on schedule and carbon intensity, shifting costs and execution risk to contractors; meeting these conditions can secure awards but often compresses margins. Transparent allocation of risks and incentive-linked payments can rebalance outcomes and protect contractor returns.

- Buyers: local content + ESG + risk-share (2024)

- Impact: higher contractor costs, margin compression

- Mitigation: clear risk allocation, incentive mechanisms

Access to financing as a lever

Clients often prefer contractors who can bundle lease financing and project debt, using control over financing terms as a buyer negotiation lever; BW Offshore’s balance sheet strength and lender network allow it to absorb financing risk and push back on price concessions. Green or transition-linked financing further differentiates bids, attracting ESG-focused buyers and potentially lowering capital costs for BW Offshore.

- Bundle financing: strengthens bids

- Balance sheet: counters buyer leverage

- Green finance: ESG differentiation

Buyers steer ~200 FPSO tenders; switching costs >$100M

Buyers (Petrobras, ADNOC, Petronas) drive procurement for ~200 FPSOs in 2024, running competitive tenders that compress lease rates; BW Offshore (9 FPSOs) counters via uptime, schedule and financing. Pre-FID optionality strengthens buyer leverage, while in-contract switching costs (> $100M) and downtime ($1–5M/day) reduce it; ESG/local-content demands shift costs to contractors.

| Metric | 2024 | Impact |

|---|---|---|

| Global FPSOs | ~200 | Competitive tenders |

| BW fleet | 9 | Differentiation via uptime |

| Downtime cost | $1–5M/day | Discourages switching |

| Switching cost | >$100M | Locks suppliers |

Preview Before You Purchase

BW Offshore Porter's Five Forces Analysis

This preview shows the exact BW Offshore Porter's Five Forces Analysis you'll receive after purchase—fully formatted and ready to use. It contains the complete competitive assessment, key implications and actionable insights. No placeholders or samples; instant download on payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

BW Offshore faces intense competitive rivalry, significant supplier and buyer pressures, and evolving threats from new entrants and substitutes—this snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable strategy insights for confident investment and planning.

Suppliers Bargaining Power

Concentrated qualified shipyards

Only about 4–6 Tier‑1 Asian yards (Samsung, Hyundai, Daewoo, Keppel, COSCO/Sembcorp) can build or convert large FPSOs to class and schedule, creating concentration risk. Limited yard slots push lead times to roughly 18–36 months during upcycles, giving yards pricing and scheduling leverage over BW Offshore. Dependency rises for complex hull conversions and integration scopes where specialized expertise is scarce. Diversifying yards and booking slots early partially offsets this supplier power.

Critical long-lead OEMs

Critical long-lead items such as turbomachinery, compressors, swivel stacks and subsea interface kits are sourced from few global OEMs (GE Vernova, Siemens Energy, MAN Energy Solutions), creating supplier concentration; lead times in 2024 commonly run 12–18 months. Design lock-in after frozen specs makes switching costly, so OEM delays or price hikes cascade into EPC schedules and liquidated damages exposure. Framework agreements and dual-qualifying packages mitigate but do not eliminate this supplier power.

Specialized marine services

Class societies such as DNV, ABS, Lloyds Register and Bureau Veritas, alongside mooring and turret specialists and offshore installation contractors, hold niche accreditation and safety expertise required by clients and regulators in 2024, granting them negotiation leverage. Peak market periods have tightened availability and pushed day rates higher. Multi-year partnerships and standardization of procedures help BW Offshore balance terms and secure capacity.

Commodity and logistics volatility

Steel, fuel and global logistics drove roughly 35% of FPSO capex/opex in 2024, and price or shipping shocks in 2024 have been sufficient to erode 5–15% of project margins post‑FID. Hedging and pass‑through clauses in lease and EPCI contracts lower exposure but do not fully shield against multi-month shipping constraints. Inventory planning and near‑shore staging cut schedule risk and margin volatility.

- 2024 steel/fuel/logistics ≈35% of cost stack

- Price/shipping shocks can cut 5–15% margins post‑FID

- Hedging/pass‑through help but not fully protective

- Inventory planning & near‑shore staging reduce schedule risk

Skilled labor and crewing

Experienced offshore crews and engineers remain scarce in 2024, with industry estimates pointing to a global seafarer/officer gap around 100,000 that tight cycles amplify; wage inflation and retention bonuses (reported up to ~15% in some basins 2023–24) boost manning agencies' bargaining power. Local content rules in Brazil and West Africa intensify basin-specific bottlenecks, while BW Offshore’s training pipelines and in-house crewing reduce external dependency.

- 2024 shortage ≈100,000 (industry estimate)

- Wage/bonus inflation up to ~15%

- In-house training lowers supplier leverage

Supply squeeze: 4–6, 12–18m leads cut FPSO margins

Only 4–6 Tier‑1 yards dominate FPSO builds (18–36m lead times) and OEMs (GE, Siemens, MAN) have 12–18m lead times in 2024, creating concentrated supplier power. Class societies and specialists command premiums during peaks. Steel/fuel/logistics ≈35% of cost; shocks cut 5–15% margins despite hedges and pass‑throughs.

| Item | 2024 metric | Impact |

|---|---|---|

| Tier‑1 yards | 4–6 | High leverage |

| OEM lead time | 12–18m | Schedule risk |

| Cost share | ≈35% | Margin exposure 5–15% |

What is included in the product

Concise Porter’s Five Forces appraisal tailored to BW Offshore, uncovering competitive intensity, buyer and supplier leverage, substitute threats, and entry barriers shaping its FPSO-focused profitability. Includes strategic implications for pricing, contract terms, and defensive moves against emerging offshore entrants and technology-driven substitutes.

One-sheet Porter's Five Forces for BW Offshore that distills competitive pressures into a customizable radar view for swift strategic decisions. Clean, no-code layout lets you tweak inputs, compare scenarios, and drop the chart straight into decks or reports.

Customers Bargaining Power

Few large IOC/NOC buyers

Global FPSO demand is concentrated among a few majors and NOCs (e.g., Petrobras, ADNOC, Petronas) that in 2024 drive procurement for a global fleet of roughly 200 FPSOs; they run competitive tenders that pressure lease rates and insist on tighter performance guarantees. Vendor lists and prequalification amplify buyer leverage, though long-term relationships and proven uptime can mitigate pricing pressure.

High pre-award optionality

Before FID buyers in 2024 retained high optionality—able to switch concepts, choose rival FPSO contractors, or defer sanction—strengthening price and term leverage. This forces BW Offshore, with a fleet of 9 FPSOs in 2024, to differentiate on schedule, reliability and bespoke financing solutions. Early engagement and FEED participation let BW shape specs and reduce apples-to-apples bidding, shortening decision cycles and protecting margins.

Switching costs mid-contract

Once an FPSO is contracted and integrated, switching suppliers typically incurs redeployment and re-configuration costs often exceeding $100 million and operational disruption risks, reducing buyer leverage during operations. Downtime can cost operators an estimated $1–5 million per day, further discouraging mid-contract changes. Renewal options and extension talks reopen pricing discussions, where BW Offshore’s strong uptime KPIs (commonly 98–99%+) and low emissions profiles command better renewal terms.

Local content and risk transfer

Buyers in 2024 increasingly insist on local content, stronger ESG performance and risk-sharing on schedule and carbon intensity, shifting costs and execution risk to contractors; meeting these conditions can secure awards but often compresses margins. Transparent allocation of risks and incentive-linked payments can rebalance outcomes and protect contractor returns.

- Buyers: local content + ESG + risk-share (2024)

- Impact: higher contractor costs, margin compression

- Mitigation: clear risk allocation, incentive mechanisms

Access to financing as a lever

Clients often prefer contractors who can bundle lease financing and project debt, using control over financing terms as a buyer negotiation lever; BW Offshore’s balance sheet strength and lender network allow it to absorb financing risk and push back on price concessions. Green or transition-linked financing further differentiates bids, attracting ESG-focused buyers and potentially lowering capital costs for BW Offshore.

- Bundle financing: strengthens bids

- Balance sheet: counters buyer leverage

- Green finance: ESG differentiation

Buyers steer ~200 FPSO tenders; switching costs >$100M

Buyers (Petrobras, ADNOC, Petronas) drive procurement for ~200 FPSOs in 2024, running competitive tenders that compress lease rates; BW Offshore (9 FPSOs) counters via uptime, schedule and financing. Pre-FID optionality strengthens buyer leverage, while in-contract switching costs (> $100M) and downtime ($1–5M/day) reduce it; ESG/local-content demands shift costs to contractors.

| Metric | 2024 | Impact |

|---|---|---|

| Global FPSOs | ~200 | Competitive tenders |

| BW fleet | 9 | Differentiation via uptime |

| Downtime cost | $1–5M/day | Discourages switching |

| Switching cost | >$100M | Locks suppliers |

Preview Before You Purchase

BW Offshore Porter's Five Forces Analysis

This preview shows the exact BW Offshore Porter's Five Forces Analysis you'll receive after purchase—fully formatted and ready to use. It contains the complete competitive assessment, key implications and actionable insights. No placeholders or samples; instant download on payment.