BWXT Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

BWXT operates in a capital‑intensive, highly regulated niche where supplier relationships, buyer concentration, and regulatory barriers shape its competitive edge; this snapshot highlights key tensions but only scratches the surface. The full Porter's Five Forces Analysis quantifies each force, maps substitute and entrant risks, and interprets implications for strategy and valuation. Unlock the complete report for visuals, force ratings, and actionable recommendations tailored to BWXT.

Suppliers Bargaining Power

Scarce nuclear-grade inputs

Supply of HEU/LEU, emerging HALEU, zirconium alloys and specialty steels is tightly constrained and subject to export controls, with only a handful of certified global suppliers, elevating suppliers’ pricing leverage; BWXT offsets risk with government-facilitated, long-term contracts and inventory buffers typically in the range of 3–12 months to smooth procurement and pricing volatility in 2024.

Qualified, hard-to-switch vendors

Nuclear QA standards such as NQA-1 and naval specs require supplier qualification that commonly takes 12–36 months, with repeated audits and documentation updates extending timelines. High switching costs from requalification, supplier audits, and customer approvals give incumbent vendors leverage over contract terms and lead times. Dual-qualifying second sources lowers but often does not eliminate dependence, as incumbents frequently retain majority share and pricing power.

Specialized equipment and tooling

Precision machining, advanced welding, and radiological systems for BWXT often come from niche OEMs, concentrating supply and giving vendors leverage as capital goods commonly carry lead times of 12–36 months. Limited alternatives and long lead-times let suppliers extract higher margins and tie pricing through bundled spares and multi-year service agreements. BWXT mitigates pressure via lifecycle contracts and targeted in-house capability development to reduce dependence on single-source suppliers.

Cleared, skilled labor as a supplier

Unionized, security-cleared nuclear trades and engineers are scarce, increasing supplier power; tight U.S. labor markets (unemployment ~3.7% in 2024) raise wage pressure and project-scheduling risk. Long training pipelines (apprenticeships often 4–5 years) amplify labor leverage. BWXT invests in apprenticeships and retention to stabilize availability.

- High scarcity: cleared, unionized specialists

- Market tightness: US unemployment ~3.7% (2024)

- Long pipelines: 4–5 year apprenticeships

- BWXT response: apprenticeship and retention investment

Geopolitical and compliance constraints

Export controls (EAR/ITAR), ongoing 2024 sanctions on Russia and Iran, and NRC/DOE qualification rules materially constrain where BWXT can source nuclear-grade materials and equipment, raising lead times and limiting global suppliers.

Compliance overhead concentrates vendors—cleared suppliers capture sourcing share and can demand premiums—while government-facilitated channels for naval programs (NNSA/Navy logistics) partially normalize pricing and contract terms.

- Export controls/EAR/ITAR limit foreign sourcing

- 2024 sanctions (Russia, Iran) restrict supplier pools

- NRC/DOE qualification raises vendor concentration

- Cleared suppliers can extract premiums

- Government channels partially standardize naval procurements

Scarce certified nuclear supplies boost supplier pricing power; buyers use contracts, buffers

Supplier power is high due to few certified HEU/LEU/HALEU and specialty-material vendors, export controls, and long requalification (12–36 months), enabling pricing leverage. BWXT offsets via government-backed long-term contracts and 3–12 month inventory buffers and in-house capability build-out. Labor scarcity (US unemployment ~3.7% in 2024) and unionized, cleared trades further elevate supplier bargaining power.

| Metric | 2024 |

|---|---|

| Requalification lead time | 12–36 months |

| Inventory buffer | 3–12 months |

| US unemployment | ~3.7% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry/substitute risks tailored to BWXT. Identifies disruptive threats, protective barriers, and strategic levers; fully editable Word format for investor materials, strategy decks, or academic use.

A concise one-sheet BWXT Porter's Five Forces snapshot that highlights nuclear supply-chain risks, regulatory pressures, and competitive threats for rapid executive decisions; customizable pressure levels and export-ready visuals simplify inclusion in decks and boardroom briefings.

Customers Bargaining Power

Concentrated government buyers

U.S. Navy/DoD and DOE are the dominant buyers for BWXT, with the DoD FY2024 enacted budget at about $858 billion, creating monopsony dynamics that concentrate negotiating power. Their scale enforces stringent contract terms, compliance and oversight. Mission-critical nuclear and reactor work limits decisions based solely on price, as performance and safety drive awards. Strong performance history can yield sole-source or limited-competition contracts.

Contract structure influence

Cost-plus versus fixed-price contracts shift risk and margin, with customers pushing for fixed-price to cap liabilities while BWXT uses cost-plus where technical uncertainty is high. Customers demand cost transparency and earned-value controls, and BWXT reported a backlog exceeding $6 billion in 2024 supporting such oversight. Incentive fees and penalties heighten execution discipline, and BWXT actively manages its contract mix to balance predictability and upside.

High switching costs for buyers

Nuclear qualification, classified security requirements, and supplier-specific IP create multi-year, costly switching processes that impede buyer mobility. Program risk and certification lead customers to avoid supplier experiments, tempering price pressure even when buyers are concentrated. Sole-source justifications commonly cite these technical and regulatory frictions as the primary rationale.

Budget cycles and political risk

Appropriations timing and continuing resolutions (CRs) disrupt BWXT order flow: FY2024 US defense discretionary funding was about 858 billion, but CRs and shifting priorities force customers to defer or re-scope programs, pressuring pricing and cash. Multi-year contracts provide cushioning but do not remove quarter-to-quarter volatility. BWXT offsets swings by diversifying across defense, DOE, and commercial customers.

- Appropriations timing: causes timing gaps

- CRs: increase order uncertainty

- Deferrals/rescoping: pressure margins and cash

- Multi-year contracts: reduce but not remove volatility

- Diversification: defense, DOE, commercial offsets

Commercial nuclear price sensitivity

Utility customers in competitive wholesale markets such as PJM (serving ~65 million people) and ERCOT push hard on outage services and fuel solutions; nuclear remained a material baseload source in 2024, with U.S. reactors providing roughly 18% of electricity per EIA, increasing buyer price sensitivity and leverage. BWXT defends value via reliability, safety record, and bundled service offerings.

- Buyer leverage: presence of alternative suppliers

- Negotiation focus: outages, fuel solutions

- Market context: PJM ~65M population served

- BWXT defense: reliability, safety, bundled services

Defense nuclear market: monopsony power, big budgets, backlog, earned-value & safety premiums

DoD/DOE monopsony concentrates negotiating power; DoD FY2024 enacted ~$858B. Contract mix (cost-plus vs fixed-price) shifts risk; BWXT reported backlog >$6B in 2024 and customers demand earned-value controls. High qualification/safety and nuclear's ~18% share of US electricity reduce pure price competition.

| Metric | 2024 |

|---|---|

| DoD enacted budget | $858B |

| BWXT backlog | >$6B |

| Nuclear share US electricity | ~18% |

| PJM population | ~65M |

Same Document Delivered

BWXT Porter's Five Forces Analysis

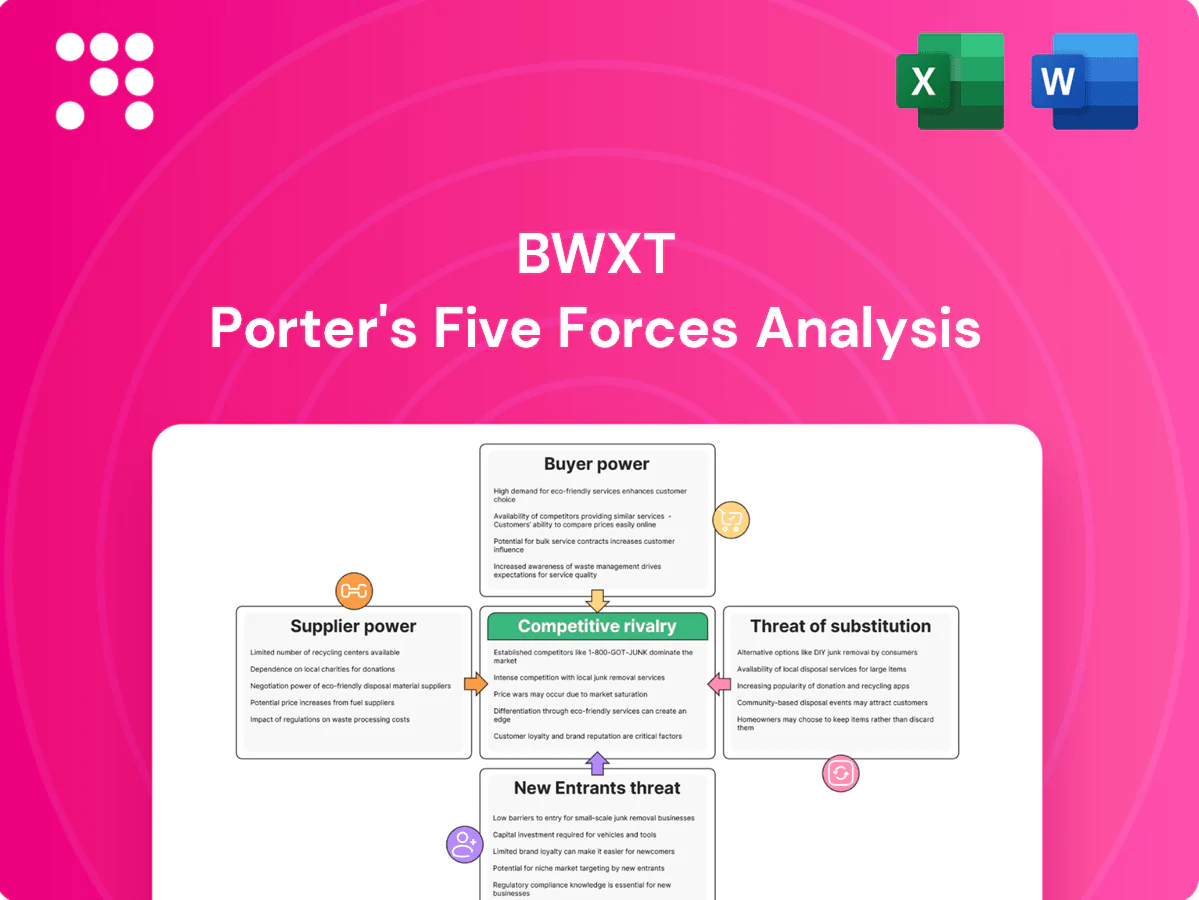

This preview shows the exact BWXT Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The file is professionally formatted and ready for download and use upon payment. It is the full, final deliverable, covering threat of entrants, supplier power, buyer power, substitutes, and competitive rivalry.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

BWXT operates in a capital‑intensive, highly regulated niche where supplier relationships, buyer concentration, and regulatory barriers shape its competitive edge; this snapshot highlights key tensions but only scratches the surface. The full Porter's Five Forces Analysis quantifies each force, maps substitute and entrant risks, and interprets implications for strategy and valuation. Unlock the complete report for visuals, force ratings, and actionable recommendations tailored to BWXT.

Suppliers Bargaining Power

Scarce nuclear-grade inputs

Supply of HEU/LEU, emerging HALEU, zirconium alloys and specialty steels is tightly constrained and subject to export controls, with only a handful of certified global suppliers, elevating suppliers’ pricing leverage; BWXT offsets risk with government-facilitated, long-term contracts and inventory buffers typically in the range of 3–12 months to smooth procurement and pricing volatility in 2024.

Qualified, hard-to-switch vendors

Nuclear QA standards such as NQA-1 and naval specs require supplier qualification that commonly takes 12–36 months, with repeated audits and documentation updates extending timelines. High switching costs from requalification, supplier audits, and customer approvals give incumbent vendors leverage over contract terms and lead times. Dual-qualifying second sources lowers but often does not eliminate dependence, as incumbents frequently retain majority share and pricing power.

Specialized equipment and tooling

Precision machining, advanced welding, and radiological systems for BWXT often come from niche OEMs, concentrating supply and giving vendors leverage as capital goods commonly carry lead times of 12–36 months. Limited alternatives and long lead-times let suppliers extract higher margins and tie pricing through bundled spares and multi-year service agreements. BWXT mitigates pressure via lifecycle contracts and targeted in-house capability development to reduce dependence on single-source suppliers.

Cleared, skilled labor as a supplier

Unionized, security-cleared nuclear trades and engineers are scarce, increasing supplier power; tight U.S. labor markets (unemployment ~3.7% in 2024) raise wage pressure and project-scheduling risk. Long training pipelines (apprenticeships often 4–5 years) amplify labor leverage. BWXT invests in apprenticeships and retention to stabilize availability.

- High scarcity: cleared, unionized specialists

- Market tightness: US unemployment ~3.7% (2024)

- Long pipelines: 4–5 year apprenticeships

- BWXT response: apprenticeship and retention investment

Geopolitical and compliance constraints

Export controls (EAR/ITAR), ongoing 2024 sanctions on Russia and Iran, and NRC/DOE qualification rules materially constrain where BWXT can source nuclear-grade materials and equipment, raising lead times and limiting global suppliers.

Compliance overhead concentrates vendors—cleared suppliers capture sourcing share and can demand premiums—while government-facilitated channels for naval programs (NNSA/Navy logistics) partially normalize pricing and contract terms.

- Export controls/EAR/ITAR limit foreign sourcing

- 2024 sanctions (Russia, Iran) restrict supplier pools

- NRC/DOE qualification raises vendor concentration

- Cleared suppliers can extract premiums

- Government channels partially standardize naval procurements

Scarce certified nuclear supplies boost supplier pricing power; buyers use contracts, buffers

Supplier power is high due to few certified HEU/LEU/HALEU and specialty-material vendors, export controls, and long requalification (12–36 months), enabling pricing leverage. BWXT offsets via government-backed long-term contracts and 3–12 month inventory buffers and in-house capability build-out. Labor scarcity (US unemployment ~3.7% in 2024) and unionized, cleared trades further elevate supplier bargaining power.

| Metric | 2024 |

|---|---|

| Requalification lead time | 12–36 months |

| Inventory buffer | 3–12 months |

| US unemployment | ~3.7% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry/substitute risks tailored to BWXT. Identifies disruptive threats, protective barriers, and strategic levers; fully editable Word format for investor materials, strategy decks, or academic use.

A concise one-sheet BWXT Porter's Five Forces snapshot that highlights nuclear supply-chain risks, regulatory pressures, and competitive threats for rapid executive decisions; customizable pressure levels and export-ready visuals simplify inclusion in decks and boardroom briefings.

Customers Bargaining Power

Concentrated government buyers

U.S. Navy/DoD and DOE are the dominant buyers for BWXT, with the DoD FY2024 enacted budget at about $858 billion, creating monopsony dynamics that concentrate negotiating power. Their scale enforces stringent contract terms, compliance and oversight. Mission-critical nuclear and reactor work limits decisions based solely on price, as performance and safety drive awards. Strong performance history can yield sole-source or limited-competition contracts.

Contract structure influence

Cost-plus versus fixed-price contracts shift risk and margin, with customers pushing for fixed-price to cap liabilities while BWXT uses cost-plus where technical uncertainty is high. Customers demand cost transparency and earned-value controls, and BWXT reported a backlog exceeding $6 billion in 2024 supporting such oversight. Incentive fees and penalties heighten execution discipline, and BWXT actively manages its contract mix to balance predictability and upside.

High switching costs for buyers

Nuclear qualification, classified security requirements, and supplier-specific IP create multi-year, costly switching processes that impede buyer mobility. Program risk and certification lead customers to avoid supplier experiments, tempering price pressure even when buyers are concentrated. Sole-source justifications commonly cite these technical and regulatory frictions as the primary rationale.

Budget cycles and political risk

Appropriations timing and continuing resolutions (CRs) disrupt BWXT order flow: FY2024 US defense discretionary funding was about 858 billion, but CRs and shifting priorities force customers to defer or re-scope programs, pressuring pricing and cash. Multi-year contracts provide cushioning but do not remove quarter-to-quarter volatility. BWXT offsets swings by diversifying across defense, DOE, and commercial customers.

- Appropriations timing: causes timing gaps

- CRs: increase order uncertainty

- Deferrals/rescoping: pressure margins and cash

- Multi-year contracts: reduce but not remove volatility

- Diversification: defense, DOE, commercial offsets

Commercial nuclear price sensitivity

Utility customers in competitive wholesale markets such as PJM (serving ~65 million people) and ERCOT push hard on outage services and fuel solutions; nuclear remained a material baseload source in 2024, with U.S. reactors providing roughly 18% of electricity per EIA, increasing buyer price sensitivity and leverage. BWXT defends value via reliability, safety record, and bundled service offerings.

- Buyer leverage: presence of alternative suppliers

- Negotiation focus: outages, fuel solutions

- Market context: PJM ~65M population served

- BWXT defense: reliability, safety, bundled services

Defense nuclear market: monopsony power, big budgets, backlog, earned-value & safety premiums

DoD/DOE monopsony concentrates negotiating power; DoD FY2024 enacted ~$858B. Contract mix (cost-plus vs fixed-price) shifts risk; BWXT reported backlog >$6B in 2024 and customers demand earned-value controls. High qualification/safety and nuclear's ~18% share of US electricity reduce pure price competition.

| Metric | 2024 |

|---|---|

| DoD enacted budget | $858B |

| BWXT backlog | >$6B |

| Nuclear share US electricity | ~18% |

| PJM population | ~65M |

Same Document Delivered

BWXT Porter's Five Forces Analysis

This preview shows the exact BWXT Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The file is professionally formatted and ready for download and use upon payment. It is the full, final deliverable, covering threat of entrants, supplier power, buyer power, substitutes, and competitive rivalry.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

BWXT operates in a capital‑intensive, highly regulated niche where supplier relationships, buyer concentration, and regulatory barriers shape its competitive edge; this snapshot highlights key tensions but only scratches the surface. The full Porter's Five Forces Analysis quantifies each force, maps substitute and entrant risks, and interprets implications for strategy and valuation. Unlock the complete report for visuals, force ratings, and actionable recommendations tailored to BWXT.

Suppliers Bargaining Power

Scarce nuclear-grade inputs

Supply of HEU/LEU, emerging HALEU, zirconium alloys and specialty steels is tightly constrained and subject to export controls, with only a handful of certified global suppliers, elevating suppliers’ pricing leverage; BWXT offsets risk with government-facilitated, long-term contracts and inventory buffers typically in the range of 3–12 months to smooth procurement and pricing volatility in 2024.

Qualified, hard-to-switch vendors

Nuclear QA standards such as NQA-1 and naval specs require supplier qualification that commonly takes 12–36 months, with repeated audits and documentation updates extending timelines. High switching costs from requalification, supplier audits, and customer approvals give incumbent vendors leverage over contract terms and lead times. Dual-qualifying second sources lowers but often does not eliminate dependence, as incumbents frequently retain majority share and pricing power.

Specialized equipment and tooling

Precision machining, advanced welding, and radiological systems for BWXT often come from niche OEMs, concentrating supply and giving vendors leverage as capital goods commonly carry lead times of 12–36 months. Limited alternatives and long lead-times let suppliers extract higher margins and tie pricing through bundled spares and multi-year service agreements. BWXT mitigates pressure via lifecycle contracts and targeted in-house capability development to reduce dependence on single-source suppliers.

Cleared, skilled labor as a supplier

Unionized, security-cleared nuclear trades and engineers are scarce, increasing supplier power; tight U.S. labor markets (unemployment ~3.7% in 2024) raise wage pressure and project-scheduling risk. Long training pipelines (apprenticeships often 4–5 years) amplify labor leverage. BWXT invests in apprenticeships and retention to stabilize availability.

- High scarcity: cleared, unionized specialists

- Market tightness: US unemployment ~3.7% (2024)

- Long pipelines: 4–5 year apprenticeships

- BWXT response: apprenticeship and retention investment

Geopolitical and compliance constraints

Export controls (EAR/ITAR), ongoing 2024 sanctions on Russia and Iran, and NRC/DOE qualification rules materially constrain where BWXT can source nuclear-grade materials and equipment, raising lead times and limiting global suppliers.

Compliance overhead concentrates vendors—cleared suppliers capture sourcing share and can demand premiums—while government-facilitated channels for naval programs (NNSA/Navy logistics) partially normalize pricing and contract terms.

- Export controls/EAR/ITAR limit foreign sourcing

- 2024 sanctions (Russia, Iran) restrict supplier pools

- NRC/DOE qualification raises vendor concentration

- Cleared suppliers can extract premiums

- Government channels partially standardize naval procurements

Scarce certified nuclear supplies boost supplier pricing power; buyers use contracts, buffers

Supplier power is high due to few certified HEU/LEU/HALEU and specialty-material vendors, export controls, and long requalification (12–36 months), enabling pricing leverage. BWXT offsets via government-backed long-term contracts and 3–12 month inventory buffers and in-house capability build-out. Labor scarcity (US unemployment ~3.7% in 2024) and unionized, cleared trades further elevate supplier bargaining power.

| Metric | 2024 |

|---|---|

| Requalification lead time | 12–36 months |

| Inventory buffer | 3–12 months |

| US unemployment | ~3.7% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry/substitute risks tailored to BWXT. Identifies disruptive threats, protective barriers, and strategic levers; fully editable Word format for investor materials, strategy decks, or academic use.

A concise one-sheet BWXT Porter's Five Forces snapshot that highlights nuclear supply-chain risks, regulatory pressures, and competitive threats for rapid executive decisions; customizable pressure levels and export-ready visuals simplify inclusion in decks and boardroom briefings.

Customers Bargaining Power

Concentrated government buyers

U.S. Navy/DoD and DOE are the dominant buyers for BWXT, with the DoD FY2024 enacted budget at about $858 billion, creating monopsony dynamics that concentrate negotiating power. Their scale enforces stringent contract terms, compliance and oversight. Mission-critical nuclear and reactor work limits decisions based solely on price, as performance and safety drive awards. Strong performance history can yield sole-source or limited-competition contracts.

Contract structure influence

Cost-plus versus fixed-price contracts shift risk and margin, with customers pushing for fixed-price to cap liabilities while BWXT uses cost-plus where technical uncertainty is high. Customers demand cost transparency and earned-value controls, and BWXT reported a backlog exceeding $6 billion in 2024 supporting such oversight. Incentive fees and penalties heighten execution discipline, and BWXT actively manages its contract mix to balance predictability and upside.

High switching costs for buyers

Nuclear qualification, classified security requirements, and supplier-specific IP create multi-year, costly switching processes that impede buyer mobility. Program risk and certification lead customers to avoid supplier experiments, tempering price pressure even when buyers are concentrated. Sole-source justifications commonly cite these technical and regulatory frictions as the primary rationale.

Budget cycles and political risk

Appropriations timing and continuing resolutions (CRs) disrupt BWXT order flow: FY2024 US defense discretionary funding was about 858 billion, but CRs and shifting priorities force customers to defer or re-scope programs, pressuring pricing and cash. Multi-year contracts provide cushioning but do not remove quarter-to-quarter volatility. BWXT offsets swings by diversifying across defense, DOE, and commercial customers.

- Appropriations timing: causes timing gaps

- CRs: increase order uncertainty

- Deferrals/rescoping: pressure margins and cash

- Multi-year contracts: reduce but not remove volatility

- Diversification: defense, DOE, commercial offsets

Commercial nuclear price sensitivity

Utility customers in competitive wholesale markets such as PJM (serving ~65 million people) and ERCOT push hard on outage services and fuel solutions; nuclear remained a material baseload source in 2024, with U.S. reactors providing roughly 18% of electricity per EIA, increasing buyer price sensitivity and leverage. BWXT defends value via reliability, safety record, and bundled service offerings.

- Buyer leverage: presence of alternative suppliers

- Negotiation focus: outages, fuel solutions

- Market context: PJM ~65M population served

- BWXT defense: reliability, safety, bundled services

Defense nuclear market: monopsony power, big budgets, backlog, earned-value & safety premiums

DoD/DOE monopsony concentrates negotiating power; DoD FY2024 enacted ~$858B. Contract mix (cost-plus vs fixed-price) shifts risk; BWXT reported backlog >$6B in 2024 and customers demand earned-value controls. High qualification/safety and nuclear's ~18% share of US electricity reduce pure price competition.

| Metric | 2024 |

|---|---|

| DoD enacted budget | $858B |

| BWXT backlog | >$6B |

| Nuclear share US electricity | ~18% |

| PJM population | ~65M |

Same Document Delivered

BWXT Porter's Five Forces Analysis

This preview shows the exact BWXT Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The file is professionally formatted and ready for download and use upon payment. It is the full, final deliverable, covering threat of entrants, supplier power, buyer power, substitutes, and competitive rivalry.