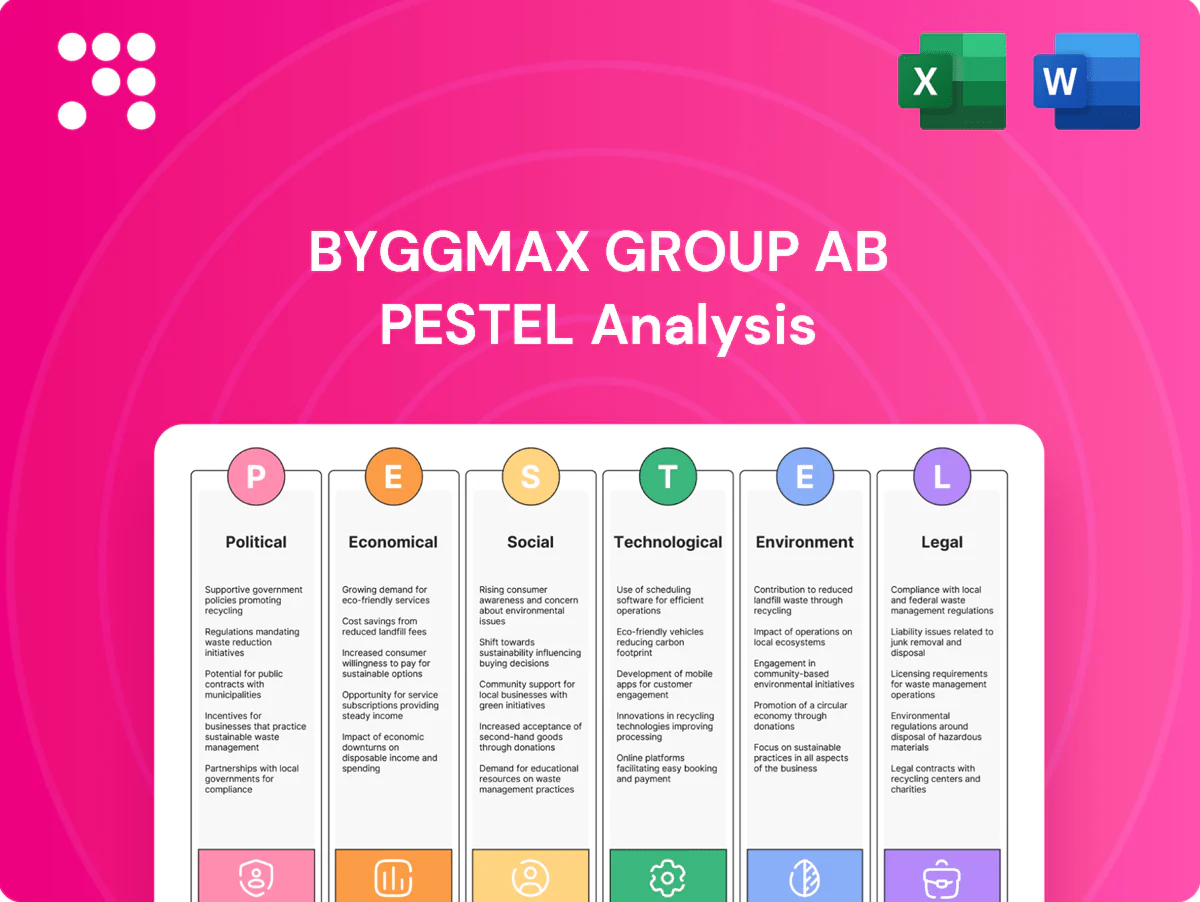

Byggmax Group AB PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Byggmax Group AB — three to five key external forces shaping its market position are examined in depth. Ideal for investors and strategists, it highlights regulatory, economic and environmental risks plus opportunities. Purchase the full report to access the complete, actionable insights.

Political factors

Nordic housing and renovation policies

Government incentives for energy-efficient upgrades can boost demand for insulation, windows and heating materials sold by Byggmax, especially given buildings account for about 40% of EU energy use. Sweden’s climate target of net-zero greenhouse gas emissions by 2045 keeps renovation policy on the agenda, while cuts to subsidies would reduce DIY activity. Municipal permitting lead times shape project starts and store traffic, so monitoring Sweden and neighboring markets’ policy cycles is critical for volume forecasts.

EU trade and customs dynamics

As an EU/EEA-linked retailer, Byggmax is exposed to tariff shifts, anti-dumping measures on steel and wood and sanctions that have historically affected sourcing costs; the EU applies anti-dumping duties and trade remedies case-by-case. Customs frictions and port bottlenecks lengthen lead times and raise safety-stock needs across the single market (EU+EEA). Harmonized standards across the single market ease cross-border procurement, while variable national enforcement adds compliance complexity. The EU’s stable trade framework, including the Common Customs Tariff and ICS2 rollout (phased 2024–2025), reduces pricing and availability volatility.

Public infrastructure and housing programs

Government-funded renovations and housing maintenance, supported by EU and national recovery funds (NextGenerationEU ~€800bn) and Sweden’s ongoing housing initiatives, can boost professional customer demand for aggregates, timber and tools. Budget austerity or election-driven reallocations can swiftly reverse this tailwind. Local authority capex levels determine small civil project volumes. Aligning assortment with funded categories captures incremental share.

Labor market and wage policies

Changes in minimum wages, collective bargaining outcomes and hiring rules materially affect Byggmax store and logistics cost structures; Sweden relies on collective agreements covering about 90% of employees (OECD), so bargaining rounds directly influence labor spend. Flexible scheduling and Working Time Directive constraints affect peak-season efficiency and overtime costs. Political emphasis on apprenticeships and vocational training expands contractor capacity and shifts product mix, while predictable labor policy supports margin planning.

- collective_bargaining_coverage: ~90% (OECD)

- flexible_scheduling: impacts peak-season opex

- apprenticeships: raises contractor capacity, alters product demand

- predictability: aids margin forecasting

Energy and climate policy direction

- Carbon price: €95/t (EU ETS, 2024)

- Subsidies drive new product lines; require training and compliant SKUs

- Policy volatility → demand spikes and supply bottlenecks

EU ~€800bn funds, €95/t carbon price spur Sweden retro; wages ~90%

Political factors: Sweden/EU renovation incentives (NextGenerationEU ~€800bn) and Sweden net-zero by 2045 boost DIY and pro demand; collective bargaining covers ~90% (OECD) raising wage exposure; EU carbon price €95/t (2024) shifts demand to low-carbon products.

| Metric | Value |

|---|---|

| Carbon price | €95/t (2024) |

| Collective coverage | ~90% |

| EU fund | ~€800bn |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces shape Byggmax Group AB’s strategy and operations, providing data-backed trends, industry-specific examples and forward-looking insights to help executives, investors and advisors identify risks and opportunities across Nordic DIY/building retail markets.

A clean, summarized PESTLE of Byggmax Group AB for quick reference in meetings or presentations, visually segmented by category and easily editable so teams can add regional notes, share alignment, and support discussions on external risks and market positioning.

Economic factors

Interest rates and housing cycle

Higher mortgage rates typically slow new-build activity but push homeowners toward renovation, benefiting DIY-focused retailers; Swedish household mortgage rates averaged about 4.5% in 2024. Rate cuts historically revive construction volumes, supporting both pro and consumer segments. Sensitivity varies by category — structural lumber is more cyclical than décor and fittings. Scenario planning across rate paths helps balance inventory and working capital.

Input cost inflation and lumber volatility

Lumber and commodity swings—Random Lengths framing lumber peaked near 1,670 USD/MBF in May 2021 then averaged roughly 400–600 USD/MBF in 2023–24, a >60% move—directly alter ticket sizes and margins for builders' merchants. Rapid cost pass-through risks volume losses while delayed passthrough compresses gross margin. Active hedging and diversified Nordic sourcing reduce shock exposure. Clear, timely price communication sustains value perception.

SEK exchange rate movements

SEK swings directly affect costs for imported tools, fixtures and materials, with EUR/SEK trading around 11.7 in mid‑2025, keeping import costs elevated versus 2022 levels. A weaker SEK raises COGS and may force selective price increases to protect gross margin. Regional sourcing and natural hedges across Nordic suppliers cushion volatility. Transparent, centralized procurement policies help stabilize assortment availability and delivery lead times.

Consumer confidence and real disposable income

DIY demand closely follows household sentiment and real disposable income; Sweden saw weakening consumer confidence through 2024, pressuring mid-ticket home upgrades while wage growth in 2024 supported selective spending on renovations. In downturns, Byggmax defends traffic with promotions and entry-price ranges, while loyalty programs help smooth volatility in repeat purchases.

- DIY tied to sentiment and purchasing power

- Wage growth backs mid-ticket items

- Promos/entry prices defend traffic

- Loyalty smooths repeat sales

Freight, logistics, and fuel costs

Diesel price averaged about €1.70/l in 2024, so diesel and carrier rate swings materially affect last-mile and interstore transfers for Byggmax.

Efficient routing and load optimization protect margins on bulky, low-margin building materials; freight cost volatility hit transport-heavy retail margins in 2024.

Regional distribution centers shorten distances and reduce exposure to distance-driven costs, while click-and-collect shifts volume away from costly home delivery.

- Diesel €1.70/l (2024)

- Carrier rate sensitivity: last-mile & interstore

- Routing/load optimization preserves low-margin SKUs

- Regional DCs + click-and-collect cut delivery spend

EU ~€800bn funds, €95/t carbon price spur Sweden retro; wages ~90%

Higher mortgage rates (Sweden avg 4.5% in 2024) shift demand from new builds to renovations, aiding DIY sales. Lumber volatility (400–600 USD/MBF avg 2023–24) and weaker SEK (EUR/SEK ~11.7 mid‑2025) pressure COGS and margins. Diesel ~€1.70/l in 2024 and freight swings materially affect distribution costs; routing, regional DCs and pricing discipline mitigate impacts.

| Metric | Value/Period |

|---|---|

| Mortgage rate (SE) | 4.5% (2024) |

| Lumber | 400–600 USD/MBF (2023–24 avg) |

| EUR/SEK | ~11.7 (mid‑2025) |

| Diesel | €1.70/l (2024) |

Preview the Actual Deliverable

Byggmax Group AB PESTLE Analysis

This Byggmax Group AB PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The content and structure shown in the preview is the same document you’ll download after payment. No placeholders — the file is ready to use immediately after purchase.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Byggmax Group AB — three to five key external forces shaping its market position are examined in depth. Ideal for investors and strategists, it highlights regulatory, economic and environmental risks plus opportunities. Purchase the full report to access the complete, actionable insights.

Political factors

Nordic housing and renovation policies

Government incentives for energy-efficient upgrades can boost demand for insulation, windows and heating materials sold by Byggmax, especially given buildings account for about 40% of EU energy use. Sweden’s climate target of net-zero greenhouse gas emissions by 2045 keeps renovation policy on the agenda, while cuts to subsidies would reduce DIY activity. Municipal permitting lead times shape project starts and store traffic, so monitoring Sweden and neighboring markets’ policy cycles is critical for volume forecasts.

EU trade and customs dynamics

As an EU/EEA-linked retailer, Byggmax is exposed to tariff shifts, anti-dumping measures on steel and wood and sanctions that have historically affected sourcing costs; the EU applies anti-dumping duties and trade remedies case-by-case. Customs frictions and port bottlenecks lengthen lead times and raise safety-stock needs across the single market (EU+EEA). Harmonized standards across the single market ease cross-border procurement, while variable national enforcement adds compliance complexity. The EU’s stable trade framework, including the Common Customs Tariff and ICS2 rollout (phased 2024–2025), reduces pricing and availability volatility.

Public infrastructure and housing programs

Government-funded renovations and housing maintenance, supported by EU and national recovery funds (NextGenerationEU ~€800bn) and Sweden’s ongoing housing initiatives, can boost professional customer demand for aggregates, timber and tools. Budget austerity or election-driven reallocations can swiftly reverse this tailwind. Local authority capex levels determine small civil project volumes. Aligning assortment with funded categories captures incremental share.

Labor market and wage policies

Changes in minimum wages, collective bargaining outcomes and hiring rules materially affect Byggmax store and logistics cost structures; Sweden relies on collective agreements covering about 90% of employees (OECD), so bargaining rounds directly influence labor spend. Flexible scheduling and Working Time Directive constraints affect peak-season efficiency and overtime costs. Political emphasis on apprenticeships and vocational training expands contractor capacity and shifts product mix, while predictable labor policy supports margin planning.

- collective_bargaining_coverage: ~90% (OECD)

- flexible_scheduling: impacts peak-season opex

- apprenticeships: raises contractor capacity, alters product demand

- predictability: aids margin forecasting

Energy and climate policy direction

- Carbon price: €95/t (EU ETS, 2024)

- Subsidies drive new product lines; require training and compliant SKUs

- Policy volatility → demand spikes and supply bottlenecks

EU ~€800bn funds, €95/t carbon price spur Sweden retro; wages ~90%

Political factors: Sweden/EU renovation incentives (NextGenerationEU ~€800bn) and Sweden net-zero by 2045 boost DIY and pro demand; collective bargaining covers ~90% (OECD) raising wage exposure; EU carbon price €95/t (2024) shifts demand to low-carbon products.

| Metric | Value |

|---|---|

| Carbon price | €95/t (2024) |

| Collective coverage | ~90% |

| EU fund | ~€800bn |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces shape Byggmax Group AB’s strategy and operations, providing data-backed trends, industry-specific examples and forward-looking insights to help executives, investors and advisors identify risks and opportunities across Nordic DIY/building retail markets.

A clean, summarized PESTLE of Byggmax Group AB for quick reference in meetings or presentations, visually segmented by category and easily editable so teams can add regional notes, share alignment, and support discussions on external risks and market positioning.

Economic factors

Interest rates and housing cycle

Higher mortgage rates typically slow new-build activity but push homeowners toward renovation, benefiting DIY-focused retailers; Swedish household mortgage rates averaged about 4.5% in 2024. Rate cuts historically revive construction volumes, supporting both pro and consumer segments. Sensitivity varies by category — structural lumber is more cyclical than décor and fittings. Scenario planning across rate paths helps balance inventory and working capital.

Input cost inflation and lumber volatility

Lumber and commodity swings—Random Lengths framing lumber peaked near 1,670 USD/MBF in May 2021 then averaged roughly 400–600 USD/MBF in 2023–24, a >60% move—directly alter ticket sizes and margins for builders' merchants. Rapid cost pass-through risks volume losses while delayed passthrough compresses gross margin. Active hedging and diversified Nordic sourcing reduce shock exposure. Clear, timely price communication sustains value perception.

SEK exchange rate movements

SEK swings directly affect costs for imported tools, fixtures and materials, with EUR/SEK trading around 11.7 in mid‑2025, keeping import costs elevated versus 2022 levels. A weaker SEK raises COGS and may force selective price increases to protect gross margin. Regional sourcing and natural hedges across Nordic suppliers cushion volatility. Transparent, centralized procurement policies help stabilize assortment availability and delivery lead times.

Consumer confidence and real disposable income

DIY demand closely follows household sentiment and real disposable income; Sweden saw weakening consumer confidence through 2024, pressuring mid-ticket home upgrades while wage growth in 2024 supported selective spending on renovations. In downturns, Byggmax defends traffic with promotions and entry-price ranges, while loyalty programs help smooth volatility in repeat purchases.

- DIY tied to sentiment and purchasing power

- Wage growth backs mid-ticket items

- Promos/entry prices defend traffic

- Loyalty smooths repeat sales

Freight, logistics, and fuel costs

Diesel price averaged about €1.70/l in 2024, so diesel and carrier rate swings materially affect last-mile and interstore transfers for Byggmax.

Efficient routing and load optimization protect margins on bulky, low-margin building materials; freight cost volatility hit transport-heavy retail margins in 2024.

Regional distribution centers shorten distances and reduce exposure to distance-driven costs, while click-and-collect shifts volume away from costly home delivery.

- Diesel €1.70/l (2024)

- Carrier rate sensitivity: last-mile & interstore

- Routing/load optimization preserves low-margin SKUs

- Regional DCs + click-and-collect cut delivery spend

EU ~€800bn funds, €95/t carbon price spur Sweden retro; wages ~90%

Higher mortgage rates (Sweden avg 4.5% in 2024) shift demand from new builds to renovations, aiding DIY sales. Lumber volatility (400–600 USD/MBF avg 2023–24) and weaker SEK (EUR/SEK ~11.7 mid‑2025) pressure COGS and margins. Diesel ~€1.70/l in 2024 and freight swings materially affect distribution costs; routing, regional DCs and pricing discipline mitigate impacts.

| Metric | Value/Period |

|---|---|

| Mortgage rate (SE) | 4.5% (2024) |

| Lumber | 400–600 USD/MBF (2023–24 avg) |

| EUR/SEK | ~11.7 (mid‑2025) |

| Diesel | €1.70/l (2024) |

Preview the Actual Deliverable

Byggmax Group AB PESTLE Analysis

This Byggmax Group AB PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The content and structure shown in the preview is the same document you’ll download after payment. No placeholders — the file is ready to use immediately after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Byggmax Group AB — three to five key external forces shaping its market position are examined in depth. Ideal for investors and strategists, it highlights regulatory, economic and environmental risks plus opportunities. Purchase the full report to access the complete, actionable insights.

Political factors

Nordic housing and renovation policies

Government incentives for energy-efficient upgrades can boost demand for insulation, windows and heating materials sold by Byggmax, especially given buildings account for about 40% of EU energy use. Sweden’s climate target of net-zero greenhouse gas emissions by 2045 keeps renovation policy on the agenda, while cuts to subsidies would reduce DIY activity. Municipal permitting lead times shape project starts and store traffic, so monitoring Sweden and neighboring markets’ policy cycles is critical for volume forecasts.

EU trade and customs dynamics

As an EU/EEA-linked retailer, Byggmax is exposed to tariff shifts, anti-dumping measures on steel and wood and sanctions that have historically affected sourcing costs; the EU applies anti-dumping duties and trade remedies case-by-case. Customs frictions and port bottlenecks lengthen lead times and raise safety-stock needs across the single market (EU+EEA). Harmonized standards across the single market ease cross-border procurement, while variable national enforcement adds compliance complexity. The EU’s stable trade framework, including the Common Customs Tariff and ICS2 rollout (phased 2024–2025), reduces pricing and availability volatility.

Public infrastructure and housing programs

Government-funded renovations and housing maintenance, supported by EU and national recovery funds (NextGenerationEU ~€800bn) and Sweden’s ongoing housing initiatives, can boost professional customer demand for aggregates, timber and tools. Budget austerity or election-driven reallocations can swiftly reverse this tailwind. Local authority capex levels determine small civil project volumes. Aligning assortment with funded categories captures incremental share.

Labor market and wage policies

Changes in minimum wages, collective bargaining outcomes and hiring rules materially affect Byggmax store and logistics cost structures; Sweden relies on collective agreements covering about 90% of employees (OECD), so bargaining rounds directly influence labor spend. Flexible scheduling and Working Time Directive constraints affect peak-season efficiency and overtime costs. Political emphasis on apprenticeships and vocational training expands contractor capacity and shifts product mix, while predictable labor policy supports margin planning.

- collective_bargaining_coverage: ~90% (OECD)

- flexible_scheduling: impacts peak-season opex

- apprenticeships: raises contractor capacity, alters product demand

- predictability: aids margin forecasting

Energy and climate policy direction

- Carbon price: €95/t (EU ETS, 2024)

- Subsidies drive new product lines; require training and compliant SKUs

- Policy volatility → demand spikes and supply bottlenecks

EU ~€800bn funds, €95/t carbon price spur Sweden retro; wages ~90%

Political factors: Sweden/EU renovation incentives (NextGenerationEU ~€800bn) and Sweden net-zero by 2045 boost DIY and pro demand; collective bargaining covers ~90% (OECD) raising wage exposure; EU carbon price €95/t (2024) shifts demand to low-carbon products.

| Metric | Value |

|---|---|

| Carbon price | €95/t (2024) |

| Collective coverage | ~90% |

| EU fund | ~€800bn |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental and Legal forces shape Byggmax Group AB’s strategy and operations, providing data-backed trends, industry-specific examples and forward-looking insights to help executives, investors and advisors identify risks and opportunities across Nordic DIY/building retail markets.

A clean, summarized PESTLE of Byggmax Group AB for quick reference in meetings or presentations, visually segmented by category and easily editable so teams can add regional notes, share alignment, and support discussions on external risks and market positioning.

Economic factors

Interest rates and housing cycle

Higher mortgage rates typically slow new-build activity but push homeowners toward renovation, benefiting DIY-focused retailers; Swedish household mortgage rates averaged about 4.5% in 2024. Rate cuts historically revive construction volumes, supporting both pro and consumer segments. Sensitivity varies by category — structural lumber is more cyclical than décor and fittings. Scenario planning across rate paths helps balance inventory and working capital.

Input cost inflation and lumber volatility

Lumber and commodity swings—Random Lengths framing lumber peaked near 1,670 USD/MBF in May 2021 then averaged roughly 400–600 USD/MBF in 2023–24, a >60% move—directly alter ticket sizes and margins for builders' merchants. Rapid cost pass-through risks volume losses while delayed passthrough compresses gross margin. Active hedging and diversified Nordic sourcing reduce shock exposure. Clear, timely price communication sustains value perception.

SEK exchange rate movements

SEK swings directly affect costs for imported tools, fixtures and materials, with EUR/SEK trading around 11.7 in mid‑2025, keeping import costs elevated versus 2022 levels. A weaker SEK raises COGS and may force selective price increases to protect gross margin. Regional sourcing and natural hedges across Nordic suppliers cushion volatility. Transparent, centralized procurement policies help stabilize assortment availability and delivery lead times.

Consumer confidence and real disposable income

DIY demand closely follows household sentiment and real disposable income; Sweden saw weakening consumer confidence through 2024, pressuring mid-ticket home upgrades while wage growth in 2024 supported selective spending on renovations. In downturns, Byggmax defends traffic with promotions and entry-price ranges, while loyalty programs help smooth volatility in repeat purchases.

- DIY tied to sentiment and purchasing power

- Wage growth backs mid-ticket items

- Promos/entry prices defend traffic

- Loyalty smooths repeat sales

Freight, logistics, and fuel costs

Diesel price averaged about €1.70/l in 2024, so diesel and carrier rate swings materially affect last-mile and interstore transfers for Byggmax.

Efficient routing and load optimization protect margins on bulky, low-margin building materials; freight cost volatility hit transport-heavy retail margins in 2024.

Regional distribution centers shorten distances and reduce exposure to distance-driven costs, while click-and-collect shifts volume away from costly home delivery.

- Diesel €1.70/l (2024)

- Carrier rate sensitivity: last-mile & interstore

- Routing/load optimization preserves low-margin SKUs

- Regional DCs + click-and-collect cut delivery spend

EU ~€800bn funds, €95/t carbon price spur Sweden retro; wages ~90%

Higher mortgage rates (Sweden avg 4.5% in 2024) shift demand from new builds to renovations, aiding DIY sales. Lumber volatility (400–600 USD/MBF avg 2023–24) and weaker SEK (EUR/SEK ~11.7 mid‑2025) pressure COGS and margins. Diesel ~€1.70/l in 2024 and freight swings materially affect distribution costs; routing, regional DCs and pricing discipline mitigate impacts.

| Metric | Value/Period |

|---|---|

| Mortgage rate (SE) | 4.5% (2024) |

| Lumber | 400–600 USD/MBF (2023–24 avg) |

| EUR/SEK | ~11.7 (mid‑2025) |

| Diesel | €1.70/l (2024) |

Preview the Actual Deliverable

Byggmax Group AB PESTLE Analysis

This Byggmax Group AB PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The content and structure shown in the preview is the same document you’ll download after payment. No placeholders — the file is ready to use immediately after purchase.