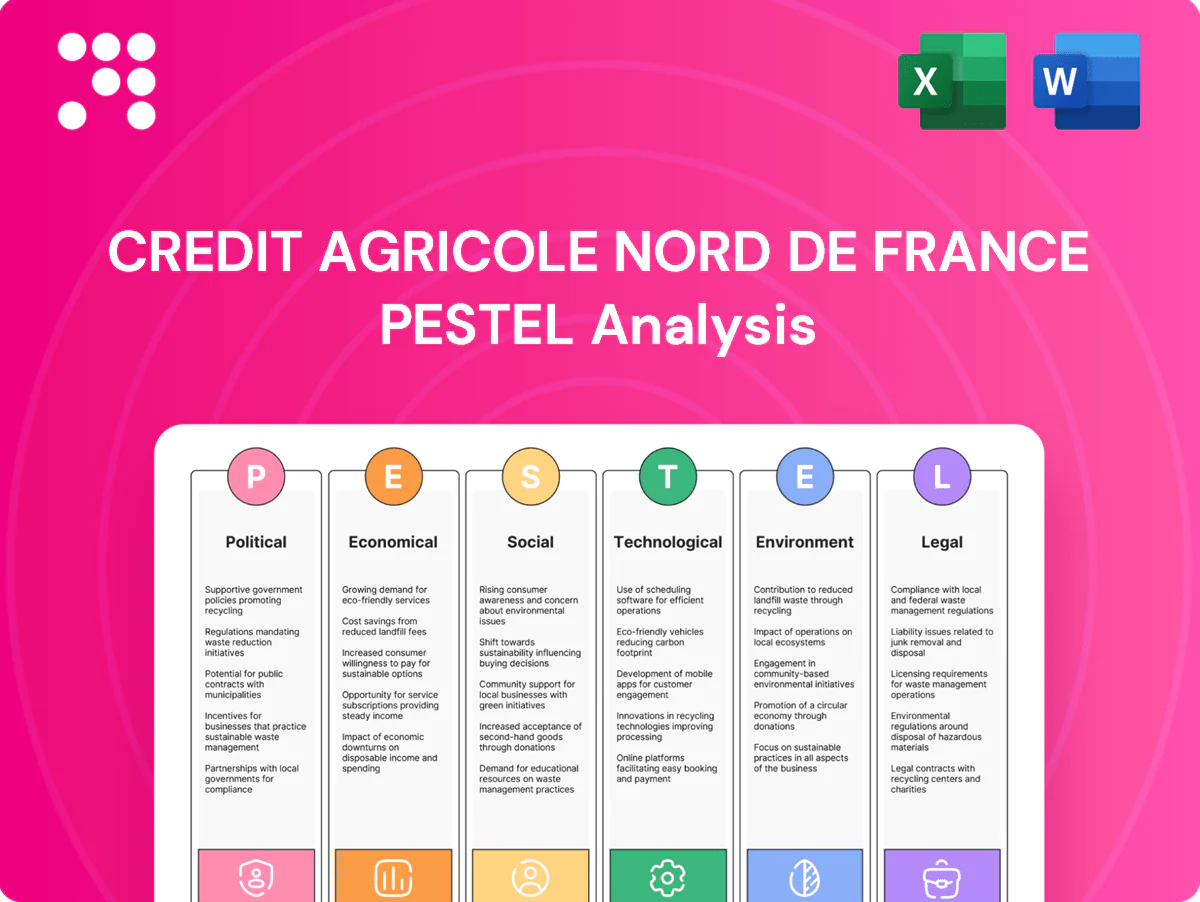

Credit Agricole Nord de France PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE analysis for Credit Agricole Nord de France reveals how political shifts, economic cycles, social trends, technological innovation, legal changes, and environmental risks converge to shape strategy and performance. Use these insights to anticipate risks and spot growth areas. Purchase the full report for actionable, downloadable intelligence now.

Political factors

EU and French banking policy direction

Shifts in EU and French policy — under ECB supervision of 114 significant institutions covering about 82% of euro-area banking assets (2024) — directly influence capital, liquidity and lending priorities for regional banks. Changes in state support, including the France 2030 plan (€54 billion through 2025), can alter funding and incentives for cooperatives. Active monitoring of policy signals lets the bank adjust balance-sheet composition and product mix, while stable governance underpins its cooperative mission.

Agricultural and CAP subsidy dynamics

Revisions to the EU Common Agricultural Policy (CAP) — budgeted at €386.6 billion for 2021–27 — materially affect farm incomes and thus Credit Agricole Nord de France’s agri loan demand and asset quality; timing and eligibility of CAP payments drive seasonal cash flows and collateral strength. Advisory services and tailored lending products help smooth volatility, while client diversification lowers sector concentration risk.

Regional development and public investment

Local government projects in Hauts-de-France boost SME activity and housing/infrastructure finance demand, aligning with national France Relance public investment of €100bn that channels regional grants and guarantees. Participation in public-private initiatives increases Crédit Agricole Nord de France fee income and community impact through co-financing and PPPs. Policy-led regeneration can reprioritise branch footprints toward growth zones; political turnover may rapidly alter project pipelines and funding timelines.

Geopolitical risk and sanctions exposure

Geopolitical sanctions since 2022 have disrupted exporters in Nord de France, increasing demand for bank trade services and tighter screening during volatile periods.

Supply-chain shifts raise working-capital and FX needs, while Crédit Agricole Nord de France maintains conservative risk governance to protect reputation and capital.

- Sanctions: heightened screening

- Compliance: rising operational burden

- Liquidity: higher WC and FX demand

Political expectations of cooperative banking

Authorities and stakeholders expect cooperative banks like Crédit Agricole Nord de France to foster inclusion and local resilience, with Crédit Agricole Group reporting roughly €2.2 trillion in total assets in 2024 highlighting systemic relevance. Political pressure may rise to maintain SME and household credit in downturns; balancing prudence with mission requires a clear risk appetite, active member engagement and ACPR-aligned governance. Transparent impact reporting sustains the cooperative mandate.

- Inclusion/local resilience

- Downturn credit preservation

- Clear risk appetite & member engagement

- Transparent impact reporting

ECB tightening raises capital and liquidity pressure on major French regional bank

ECB supervision of 114 significant banks covering ~82% of euro-area banking assets (2024) tightens capital/liquidity expectations for Crédit Agricole Nord de France. France 2030 (€54bn to 2025) and France Relance (€100bn) shift regional funding and SME demand. CAP budget €386.6bn (2021–27) directly affects agri loan quality and seasonality.

| Metric | Value |

|---|---|

| ECB scope | 114 banks / ~82% assets (2024) |

| France 2030 | €54bn to 2025 |

| France Relance | €100bn |

| CAP | €386.6bn (2021–27) |

| CA Group assets | €2.2tn (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Crédit Agricole Nord de France, with data-driven insights and regional regulatory context. Designed for executives and advisors, the analysis highlights risks, opportunities and forward-looking scenarios to inform strategy and funding decisions.

A concise PESTLE snapshot for Crédit Agricole Nord de France that distills regulatory, economic, social, technological, environmental and political impacts into an easily shareable slide or briefing, enabling quick risk assessment, team alignment and customizable notes for regional or business-line decisions.

Economic factors

ECB rate cycle and net interest margin

ECB policy tightened from -0.50% in 2021 to around 4.0% by 2024–25 (≈450bp), driving deposit betas, loan repricing and net interest margin for Ca Nord de France; rapid pivots can compress NIM or reprice credit risk unevenly across retail and corporate portfolios. Interest‑rate risk management and product mix are pivotal, while hedging and frequent sensitivity monitoring mitigate shocks.

Regional growth and employment trends

Economic health in Hauts-de-France directs mortgage, SME loan and insurance demand as regional GDP growth was around 0.9% annualized in 2023–24, while unemployment stood at about 8.7% in 2024 versus the national 7.6% (INSEE), pressuring arrears and provisioning. Heavy exposure to industry, logistics and agriculture—roughly 30% of jobs—adds cyclicality. Granular local data enables targeted underwriting, outreach and relief measures to limit losses.

Housing market and real estate finance

Price dynamics and subdued construction — France had roughly €1.3tn outstanding residential mortgages at end-2023 — directly drive mortgage volumes and lift LTV risk as valuations shift.

Regulatory affordability tests tightened in 2024 cap originations during higher-rate phases, reducing new loan flow and average ticket size.

Diversified fees from brokerage and insurance (often 1–2% of loan value) stabilize income while strict collateral valuation policies limit LGD.

SME liquidity and export conditions

SME working capital needs shift quickly with input-cost swings, inventory build-ups and trade-flow disruptions; EU SMEs represent 99.8% of firms and provide about 66.6% of employment (Eurostat), amplifying systemic liquidity risk for Crédit Agricole Nord de France’s client base. Exporters face FX, demand and compliance frictions, while tailored credit lines and guarantees (public-private schemes) and payment-data trends feed early-warning systems.

- Working capital: input costs + inventories

- Exports: FX, demand, compliance

- Support: tailored credit lines/guarantees

- Signals: payment behavior → early warnings

Inflation and household savings behavior

Inflation (French CPI averaged 3.0% in 2024) shifts household allocations from sight and term deposits toward investment products, while the household gross saving rate (~13% in 2024) signals constrained buffers and higher fee sensitivity and churn as real incomes tighten.

- Indexed pricing to CPI protects margins

- Cost discipline critical as NIMs compress

- Advisory on protection/budgeting deepens customer ties

ECB tightening raises capital and liquidity pressure on major French regional bank

ECB rate jump to ~4.0% (2024–25) raised deposit betas and repriced loans, affecting NIM and affordability; Hauts‑de‑France GDP ~0.9% (2023–24) and unemployment 8.7% (2024) heighten credit risk; €1.3tn residential mortgages (end‑2023) and tighter 2024 affordability tests curb originations; CPI ~3.0% and 13% household saving (2024) shift deposits to investments.

| Metric | Value |

|---|---|

| ECB rate | ~4.0% |

| Hauts‑de‑France GDP | 0.9% |

| Unemployment | 8.7% |

| Residential mortgages | €1.3tn |

Same Document Delivered

Credit Agricole Nord de France PESTLE Analysis

This Credit Agricole Nord de France PESTLE Analysis presents a concise examination of political, economic, social, technological, legal, and environmental factors affecting the bank; the preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes actionable insights and structured findings for strategy and risk assessment. No placeholders—this is the final, downloadable file.

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE analysis for Credit Agricole Nord de France reveals how political shifts, economic cycles, social trends, technological innovation, legal changes, and environmental risks converge to shape strategy and performance. Use these insights to anticipate risks and spot growth areas. Purchase the full report for actionable, downloadable intelligence now.

Political factors

EU and French banking policy direction

Shifts in EU and French policy — under ECB supervision of 114 significant institutions covering about 82% of euro-area banking assets (2024) — directly influence capital, liquidity and lending priorities for regional banks. Changes in state support, including the France 2030 plan (€54 billion through 2025), can alter funding and incentives for cooperatives. Active monitoring of policy signals lets the bank adjust balance-sheet composition and product mix, while stable governance underpins its cooperative mission.

Agricultural and CAP subsidy dynamics

Revisions to the EU Common Agricultural Policy (CAP) — budgeted at €386.6 billion for 2021–27 — materially affect farm incomes and thus Credit Agricole Nord de France’s agri loan demand and asset quality; timing and eligibility of CAP payments drive seasonal cash flows and collateral strength. Advisory services and tailored lending products help smooth volatility, while client diversification lowers sector concentration risk.

Regional development and public investment

Local government projects in Hauts-de-France boost SME activity and housing/infrastructure finance demand, aligning with national France Relance public investment of €100bn that channels regional grants and guarantees. Participation in public-private initiatives increases Crédit Agricole Nord de France fee income and community impact through co-financing and PPPs. Policy-led regeneration can reprioritise branch footprints toward growth zones; political turnover may rapidly alter project pipelines and funding timelines.

Geopolitical risk and sanctions exposure

Geopolitical sanctions since 2022 have disrupted exporters in Nord de France, increasing demand for bank trade services and tighter screening during volatile periods.

Supply-chain shifts raise working-capital and FX needs, while Crédit Agricole Nord de France maintains conservative risk governance to protect reputation and capital.

- Sanctions: heightened screening

- Compliance: rising operational burden

- Liquidity: higher WC and FX demand

Political expectations of cooperative banking

Authorities and stakeholders expect cooperative banks like Crédit Agricole Nord de France to foster inclusion and local resilience, with Crédit Agricole Group reporting roughly €2.2 trillion in total assets in 2024 highlighting systemic relevance. Political pressure may rise to maintain SME and household credit in downturns; balancing prudence with mission requires a clear risk appetite, active member engagement and ACPR-aligned governance. Transparent impact reporting sustains the cooperative mandate.

- Inclusion/local resilience

- Downturn credit preservation

- Clear risk appetite & member engagement

- Transparent impact reporting

ECB tightening raises capital and liquidity pressure on major French regional bank

ECB supervision of 114 significant banks covering ~82% of euro-area banking assets (2024) tightens capital/liquidity expectations for Crédit Agricole Nord de France. France 2030 (€54bn to 2025) and France Relance (€100bn) shift regional funding and SME demand. CAP budget €386.6bn (2021–27) directly affects agri loan quality and seasonality.

| Metric | Value |

|---|---|

| ECB scope | 114 banks / ~82% assets (2024) |

| France 2030 | €54bn to 2025 |

| France Relance | €100bn |

| CAP | €386.6bn (2021–27) |

| CA Group assets | €2.2tn (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Crédit Agricole Nord de France, with data-driven insights and regional regulatory context. Designed for executives and advisors, the analysis highlights risks, opportunities and forward-looking scenarios to inform strategy and funding decisions.

A concise PESTLE snapshot for Crédit Agricole Nord de France that distills regulatory, economic, social, technological, environmental and political impacts into an easily shareable slide or briefing, enabling quick risk assessment, team alignment and customizable notes for regional or business-line decisions.

Economic factors

ECB rate cycle and net interest margin

ECB policy tightened from -0.50% in 2021 to around 4.0% by 2024–25 (≈450bp), driving deposit betas, loan repricing and net interest margin for Ca Nord de France; rapid pivots can compress NIM or reprice credit risk unevenly across retail and corporate portfolios. Interest‑rate risk management and product mix are pivotal, while hedging and frequent sensitivity monitoring mitigate shocks.

Regional growth and employment trends

Economic health in Hauts-de-France directs mortgage, SME loan and insurance demand as regional GDP growth was around 0.9% annualized in 2023–24, while unemployment stood at about 8.7% in 2024 versus the national 7.6% (INSEE), pressuring arrears and provisioning. Heavy exposure to industry, logistics and agriculture—roughly 30% of jobs—adds cyclicality. Granular local data enables targeted underwriting, outreach and relief measures to limit losses.

Housing market and real estate finance

Price dynamics and subdued construction — France had roughly €1.3tn outstanding residential mortgages at end-2023 — directly drive mortgage volumes and lift LTV risk as valuations shift.

Regulatory affordability tests tightened in 2024 cap originations during higher-rate phases, reducing new loan flow and average ticket size.

Diversified fees from brokerage and insurance (often 1–2% of loan value) stabilize income while strict collateral valuation policies limit LGD.

SME liquidity and export conditions

SME working capital needs shift quickly with input-cost swings, inventory build-ups and trade-flow disruptions; EU SMEs represent 99.8% of firms and provide about 66.6% of employment (Eurostat), amplifying systemic liquidity risk for Crédit Agricole Nord de France’s client base. Exporters face FX, demand and compliance frictions, while tailored credit lines and guarantees (public-private schemes) and payment-data trends feed early-warning systems.

- Working capital: input costs + inventories

- Exports: FX, demand, compliance

- Support: tailored credit lines/guarantees

- Signals: payment behavior → early warnings

Inflation and household savings behavior

Inflation (French CPI averaged 3.0% in 2024) shifts household allocations from sight and term deposits toward investment products, while the household gross saving rate (~13% in 2024) signals constrained buffers and higher fee sensitivity and churn as real incomes tighten.

- Indexed pricing to CPI protects margins

- Cost discipline critical as NIMs compress

- Advisory on protection/budgeting deepens customer ties

ECB tightening raises capital and liquidity pressure on major French regional bank

ECB rate jump to ~4.0% (2024–25) raised deposit betas and repriced loans, affecting NIM and affordability; Hauts‑de‑France GDP ~0.9% (2023–24) and unemployment 8.7% (2024) heighten credit risk; €1.3tn residential mortgages (end‑2023) and tighter 2024 affordability tests curb originations; CPI ~3.0% and 13% household saving (2024) shift deposits to investments.

| Metric | Value |

|---|---|

| ECB rate | ~4.0% |

| Hauts‑de‑France GDP | 0.9% |

| Unemployment | 8.7% |

| Residential mortgages | €1.3tn |

Same Document Delivered

Credit Agricole Nord de France PESTLE Analysis

This Credit Agricole Nord de France PESTLE Analysis presents a concise examination of political, economic, social, technological, legal, and environmental factors affecting the bank; the preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes actionable insights and structured findings for strategy and risk assessment. No placeholders—this is the final, downloadable file.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE analysis for Credit Agricole Nord de France reveals how political shifts, economic cycles, social trends, technological innovation, legal changes, and environmental risks converge to shape strategy and performance. Use these insights to anticipate risks and spot growth areas. Purchase the full report for actionable, downloadable intelligence now.

Political factors

EU and French banking policy direction

Shifts in EU and French policy — under ECB supervision of 114 significant institutions covering about 82% of euro-area banking assets (2024) — directly influence capital, liquidity and lending priorities for regional banks. Changes in state support, including the France 2030 plan (€54 billion through 2025), can alter funding and incentives for cooperatives. Active monitoring of policy signals lets the bank adjust balance-sheet composition and product mix, while stable governance underpins its cooperative mission.

Agricultural and CAP subsidy dynamics

Revisions to the EU Common Agricultural Policy (CAP) — budgeted at €386.6 billion for 2021–27 — materially affect farm incomes and thus Credit Agricole Nord de France’s agri loan demand and asset quality; timing and eligibility of CAP payments drive seasonal cash flows and collateral strength. Advisory services and tailored lending products help smooth volatility, while client diversification lowers sector concentration risk.

Regional development and public investment

Local government projects in Hauts-de-France boost SME activity and housing/infrastructure finance demand, aligning with national France Relance public investment of €100bn that channels regional grants and guarantees. Participation in public-private initiatives increases Crédit Agricole Nord de France fee income and community impact through co-financing and PPPs. Policy-led regeneration can reprioritise branch footprints toward growth zones; political turnover may rapidly alter project pipelines and funding timelines.

Geopolitical risk and sanctions exposure

Geopolitical sanctions since 2022 have disrupted exporters in Nord de France, increasing demand for bank trade services and tighter screening during volatile periods.

Supply-chain shifts raise working-capital and FX needs, while Crédit Agricole Nord de France maintains conservative risk governance to protect reputation and capital.

- Sanctions: heightened screening

- Compliance: rising operational burden

- Liquidity: higher WC and FX demand

Political expectations of cooperative banking

Authorities and stakeholders expect cooperative banks like Crédit Agricole Nord de France to foster inclusion and local resilience, with Crédit Agricole Group reporting roughly €2.2 trillion in total assets in 2024 highlighting systemic relevance. Political pressure may rise to maintain SME and household credit in downturns; balancing prudence with mission requires a clear risk appetite, active member engagement and ACPR-aligned governance. Transparent impact reporting sustains the cooperative mandate.

- Inclusion/local resilience

- Downturn credit preservation

- Clear risk appetite & member engagement

- Transparent impact reporting

ECB tightening raises capital and liquidity pressure on major French regional bank

ECB supervision of 114 significant banks covering ~82% of euro-area banking assets (2024) tightens capital/liquidity expectations for Crédit Agricole Nord de France. France 2030 (€54bn to 2025) and France Relance (€100bn) shift regional funding and SME demand. CAP budget €386.6bn (2021–27) directly affects agri loan quality and seasonality.

| Metric | Value |

|---|---|

| ECB scope | 114 banks / ~82% assets (2024) |

| France 2030 | €54bn to 2025 |

| France Relance | €100bn |

| CAP | €386.6bn (2021–27) |

| CA Group assets | €2.2tn (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Crédit Agricole Nord de France, with data-driven insights and regional regulatory context. Designed for executives and advisors, the analysis highlights risks, opportunities and forward-looking scenarios to inform strategy and funding decisions.

A concise PESTLE snapshot for Crédit Agricole Nord de France that distills regulatory, economic, social, technological, environmental and political impacts into an easily shareable slide or briefing, enabling quick risk assessment, team alignment and customizable notes for regional or business-line decisions.

Economic factors

ECB rate cycle and net interest margin

ECB policy tightened from -0.50% in 2021 to around 4.0% by 2024–25 (≈450bp), driving deposit betas, loan repricing and net interest margin for Ca Nord de France; rapid pivots can compress NIM or reprice credit risk unevenly across retail and corporate portfolios. Interest‑rate risk management and product mix are pivotal, while hedging and frequent sensitivity monitoring mitigate shocks.

Regional growth and employment trends

Economic health in Hauts-de-France directs mortgage, SME loan and insurance demand as regional GDP growth was around 0.9% annualized in 2023–24, while unemployment stood at about 8.7% in 2024 versus the national 7.6% (INSEE), pressuring arrears and provisioning. Heavy exposure to industry, logistics and agriculture—roughly 30% of jobs—adds cyclicality. Granular local data enables targeted underwriting, outreach and relief measures to limit losses.

Housing market and real estate finance

Price dynamics and subdued construction — France had roughly €1.3tn outstanding residential mortgages at end-2023 — directly drive mortgage volumes and lift LTV risk as valuations shift.

Regulatory affordability tests tightened in 2024 cap originations during higher-rate phases, reducing new loan flow and average ticket size.

Diversified fees from brokerage and insurance (often 1–2% of loan value) stabilize income while strict collateral valuation policies limit LGD.

SME liquidity and export conditions

SME working capital needs shift quickly with input-cost swings, inventory build-ups and trade-flow disruptions; EU SMEs represent 99.8% of firms and provide about 66.6% of employment (Eurostat), amplifying systemic liquidity risk for Crédit Agricole Nord de France’s client base. Exporters face FX, demand and compliance frictions, while tailored credit lines and guarantees (public-private schemes) and payment-data trends feed early-warning systems.

- Working capital: input costs + inventories

- Exports: FX, demand, compliance

- Support: tailored credit lines/guarantees

- Signals: payment behavior → early warnings

Inflation and household savings behavior

Inflation (French CPI averaged 3.0% in 2024) shifts household allocations from sight and term deposits toward investment products, while the household gross saving rate (~13% in 2024) signals constrained buffers and higher fee sensitivity and churn as real incomes tighten.

- Indexed pricing to CPI protects margins

- Cost discipline critical as NIMs compress

- Advisory on protection/budgeting deepens customer ties

ECB tightening raises capital and liquidity pressure on major French regional bank

ECB rate jump to ~4.0% (2024–25) raised deposit betas and repriced loans, affecting NIM and affordability; Hauts‑de‑France GDP ~0.9% (2023–24) and unemployment 8.7% (2024) heighten credit risk; €1.3tn residential mortgages (end‑2023) and tighter 2024 affordability tests curb originations; CPI ~3.0% and 13% household saving (2024) shift deposits to investments.

| Metric | Value |

|---|---|

| ECB rate | ~4.0% |

| Hauts‑de‑France GDP | 0.9% |

| Unemployment | 8.7% |

| Residential mortgages | €1.3tn |

Same Document Delivered

Credit Agricole Nord de France PESTLE Analysis

This Credit Agricole Nord de France PESTLE Analysis presents a concise examination of political, economic, social, technological, legal, and environmental factors affecting the bank; the preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes actionable insights and structured findings for strategy and risk assessment. No placeholders—this is the final, downloadable file.