Cadre Holdings PESTLE Analysis

Your Competitive Advantage Starts with This Report

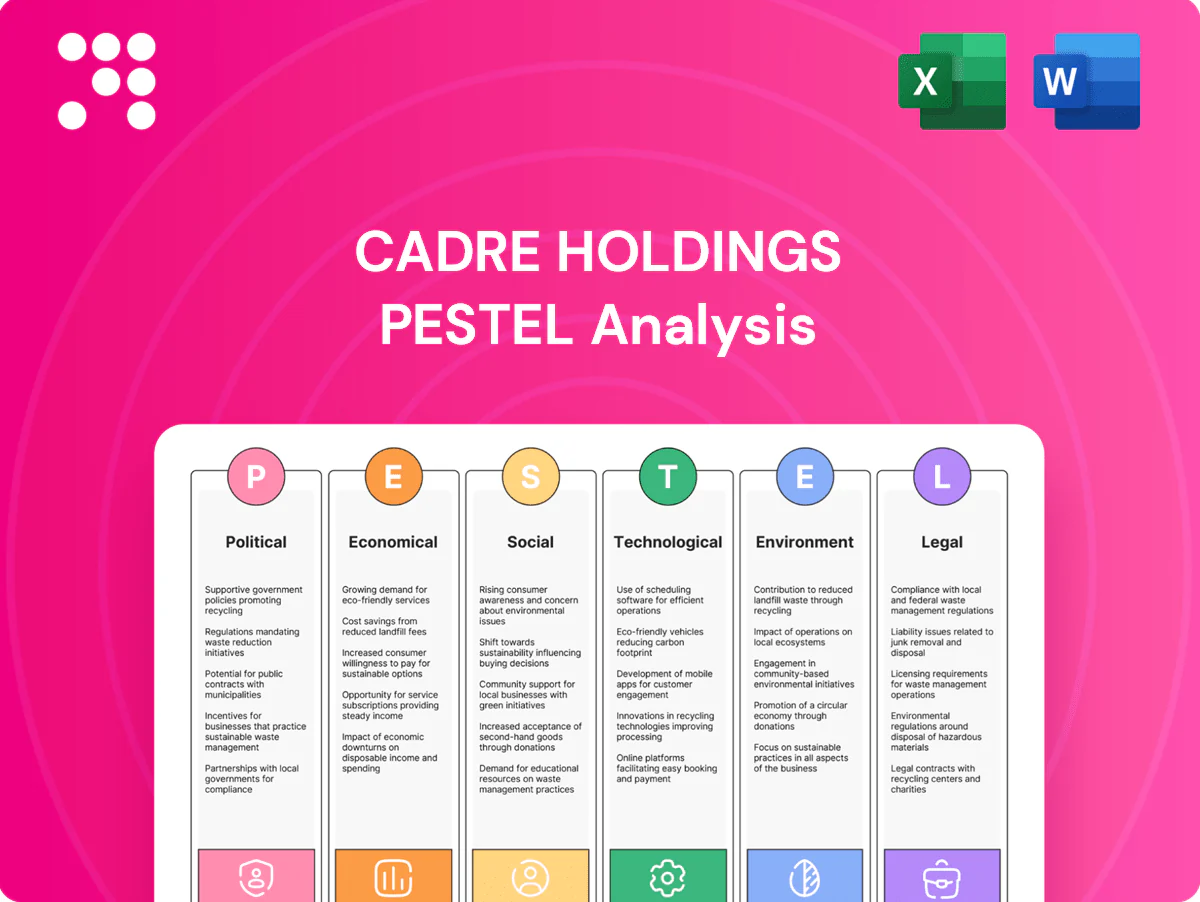

Unlock strategic clarity with our PESTLE Analysis of Cadre Holdings—three concise chapters reveal how political shifts, economic cycles, and tech trends are reshaping its prospects. Ideal for investors and strategists seeking actionable foresight. Purchase the full report for the complete, editable breakdown and immediate insights.

Political factors

Defense budgets and procurement cycles

Government spending priorities directly shape demand for body armor, EOD tools and duty gear; global military expenditure reached 2.24 trillion USD in 2023 (SIPRI), so shifts in allocations materially affect order books. Election cycles, fiscal deficits and supplemental appropriations can accelerate or delay orders, while multi‑year procurement programs improve visibility but may be rebaselined with policy shifts. Diversifying across agencies and countries reduces single‑budget exposure.

Geopolitical tensions and conflict intensity

Geopolitical tensions and higher conflict intensity drive urgent procurement spikes — global military expenditure reached about 2.24 trillion USD in 2023 and the US defense budget was roughly 858 billion USD in 2024, lifting demand and order volumes for suppliers like Cadre Holdings. Periods of détente compress order flow and revenue visibility. Sanctions and shifting alliances restrict market access regionally. Rigorous scenario planning is needed to match production capacity to volatile demand.

Export controls and foreign policy alignment

Access to international customers for Cadre Holdings depends on home‑country export licenses and end‑use restrictions, with US and allied controls tightened for advanced technologies during 2022–2024 and continuing into 2025. Policy shifts can abruptly close or open markets, as seen when 2024 semiconductor export rules reshaped buyer eligibility. Strong compliance processes protect continuity of approvals and limit revenue disruption. Building relationships with vetted, compliant distributors mitigates license risk.

Public safety policy and policing reforms

Legislative reforms since 2023 have shifted equipment standards, permissible use, and funding, with federal COPS and Byrne-style grants and related programs dispersing roughly $1.1 billion to local agencies in 2024, boosting purchasing power for protective gear. Body armor mandates in several states increased procurement, while bans or restrictions on crowd-control gear have reduced demand for those lines. Cadre Holdings’ participation in NIJ and ASTM committees helps anticipate standards and capture demand shifts.

- Grants 2024 ≈ $1.1B (federal COPS/Byrne)

- Body armor mandate states: procurement uptick

- Restrictions curb crowd-control equipment sales

- Standards committee engagement = early signal

Trade policy, tariffs, and reshoring incentives

Tariffs on textiles, composites and electronics (Section 301 rates up to 25%) materially raise Cadre Holdings input costs and force price pass‑through; US industrial policy — CHIPS Act $52B and IRA $369B — plus state reshoring grants support domestic manufacturing investment. Customs bottlenecks (port dwell times spiking to >6 days in 2021–22) and geopolitical friction can halt cross‑border supply, so flexible multi‑source strategies hedge policy swings.

- Tariffs: up to 25% on key inputs

- Reshoring: CHIPS $52B; IRA $369B

- Customs risk: port dwell >6 days peak

- Mitigation: diversified sourcing, nearshoring

Procurement volatility, trade curbs 2.24T US ≈858B

Government budgets and election cycles drive order timing; global military spend was 2.24T USD in 2023 and US defense ≈858B USD in 2024, so procurement volatility affects Cadre’s revenue visibility. Export controls, tariffs (up to 25%) and grants ($1.1B COPS/Byrne 2024) reshape market access and sourcing. Active standards engagement and multi‑source supply reduce policy risk.

| Metric | Value |

|---|---|

| Global mil. spend 2023 | 2.24T USD |

| US defense 2024 | ≈858B USD |

| Federal grants 2024 | ≈1.1B USD |

| Tariffs | Up to 25% |

What is included in the product

Provides a concise PESTLE review of how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Cadre Holdings, grounded in current market and regulatory data. Designed for executives and investors, it highlights risks, opportunities and forward‑looking scenarios ready for reports or decks.

A concise, visually segmented Cadre Holdings PESTLE summary that relieves planning friction by highlighting key political, economic, social, technological, legal and environmental risks at a glance for meeting use. Easily shareable and editable, it supports quick alignment across teams, client reports, and strategic discussions on external risk and market positioning.

Economic factors

Macroeconomic cycles and budget constraints

Recessions squeeze tax revenues, constraining public safety and defense budgets and forcing re-prioritization of spending; global military expenditure still rose to about 2.24 trillion USD in 2023 (SIPRI). Conversely, fiscal stimulus or security-focused appropriations often offset downturns. Commercial demand for private security tracks broader business activity and trade volumes. A resilient mix of end-markets smooths cyclical exposure for Cadre Holdings.

Inflation, input costs, and pricing power

Aramid fibers, ceramics and specialty metals are highly sensitive to commodity and energy swings; Brent crude averaged about $85/bbl in 2024 and U.S. CPI rose 3.4% (BLS, 2024). Contract structures that limit pass‑through risk compressing margins. Indexing and strategic sourcing can protect profitability. Continuous value engineering preserves affordability and performance.

Foreign exchange and global revenue mix

Multi‑currency sales expose Cadre Holdings earnings to FX volatility, especially with the US dollar trading near a DXY of about 106 in July 2025, which amplifies translation risk for foreign revenue streams. Robust hedging policies and shifting production locally have been shown to curb both transaction and translation shocks. Dollar strength can erode overseas competitiveness, so pricing strategies must reflect currency dynamics and pass‑through limits to protect margins.

Supply chain resilience and lead times

Disruptions in advanced materials and electronics extended lead times—semiconductor lead times peaked near 26 weeks in 2021 and averaged about 14 weeks by 2024—pressuring Cadre Holdings delivery schedules. Dual sourcing and inventory buffers raise on‑time rates and resilience. Vendor qualification and nearshoring cut geopolitical and logistics risk while transparent lead‑time communication sustains customer trust.

- 26w peak (2021); ~14w avg (2024)

- Dual sourcing + buffers = higher reliability

- Nearshoring reduces geopolitical/logistics exposure

- Clear lead‑time updates sustain trust

Scale economies and operating leverage

Batch production and shared components reduce Cadre Holdings unit costs, raising gross margins as volumes grow while making profits more sensitive to demand swings; modular designs boost throughput flexibility and shorten changeover times; disciplined cost control and fixed-cost management stabilize earnings across cycles.

- scale-economies

- operating-leverage

- modularity

- cost-discipline

Procurement volatility, trade curbs 2.24T US ≈858B

Global military spend rose to ~2.24 trillion USD in 2023, supporting steady defense orders; recessions compress tax revenues and reprioritize spending. Brent averaged ~85 USD/bbl in 2024 and US CPI was 3.4% (BLS 2024), pressuring input costs and margins. DXY ~106 (Jul 2025) heightens FX translation risk; semiconductor lead times averaged ~14 weeks in 2024, straining delivery.

| Metric | Value |

|---|---|

| Military spend (2023) | 2.24T USD |

| Brent (2024 avg) | ~85 USD/bbl |

| US CPI (2024) | 3.4% |

| DXY (Jul 2025) | ~106 |

| Semiconductor lead time (2024) | ~14 wks |

What You See Is What You Get

Cadre Holdings PESTLE Analysis

The preview shown here is the exact Cadre Holdings PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with complete content and structure, not a placeholder. After checkout you’ll instantly download the exact document displayed here.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Cadre Holdings—three concise chapters reveal how political shifts, economic cycles, and tech trends are reshaping its prospects. Ideal for investors and strategists seeking actionable foresight. Purchase the full report for the complete, editable breakdown and immediate insights.

Political factors

Defense budgets and procurement cycles

Government spending priorities directly shape demand for body armor, EOD tools and duty gear; global military expenditure reached 2.24 trillion USD in 2023 (SIPRI), so shifts in allocations materially affect order books. Election cycles, fiscal deficits and supplemental appropriations can accelerate or delay orders, while multi‑year procurement programs improve visibility but may be rebaselined with policy shifts. Diversifying across agencies and countries reduces single‑budget exposure.

Geopolitical tensions and conflict intensity

Geopolitical tensions and higher conflict intensity drive urgent procurement spikes — global military expenditure reached about 2.24 trillion USD in 2023 and the US defense budget was roughly 858 billion USD in 2024, lifting demand and order volumes for suppliers like Cadre Holdings. Periods of détente compress order flow and revenue visibility. Sanctions and shifting alliances restrict market access regionally. Rigorous scenario planning is needed to match production capacity to volatile demand.

Export controls and foreign policy alignment

Access to international customers for Cadre Holdings depends on home‑country export licenses and end‑use restrictions, with US and allied controls tightened for advanced technologies during 2022–2024 and continuing into 2025. Policy shifts can abruptly close or open markets, as seen when 2024 semiconductor export rules reshaped buyer eligibility. Strong compliance processes protect continuity of approvals and limit revenue disruption. Building relationships with vetted, compliant distributors mitigates license risk.

Public safety policy and policing reforms

Legislative reforms since 2023 have shifted equipment standards, permissible use, and funding, with federal COPS and Byrne-style grants and related programs dispersing roughly $1.1 billion to local agencies in 2024, boosting purchasing power for protective gear. Body armor mandates in several states increased procurement, while bans or restrictions on crowd-control gear have reduced demand for those lines. Cadre Holdings’ participation in NIJ and ASTM committees helps anticipate standards and capture demand shifts.

- Grants 2024 ≈ $1.1B (federal COPS/Byrne)

- Body armor mandate states: procurement uptick

- Restrictions curb crowd-control equipment sales

- Standards committee engagement = early signal

Trade policy, tariffs, and reshoring incentives

Tariffs on textiles, composites and electronics (Section 301 rates up to 25%) materially raise Cadre Holdings input costs and force price pass‑through; US industrial policy — CHIPS Act $52B and IRA $369B — plus state reshoring grants support domestic manufacturing investment. Customs bottlenecks (port dwell times spiking to >6 days in 2021–22) and geopolitical friction can halt cross‑border supply, so flexible multi‑source strategies hedge policy swings.

- Tariffs: up to 25% on key inputs

- Reshoring: CHIPS $52B; IRA $369B

- Customs risk: port dwell >6 days peak

- Mitigation: diversified sourcing, nearshoring

Procurement volatility, trade curbs 2.24T US ≈858B

Government budgets and election cycles drive order timing; global military spend was 2.24T USD in 2023 and US defense ≈858B USD in 2024, so procurement volatility affects Cadre’s revenue visibility. Export controls, tariffs (up to 25%) and grants ($1.1B COPS/Byrne 2024) reshape market access and sourcing. Active standards engagement and multi‑source supply reduce policy risk.

| Metric | Value |

|---|---|

| Global mil. spend 2023 | 2.24T USD |

| US defense 2024 | ≈858B USD |

| Federal grants 2024 | ≈1.1B USD |

| Tariffs | Up to 25% |

What is included in the product

Provides a concise PESTLE review of how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Cadre Holdings, grounded in current market and regulatory data. Designed for executives and investors, it highlights risks, opportunities and forward‑looking scenarios ready for reports or decks.

A concise, visually segmented Cadre Holdings PESTLE summary that relieves planning friction by highlighting key political, economic, social, technological, legal and environmental risks at a glance for meeting use. Easily shareable and editable, it supports quick alignment across teams, client reports, and strategic discussions on external risk and market positioning.

Economic factors

Macroeconomic cycles and budget constraints

Recessions squeeze tax revenues, constraining public safety and defense budgets and forcing re-prioritization of spending; global military expenditure still rose to about 2.24 trillion USD in 2023 (SIPRI). Conversely, fiscal stimulus or security-focused appropriations often offset downturns. Commercial demand for private security tracks broader business activity and trade volumes. A resilient mix of end-markets smooths cyclical exposure for Cadre Holdings.

Inflation, input costs, and pricing power

Aramid fibers, ceramics and specialty metals are highly sensitive to commodity and energy swings; Brent crude averaged about $85/bbl in 2024 and U.S. CPI rose 3.4% (BLS, 2024). Contract structures that limit pass‑through risk compressing margins. Indexing and strategic sourcing can protect profitability. Continuous value engineering preserves affordability and performance.

Foreign exchange and global revenue mix

Multi‑currency sales expose Cadre Holdings earnings to FX volatility, especially with the US dollar trading near a DXY of about 106 in July 2025, which amplifies translation risk for foreign revenue streams. Robust hedging policies and shifting production locally have been shown to curb both transaction and translation shocks. Dollar strength can erode overseas competitiveness, so pricing strategies must reflect currency dynamics and pass‑through limits to protect margins.

Supply chain resilience and lead times

Disruptions in advanced materials and electronics extended lead times—semiconductor lead times peaked near 26 weeks in 2021 and averaged about 14 weeks by 2024—pressuring Cadre Holdings delivery schedules. Dual sourcing and inventory buffers raise on‑time rates and resilience. Vendor qualification and nearshoring cut geopolitical and logistics risk while transparent lead‑time communication sustains customer trust.

- 26w peak (2021); ~14w avg (2024)

- Dual sourcing + buffers = higher reliability

- Nearshoring reduces geopolitical/logistics exposure

- Clear lead‑time updates sustain trust

Scale economies and operating leverage

Batch production and shared components reduce Cadre Holdings unit costs, raising gross margins as volumes grow while making profits more sensitive to demand swings; modular designs boost throughput flexibility and shorten changeover times; disciplined cost control and fixed-cost management stabilize earnings across cycles.

- scale-economies

- operating-leverage

- modularity

- cost-discipline

Procurement volatility, trade curbs 2.24T US ≈858B

Global military spend rose to ~2.24 trillion USD in 2023, supporting steady defense orders; recessions compress tax revenues and reprioritize spending. Brent averaged ~85 USD/bbl in 2024 and US CPI was 3.4% (BLS 2024), pressuring input costs and margins. DXY ~106 (Jul 2025) heightens FX translation risk; semiconductor lead times averaged ~14 weeks in 2024, straining delivery.

| Metric | Value |

|---|---|

| Military spend (2023) | 2.24T USD |

| Brent (2024 avg) | ~85 USD/bbl |

| US CPI (2024) | 3.4% |

| DXY (Jul 2025) | ~106 |

| Semiconductor lead time (2024) | ~14 wks |

What You See Is What You Get

Cadre Holdings PESTLE Analysis

The preview shown here is the exact Cadre Holdings PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with complete content and structure, not a placeholder. After checkout you’ll instantly download the exact document displayed here.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Cadre Holdings—three concise chapters reveal how political shifts, economic cycles, and tech trends are reshaping its prospects. Ideal for investors and strategists seeking actionable foresight. Purchase the full report for the complete, editable breakdown and immediate insights.

Political factors

Defense budgets and procurement cycles

Government spending priorities directly shape demand for body armor, EOD tools and duty gear; global military expenditure reached 2.24 trillion USD in 2023 (SIPRI), so shifts in allocations materially affect order books. Election cycles, fiscal deficits and supplemental appropriations can accelerate or delay orders, while multi‑year procurement programs improve visibility but may be rebaselined with policy shifts. Diversifying across agencies and countries reduces single‑budget exposure.

Geopolitical tensions and conflict intensity

Geopolitical tensions and higher conflict intensity drive urgent procurement spikes — global military expenditure reached about 2.24 trillion USD in 2023 and the US defense budget was roughly 858 billion USD in 2024, lifting demand and order volumes for suppliers like Cadre Holdings. Periods of détente compress order flow and revenue visibility. Sanctions and shifting alliances restrict market access regionally. Rigorous scenario planning is needed to match production capacity to volatile demand.

Export controls and foreign policy alignment

Access to international customers for Cadre Holdings depends on home‑country export licenses and end‑use restrictions, with US and allied controls tightened for advanced technologies during 2022–2024 and continuing into 2025. Policy shifts can abruptly close or open markets, as seen when 2024 semiconductor export rules reshaped buyer eligibility. Strong compliance processes protect continuity of approvals and limit revenue disruption. Building relationships with vetted, compliant distributors mitigates license risk.

Public safety policy and policing reforms

Legislative reforms since 2023 have shifted equipment standards, permissible use, and funding, with federal COPS and Byrne-style grants and related programs dispersing roughly $1.1 billion to local agencies in 2024, boosting purchasing power for protective gear. Body armor mandates in several states increased procurement, while bans or restrictions on crowd-control gear have reduced demand for those lines. Cadre Holdings’ participation in NIJ and ASTM committees helps anticipate standards and capture demand shifts.

- Grants 2024 ≈ $1.1B (federal COPS/Byrne)

- Body armor mandate states: procurement uptick

- Restrictions curb crowd-control equipment sales

- Standards committee engagement = early signal

Trade policy, tariffs, and reshoring incentives

Tariffs on textiles, composites and electronics (Section 301 rates up to 25%) materially raise Cadre Holdings input costs and force price pass‑through; US industrial policy — CHIPS Act $52B and IRA $369B — plus state reshoring grants support domestic manufacturing investment. Customs bottlenecks (port dwell times spiking to >6 days in 2021–22) and geopolitical friction can halt cross‑border supply, so flexible multi‑source strategies hedge policy swings.

- Tariffs: up to 25% on key inputs

- Reshoring: CHIPS $52B; IRA $369B

- Customs risk: port dwell >6 days peak

- Mitigation: diversified sourcing, nearshoring

Procurement volatility, trade curbs 2.24T US ≈858B

Government budgets and election cycles drive order timing; global military spend was 2.24T USD in 2023 and US defense ≈858B USD in 2024, so procurement volatility affects Cadre’s revenue visibility. Export controls, tariffs (up to 25%) and grants ($1.1B COPS/Byrne 2024) reshape market access and sourcing. Active standards engagement and multi‑source supply reduce policy risk.

| Metric | Value |

|---|---|

| Global mil. spend 2023 | 2.24T USD |

| US defense 2024 | ≈858B USD |

| Federal grants 2024 | ≈1.1B USD |

| Tariffs | Up to 25% |

What is included in the product

Provides a concise PESTLE review of how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Cadre Holdings, grounded in current market and regulatory data. Designed for executives and investors, it highlights risks, opportunities and forward‑looking scenarios ready for reports or decks.

A concise, visually segmented Cadre Holdings PESTLE summary that relieves planning friction by highlighting key political, economic, social, technological, legal and environmental risks at a glance for meeting use. Easily shareable and editable, it supports quick alignment across teams, client reports, and strategic discussions on external risk and market positioning.

Economic factors

Macroeconomic cycles and budget constraints

Recessions squeeze tax revenues, constraining public safety and defense budgets and forcing re-prioritization of spending; global military expenditure still rose to about 2.24 trillion USD in 2023 (SIPRI). Conversely, fiscal stimulus or security-focused appropriations often offset downturns. Commercial demand for private security tracks broader business activity and trade volumes. A resilient mix of end-markets smooths cyclical exposure for Cadre Holdings.

Inflation, input costs, and pricing power

Aramid fibers, ceramics and specialty metals are highly sensitive to commodity and energy swings; Brent crude averaged about $85/bbl in 2024 and U.S. CPI rose 3.4% (BLS, 2024). Contract structures that limit pass‑through risk compressing margins. Indexing and strategic sourcing can protect profitability. Continuous value engineering preserves affordability and performance.

Foreign exchange and global revenue mix

Multi‑currency sales expose Cadre Holdings earnings to FX volatility, especially with the US dollar trading near a DXY of about 106 in July 2025, which amplifies translation risk for foreign revenue streams. Robust hedging policies and shifting production locally have been shown to curb both transaction and translation shocks. Dollar strength can erode overseas competitiveness, so pricing strategies must reflect currency dynamics and pass‑through limits to protect margins.

Supply chain resilience and lead times

Disruptions in advanced materials and electronics extended lead times—semiconductor lead times peaked near 26 weeks in 2021 and averaged about 14 weeks by 2024—pressuring Cadre Holdings delivery schedules. Dual sourcing and inventory buffers raise on‑time rates and resilience. Vendor qualification and nearshoring cut geopolitical and logistics risk while transparent lead‑time communication sustains customer trust.

- 26w peak (2021); ~14w avg (2024)

- Dual sourcing + buffers = higher reliability

- Nearshoring reduces geopolitical/logistics exposure

- Clear lead‑time updates sustain trust

Scale economies and operating leverage

Batch production and shared components reduce Cadre Holdings unit costs, raising gross margins as volumes grow while making profits more sensitive to demand swings; modular designs boost throughput flexibility and shorten changeover times; disciplined cost control and fixed-cost management stabilize earnings across cycles.

- scale-economies

- operating-leverage

- modularity

- cost-discipline

Procurement volatility, trade curbs 2.24T US ≈858B

Global military spend rose to ~2.24 trillion USD in 2023, supporting steady defense orders; recessions compress tax revenues and reprioritize spending. Brent averaged ~85 USD/bbl in 2024 and US CPI was 3.4% (BLS 2024), pressuring input costs and margins. DXY ~106 (Jul 2025) heightens FX translation risk; semiconductor lead times averaged ~14 weeks in 2024, straining delivery.

| Metric | Value |

|---|---|

| Military spend (2023) | 2.24T USD |

| Brent (2024 avg) | ~85 USD/bbl |

| US CPI (2024) | 3.4% |

| DXY (Jul 2025) | ~106 |

| Semiconductor lead time (2024) | ~14 wks |

What You See Is What You Get

Cadre Holdings PESTLE Analysis

The preview shown here is the exact Cadre Holdings PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, final file with complete content and structure, not a placeholder. After checkout you’ll instantly download the exact document displayed here.