CaixaBank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

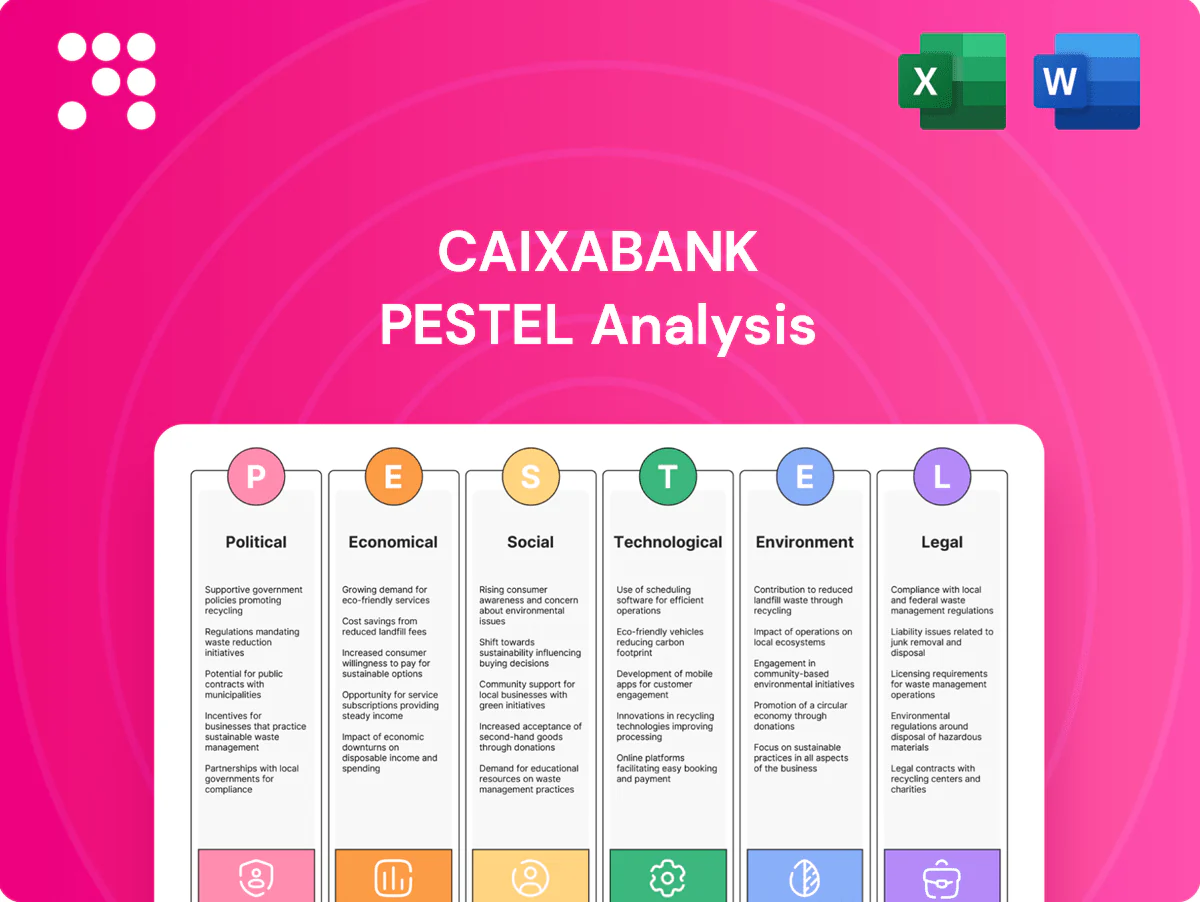

Gain strategic clarity with our PESTLE Analysis of CaixaBank. Explore how political, economic, social, technological, legal and environmental forces shape its risks and opportunities. Purchase the full report for detailed, ready-to-use insights and downloadable charts.

Political factors

EU-ECB supervision stance

CaixaBank operates under the EU Banking Union and ECB/SSM oversight, which directly shape its capital, liquidity and risk appetites; the bank reported a fully-loaded CET1 ratio of 12.6% at 2024 year-end. Policy shifts on countercyclical buffers or MREL requirements can materially alter lending capacity and funding structures across the sector. CaixaBank’s strategic engagement with regulators aims to align growth plans with prudential expectations. Stable compliance lowers funding costs and sustains investor confidence, supporting access to wholesale markets.

Spanish fiscal-policy direction

Spanish fiscal direction—with NextGenerationEU support of €69.5bn and public debt near 115% of GDP (2024)—shapes CaixaBank risk and demand. Expansionary spending and NGEU transfers boost SME and household lending pipelines, while fiscal consolidation would slow credit growth. Bank-targeted tax changes or windfall levies would compress ROE. ICO guarantees and government-backed programs cyclically reduce credit losses.

Regional dynamics and governance

Regional dynamics across Spain’s 17 autonomous communities shape public procurement, subsidies and local deposits, directly influencing CaixaBank’s regional lending flows; as Spain’s largest retail bank CaixaBank maintains a broad branch footprint across these regions. Political frictions or policy divergence can alter local sentiment and credit performance, requiring nuanced stakeholder management. Public-private partnerships tied to Spain’s €69.5bn NextGenerationEU funds create opportunities in infrastructure and social housing finance.

EU funding and green agenda

NextGenerationEU (€800bn) and the RRF (€672.5bn) channel capital to digital and green projects, creating mandates that banks can co-finance to earn fees and lending flows; alignment with the EU Green Deal (carbon neutrality by 2050) improves access to guarantees and preferential schemes like InvestEU (expected mobilization ~€372bn).

- NGEU: €800bn

- RRF: €672.5bn

- InvestEU mobilization: ~€372bn

- Key: monitor eligibility to convert pipeline

Geopolitical shocks and sanctions

Geopolitical shocks—energy disruptions, war and strained supply chains—raise macro volatility and credit risk, pressuring CaixaBank’s risk costs even as the ECB policy rate stayed near 4% in 2024; CaixaBank reported a fully loaded CET1 around 12.7% in 2024, underpinning resilience. Sanctions regimes force enhanced screening and can curtail specific cross-border business, while market volatility can widen funding spreads by multiple basis points and shift customer liquidity behavior; scenario planning preserves capital and enforces pricing discipline.

- impact: higher credit risk and provisioning

- compliance: stricter screening, limited corridors

- funding: spreads can widen by tens of bps

- mitigation: scenario-driven capital and pricing actions

ECB regulation and NGEU transfers reshape Spanish banks lending capacity and margins

CaixaBank is tightly regulated by the ECB/SSM and EU Banking Union, with fully-loaded CET1 at 12.6% (2024), so prudential shifts (CCyB, MREL) materially affect lending capacity. Spanish fiscal policy and €69.5bn NGEU transfers boost credit pipelines while public debt ~115% GDP moderates consolidation risk. Geopolitical shocks and sanctions raise provisioning and funding spreads; ECB rate ~4% in 2024 shapes net interest margins.

| Metric | Value |

|---|---|

| Fully-loaded CET1 (2024) | 12.6% |

| ECB policy rate (2024) | ~4% |

| Spain public debt (2024) | ~115% GDP |

| NGEU to Spain | €69.5bn |

What is included in the product

Explores how macro-environmental forces uniquely affect CaixaBank across Political, Economic, Social, Technological, Environmental and Legal dimensions, with Spain/EU-specific trends and data-driven subpoints. Designed for executives and investors, it delivers forward-looking insights for risk mitigation, opportunity spotting and scenario planning.

A concise, visually segmented CaixaBank PESTLE summary that clarifies regulatory, economic and technological risks for quick use in presentations and planning sessions, with editable notes for regional or business‑line tailoring to speed decision-making and align teams.

Economic factors

ECB rate cycle impact

CaixaBanks net interest income remains highly sensitive to the ECB policy rate, which rose to about 4.0% by end‑2024, with deposit beta around 50% driving margin pressure. Easing would compress margins but likely lower credit costs, while further tightening boosts NII yet raises default risk. Robust ALM, hedging and deposit pricing discipline are critical to preserve spread resilience.

Spain’s growth and labor market

Spain's GDP, driven heavily by tourism (recovering to about 90% of 2019 arrivals) and strong services and construction, shapes CaixaBank's loan demand and credit quality as tourism-linked cashflows and mortgages rise. Employment improvements—Spain's unemployment near 12% in 2024—support retail lending and keep NPLs lower, while deterioration would boost provisions. SMEs, representing ~99% of firms and ~60% of employment, are a key transmission channel. Regional diversification across Catalonia, Madrid and Andalusia smooths cyclicality.

Housing market dynamics

Mortgage origination at CaixaBank is constrained by affordability, rising house prices (Spain house prices rose about 6–7% in 2024) and limited supply, keeping new mortgage volumes subdued versus pre‑pandemic levels. Rate resets from higher ECB-driven borrowing costs (policy rates near 4% in 2024) increase refinancing needs and pressure delinquency trajectories for adjustable loans. Stricter regulatory affordability tests introduced since 2021 have reduced approval rates, while declines in mortgage‑backed collateral values would raise risk weights and capital consumption for the bank.

Inflation and household budgets

Sticky inflation squeezes household cash flows and compresses SME margins, boosting demand for short-term credit and working-capital lines. Euro-area HICP averaged 2.4% in 2024 and ECB policy rates were around 4% by mid-2025, altering real-income trends and savings mixes. CaixaBank fee businesses (payments, insurance) show resilience, while cost control and efficiency programmes are essential to offset margin pressure.

- Inflation: euro-area HICP 2.4% (2024)

- Rates: ECB policy ~4% (mid-2025)

- Impacts: higher credit demand, mixed fee income resilience

Funding markets and liquidity

Wholesale spreads widened as TLTRO roll-offs reduced ECB-sourced funding, so CaixaBank leaned on diversified markets; its reported liquidity buffers remained above regulatory minima with LCR and NSFR both held above 100%, supporting stability through cycles. Covered bonds and securitisations (ongoing EUR issuance) broadened funding, while proactive investor communication preserved access during bouts of volatility.

- Wholesale spreads rose amid TLTRO roll-offs

- LCR & NSFR maintained above 100%

- Covered bonds/securitisations diversify funding

- Active investor communication sustains market access

ECB regulation and NGEU transfers reshape Spanish banks lending capacity and margins

CaixaBank NII remains highly sensitive to ECB policy ~4% (mid‑2025) with deposit beta ~50% affecting margins. Spain recovery led by tourism (arrivals ~90% of 2019) and services supports loan demand; unemployment ~12% (2024). House prices +6–7% (2024) and inflation HICP 2.4% (2024) pressure affordability; LCR/NSFR >100% and SMEs (~99% firms, ~60% employment) drive credit exposure.

| Metric | Value |

|---|---|

| ECB rate | ~4% (mid‑2025) |

| HICP | 2.4% (2024) |

| Unemployment | ~12% (2024) |

Full Version Awaits

CaixaBank PESTLE Analysis

The preview shown here is the exact CaixaBank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the final, professionally structured file. After checkout you’ll be able to download this exact document immediately.

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis of CaixaBank. Explore how political, economic, social, technological, legal and environmental forces shape its risks and opportunities. Purchase the full report for detailed, ready-to-use insights and downloadable charts.

Political factors

EU-ECB supervision stance

CaixaBank operates under the EU Banking Union and ECB/SSM oversight, which directly shape its capital, liquidity and risk appetites; the bank reported a fully-loaded CET1 ratio of 12.6% at 2024 year-end. Policy shifts on countercyclical buffers or MREL requirements can materially alter lending capacity and funding structures across the sector. CaixaBank’s strategic engagement with regulators aims to align growth plans with prudential expectations. Stable compliance lowers funding costs and sustains investor confidence, supporting access to wholesale markets.

Spanish fiscal-policy direction

Spanish fiscal direction—with NextGenerationEU support of €69.5bn and public debt near 115% of GDP (2024)—shapes CaixaBank risk and demand. Expansionary spending and NGEU transfers boost SME and household lending pipelines, while fiscal consolidation would slow credit growth. Bank-targeted tax changes or windfall levies would compress ROE. ICO guarantees and government-backed programs cyclically reduce credit losses.

Regional dynamics and governance

Regional dynamics across Spain’s 17 autonomous communities shape public procurement, subsidies and local deposits, directly influencing CaixaBank’s regional lending flows; as Spain’s largest retail bank CaixaBank maintains a broad branch footprint across these regions. Political frictions or policy divergence can alter local sentiment and credit performance, requiring nuanced stakeholder management. Public-private partnerships tied to Spain’s €69.5bn NextGenerationEU funds create opportunities in infrastructure and social housing finance.

EU funding and green agenda

NextGenerationEU (€800bn) and the RRF (€672.5bn) channel capital to digital and green projects, creating mandates that banks can co-finance to earn fees and lending flows; alignment with the EU Green Deal (carbon neutrality by 2050) improves access to guarantees and preferential schemes like InvestEU (expected mobilization ~€372bn).

- NGEU: €800bn

- RRF: €672.5bn

- InvestEU mobilization: ~€372bn

- Key: monitor eligibility to convert pipeline

Geopolitical shocks and sanctions

Geopolitical shocks—energy disruptions, war and strained supply chains—raise macro volatility and credit risk, pressuring CaixaBank’s risk costs even as the ECB policy rate stayed near 4% in 2024; CaixaBank reported a fully loaded CET1 around 12.7% in 2024, underpinning resilience. Sanctions regimes force enhanced screening and can curtail specific cross-border business, while market volatility can widen funding spreads by multiple basis points and shift customer liquidity behavior; scenario planning preserves capital and enforces pricing discipline.

- impact: higher credit risk and provisioning

- compliance: stricter screening, limited corridors

- funding: spreads can widen by tens of bps

- mitigation: scenario-driven capital and pricing actions

ECB regulation and NGEU transfers reshape Spanish banks lending capacity and margins

CaixaBank is tightly regulated by the ECB/SSM and EU Banking Union, with fully-loaded CET1 at 12.6% (2024), so prudential shifts (CCyB, MREL) materially affect lending capacity. Spanish fiscal policy and €69.5bn NGEU transfers boost credit pipelines while public debt ~115% GDP moderates consolidation risk. Geopolitical shocks and sanctions raise provisioning and funding spreads; ECB rate ~4% in 2024 shapes net interest margins.

| Metric | Value |

|---|---|

| Fully-loaded CET1 (2024) | 12.6% |

| ECB policy rate (2024) | ~4% |

| Spain public debt (2024) | ~115% GDP |

| NGEU to Spain | €69.5bn |

What is included in the product

Explores how macro-environmental forces uniquely affect CaixaBank across Political, Economic, Social, Technological, Environmental and Legal dimensions, with Spain/EU-specific trends and data-driven subpoints. Designed for executives and investors, it delivers forward-looking insights for risk mitigation, opportunity spotting and scenario planning.

A concise, visually segmented CaixaBank PESTLE summary that clarifies regulatory, economic and technological risks for quick use in presentations and planning sessions, with editable notes for regional or business‑line tailoring to speed decision-making and align teams.

Economic factors

ECB rate cycle impact

CaixaBanks net interest income remains highly sensitive to the ECB policy rate, which rose to about 4.0% by end‑2024, with deposit beta around 50% driving margin pressure. Easing would compress margins but likely lower credit costs, while further tightening boosts NII yet raises default risk. Robust ALM, hedging and deposit pricing discipline are critical to preserve spread resilience.

Spain’s growth and labor market

Spain's GDP, driven heavily by tourism (recovering to about 90% of 2019 arrivals) and strong services and construction, shapes CaixaBank's loan demand and credit quality as tourism-linked cashflows and mortgages rise. Employment improvements—Spain's unemployment near 12% in 2024—support retail lending and keep NPLs lower, while deterioration would boost provisions. SMEs, representing ~99% of firms and ~60% of employment, are a key transmission channel. Regional diversification across Catalonia, Madrid and Andalusia smooths cyclicality.

Housing market dynamics

Mortgage origination at CaixaBank is constrained by affordability, rising house prices (Spain house prices rose about 6–7% in 2024) and limited supply, keeping new mortgage volumes subdued versus pre‑pandemic levels. Rate resets from higher ECB-driven borrowing costs (policy rates near 4% in 2024) increase refinancing needs and pressure delinquency trajectories for adjustable loans. Stricter regulatory affordability tests introduced since 2021 have reduced approval rates, while declines in mortgage‑backed collateral values would raise risk weights and capital consumption for the bank.

Inflation and household budgets

Sticky inflation squeezes household cash flows and compresses SME margins, boosting demand for short-term credit and working-capital lines. Euro-area HICP averaged 2.4% in 2024 and ECB policy rates were around 4% by mid-2025, altering real-income trends and savings mixes. CaixaBank fee businesses (payments, insurance) show resilience, while cost control and efficiency programmes are essential to offset margin pressure.

- Inflation: euro-area HICP 2.4% (2024)

- Rates: ECB policy ~4% (mid-2025)

- Impacts: higher credit demand, mixed fee income resilience

Funding markets and liquidity

Wholesale spreads widened as TLTRO roll-offs reduced ECB-sourced funding, so CaixaBank leaned on diversified markets; its reported liquidity buffers remained above regulatory minima with LCR and NSFR both held above 100%, supporting stability through cycles. Covered bonds and securitisations (ongoing EUR issuance) broadened funding, while proactive investor communication preserved access during bouts of volatility.

- Wholesale spreads rose amid TLTRO roll-offs

- LCR & NSFR maintained above 100%

- Covered bonds/securitisations diversify funding

- Active investor communication sustains market access

ECB regulation and NGEU transfers reshape Spanish banks lending capacity and margins

CaixaBank NII remains highly sensitive to ECB policy ~4% (mid‑2025) with deposit beta ~50% affecting margins. Spain recovery led by tourism (arrivals ~90% of 2019) and services supports loan demand; unemployment ~12% (2024). House prices +6–7% (2024) and inflation HICP 2.4% (2024) pressure affordability; LCR/NSFR >100% and SMEs (~99% firms, ~60% employment) drive credit exposure.

| Metric | Value |

|---|---|

| ECB rate | ~4% (mid‑2025) |

| HICP | 2.4% (2024) |

| Unemployment | ~12% (2024) |

Full Version Awaits

CaixaBank PESTLE Analysis

The preview shown here is the exact CaixaBank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the final, professionally structured file. After checkout you’ll be able to download this exact document immediately.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis of CaixaBank. Explore how political, economic, social, technological, legal and environmental forces shape its risks and opportunities. Purchase the full report for detailed, ready-to-use insights and downloadable charts.

Political factors

EU-ECB supervision stance

CaixaBank operates under the EU Banking Union and ECB/SSM oversight, which directly shape its capital, liquidity and risk appetites; the bank reported a fully-loaded CET1 ratio of 12.6% at 2024 year-end. Policy shifts on countercyclical buffers or MREL requirements can materially alter lending capacity and funding structures across the sector. CaixaBank’s strategic engagement with regulators aims to align growth plans with prudential expectations. Stable compliance lowers funding costs and sustains investor confidence, supporting access to wholesale markets.

Spanish fiscal-policy direction

Spanish fiscal direction—with NextGenerationEU support of €69.5bn and public debt near 115% of GDP (2024)—shapes CaixaBank risk and demand. Expansionary spending and NGEU transfers boost SME and household lending pipelines, while fiscal consolidation would slow credit growth. Bank-targeted tax changes or windfall levies would compress ROE. ICO guarantees and government-backed programs cyclically reduce credit losses.

Regional dynamics and governance

Regional dynamics across Spain’s 17 autonomous communities shape public procurement, subsidies and local deposits, directly influencing CaixaBank’s regional lending flows; as Spain’s largest retail bank CaixaBank maintains a broad branch footprint across these regions. Political frictions or policy divergence can alter local sentiment and credit performance, requiring nuanced stakeholder management. Public-private partnerships tied to Spain’s €69.5bn NextGenerationEU funds create opportunities in infrastructure and social housing finance.

EU funding and green agenda

NextGenerationEU (€800bn) and the RRF (€672.5bn) channel capital to digital and green projects, creating mandates that banks can co-finance to earn fees and lending flows; alignment with the EU Green Deal (carbon neutrality by 2050) improves access to guarantees and preferential schemes like InvestEU (expected mobilization ~€372bn).

- NGEU: €800bn

- RRF: €672.5bn

- InvestEU mobilization: ~€372bn

- Key: monitor eligibility to convert pipeline

Geopolitical shocks and sanctions

Geopolitical shocks—energy disruptions, war and strained supply chains—raise macro volatility and credit risk, pressuring CaixaBank’s risk costs even as the ECB policy rate stayed near 4% in 2024; CaixaBank reported a fully loaded CET1 around 12.7% in 2024, underpinning resilience. Sanctions regimes force enhanced screening and can curtail specific cross-border business, while market volatility can widen funding spreads by multiple basis points and shift customer liquidity behavior; scenario planning preserves capital and enforces pricing discipline.

- impact: higher credit risk and provisioning

- compliance: stricter screening, limited corridors

- funding: spreads can widen by tens of bps

- mitigation: scenario-driven capital and pricing actions

ECB regulation and NGEU transfers reshape Spanish banks lending capacity and margins

CaixaBank is tightly regulated by the ECB/SSM and EU Banking Union, with fully-loaded CET1 at 12.6% (2024), so prudential shifts (CCyB, MREL) materially affect lending capacity. Spanish fiscal policy and €69.5bn NGEU transfers boost credit pipelines while public debt ~115% GDP moderates consolidation risk. Geopolitical shocks and sanctions raise provisioning and funding spreads; ECB rate ~4% in 2024 shapes net interest margins.

| Metric | Value |

|---|---|

| Fully-loaded CET1 (2024) | 12.6% |

| ECB policy rate (2024) | ~4% |

| Spain public debt (2024) | ~115% GDP |

| NGEU to Spain | €69.5bn |

What is included in the product

Explores how macro-environmental forces uniquely affect CaixaBank across Political, Economic, Social, Technological, Environmental and Legal dimensions, with Spain/EU-specific trends and data-driven subpoints. Designed for executives and investors, it delivers forward-looking insights for risk mitigation, opportunity spotting and scenario planning.

A concise, visually segmented CaixaBank PESTLE summary that clarifies regulatory, economic and technological risks for quick use in presentations and planning sessions, with editable notes for regional or business‑line tailoring to speed decision-making and align teams.

Economic factors

ECB rate cycle impact

CaixaBanks net interest income remains highly sensitive to the ECB policy rate, which rose to about 4.0% by end‑2024, with deposit beta around 50% driving margin pressure. Easing would compress margins but likely lower credit costs, while further tightening boosts NII yet raises default risk. Robust ALM, hedging and deposit pricing discipline are critical to preserve spread resilience.

Spain’s growth and labor market

Spain's GDP, driven heavily by tourism (recovering to about 90% of 2019 arrivals) and strong services and construction, shapes CaixaBank's loan demand and credit quality as tourism-linked cashflows and mortgages rise. Employment improvements—Spain's unemployment near 12% in 2024—support retail lending and keep NPLs lower, while deterioration would boost provisions. SMEs, representing ~99% of firms and ~60% of employment, are a key transmission channel. Regional diversification across Catalonia, Madrid and Andalusia smooths cyclicality.

Housing market dynamics

Mortgage origination at CaixaBank is constrained by affordability, rising house prices (Spain house prices rose about 6–7% in 2024) and limited supply, keeping new mortgage volumes subdued versus pre‑pandemic levels. Rate resets from higher ECB-driven borrowing costs (policy rates near 4% in 2024) increase refinancing needs and pressure delinquency trajectories for adjustable loans. Stricter regulatory affordability tests introduced since 2021 have reduced approval rates, while declines in mortgage‑backed collateral values would raise risk weights and capital consumption for the bank.

Inflation and household budgets

Sticky inflation squeezes household cash flows and compresses SME margins, boosting demand for short-term credit and working-capital lines. Euro-area HICP averaged 2.4% in 2024 and ECB policy rates were around 4% by mid-2025, altering real-income trends and savings mixes. CaixaBank fee businesses (payments, insurance) show resilience, while cost control and efficiency programmes are essential to offset margin pressure.

- Inflation: euro-area HICP 2.4% (2024)

- Rates: ECB policy ~4% (mid-2025)

- Impacts: higher credit demand, mixed fee income resilience

Funding markets and liquidity

Wholesale spreads widened as TLTRO roll-offs reduced ECB-sourced funding, so CaixaBank leaned on diversified markets; its reported liquidity buffers remained above regulatory minima with LCR and NSFR both held above 100%, supporting stability through cycles. Covered bonds and securitisations (ongoing EUR issuance) broadened funding, while proactive investor communication preserved access during bouts of volatility.

- Wholesale spreads rose amid TLTRO roll-offs

- LCR & NSFR maintained above 100%

- Covered bonds/securitisations diversify funding

- Active investor communication sustains market access

ECB regulation and NGEU transfers reshape Spanish banks lending capacity and margins

CaixaBank NII remains highly sensitive to ECB policy ~4% (mid‑2025) with deposit beta ~50% affecting margins. Spain recovery led by tourism (arrivals ~90% of 2019) and services supports loan demand; unemployment ~12% (2024). House prices +6–7% (2024) and inflation HICP 2.4% (2024) pressure affordability; LCR/NSFR >100% and SMEs (~99% firms, ~60% employment) drive credit exposure.

| Metric | Value |

|---|---|

| ECB rate | ~4% (mid‑2025) |

| HICP | 2.4% (2024) |

| Unemployment | ~12% (2024) |

Full Version Awaits

CaixaBank PESTLE Analysis

The preview shown here is the exact CaixaBank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the final, professionally structured file. After checkout you’ll be able to download this exact document immediately.