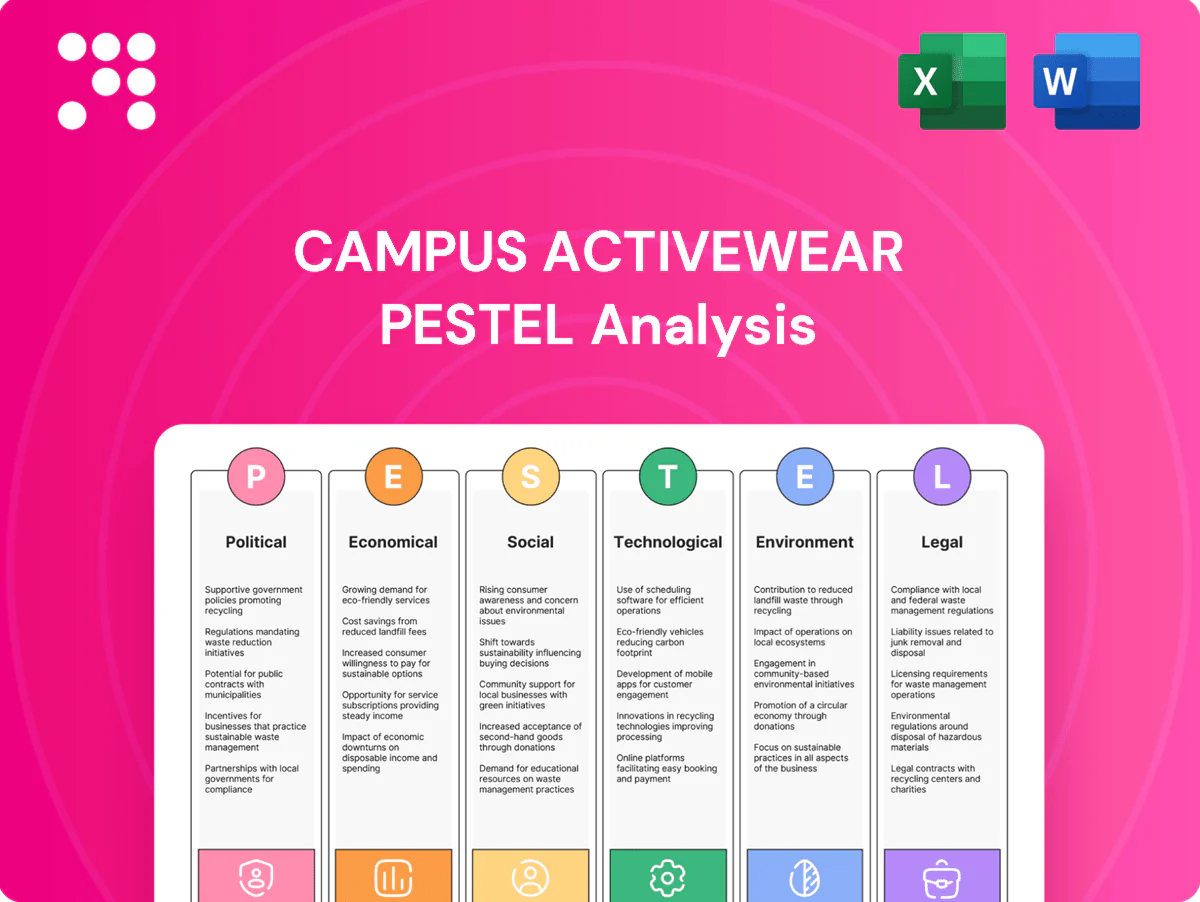

Campus Activewear PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal and environmental forces are shaping Campus Activewear’s trajectory—our PESTLE pinpoints risks and opportunities you can act on today. Ideal for investors and strategists; purchase the full, downloadable analysis for the complete, editable report.

Political factors

GST regime and indirect tax stability

India’s GST treats footwear with MRP up to ₹1,000 at 5% (no input tax credit) and footwear above ₹1,000 at 18% (with ITC), directly influencing Campus pricing, gross margins and channel economics. Rate revisions can reallocate demand across price bands and alter working capital because input credits affect cash flow timing. Campus should monitor SKU price thresholds and structure assortments to optimize tax slabs. Engagement through CII/industry bodies can help mitigate adverse rate changes.

Make in India incentives and PLI

India’s Make in India/PLI drive (total outlay INR 1.97 lakh crore across sectors) plus duty-drawback and state capital/subsidy schemes can cut unit costs and fund capacity expansion; eligibility depends on local value-addition and export targets. Campus can realign sourcing/assembly to qualify, while site choice must weigh power tariffs and logistics connectivity.

Import duties on raw materials

Customs duties on EVA, rubber, textiles and machinery materially affect Campus Activewear’s cost structure; India’s applied MFN tariff averaged about 13.5% per WTO latest published data, and specific duties on footwear inputs commonly fall in the mid-single to low-double digits, raising input costs when domestic supply is limited. Protective tariffs support local manufacturing but can inflate COGS if suppliers are thin. Scenario planning for duty shifts reduces price shock, while supplier diversification hedges geopolitical disruptions.

State-level policies and compliance

State-level policies matter: India has 28 states and 8 union territories, and industrial power tariffs, labor registration norms and local levies differ materially across them, affecting operating costs and hiring. Multi-plant footprints face distinct approvals and inspections per state, lengthening project timelines. Consolidated compliance calendars reduce penalty risk, while strong government relations speed permits and expansions.

- Labor norms vary by state

- Industrial power tariffs differ regionally

- Distinct approvals & inspections per plant

- Compliance calendars cut penalty exposure

- Good govt relations accelerate permits

Infrastructure and logistics push

Public investment under PM GatiShakti (launched 2021) and continued road, rail and freight corridor expansion shortens lead times to MBOs and EBOs, enabling Campus to reoptimize distribution centers as corridors open; India’s logistics cost remains around 13–14% of GDP, highlighting upside from better infrastructure.

- Shorter lead times

- DC network reoptimization

- Lower inventory buffers

- Improved last-mile via e‑commerce logistics

Policy: GST 5%/18%, PLI ₹1.97L cr, tariffs ~13.5% pressure margins

Political factors: GST slabs (5% ≤₹1,000; 18% >₹1,000) and input tax credit rules materially affect Campus pricing, margins and cash flow. PLI/Make in India (PLI outlay ₹1.97 lakh crore) + state subsidies can lower unit costs if local value-add targets met. Customs/MFN tariffs (~13.5%) and state power/labor variance drive COGS and site selection; PM GatiShakti reduces logistics cost exposure (logistics ≈13–14% of GDP).

| Factor | Impact | Metric (2024/25) |

|---|---|---|

| GST | Pricing, margins | 5%/18% |

| PLI | Capex subsidy | ₹1.97L cr |

| Tariffs | COGS risk | MFN ~13.5% |

| Logistics | Lead-time/cost | 13–14% GDP |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Campus Activewear, using current data and trend-driven sub-points to identify risks and opportunities; designed for executives, advisors and investors, the analysis is region- and industry-specific, formatted for decks and plans and includes forward-looking insights to support scenario planning and funding discussions.

A concise Campus Activewear PESTLE Analysis that highlights regulatory, economic, social, technological and environmental risks and opportunities, formatted for quick insertion into presentations and team planning—editable and shareable to align stakeholders and simplify external risk discussions.

Economic factors

Consumer discretionary cycles

Footwear demand in urban and semi-urban India closely follows income and employment trends; with India GDP growth near 7.2% in 2024, discretionary spend lifted premium and athleisure share, while slowdowns push consumers to value SKUs and promotions. Campus should flex pricing ladders and inventory mix between value and premium SKUs accordingly.

Input cost inflation and volatility

Input costs for Campus Activewear—EVA, rubber, synthetics, adhesives—track crude and commodity cycles (Brent averaged about 85 USD/bbl in 2024) and polymer/resin costs rose roughly 10–15% Y/Y in 2024. Inflation can compress gross margins by 100–300 bps if price pass-through lags. Hedging, formula-based contracts and material redesigns improve resilience. Ongoing cost engineering sustains competitiveness.

FX exposure and import content

Imported components and machinery create direct dollar exposure for Campus Activewear; INR traded near 83.5 per USD in mid-2025, lifting landed costs and capex budgets. INR depreciation raises input costs and compresses margins unless mitigated. Natural hedges from export receipts and using forward cover stabilize margins, while progressive localization of critical inputs reduces FX risk over time.

Interest rates and channel credit

Higher interest environment (RBI repo at 6.50% in July 2025) raises working capital costs and reduces distributor credit appetite; collections from MBOs often elongate in tight liquidity, pushing DSO higher. Dynamic discounting and fintech receivables can cut DSO by up to 15%, improving cash conversion. Align inventory to sell-through to avoid elevated carrying costs.

- repo_rate: 6.50%

- DSO_reduction_potential: up to 15%

- focus: inventory vs sell-through

Tier-2 and tier-3 market expansion

- Non-metro consumption share ~55% (2024)

- Higher price elasticity, stronger potential volumes

- Tailored assortments & regional sizing = better sell-through

- Micro-fulfillment reduces last-mile costs ~25–35%

Policy: GST 5%/18%, PLI ₹1.97L cr, tariffs ~13.5% pressure margins

GDP ~7.2% (2024) lifts premium/athleisure; slowdowns shift demand to value SKUs. Brent ~$85/bbl (2024) and polymers +10–15% Y/Y squeeze margins; hedging and cost engineering critical. INR ~83.5/USD (mid-2025) and RBI repo 6.50% (Jul 2025) raise input and WC costs; non-metro share ~55% (2024) offers volume growth with higher price elasticity.

| Metric | Value |

|---|---|

| GDP (2024) | 7.2% |

| Brent (2024) | $85/bbl |

| Polymers Δ (2024) | +10–15% Y/Y |

| INR (mid-2025) | 83.5/USD |

| RBI repo (Jul 2025) | 6.50% |

| Non-metro consumption (2024) | ~55% |

| DSO reduction potential | up to 15% |

| Last-mile savings (micro-hub) | 25–35% |

Preview Before You Purchase

Campus Activewear PESTLE Analysis

The preview shown here is the exact Campus Activewear PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with concise, actionable insights. No placeholders or teasers; the final file is available for instant download.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal and environmental forces are shaping Campus Activewear’s trajectory—our PESTLE pinpoints risks and opportunities you can act on today. Ideal for investors and strategists; purchase the full, downloadable analysis for the complete, editable report.

Political factors

GST regime and indirect tax stability

India’s GST treats footwear with MRP up to ₹1,000 at 5% (no input tax credit) and footwear above ₹1,000 at 18% (with ITC), directly influencing Campus pricing, gross margins and channel economics. Rate revisions can reallocate demand across price bands and alter working capital because input credits affect cash flow timing. Campus should monitor SKU price thresholds and structure assortments to optimize tax slabs. Engagement through CII/industry bodies can help mitigate adverse rate changes.

Make in India incentives and PLI

India’s Make in India/PLI drive (total outlay INR 1.97 lakh crore across sectors) plus duty-drawback and state capital/subsidy schemes can cut unit costs and fund capacity expansion; eligibility depends on local value-addition and export targets. Campus can realign sourcing/assembly to qualify, while site choice must weigh power tariffs and logistics connectivity.

Import duties on raw materials

Customs duties on EVA, rubber, textiles and machinery materially affect Campus Activewear’s cost structure; India’s applied MFN tariff averaged about 13.5% per WTO latest published data, and specific duties on footwear inputs commonly fall in the mid-single to low-double digits, raising input costs when domestic supply is limited. Protective tariffs support local manufacturing but can inflate COGS if suppliers are thin. Scenario planning for duty shifts reduces price shock, while supplier diversification hedges geopolitical disruptions.

State-level policies and compliance

State-level policies matter: India has 28 states and 8 union territories, and industrial power tariffs, labor registration norms and local levies differ materially across them, affecting operating costs and hiring. Multi-plant footprints face distinct approvals and inspections per state, lengthening project timelines. Consolidated compliance calendars reduce penalty risk, while strong government relations speed permits and expansions.

- Labor norms vary by state

- Industrial power tariffs differ regionally

- Distinct approvals & inspections per plant

- Compliance calendars cut penalty exposure

- Good govt relations accelerate permits

Infrastructure and logistics push

Public investment under PM GatiShakti (launched 2021) and continued road, rail and freight corridor expansion shortens lead times to MBOs and EBOs, enabling Campus to reoptimize distribution centers as corridors open; India’s logistics cost remains around 13–14% of GDP, highlighting upside from better infrastructure.

- Shorter lead times

- DC network reoptimization

- Lower inventory buffers

- Improved last-mile via e‑commerce logistics

Policy: GST 5%/18%, PLI ₹1.97L cr, tariffs ~13.5% pressure margins

Political factors: GST slabs (5% ≤₹1,000; 18% >₹1,000) and input tax credit rules materially affect Campus pricing, margins and cash flow. PLI/Make in India (PLI outlay ₹1.97 lakh crore) + state subsidies can lower unit costs if local value-add targets met. Customs/MFN tariffs (~13.5%) and state power/labor variance drive COGS and site selection; PM GatiShakti reduces logistics cost exposure (logistics ≈13–14% of GDP).

| Factor | Impact | Metric (2024/25) |

|---|---|---|

| GST | Pricing, margins | 5%/18% |

| PLI | Capex subsidy | ₹1.97L cr |

| Tariffs | COGS risk | MFN ~13.5% |

| Logistics | Lead-time/cost | 13–14% GDP |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Campus Activewear, using current data and trend-driven sub-points to identify risks and opportunities; designed for executives, advisors and investors, the analysis is region- and industry-specific, formatted for decks and plans and includes forward-looking insights to support scenario planning and funding discussions.

A concise Campus Activewear PESTLE Analysis that highlights regulatory, economic, social, technological and environmental risks and opportunities, formatted for quick insertion into presentations and team planning—editable and shareable to align stakeholders and simplify external risk discussions.

Economic factors

Consumer discretionary cycles

Footwear demand in urban and semi-urban India closely follows income and employment trends; with India GDP growth near 7.2% in 2024, discretionary spend lifted premium and athleisure share, while slowdowns push consumers to value SKUs and promotions. Campus should flex pricing ladders and inventory mix between value and premium SKUs accordingly.

Input cost inflation and volatility

Input costs for Campus Activewear—EVA, rubber, synthetics, adhesives—track crude and commodity cycles (Brent averaged about 85 USD/bbl in 2024) and polymer/resin costs rose roughly 10–15% Y/Y in 2024. Inflation can compress gross margins by 100–300 bps if price pass-through lags. Hedging, formula-based contracts and material redesigns improve resilience. Ongoing cost engineering sustains competitiveness.

FX exposure and import content

Imported components and machinery create direct dollar exposure for Campus Activewear; INR traded near 83.5 per USD in mid-2025, lifting landed costs and capex budgets. INR depreciation raises input costs and compresses margins unless mitigated. Natural hedges from export receipts and using forward cover stabilize margins, while progressive localization of critical inputs reduces FX risk over time.

Interest rates and channel credit

Higher interest environment (RBI repo at 6.50% in July 2025) raises working capital costs and reduces distributor credit appetite; collections from MBOs often elongate in tight liquidity, pushing DSO higher. Dynamic discounting and fintech receivables can cut DSO by up to 15%, improving cash conversion. Align inventory to sell-through to avoid elevated carrying costs.

- repo_rate: 6.50%

- DSO_reduction_potential: up to 15%

- focus: inventory vs sell-through

Tier-2 and tier-3 market expansion

- Non-metro consumption share ~55% (2024)

- Higher price elasticity, stronger potential volumes

- Tailored assortments & regional sizing = better sell-through

- Micro-fulfillment reduces last-mile costs ~25–35%

Policy: GST 5%/18%, PLI ₹1.97L cr, tariffs ~13.5% pressure margins

GDP ~7.2% (2024) lifts premium/athleisure; slowdowns shift demand to value SKUs. Brent ~$85/bbl (2024) and polymers +10–15% Y/Y squeeze margins; hedging and cost engineering critical. INR ~83.5/USD (mid-2025) and RBI repo 6.50% (Jul 2025) raise input and WC costs; non-metro share ~55% (2024) offers volume growth with higher price elasticity.

| Metric | Value |

|---|---|

| GDP (2024) | 7.2% |

| Brent (2024) | $85/bbl |

| Polymers Δ (2024) | +10–15% Y/Y |

| INR (mid-2025) | 83.5/USD |

| RBI repo (Jul 2025) | 6.50% |

| Non-metro consumption (2024) | ~55% |

| DSO reduction potential | up to 15% |

| Last-mile savings (micro-hub) | 25–35% |

Preview Before You Purchase

Campus Activewear PESTLE Analysis

The preview shown here is the exact Campus Activewear PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with concise, actionable insights. No placeholders or teasers; the final file is available for instant download.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal and environmental forces are shaping Campus Activewear’s trajectory—our PESTLE pinpoints risks and opportunities you can act on today. Ideal for investors and strategists; purchase the full, downloadable analysis for the complete, editable report.

Political factors

GST regime and indirect tax stability

India’s GST treats footwear with MRP up to ₹1,000 at 5% (no input tax credit) and footwear above ₹1,000 at 18% (with ITC), directly influencing Campus pricing, gross margins and channel economics. Rate revisions can reallocate demand across price bands and alter working capital because input credits affect cash flow timing. Campus should monitor SKU price thresholds and structure assortments to optimize tax slabs. Engagement through CII/industry bodies can help mitigate adverse rate changes.

Make in India incentives and PLI

India’s Make in India/PLI drive (total outlay INR 1.97 lakh crore across sectors) plus duty-drawback and state capital/subsidy schemes can cut unit costs and fund capacity expansion; eligibility depends on local value-addition and export targets. Campus can realign sourcing/assembly to qualify, while site choice must weigh power tariffs and logistics connectivity.

Import duties on raw materials

Customs duties on EVA, rubber, textiles and machinery materially affect Campus Activewear’s cost structure; India’s applied MFN tariff averaged about 13.5% per WTO latest published data, and specific duties on footwear inputs commonly fall in the mid-single to low-double digits, raising input costs when domestic supply is limited. Protective tariffs support local manufacturing but can inflate COGS if suppliers are thin. Scenario planning for duty shifts reduces price shock, while supplier diversification hedges geopolitical disruptions.

State-level policies and compliance

State-level policies matter: India has 28 states and 8 union territories, and industrial power tariffs, labor registration norms and local levies differ materially across them, affecting operating costs and hiring. Multi-plant footprints face distinct approvals and inspections per state, lengthening project timelines. Consolidated compliance calendars reduce penalty risk, while strong government relations speed permits and expansions.

- Labor norms vary by state

- Industrial power tariffs differ regionally

- Distinct approvals & inspections per plant

- Compliance calendars cut penalty exposure

- Good govt relations accelerate permits

Infrastructure and logistics push

Public investment under PM GatiShakti (launched 2021) and continued road, rail and freight corridor expansion shortens lead times to MBOs and EBOs, enabling Campus to reoptimize distribution centers as corridors open; India’s logistics cost remains around 13–14% of GDP, highlighting upside from better infrastructure.

- Shorter lead times

- DC network reoptimization

- Lower inventory buffers

- Improved last-mile via e‑commerce logistics

Policy: GST 5%/18%, PLI ₹1.97L cr, tariffs ~13.5% pressure margins

Political factors: GST slabs (5% ≤₹1,000; 18% >₹1,000) and input tax credit rules materially affect Campus pricing, margins and cash flow. PLI/Make in India (PLI outlay ₹1.97 lakh crore) + state subsidies can lower unit costs if local value-add targets met. Customs/MFN tariffs (~13.5%) and state power/labor variance drive COGS and site selection; PM GatiShakti reduces logistics cost exposure (logistics ≈13–14% of GDP).

| Factor | Impact | Metric (2024/25) |

|---|---|---|

| GST | Pricing, margins | 5%/18% |

| PLI | Capex subsidy | ₹1.97L cr |

| Tariffs | COGS risk | MFN ~13.5% |

| Logistics | Lead-time/cost | 13–14% GDP |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Campus Activewear, using current data and trend-driven sub-points to identify risks and opportunities; designed for executives, advisors and investors, the analysis is region- and industry-specific, formatted for decks and plans and includes forward-looking insights to support scenario planning and funding discussions.

A concise Campus Activewear PESTLE Analysis that highlights regulatory, economic, social, technological and environmental risks and opportunities, formatted for quick insertion into presentations and team planning—editable and shareable to align stakeholders and simplify external risk discussions.

Economic factors

Consumer discretionary cycles

Footwear demand in urban and semi-urban India closely follows income and employment trends; with India GDP growth near 7.2% in 2024, discretionary spend lifted premium and athleisure share, while slowdowns push consumers to value SKUs and promotions. Campus should flex pricing ladders and inventory mix between value and premium SKUs accordingly.

Input cost inflation and volatility

Input costs for Campus Activewear—EVA, rubber, synthetics, adhesives—track crude and commodity cycles (Brent averaged about 85 USD/bbl in 2024) and polymer/resin costs rose roughly 10–15% Y/Y in 2024. Inflation can compress gross margins by 100–300 bps if price pass-through lags. Hedging, formula-based contracts and material redesigns improve resilience. Ongoing cost engineering sustains competitiveness.

FX exposure and import content

Imported components and machinery create direct dollar exposure for Campus Activewear; INR traded near 83.5 per USD in mid-2025, lifting landed costs and capex budgets. INR depreciation raises input costs and compresses margins unless mitigated. Natural hedges from export receipts and using forward cover stabilize margins, while progressive localization of critical inputs reduces FX risk over time.

Interest rates and channel credit

Higher interest environment (RBI repo at 6.50% in July 2025) raises working capital costs and reduces distributor credit appetite; collections from MBOs often elongate in tight liquidity, pushing DSO higher. Dynamic discounting and fintech receivables can cut DSO by up to 15%, improving cash conversion. Align inventory to sell-through to avoid elevated carrying costs.

- repo_rate: 6.50%

- DSO_reduction_potential: up to 15%

- focus: inventory vs sell-through

Tier-2 and tier-3 market expansion

- Non-metro consumption share ~55% (2024)

- Higher price elasticity, stronger potential volumes

- Tailored assortments & regional sizing = better sell-through

- Micro-fulfillment reduces last-mile costs ~25–35%

Policy: GST 5%/18%, PLI ₹1.97L cr, tariffs ~13.5% pressure margins

GDP ~7.2% (2024) lifts premium/athleisure; slowdowns shift demand to value SKUs. Brent ~$85/bbl (2024) and polymers +10–15% Y/Y squeeze margins; hedging and cost engineering critical. INR ~83.5/USD (mid-2025) and RBI repo 6.50% (Jul 2025) raise input and WC costs; non-metro share ~55% (2024) offers volume growth with higher price elasticity.

| Metric | Value |

|---|---|

| GDP (2024) | 7.2% |

| Brent (2024) | $85/bbl |

| Polymers Δ (2024) | +10–15% Y/Y |

| INR (mid-2025) | 83.5/USD |

| RBI repo (Jul 2025) | 6.50% |

| Non-metro consumption (2024) | ~55% |

| DSO reduction potential | up to 15% |

| Last-mile savings (micro-hub) | 25–35% |

Preview Before You Purchase

Campus Activewear PESTLE Analysis

The preview shown here is the exact Campus Activewear PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with concise, actionable insights. No placeholders or teasers; the final file is available for instant download.