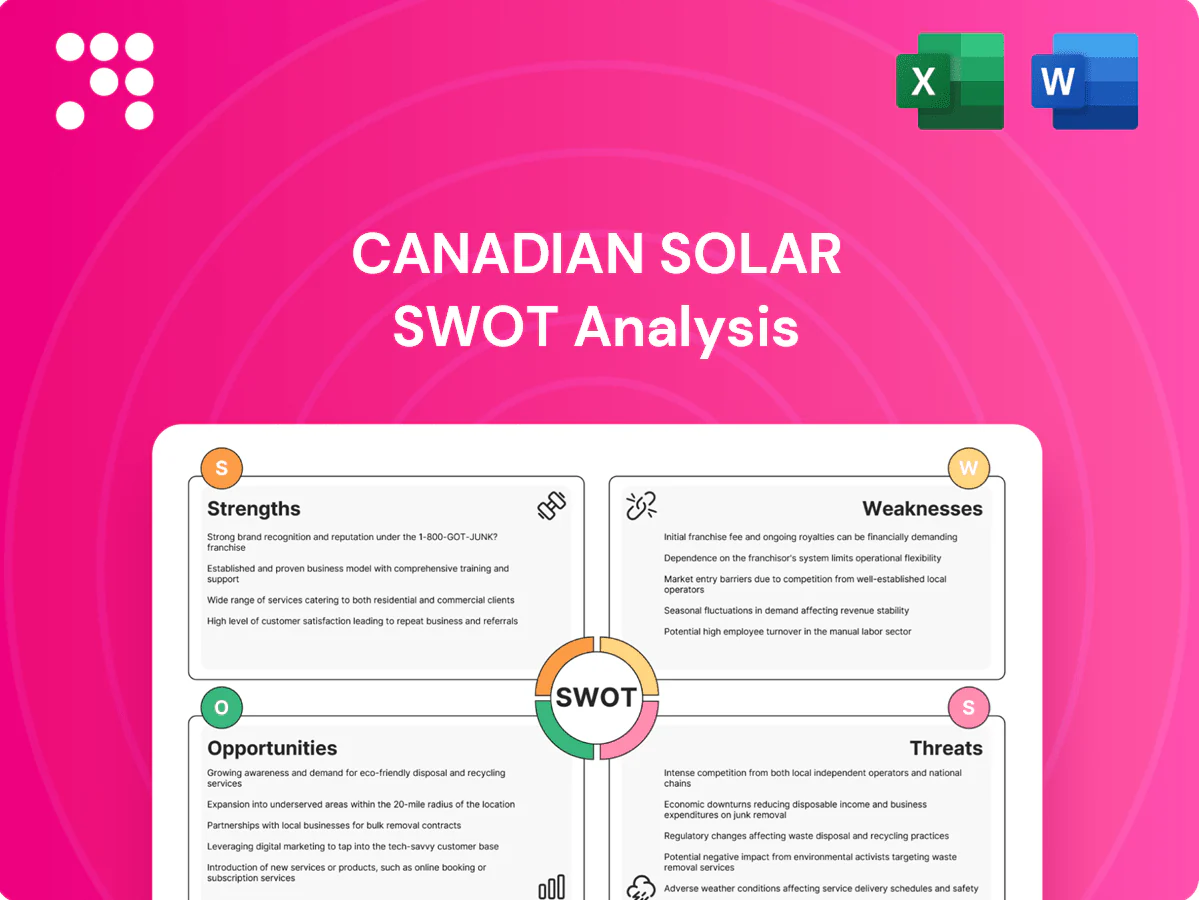

Canadian Solar SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Canadian Solar balances vertical integration and global scale with exposure to policy and supply-chain risks; innovation in module technology and a growing project pipeline are key growth drivers. Want the full picture with actionable insights, financial context, and strategic takeaways? Purchase the complete SWOT analysis to access a detailed, investor-ready report and editable Excel matrix.

Strengths

Vertically integrated

Canadian Solar, founded in 2001, designs and manufactures across the PV value chain from ingots and wafers to cells and modules, enabling tighter cost control, supply assurance, and consistent quality. Vertical integration allows faster product iteration and coordinated capacity planning, improving margins through internal sourcing and scale benefits while reducing exposure to upstream supply shocks.

Global footprint

Canadian Solar's global footprint—active in more than 150 countries since its 2001 founding and listed on NASDAQ as CSIQ—lets it sell across diversified geographies and develop projects worldwide, reducing reliance on any single market or policy regime. A broad customer base enhances resilience to regional demand swings. Global execution experience strengthens bankability with investors and lenders.

Projects + storage

Canadian Solar (NASDAQ: CSIQ) develops, builds and operates utility-scale solar plus energy storage, leveraging combined module, EPC and storage delivery to capture higher project-level value and margins. The e-STORAGE platform adds recurring revenue and grid services potential, supporting multi-GW pipeline growth reported through 2024–mid‑2025. Integrated solutions differentiate CSIQ versus module-only peers, enabling bundled EPC + O&M revenue streams per project.

Bankable brand

Founded in 2001, Canadian Solar’s 24+ years of shipment scale and proven field performance have built credibility with IPPs, utilities and financiers; that bankability lowers project financing costs and shortens sales cycles. Robust warranty support and a global service infrastructure reduce buyer risk and help secure large framework agreements.

- Founded 2001 — 24+ years

- Proven field performance — trusted by IPPs/utilities

- Bankability cuts financing costs, accelerates sales

- Warranty + global service lowers buyer risk, wins frameworks

R&D and scale

Canadian Solar invests heavily in high-efficiency TOPCon and HJT cell development and advanced manufacturing automation, enabling steady efficiency improvements that preserve competitive module ASPs and margins. Scale purchasing across global fabs reduces input cost exposure and smooths supply volatility, while formal technology roadmaps enable regular product refreshes aligned to shifting market demand.

- NASDAQ: CSIQ; TOPCon/HJT focus

Integrated solar+storage — 24+ yrs, 150+ countries

Canadian Solar (NASDAQ: CSIQ) combines vertical integration across ingots-to-modules with 24+ years' global execution in 150+ countries, improving margins, supply assurance and bankability. Integrated utility-scale + storage (e-STORAGE) drives project-level margins and recurring revenues, supporting a multi-GW pipeline and strong IPP/utility relationships.

| Metric | Value |

|---|---|

| Operating history | 24+ years |

| Geographic reach | 150+ countries |

| Listing | NASDAQ CSIQ |

| Model | Modules + EPC + Storage |

What is included in the product

Delivers a strategic overview of Canadian Solar’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position and growth prospects in the global solar and energy solutions markets.

Provides a concise SWOT matrix for Canadian Solar to accelerate strategic alignment, highlight competitive strengths and market risks, and enable rapid, presentation-ready insights for executives and investors.

Weaknesses

Margin volatility

Margin volatility is driven by falling module ASPs and swings in polysilicon and wafer costs that compress gross margins. Competitive bidding on utility-scale projects forces pricing down and squeezes project-level profitability. Earnings are cyclical and sensitive to project-sale timing, raising forecasting uncertainty for investors.

Capital intensive

Manufacturing expansions and project pipelines require significant capital expenditure, pushing Canadian Solar to allocate large sums into plants and development rather than short-term returns. Working capital is often tied up in inventory and receivables during project development, lengthening cash conversion cycles. Balance sheet leverage typically rises during build-out phases and higher financing costs when interest rates are elevated materially compress project-level returns.

Policy exposure

Policy exposure: trade actions, tariffs and U.S./EU local-content rules since 2022 raise sourcing and pricing pressures, forcing Canadian Solar to re-route supply chains and absorb higher input costs. Compliance and re‑routing add paperwork and logistics cost, while customs reviews and detentions cause delivery delays ranging from days to weeks. Profitability therefore hinges on successful navigation of evolving regulations and supply diversification.

Supply chain risk

Polysilicon, wafer and logistics constraints create recurrent bottlenecks that can delay module deliveries and compress margins for Canadian Solar; vendor concentration for key inputs increases disruption risk. Currency fluctuations across CAD, USD and EUR add margin volatility in global sales. Scaling warranty claims or quality issues could generate significant liabilities and reputational damage.

- Supply bottlenecks: polysilicon/wafer/logistics

- Vendor concentration: single-source risk

- Currency exposure: CAD/USD/EUR impacts

- Warranty/quality: liability at scale

Project timing

Revenue recognition from Canadian Solar project sales is lumpy, as permitting, interconnection and grid upgrade delays frequently slip schedules and compress deliveries, creating quarter-to-quarter variability and causing cash flows to bunch around milestone completions.

- Timing risk

- Quarterly volatility

- Milestone cash bunching

Falling ASPs, big capex and supplier constraints squeeze margins and spike timing risk

Margin volatility from falling module ASPs and upstream cost swings compresses profitability and increases forecasting risk. Large capex for fabs and project pipelines lengthens cash conversion and raises leverage during build-outs. Trade rules, supplier concentration and project timing cause delivery delays, warranty risk and quarter-to-quarter revenue bunching.

| Key | Impact |

|---|---|

| Margin volatility | High |

What You See Is What You Get

Canadian Solar SWOT Analysis

This is the actual Canadian Solar SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, ready for download once payment is completed.

Dive Deeper Into the Company’s Strategic Blueprint

Canadian Solar balances vertical integration and global scale with exposure to policy and supply-chain risks; innovation in module technology and a growing project pipeline are key growth drivers. Want the full picture with actionable insights, financial context, and strategic takeaways? Purchase the complete SWOT analysis to access a detailed, investor-ready report and editable Excel matrix.

Strengths

Vertically integrated

Canadian Solar, founded in 2001, designs and manufactures across the PV value chain from ingots and wafers to cells and modules, enabling tighter cost control, supply assurance, and consistent quality. Vertical integration allows faster product iteration and coordinated capacity planning, improving margins through internal sourcing and scale benefits while reducing exposure to upstream supply shocks.

Global footprint

Canadian Solar's global footprint—active in more than 150 countries since its 2001 founding and listed on NASDAQ as CSIQ—lets it sell across diversified geographies and develop projects worldwide, reducing reliance on any single market or policy regime. A broad customer base enhances resilience to regional demand swings. Global execution experience strengthens bankability with investors and lenders.

Projects + storage

Canadian Solar (NASDAQ: CSIQ) develops, builds and operates utility-scale solar plus energy storage, leveraging combined module, EPC and storage delivery to capture higher project-level value and margins. The e-STORAGE platform adds recurring revenue and grid services potential, supporting multi-GW pipeline growth reported through 2024–mid‑2025. Integrated solutions differentiate CSIQ versus module-only peers, enabling bundled EPC + O&M revenue streams per project.

Bankable brand

Founded in 2001, Canadian Solar’s 24+ years of shipment scale and proven field performance have built credibility with IPPs, utilities and financiers; that bankability lowers project financing costs and shortens sales cycles. Robust warranty support and a global service infrastructure reduce buyer risk and help secure large framework agreements.

- Founded 2001 — 24+ years

- Proven field performance — trusted by IPPs/utilities

- Bankability cuts financing costs, accelerates sales

- Warranty + global service lowers buyer risk, wins frameworks

R&D and scale

Canadian Solar invests heavily in high-efficiency TOPCon and HJT cell development and advanced manufacturing automation, enabling steady efficiency improvements that preserve competitive module ASPs and margins. Scale purchasing across global fabs reduces input cost exposure and smooths supply volatility, while formal technology roadmaps enable regular product refreshes aligned to shifting market demand.

- NASDAQ: CSIQ; TOPCon/HJT focus

Integrated solar+storage — 24+ yrs, 150+ countries

Canadian Solar (NASDAQ: CSIQ) combines vertical integration across ingots-to-modules with 24+ years' global execution in 150+ countries, improving margins, supply assurance and bankability. Integrated utility-scale + storage (e-STORAGE) drives project-level margins and recurring revenues, supporting a multi-GW pipeline and strong IPP/utility relationships.

| Metric | Value |

|---|---|

| Operating history | 24+ years |

| Geographic reach | 150+ countries |

| Listing | NASDAQ CSIQ |

| Model | Modules + EPC + Storage |

What is included in the product

Delivers a strategic overview of Canadian Solar’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position and growth prospects in the global solar and energy solutions markets.

Provides a concise SWOT matrix for Canadian Solar to accelerate strategic alignment, highlight competitive strengths and market risks, and enable rapid, presentation-ready insights for executives and investors.

Weaknesses

Margin volatility

Margin volatility is driven by falling module ASPs and swings in polysilicon and wafer costs that compress gross margins. Competitive bidding on utility-scale projects forces pricing down and squeezes project-level profitability. Earnings are cyclical and sensitive to project-sale timing, raising forecasting uncertainty for investors.

Capital intensive

Manufacturing expansions and project pipelines require significant capital expenditure, pushing Canadian Solar to allocate large sums into plants and development rather than short-term returns. Working capital is often tied up in inventory and receivables during project development, lengthening cash conversion cycles. Balance sheet leverage typically rises during build-out phases and higher financing costs when interest rates are elevated materially compress project-level returns.

Policy exposure

Policy exposure: trade actions, tariffs and U.S./EU local-content rules since 2022 raise sourcing and pricing pressures, forcing Canadian Solar to re-route supply chains and absorb higher input costs. Compliance and re‑routing add paperwork and logistics cost, while customs reviews and detentions cause delivery delays ranging from days to weeks. Profitability therefore hinges on successful navigation of evolving regulations and supply diversification.

Supply chain risk

Polysilicon, wafer and logistics constraints create recurrent bottlenecks that can delay module deliveries and compress margins for Canadian Solar; vendor concentration for key inputs increases disruption risk. Currency fluctuations across CAD, USD and EUR add margin volatility in global sales. Scaling warranty claims or quality issues could generate significant liabilities and reputational damage.

- Supply bottlenecks: polysilicon/wafer/logistics

- Vendor concentration: single-source risk

- Currency exposure: CAD/USD/EUR impacts

- Warranty/quality: liability at scale

Project timing

Revenue recognition from Canadian Solar project sales is lumpy, as permitting, interconnection and grid upgrade delays frequently slip schedules and compress deliveries, creating quarter-to-quarter variability and causing cash flows to bunch around milestone completions.

- Timing risk

- Quarterly volatility

- Milestone cash bunching

Falling ASPs, big capex and supplier constraints squeeze margins and spike timing risk

Margin volatility from falling module ASPs and upstream cost swings compresses profitability and increases forecasting risk. Large capex for fabs and project pipelines lengthens cash conversion and raises leverage during build-outs. Trade rules, supplier concentration and project timing cause delivery delays, warranty risk and quarter-to-quarter revenue bunching.

| Key | Impact |

|---|---|

| Margin volatility | High |

What You See Is What You Get

Canadian Solar SWOT Analysis

This is the actual Canadian Solar SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, ready for download once payment is completed.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Canadian Solar balances vertical integration and global scale with exposure to policy and supply-chain risks; innovation in module technology and a growing project pipeline are key growth drivers. Want the full picture with actionable insights, financial context, and strategic takeaways? Purchase the complete SWOT analysis to access a detailed, investor-ready report and editable Excel matrix.

Strengths

Vertically integrated

Canadian Solar, founded in 2001, designs and manufactures across the PV value chain from ingots and wafers to cells and modules, enabling tighter cost control, supply assurance, and consistent quality. Vertical integration allows faster product iteration and coordinated capacity planning, improving margins through internal sourcing and scale benefits while reducing exposure to upstream supply shocks.

Global footprint

Canadian Solar's global footprint—active in more than 150 countries since its 2001 founding and listed on NASDAQ as CSIQ—lets it sell across diversified geographies and develop projects worldwide, reducing reliance on any single market or policy regime. A broad customer base enhances resilience to regional demand swings. Global execution experience strengthens bankability with investors and lenders.

Projects + storage

Canadian Solar (NASDAQ: CSIQ) develops, builds and operates utility-scale solar plus energy storage, leveraging combined module, EPC and storage delivery to capture higher project-level value and margins. The e-STORAGE platform adds recurring revenue and grid services potential, supporting multi-GW pipeline growth reported through 2024–mid‑2025. Integrated solutions differentiate CSIQ versus module-only peers, enabling bundled EPC + O&M revenue streams per project.

Bankable brand

Founded in 2001, Canadian Solar’s 24+ years of shipment scale and proven field performance have built credibility with IPPs, utilities and financiers; that bankability lowers project financing costs and shortens sales cycles. Robust warranty support and a global service infrastructure reduce buyer risk and help secure large framework agreements.

- Founded 2001 — 24+ years

- Proven field performance — trusted by IPPs/utilities

- Bankability cuts financing costs, accelerates sales

- Warranty + global service lowers buyer risk, wins frameworks

R&D and scale

Canadian Solar invests heavily in high-efficiency TOPCon and HJT cell development and advanced manufacturing automation, enabling steady efficiency improvements that preserve competitive module ASPs and margins. Scale purchasing across global fabs reduces input cost exposure and smooths supply volatility, while formal technology roadmaps enable regular product refreshes aligned to shifting market demand.

- NASDAQ: CSIQ; TOPCon/HJT focus

Integrated solar+storage — 24+ yrs, 150+ countries

Canadian Solar (NASDAQ: CSIQ) combines vertical integration across ingots-to-modules with 24+ years' global execution in 150+ countries, improving margins, supply assurance and bankability. Integrated utility-scale + storage (e-STORAGE) drives project-level margins and recurring revenues, supporting a multi-GW pipeline and strong IPP/utility relationships.

| Metric | Value |

|---|---|

| Operating history | 24+ years |

| Geographic reach | 150+ countries |

| Listing | NASDAQ CSIQ |

| Model | Modules + EPC + Storage |

What is included in the product

Delivers a strategic overview of Canadian Solar’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position and growth prospects in the global solar and energy solutions markets.

Provides a concise SWOT matrix for Canadian Solar to accelerate strategic alignment, highlight competitive strengths and market risks, and enable rapid, presentation-ready insights for executives and investors.

Weaknesses

Margin volatility

Margin volatility is driven by falling module ASPs and swings in polysilicon and wafer costs that compress gross margins. Competitive bidding on utility-scale projects forces pricing down and squeezes project-level profitability. Earnings are cyclical and sensitive to project-sale timing, raising forecasting uncertainty for investors.

Capital intensive

Manufacturing expansions and project pipelines require significant capital expenditure, pushing Canadian Solar to allocate large sums into plants and development rather than short-term returns. Working capital is often tied up in inventory and receivables during project development, lengthening cash conversion cycles. Balance sheet leverage typically rises during build-out phases and higher financing costs when interest rates are elevated materially compress project-level returns.

Policy exposure

Policy exposure: trade actions, tariffs and U.S./EU local-content rules since 2022 raise sourcing and pricing pressures, forcing Canadian Solar to re-route supply chains and absorb higher input costs. Compliance and re‑routing add paperwork and logistics cost, while customs reviews and detentions cause delivery delays ranging from days to weeks. Profitability therefore hinges on successful navigation of evolving regulations and supply diversification.

Supply chain risk

Polysilicon, wafer and logistics constraints create recurrent bottlenecks that can delay module deliveries and compress margins for Canadian Solar; vendor concentration for key inputs increases disruption risk. Currency fluctuations across CAD, USD and EUR add margin volatility in global sales. Scaling warranty claims or quality issues could generate significant liabilities and reputational damage.

- Supply bottlenecks: polysilicon/wafer/logistics

- Vendor concentration: single-source risk

- Currency exposure: CAD/USD/EUR impacts

- Warranty/quality: liability at scale

Project timing

Revenue recognition from Canadian Solar project sales is lumpy, as permitting, interconnection and grid upgrade delays frequently slip schedules and compress deliveries, creating quarter-to-quarter variability and causing cash flows to bunch around milestone completions.

- Timing risk

- Quarterly volatility

- Milestone cash bunching

Falling ASPs, big capex and supplier constraints squeeze margins and spike timing risk

Margin volatility from falling module ASPs and upstream cost swings compresses profitability and increases forecasting risk. Large capex for fabs and project pipelines lengthens cash conversion and raises leverage during build-outs. Trade rules, supplier concentration and project timing cause delivery delays, warranty risk and quarter-to-quarter revenue bunching.

| Key | Impact |

|---|---|

| Margin volatility | High |

What You See Is What You Get

Canadian Solar SWOT Analysis

This is the actual Canadian Solar SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, ready for download once payment is completed.