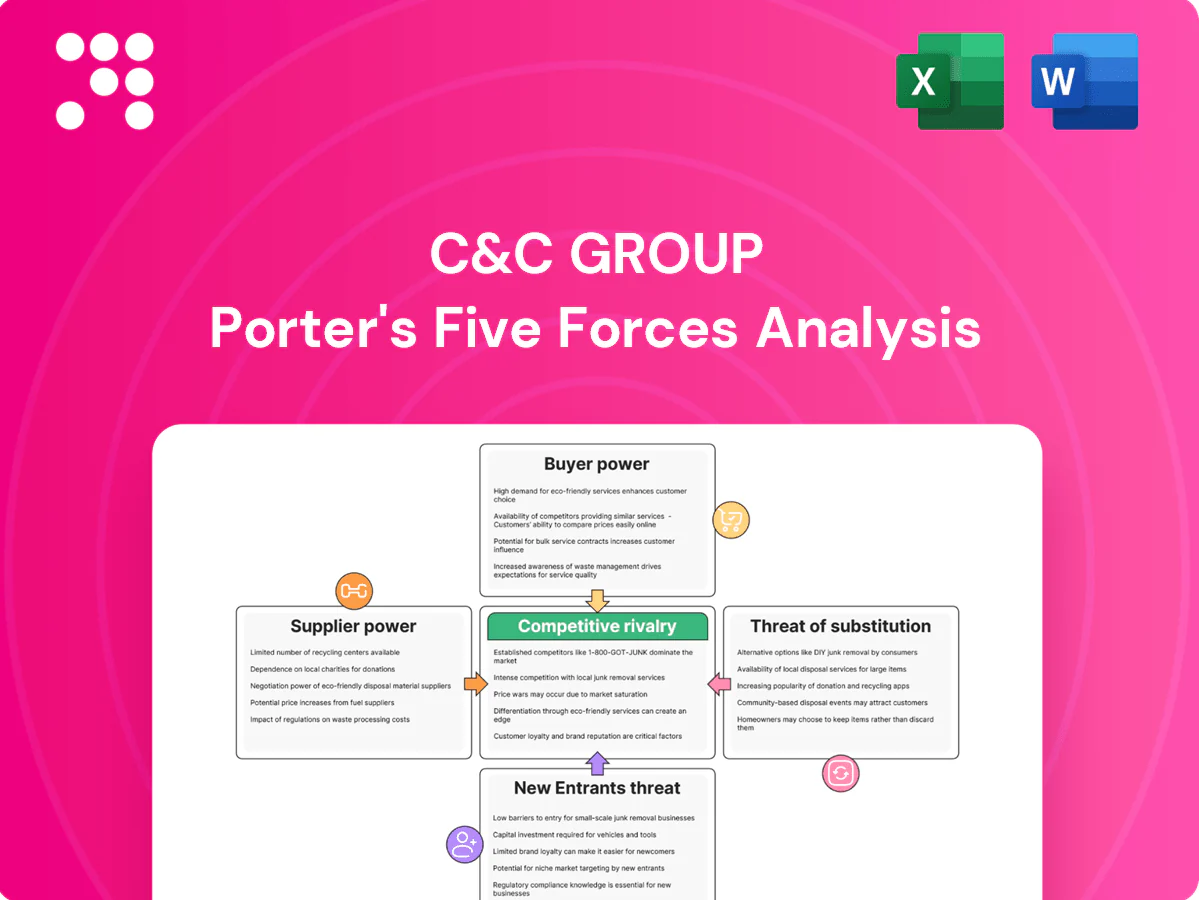

C&C Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

C&C Group faces moderate supplier power, intense retail competition, and evolving substitute threats that pressure margins and strategic positioning. This snapshot highlights key tensions but leaves force-by-force ratings and scenarios unexplored. Unlock the full Porter's Five Forces Analysis to gain the detailed insights and visuals needed to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated raw material sources

Apples for cider, malting barley and quality hops are sourced from concentrated regions and specialist growers, and 2024 saw harvest volatility that tightened availability and raised input leverage. Long-term contracts mitigate short-term spikes, but specialty varieties and strict quality specs limit easy switching. C&C’s scale provides bargaining weight but does not eliminate supplier influence.

Packaging and energy cost volatility

Glass, aluminium cans, cartons and energy are dominated by a few global suppliers, and 2024 market tightness has sustained cyclical pricing power that can quickly raise input costs. Input inflation — historically able to lift packaging-related COGS by double digits at peaks — can compress margins unless hedged or passed through. Switching formats needs capex and lead times, keeping supplier leverage high, while energy surcharges and episodic CO2 shortages add periodic pressure.

Logistics and distribution dependencies

Haulage, warehousing and last-mile services for C&C face capacity swings and labor constraints, with UK HGV driver shortages estimated at c.60,000 in 2024, tightening supply chains. Fuel price volatility—Brent averaging about $85/barrel in 2024—plus regulatory shifts (emissions rules) strengthen transport providers’ bargaining position. Peak seasonality (summer, holidays) can push spot rates up c.20-30%, further tightening capacity. C&C’s owned distribution reduces but does not eliminate exposure to these cost and capacity shocks.

Specialty ingredients and adjuncts

Specialty yeast strains, flavorings and no/low-alcohol inputs are supplied by a small pool of qualified vendors, raising supplier bargaining power for C&C due to strict compliance and batch-consistency demands. Limited substitution increases risk: single-source disruptions can delay multiple SKUs and damage seasonal availability. Strategic supplier partnerships and dual-sourcing are therefore critical to dilute leverage and protect continuity.

- niche vendors restrict substitution

- compliance drives consistency needs

- single disruptions ripple across SKUs

- partnerships and dual-sourcing reduce supplier power

Sustainability and compliance requirements

Rising ESG standards demand full traceability and recyclable packaging, narrowing supplier pools and concentrating spend with certified vendors; EU/UK 2024 packaging rules target around 65% recycling rates, tightening sourcing options.

Higher compliance and audit costs are often passed to buyers, raising C&C Group input costs and reducing margin flexibility.

Certifications and audits lengthen switching times, increasing effective supplier power for compliant vendors.

- Supplier concentration: higher

- Compliance cost pass-through: likely

- Switching flexibility: reduced

- Effective supplier power: increased

Supplier power tightens: Brent $85, HGV ~60k, EU/UK ~65% recycling

Supplier power is elevated: concentrated growers and packaging suppliers tightened availability in 2024 (harvest volatility, Brent ~$85/bbl), raising input leverage. Logistics capacity strain (UK HGV short ~60,000) and specialty inputs (single-source yeast/flavors) constrain switching. ESG rules (EU/UK ~65% recycling target) further narrow vendor pool, so C&C’s scale reduces but does not remove supplier influence.

| Metric | 2024 |

|---|---|

| Brent oil | $85/bbl |

| UK HGV shortage | ~60,000 |

| EU/UK recycling target | ~65% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to C&C Group, evaluating supplier/buyer power, threat of substitutes, competitive rivalry and barriers to entry; highlights disruptive forces and strategic implications for pricing, profitability and market share.

A concise one-sheet Porter's Five Forces for C&C Group that instantly highlights supplier, buyer, rivalry, entrant and substitute pressures with a customizable spider chart—easy to update for regulatory or market shifts and export-ready for decks or reports.

Customers Bargaining Power

Concentrated retail and pub chains

Grocery multiples in the UK and Ireland command shelf access, with the top grocers accounting for roughly two-thirds of UK grocery sales in 2024 (≈67%), while large pub groups concentrate tap access. They negotiate aggressively on price, promotions and payment terms, using delist threat and space allocation as leverage. C&C must trade off tighter terms against portfolio breadth and SKU velocity to protect revenue and margins.

Low switching costs for consumers

Low switching costs mean shoppers bounce between cider and beer for taste or deals; Kantar 2024 shows promotional penetration in UK grocery at about 33%, driving volume migration via price promos and multipacks. Limited differentiation in mainstream cider/beer segments amplifies buyer leverage, and while strong brands (e.g., Magners) retain premium pockets, brand equity cannot fully offset pervasive deal sensitivity.

Private label and exclusive SKUs

By 2024 retailers expanded own-label cider and beer ranges, intensifying price comparisons and compressing branded price elasticity. Exclusive SKUs demand margin trade-offs for shelf placement, reducing route-to-market profitability for C&C. This dynamic erodes branded pricing power and forces C&C to invest in product innovation and marketing to justify premium space and protect margins.

Data-driven category management

Buyers leverage POS data to refine category mix and demand funded activations, shifting promotional risk onto suppliers via performance-based terms; underperforming SKUs are rapidly delisted as retailers prioritize shelf velocity. C&C must demonstrate strong execution, high velocity metrics and measurable ROI to retain bargaining leverage and avoid margin pressure from contingent payments.

- POS-driven assortment

- Performance-based terms

- Rapid SKU rotation

- Execution & velocity = leverage

On-trade pour rights and incentives

Pub groups negotiate tap contracts, equipment support and rebates that can swing regional volumes; winning or losing a pour can change local supply by tens of thousands of litres and C&C's on-trade route-to-market (salesforce + distributors) secures taps but increases operating cost and trade promotion spend.

Competitive bidding for pour rights compresses gross margins and forces higher promotional rebates; in 2024 UK pub estate remained around 46,000 sites, keeping competition intense for limited taps.

- Tap contracts: 3–5 year typical terms

- Volume swing: tens of thousands of litres per lost/won pour

- Cost: higher field sales and promo spend to defend taps

- Market context: ~46,000 UK pubs (2024)

Grocers' dominance (≈67%) and pub tap deals squeeze branded margins

Retailers and pub groups hold strong leverage: top grocers = ≈67% UK grocery sales (2024), promo penetration ≈33% (Kantar 2024) and ~46,000 UK pubs (2024). Low switching costs and own-label expansion compress branded pricing; pub tap contracts (typ. 3–5 yrs) and performance terms force higher promo/rebate spend and rapid SKU delisting, pressuring C&C margins.

| Metric | 2024 |

|---|---|

| Top grocers share | ≈67% |

| Promo penetration | ≈33% |

| UK pubs | ≈46,000 |

| Tap contract term | 3–5 yrs |

What You See Is What You Get

C&C Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of C&C Group you'll receive immediately after purchase—no placeholders or mockups. It is the final, professionally formatted document, ready for download and use the moment you buy. What you see is precisely what you'll get.

From Overview to Strategy Blueprint

C&C Group faces moderate supplier power, intense retail competition, and evolving substitute threats that pressure margins and strategic positioning. This snapshot highlights key tensions but leaves force-by-force ratings and scenarios unexplored. Unlock the full Porter's Five Forces Analysis to gain the detailed insights and visuals needed to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated raw material sources

Apples for cider, malting barley and quality hops are sourced from concentrated regions and specialist growers, and 2024 saw harvest volatility that tightened availability and raised input leverage. Long-term contracts mitigate short-term spikes, but specialty varieties and strict quality specs limit easy switching. C&C’s scale provides bargaining weight but does not eliminate supplier influence.

Packaging and energy cost volatility

Glass, aluminium cans, cartons and energy are dominated by a few global suppliers, and 2024 market tightness has sustained cyclical pricing power that can quickly raise input costs. Input inflation — historically able to lift packaging-related COGS by double digits at peaks — can compress margins unless hedged or passed through. Switching formats needs capex and lead times, keeping supplier leverage high, while energy surcharges and episodic CO2 shortages add periodic pressure.

Logistics and distribution dependencies

Haulage, warehousing and last-mile services for C&C face capacity swings and labor constraints, with UK HGV driver shortages estimated at c.60,000 in 2024, tightening supply chains. Fuel price volatility—Brent averaging about $85/barrel in 2024—plus regulatory shifts (emissions rules) strengthen transport providers’ bargaining position. Peak seasonality (summer, holidays) can push spot rates up c.20-30%, further tightening capacity. C&C’s owned distribution reduces but does not eliminate exposure to these cost and capacity shocks.

Specialty ingredients and adjuncts

Specialty yeast strains, flavorings and no/low-alcohol inputs are supplied by a small pool of qualified vendors, raising supplier bargaining power for C&C due to strict compliance and batch-consistency demands. Limited substitution increases risk: single-source disruptions can delay multiple SKUs and damage seasonal availability. Strategic supplier partnerships and dual-sourcing are therefore critical to dilute leverage and protect continuity.

- niche vendors restrict substitution

- compliance drives consistency needs

- single disruptions ripple across SKUs

- partnerships and dual-sourcing reduce supplier power

Sustainability and compliance requirements

Rising ESG standards demand full traceability and recyclable packaging, narrowing supplier pools and concentrating spend with certified vendors; EU/UK 2024 packaging rules target around 65% recycling rates, tightening sourcing options.

Higher compliance and audit costs are often passed to buyers, raising C&C Group input costs and reducing margin flexibility.

Certifications and audits lengthen switching times, increasing effective supplier power for compliant vendors.

- Supplier concentration: higher

- Compliance cost pass-through: likely

- Switching flexibility: reduced

- Effective supplier power: increased

Supplier power tightens: Brent $85, HGV ~60k, EU/UK ~65% recycling

Supplier power is elevated: concentrated growers and packaging suppliers tightened availability in 2024 (harvest volatility, Brent ~$85/bbl), raising input leverage. Logistics capacity strain (UK HGV short ~60,000) and specialty inputs (single-source yeast/flavors) constrain switching. ESG rules (EU/UK ~65% recycling target) further narrow vendor pool, so C&C’s scale reduces but does not remove supplier influence.

| Metric | 2024 |

|---|---|

| Brent oil | $85/bbl |

| UK HGV shortage | ~60,000 |

| EU/UK recycling target | ~65% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to C&C Group, evaluating supplier/buyer power, threat of substitutes, competitive rivalry and barriers to entry; highlights disruptive forces and strategic implications for pricing, profitability and market share.

A concise one-sheet Porter's Five Forces for C&C Group that instantly highlights supplier, buyer, rivalry, entrant and substitute pressures with a customizable spider chart—easy to update for regulatory or market shifts and export-ready for decks or reports.

Customers Bargaining Power

Concentrated retail and pub chains

Grocery multiples in the UK and Ireland command shelf access, with the top grocers accounting for roughly two-thirds of UK grocery sales in 2024 (≈67%), while large pub groups concentrate tap access. They negotiate aggressively on price, promotions and payment terms, using delist threat and space allocation as leverage. C&C must trade off tighter terms against portfolio breadth and SKU velocity to protect revenue and margins.

Low switching costs for consumers

Low switching costs mean shoppers bounce between cider and beer for taste or deals; Kantar 2024 shows promotional penetration in UK grocery at about 33%, driving volume migration via price promos and multipacks. Limited differentiation in mainstream cider/beer segments amplifies buyer leverage, and while strong brands (e.g., Magners) retain premium pockets, brand equity cannot fully offset pervasive deal sensitivity.

Private label and exclusive SKUs

By 2024 retailers expanded own-label cider and beer ranges, intensifying price comparisons and compressing branded price elasticity. Exclusive SKUs demand margin trade-offs for shelf placement, reducing route-to-market profitability for C&C. This dynamic erodes branded pricing power and forces C&C to invest in product innovation and marketing to justify premium space and protect margins.

Data-driven category management

Buyers leverage POS data to refine category mix and demand funded activations, shifting promotional risk onto suppliers via performance-based terms; underperforming SKUs are rapidly delisted as retailers prioritize shelf velocity. C&C must demonstrate strong execution, high velocity metrics and measurable ROI to retain bargaining leverage and avoid margin pressure from contingent payments.

- POS-driven assortment

- Performance-based terms

- Rapid SKU rotation

- Execution & velocity = leverage

On-trade pour rights and incentives

Pub groups negotiate tap contracts, equipment support and rebates that can swing regional volumes; winning or losing a pour can change local supply by tens of thousands of litres and C&C's on-trade route-to-market (salesforce + distributors) secures taps but increases operating cost and trade promotion spend.

Competitive bidding for pour rights compresses gross margins and forces higher promotional rebates; in 2024 UK pub estate remained around 46,000 sites, keeping competition intense for limited taps.

- Tap contracts: 3–5 year typical terms

- Volume swing: tens of thousands of litres per lost/won pour

- Cost: higher field sales and promo spend to defend taps

- Market context: ~46,000 UK pubs (2024)

Grocers' dominance (≈67%) and pub tap deals squeeze branded margins

Retailers and pub groups hold strong leverage: top grocers = ≈67% UK grocery sales (2024), promo penetration ≈33% (Kantar 2024) and ~46,000 UK pubs (2024). Low switching costs and own-label expansion compress branded pricing; pub tap contracts (typ. 3–5 yrs) and performance terms force higher promo/rebate spend and rapid SKU delisting, pressuring C&C margins.

| Metric | 2024 |

|---|---|

| Top grocers share | ≈67% |

| Promo penetration | ≈33% |

| UK pubs | ≈46,000 |

| Tap contract term | 3–5 yrs |

What You See Is What You Get

C&C Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of C&C Group you'll receive immediately after purchase—no placeholders or mockups. It is the final, professionally formatted document, ready for download and use the moment you buy. What you see is precisely what you'll get.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

C&C Group faces moderate supplier power, intense retail competition, and evolving substitute threats that pressure margins and strategic positioning. This snapshot highlights key tensions but leaves force-by-force ratings and scenarios unexplored. Unlock the full Porter's Five Forces Analysis to gain the detailed insights and visuals needed to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated raw material sources

Apples for cider, malting barley and quality hops are sourced from concentrated regions and specialist growers, and 2024 saw harvest volatility that tightened availability and raised input leverage. Long-term contracts mitigate short-term spikes, but specialty varieties and strict quality specs limit easy switching. C&C’s scale provides bargaining weight but does not eliminate supplier influence.

Packaging and energy cost volatility

Glass, aluminium cans, cartons and energy are dominated by a few global suppliers, and 2024 market tightness has sustained cyclical pricing power that can quickly raise input costs. Input inflation — historically able to lift packaging-related COGS by double digits at peaks — can compress margins unless hedged or passed through. Switching formats needs capex and lead times, keeping supplier leverage high, while energy surcharges and episodic CO2 shortages add periodic pressure.

Logistics and distribution dependencies

Haulage, warehousing and last-mile services for C&C face capacity swings and labor constraints, with UK HGV driver shortages estimated at c.60,000 in 2024, tightening supply chains. Fuel price volatility—Brent averaging about $85/barrel in 2024—plus regulatory shifts (emissions rules) strengthen transport providers’ bargaining position. Peak seasonality (summer, holidays) can push spot rates up c.20-30%, further tightening capacity. C&C’s owned distribution reduces but does not eliminate exposure to these cost and capacity shocks.

Specialty ingredients and adjuncts

Specialty yeast strains, flavorings and no/low-alcohol inputs are supplied by a small pool of qualified vendors, raising supplier bargaining power for C&C due to strict compliance and batch-consistency demands. Limited substitution increases risk: single-source disruptions can delay multiple SKUs and damage seasonal availability. Strategic supplier partnerships and dual-sourcing are therefore critical to dilute leverage and protect continuity.

- niche vendors restrict substitution

- compliance drives consistency needs

- single disruptions ripple across SKUs

- partnerships and dual-sourcing reduce supplier power

Sustainability and compliance requirements

Rising ESG standards demand full traceability and recyclable packaging, narrowing supplier pools and concentrating spend with certified vendors; EU/UK 2024 packaging rules target around 65% recycling rates, tightening sourcing options.

Higher compliance and audit costs are often passed to buyers, raising C&C Group input costs and reducing margin flexibility.

Certifications and audits lengthen switching times, increasing effective supplier power for compliant vendors.

- Supplier concentration: higher

- Compliance cost pass-through: likely

- Switching flexibility: reduced

- Effective supplier power: increased

Supplier power tightens: Brent $85, HGV ~60k, EU/UK ~65% recycling

Supplier power is elevated: concentrated growers and packaging suppliers tightened availability in 2024 (harvest volatility, Brent ~$85/bbl), raising input leverage. Logistics capacity strain (UK HGV short ~60,000) and specialty inputs (single-source yeast/flavors) constrain switching. ESG rules (EU/UK ~65% recycling target) further narrow vendor pool, so C&C’s scale reduces but does not remove supplier influence.

| Metric | 2024 |

|---|---|

| Brent oil | $85/bbl |

| UK HGV shortage | ~60,000 |

| EU/UK recycling target | ~65% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to C&C Group, evaluating supplier/buyer power, threat of substitutes, competitive rivalry and barriers to entry; highlights disruptive forces and strategic implications for pricing, profitability and market share.

A concise one-sheet Porter's Five Forces for C&C Group that instantly highlights supplier, buyer, rivalry, entrant and substitute pressures with a customizable spider chart—easy to update for regulatory or market shifts and export-ready for decks or reports.

Customers Bargaining Power

Concentrated retail and pub chains

Grocery multiples in the UK and Ireland command shelf access, with the top grocers accounting for roughly two-thirds of UK grocery sales in 2024 (≈67%), while large pub groups concentrate tap access. They negotiate aggressively on price, promotions and payment terms, using delist threat and space allocation as leverage. C&C must trade off tighter terms against portfolio breadth and SKU velocity to protect revenue and margins.

Low switching costs for consumers

Low switching costs mean shoppers bounce between cider and beer for taste or deals; Kantar 2024 shows promotional penetration in UK grocery at about 33%, driving volume migration via price promos and multipacks. Limited differentiation in mainstream cider/beer segments amplifies buyer leverage, and while strong brands (e.g., Magners) retain premium pockets, brand equity cannot fully offset pervasive deal sensitivity.

Private label and exclusive SKUs

By 2024 retailers expanded own-label cider and beer ranges, intensifying price comparisons and compressing branded price elasticity. Exclusive SKUs demand margin trade-offs for shelf placement, reducing route-to-market profitability for C&C. This dynamic erodes branded pricing power and forces C&C to invest in product innovation and marketing to justify premium space and protect margins.

Data-driven category management

Buyers leverage POS data to refine category mix and demand funded activations, shifting promotional risk onto suppliers via performance-based terms; underperforming SKUs are rapidly delisted as retailers prioritize shelf velocity. C&C must demonstrate strong execution, high velocity metrics and measurable ROI to retain bargaining leverage and avoid margin pressure from contingent payments.

- POS-driven assortment

- Performance-based terms

- Rapid SKU rotation

- Execution & velocity = leverage

On-trade pour rights and incentives

Pub groups negotiate tap contracts, equipment support and rebates that can swing regional volumes; winning or losing a pour can change local supply by tens of thousands of litres and C&C's on-trade route-to-market (salesforce + distributors) secures taps but increases operating cost and trade promotion spend.

Competitive bidding for pour rights compresses gross margins and forces higher promotional rebates; in 2024 UK pub estate remained around 46,000 sites, keeping competition intense for limited taps.

- Tap contracts: 3–5 year typical terms

- Volume swing: tens of thousands of litres per lost/won pour

- Cost: higher field sales and promo spend to defend taps

- Market context: ~46,000 UK pubs (2024)

Grocers' dominance (≈67%) and pub tap deals squeeze branded margins

Retailers and pub groups hold strong leverage: top grocers = ≈67% UK grocery sales (2024), promo penetration ≈33% (Kantar 2024) and ~46,000 UK pubs (2024). Low switching costs and own-label expansion compress branded pricing; pub tap contracts (typ. 3–5 yrs) and performance terms force higher promo/rebate spend and rapid SKU delisting, pressuring C&C margins.

| Metric | 2024 |

|---|---|

| Top grocers share | ≈67% |

| Promo penetration | ≈33% |

| UK pubs | ≈46,000 |

| Tap contract term | 3–5 yrs |

What You See Is What You Get

C&C Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of C&C Group you'll receive immediately after purchase—no placeholders or mockups. It is the final, professionally formatted document, ready for download and use the moment you buy. What you see is precisely what you'll get.