C&C Group SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Our C&C Group SWOT preview highlights core strengths, market risks, and key growth drivers shaping its outlook; the full report expands these into actionable strategies and financial context. Purchase the complete SWOT to receive a professionally written, editable Word report plus an Excel model—ideal for investors, advisors, and strategists.

Strengths

Iconic cider and beer brands

Flagship labels Bulmers, Magners and Tennent’s drive high awareness and repeat purchase, supporting C&C’s c.€1.0bn revenue in FY2024 and reinforcing category leadership in cider that secures pricing power and premium shelf space.

End-to-end supply chain control

Ownership from production to distribution improves quality, service and margin capture; C&C reported FY 2024 revenue of €1.05bn, supporting reinvestment across the chain. Vertical integration gives agility to align brewing and cider-making with demand swings, shortening lead times. Route-to-market data feedback loops inform planning and innovation, while reduced third-party dependency limits supply disruption risk.

Diverse route-to-market coverage

Strong presence across on-trade and off-trade in Ireland, Great Britain and export markets enhances resilience; established relationships with pubs, bars and major retailers secure shelf and draught placements. Consistent point-of-sale execution drives rotation and promotions, while broad channel coverage enables rapid product launches and targeted assortments to specific trade segments.

Multi-category portfolio breadth

Multi-category portfolio gives C&C balanced exposure across mainstream, premium and craft ranges, supporting trading-up and cross-selling across on- and off-trade channels; FY2024 group revenue was €1.03bn, underscoring scale. The range lets C&C address varied consumer occasions and price tiers, reducing dependence on any single brand or category.

- Balanced mainstream/premium/craft

- Supports trading-up & cross-sell

- Addresses multiple occasions/tiers

- Reduces single-brand/category risk

Scale in core geographies

Concentration in the UK and Ireland gives C&C operating scale and deep local know-how, anchored by the Wellpark brewery in Glasgow and Bulmers production in Clonmel.

Efficient regional production footprint lowers unit costs, strengthens distributor and retailer leverage, and enables proven commercial and supply-playbooks to be replicated into adjacent markets.

- Scale: UK & Ireland focus

- Assets: Wellpark, Bulmers

- Efficiency: lower unit costs

- Replicability: transferable playbooks

Flagship labels drive €1.05bn FY2024 revenue via vertical integration

Flagship labels Bulmers, Magners and Tennent’s drive strong awareness and supported C&C’s FY2024 revenue of €1.05bn.

Vertical integration boosts margin capture, shortens lead times and limits supply risk.

Wide on-/off-trade presence in UK, Ireland and exports secures placements and rotation.

Multi-category portfolio balances mainstream, premium and craft, reducing single-brand dependency.

| Metric | Value |

|---|---|

| FY2024 revenue | €1.05bn |

| Core regions | UK, Ireland, exports |

| Key assets | Wellpark brewery, Bulmers Clonmel |

What is included in the product

Provides a concise SWOT analysis of C&C Group, highlighting its market strengths, operational weaknesses, strategic opportunities and external threats to inform competitive positioning and growth strategy.

Provides a concise, visual SWOT matrix for C&C Group to speed strategic alignment and relieve analysis bottlenecks; editable format enables quick updates for evolving market dynamics and stakeholder presentations.

Weaknesses

Geographic concentration risk

Heavy reliance on UK and Ireland exposes earnings to local shocks; over 80% of FY2024 group revenue was generated in these markets per C&C filings. Regulatory, tax or macro changes in those jurisdictions can disproportionately impact margins and cash flow. Limited geographic diversification versus global peers reduces the buffer, and international capabilities remain underdeveloped.

Category exposure to cider volatility

C&C's reliance on cider exposes it to pronounced seasonality and trend sensitivity, with summer peaks amplifying revenue volatility. Growing consumer shifts toward spirits and RTDs have eroded share in key on-trade and convenience segments. Several of C&C's legacy brands show aging perceptions, necessitating continual marketing investment to maintain relevance. Faster innovation cycles are required to match competitor product launches and sustain momentum.

On-trade sensitivity

Footfall swings in pubs and bars directly affect C&C volumes, with the UK pub estate at c.39,000 outlets in 2023 amplifying exposure to seasonal patterns. Weather, events and consumer cost pressure drive volatile demand and can sharply reduce on-trade sales. Higher service costs and draught-system maintenance increase margin pressure and operational logistics complexity.

Input cost and energy intensity

Packaging, energy and agricultural inputs remain inflation-prone, with input inflation peaking around 15–20% in 2022–23 and elevated volatility persisting into 2024, squeezing C&C Group margins. Price swings undermine hedging effectiveness and force frequent price/mix adjustments that risk retailer pushback. Supply disruptions can ripple through production schedules and reduce capacity utilization.

- High input inflation (15–20% peak)

- Hedging effectiveness weakened by volatility

- Price/mix recovery faces retailer resistance

- Supply shocks disrupt production schedules

Operational and systems complexity

C&C Group, owner of Tennent's and Magners and listed on Euronext Dublin, faces execution risk from managing multiple brands, SKUs and trade channels.

IT and logistics coordination are critical to service levels; any system disruption can impair customer fulfilment and cash flow, requiring continuous investment to modernize and integrate.

- Multiple brands/SKUs: increases execution risk

- IT/logistics: critical for service levels

- System disruption: harms fulfilment & cash flow

- Ongoing capex: needed for modernization

UK/Ireland rev >80%; input inflation 15-20%, pub volatility

C&C's earnings are concentrated in UK/Ireland (>80% of FY2024 revenue), creating high exposure to local regulatory, tax and macro shocks. Heavy reliance on cider and on-trade demand drives seasonality and trend risk, while aging core brands require continuous marketing investment. Input inflation (peak 15–20% in 2022–23) and UK pub footfall volatility (c.39,000 outlets in 2023) compress margins and operational resilience.

| Metric | Value | Impact |

|---|---|---|

| UK/Ireland revenue | >80% FY2024 | Concentration risk |

| Pub outlets | c.39,000 (2023) | On-trade volatility |

| Input inflation | 15–20% peak (2022–23) | Margin pressure |

Preview Before You Purchase

C&C Group SWOT Analysis

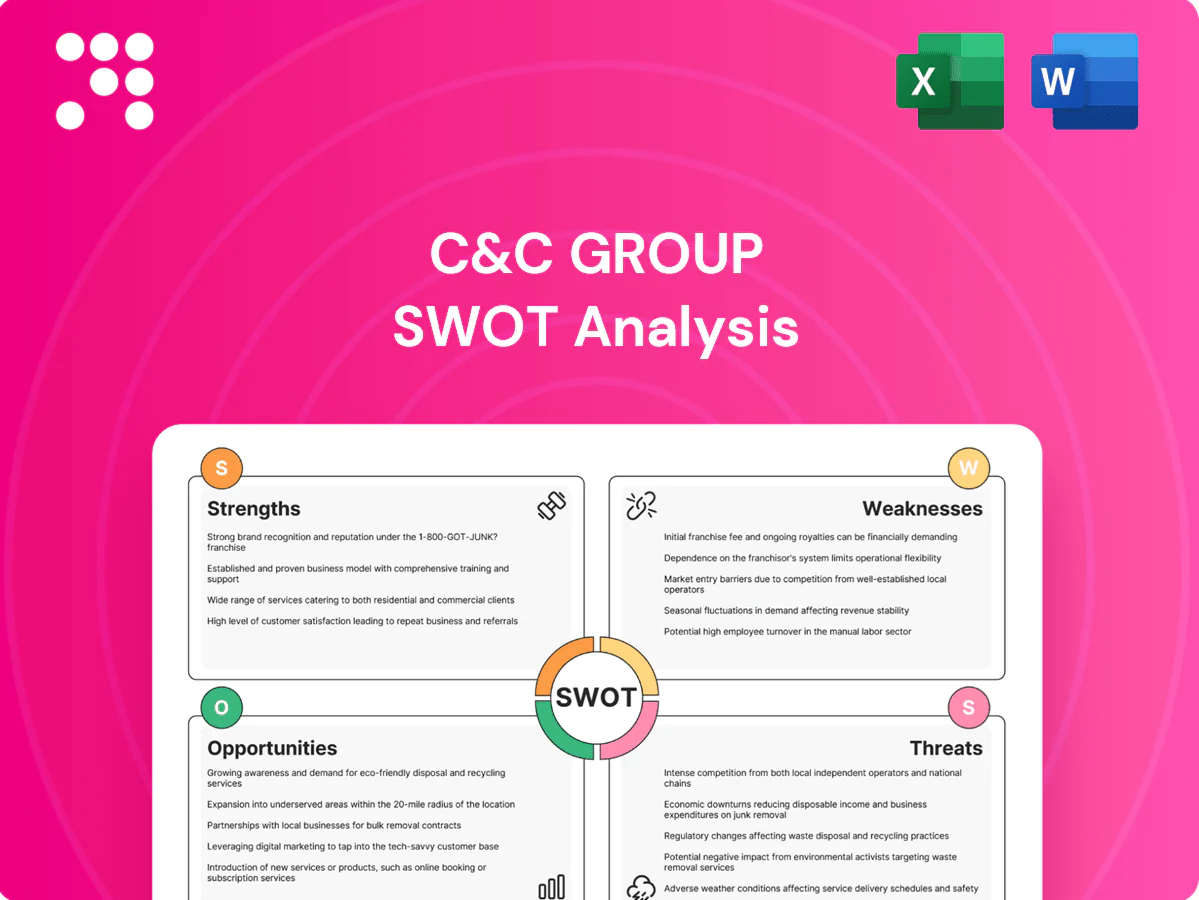

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The C&C Group assessment highlights strengths like established beverage brands and solid distribution in Ireland/UK, balanced against risks from regulatory shifts and changing consumer tastes. Opportunities include premiumisation and export growth, while weaknesses center on margin pressure and commodity cost exposure.

Make Insightful Decisions Backed by Expert Research

Our C&C Group SWOT preview highlights core strengths, market risks, and key growth drivers shaping its outlook; the full report expands these into actionable strategies and financial context. Purchase the complete SWOT to receive a professionally written, editable Word report plus an Excel model—ideal for investors, advisors, and strategists.

Strengths

Iconic cider and beer brands

Flagship labels Bulmers, Magners and Tennent’s drive high awareness and repeat purchase, supporting C&C’s c.€1.0bn revenue in FY2024 and reinforcing category leadership in cider that secures pricing power and premium shelf space.

End-to-end supply chain control

Ownership from production to distribution improves quality, service and margin capture; C&C reported FY 2024 revenue of €1.05bn, supporting reinvestment across the chain. Vertical integration gives agility to align brewing and cider-making with demand swings, shortening lead times. Route-to-market data feedback loops inform planning and innovation, while reduced third-party dependency limits supply disruption risk.

Diverse route-to-market coverage

Strong presence across on-trade and off-trade in Ireland, Great Britain and export markets enhances resilience; established relationships with pubs, bars and major retailers secure shelf and draught placements. Consistent point-of-sale execution drives rotation and promotions, while broad channel coverage enables rapid product launches and targeted assortments to specific trade segments.

Multi-category portfolio breadth

Multi-category portfolio gives C&C balanced exposure across mainstream, premium and craft ranges, supporting trading-up and cross-selling across on- and off-trade channels; FY2024 group revenue was €1.03bn, underscoring scale. The range lets C&C address varied consumer occasions and price tiers, reducing dependence on any single brand or category.

- Balanced mainstream/premium/craft

- Supports trading-up & cross-sell

- Addresses multiple occasions/tiers

- Reduces single-brand/category risk

Scale in core geographies

Concentration in the UK and Ireland gives C&C operating scale and deep local know-how, anchored by the Wellpark brewery in Glasgow and Bulmers production in Clonmel.

Efficient regional production footprint lowers unit costs, strengthens distributor and retailer leverage, and enables proven commercial and supply-playbooks to be replicated into adjacent markets.

- Scale: UK & Ireland focus

- Assets: Wellpark, Bulmers

- Efficiency: lower unit costs

- Replicability: transferable playbooks

Flagship labels drive €1.05bn FY2024 revenue via vertical integration

Flagship labels Bulmers, Magners and Tennent’s drive strong awareness and supported C&C’s FY2024 revenue of €1.05bn.

Vertical integration boosts margin capture, shortens lead times and limits supply risk.

Wide on-/off-trade presence in UK, Ireland and exports secures placements and rotation.

Multi-category portfolio balances mainstream, premium and craft, reducing single-brand dependency.

| Metric | Value |

|---|---|

| FY2024 revenue | €1.05bn |

| Core regions | UK, Ireland, exports |

| Key assets | Wellpark brewery, Bulmers Clonmel |

What is included in the product

Provides a concise SWOT analysis of C&C Group, highlighting its market strengths, operational weaknesses, strategic opportunities and external threats to inform competitive positioning and growth strategy.

Provides a concise, visual SWOT matrix for C&C Group to speed strategic alignment and relieve analysis bottlenecks; editable format enables quick updates for evolving market dynamics and stakeholder presentations.

Weaknesses

Geographic concentration risk

Heavy reliance on UK and Ireland exposes earnings to local shocks; over 80% of FY2024 group revenue was generated in these markets per C&C filings. Regulatory, tax or macro changes in those jurisdictions can disproportionately impact margins and cash flow. Limited geographic diversification versus global peers reduces the buffer, and international capabilities remain underdeveloped.

Category exposure to cider volatility

C&C's reliance on cider exposes it to pronounced seasonality and trend sensitivity, with summer peaks amplifying revenue volatility. Growing consumer shifts toward spirits and RTDs have eroded share in key on-trade and convenience segments. Several of C&C's legacy brands show aging perceptions, necessitating continual marketing investment to maintain relevance. Faster innovation cycles are required to match competitor product launches and sustain momentum.

On-trade sensitivity

Footfall swings in pubs and bars directly affect C&C volumes, with the UK pub estate at c.39,000 outlets in 2023 amplifying exposure to seasonal patterns. Weather, events and consumer cost pressure drive volatile demand and can sharply reduce on-trade sales. Higher service costs and draught-system maintenance increase margin pressure and operational logistics complexity.

Input cost and energy intensity

Packaging, energy and agricultural inputs remain inflation-prone, with input inflation peaking around 15–20% in 2022–23 and elevated volatility persisting into 2024, squeezing C&C Group margins. Price swings undermine hedging effectiveness and force frequent price/mix adjustments that risk retailer pushback. Supply disruptions can ripple through production schedules and reduce capacity utilization.

- High input inflation (15–20% peak)

- Hedging effectiveness weakened by volatility

- Price/mix recovery faces retailer resistance

- Supply shocks disrupt production schedules

Operational and systems complexity

C&C Group, owner of Tennent's and Magners and listed on Euronext Dublin, faces execution risk from managing multiple brands, SKUs and trade channels.

IT and logistics coordination are critical to service levels; any system disruption can impair customer fulfilment and cash flow, requiring continuous investment to modernize and integrate.

- Multiple brands/SKUs: increases execution risk

- IT/logistics: critical for service levels

- System disruption: harms fulfilment & cash flow

- Ongoing capex: needed for modernization

UK/Ireland rev >80%; input inflation 15-20%, pub volatility

C&C's earnings are concentrated in UK/Ireland (>80% of FY2024 revenue), creating high exposure to local regulatory, tax and macro shocks. Heavy reliance on cider and on-trade demand drives seasonality and trend risk, while aging core brands require continuous marketing investment. Input inflation (peak 15–20% in 2022–23) and UK pub footfall volatility (c.39,000 outlets in 2023) compress margins and operational resilience.

| Metric | Value | Impact |

|---|---|---|

| UK/Ireland revenue | >80% FY2024 | Concentration risk |

| Pub outlets | c.39,000 (2023) | On-trade volatility |

| Input inflation | 15–20% peak (2022–23) | Margin pressure |

Preview Before You Purchase

C&C Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The C&C Group assessment highlights strengths like established beverage brands and solid distribution in Ireland/UK, balanced against risks from regulatory shifts and changing consumer tastes. Opportunities include premiumisation and export growth, while weaknesses center on margin pressure and commodity cost exposure.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Our C&C Group SWOT preview highlights core strengths, market risks, and key growth drivers shaping its outlook; the full report expands these into actionable strategies and financial context. Purchase the complete SWOT to receive a professionally written, editable Word report plus an Excel model—ideal for investors, advisors, and strategists.

Strengths

Iconic cider and beer brands

Flagship labels Bulmers, Magners and Tennent’s drive high awareness and repeat purchase, supporting C&C’s c.€1.0bn revenue in FY2024 and reinforcing category leadership in cider that secures pricing power and premium shelf space.

End-to-end supply chain control

Ownership from production to distribution improves quality, service and margin capture; C&C reported FY 2024 revenue of €1.05bn, supporting reinvestment across the chain. Vertical integration gives agility to align brewing and cider-making with demand swings, shortening lead times. Route-to-market data feedback loops inform planning and innovation, while reduced third-party dependency limits supply disruption risk.

Diverse route-to-market coverage

Strong presence across on-trade and off-trade in Ireland, Great Britain and export markets enhances resilience; established relationships with pubs, bars and major retailers secure shelf and draught placements. Consistent point-of-sale execution drives rotation and promotions, while broad channel coverage enables rapid product launches and targeted assortments to specific trade segments.

Multi-category portfolio breadth

Multi-category portfolio gives C&C balanced exposure across mainstream, premium and craft ranges, supporting trading-up and cross-selling across on- and off-trade channels; FY2024 group revenue was €1.03bn, underscoring scale. The range lets C&C address varied consumer occasions and price tiers, reducing dependence on any single brand or category.

- Balanced mainstream/premium/craft

- Supports trading-up & cross-sell

- Addresses multiple occasions/tiers

- Reduces single-brand/category risk

Scale in core geographies

Concentration in the UK and Ireland gives C&C operating scale and deep local know-how, anchored by the Wellpark brewery in Glasgow and Bulmers production in Clonmel.

Efficient regional production footprint lowers unit costs, strengthens distributor and retailer leverage, and enables proven commercial and supply-playbooks to be replicated into adjacent markets.

- Scale: UK & Ireland focus

- Assets: Wellpark, Bulmers

- Efficiency: lower unit costs

- Replicability: transferable playbooks

Flagship labels drive €1.05bn FY2024 revenue via vertical integration

Flagship labels Bulmers, Magners and Tennent’s drive strong awareness and supported C&C’s FY2024 revenue of €1.05bn.

Vertical integration boosts margin capture, shortens lead times and limits supply risk.

Wide on-/off-trade presence in UK, Ireland and exports secures placements and rotation.

Multi-category portfolio balances mainstream, premium and craft, reducing single-brand dependency.

| Metric | Value |

|---|---|

| FY2024 revenue | €1.05bn |

| Core regions | UK, Ireland, exports |

| Key assets | Wellpark brewery, Bulmers Clonmel |

What is included in the product

Provides a concise SWOT analysis of C&C Group, highlighting its market strengths, operational weaknesses, strategic opportunities and external threats to inform competitive positioning and growth strategy.

Provides a concise, visual SWOT matrix for C&C Group to speed strategic alignment and relieve analysis bottlenecks; editable format enables quick updates for evolving market dynamics and stakeholder presentations.

Weaknesses

Geographic concentration risk

Heavy reliance on UK and Ireland exposes earnings to local shocks; over 80% of FY2024 group revenue was generated in these markets per C&C filings. Regulatory, tax or macro changes in those jurisdictions can disproportionately impact margins and cash flow. Limited geographic diversification versus global peers reduces the buffer, and international capabilities remain underdeveloped.

Category exposure to cider volatility

C&C's reliance on cider exposes it to pronounced seasonality and trend sensitivity, with summer peaks amplifying revenue volatility. Growing consumer shifts toward spirits and RTDs have eroded share in key on-trade and convenience segments. Several of C&C's legacy brands show aging perceptions, necessitating continual marketing investment to maintain relevance. Faster innovation cycles are required to match competitor product launches and sustain momentum.

On-trade sensitivity

Footfall swings in pubs and bars directly affect C&C volumes, with the UK pub estate at c.39,000 outlets in 2023 amplifying exposure to seasonal patterns. Weather, events and consumer cost pressure drive volatile demand and can sharply reduce on-trade sales. Higher service costs and draught-system maintenance increase margin pressure and operational logistics complexity.

Input cost and energy intensity

Packaging, energy and agricultural inputs remain inflation-prone, with input inflation peaking around 15–20% in 2022–23 and elevated volatility persisting into 2024, squeezing C&C Group margins. Price swings undermine hedging effectiveness and force frequent price/mix adjustments that risk retailer pushback. Supply disruptions can ripple through production schedules and reduce capacity utilization.

- High input inflation (15–20% peak)

- Hedging effectiveness weakened by volatility

- Price/mix recovery faces retailer resistance

- Supply shocks disrupt production schedules

Operational and systems complexity

C&C Group, owner of Tennent's and Magners and listed on Euronext Dublin, faces execution risk from managing multiple brands, SKUs and trade channels.

IT and logistics coordination are critical to service levels; any system disruption can impair customer fulfilment and cash flow, requiring continuous investment to modernize and integrate.

- Multiple brands/SKUs: increases execution risk

- IT/logistics: critical for service levels

- System disruption: harms fulfilment & cash flow

- Ongoing capex: needed for modernization

UK/Ireland rev >80%; input inflation 15-20%, pub volatility

C&C's earnings are concentrated in UK/Ireland (>80% of FY2024 revenue), creating high exposure to local regulatory, tax and macro shocks. Heavy reliance on cider and on-trade demand drives seasonality and trend risk, while aging core brands require continuous marketing investment. Input inflation (peak 15–20% in 2022–23) and UK pub footfall volatility (c.39,000 outlets in 2023) compress margins and operational resilience.

| Metric | Value | Impact |

|---|---|---|

| UK/Ireland revenue | >80% FY2024 | Concentration risk |

| Pub outlets | c.39,000 (2023) | On-trade volatility |

| Input inflation | 15–20% peak (2022–23) | Margin pressure |

Preview Before You Purchase

C&C Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The C&C Group assessment highlights strengths like established beverage brands and solid distribution in Ireland/UK, balanced against risks from regulatory shifts and changing consumer tastes. Opportunities include premiumisation and export growth, while weaknesses center on margin pressure and commodity cost exposure.