Cannae Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

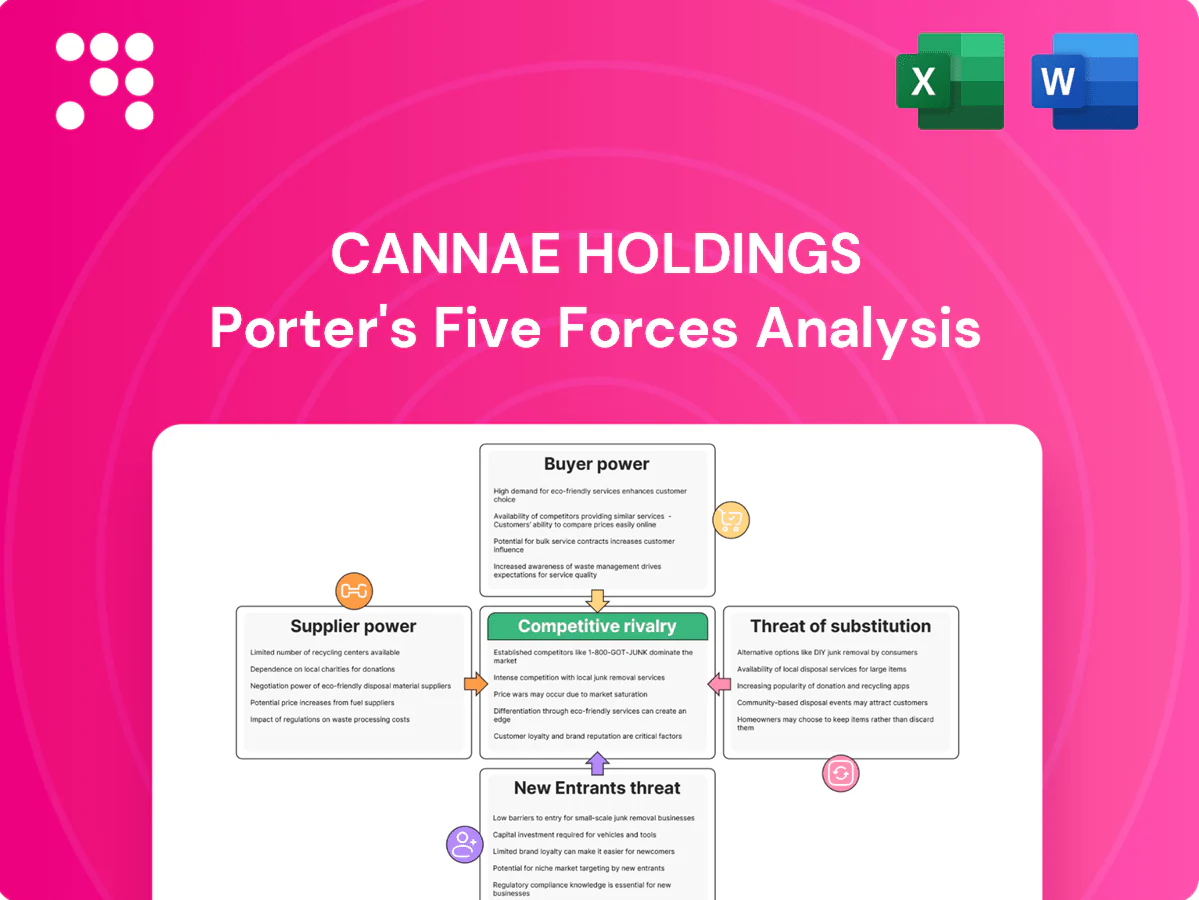

Cannae Holdings faces complex competitive pressures from concentrated buyers, diversified rivals, and acquisition-driven strategy shifts; supplier leverage and low-cost substitutes vary across its portfolio. This snapshot teases the dynamics—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated critical vendors

Cannae’s portfolio depends on a small set of specialized vendors—core banking processors, healthcare IT platforms and major restaurant distributors—which concentrates supply risk and can give these providers leverage over pricing and contractual terms. Long-term contracts (often 3–7 years) reduce short-term volatility but commonly include annual escalators and CPI-linked increases. High switching costs and integration complexity further entrench supplier bargaining power; top three payment processors held over 60% of US merchant processing share in 2024.

Human capital and executive talent

Top management teams and sector experts are scarce and command premium compensation, with equity incentives commonly representing 10–30% of total pay and senior hires often priced 20–40% above peer averages. Retention packages and equity grants therefore raise the effective cost of leadership “supply,” compressing margins for acquirers like Cannae. Competition from PE-backed platforms intensified in 2024 as global private equity dry powder reached roughly $2.2 trillion, escalating bidding for talent. Dependence on proven operators increases supplier power of labor markets and deal execution risk.

Data, payments, and tech platforms

Cannae Holdings' financial services and healthcare units rely on regulated data feeds, payment rails, and cloud providers where AWS (32%), Microsoft Azure (22%) and Google Cloud (11%) dominated cloud market share in 2024, concentrating supplier power. Compliance and security mandates (HIPAA, PCI) restrict vendor pools, while card interchange in the US averaged about 1.8–2.5% in 2024. Tier-1 platforms can impose standardized contracts and pass-through fees, and vendor lock-in—often reflected in costly migrations—raises switching costs and strengthens supplier influence.

Food and commodity inputs

Restaurant holdings face volatile protein, grains, and packaging costs; four meat packers account for about 85% of US beef processing capacity (USDA), concentrating supplier leverage, while large distributors like Sysco and US Foods secure firm-wide contracts and pass-through pricing that squeeze margins; hedging and multi-sourcing mitigate but do not remove this pressure.

- Concentration: four packers ≈85% (USDA)

- Distributor dominance: Sysco, US Foods negotiate firm-wide terms

- Pass-through pricing: compresses margins

- Risk mitigation: hedging and multi-sourcing reduce but not eliminate supplier power

Regulatory and compliance services

- Specialization: concentrated vendors

- Rates: upward pressure in 2024

- Regulatory shocks: increase demand and leverage

- Relationships: mitigate but not remove power

Concentrated suppliers, long contracts and $2.2T PE dry powder compress margins

Cannae faces concentrated supplier power: top three payment processors held ~60% US share in 2024, four meat packers ≈85% capacity, and AWS/Azure/GCP = 32/22/11% cloud share. Long contracts, high switching costs, equity-heavy executive pay (10–30%), and PE competition ($2.2T dry powder) raise supplier leverage and compress margins.

| Metric | 2024 |

|---|---|

| Top3 processors | ~60% |

| Meat packers | ≈85% |

| Cloud (AWS/AZ/GCP) | 32/22/11% |

| PE dry powder | $2.2T |

What is included in the product

Tailored Porter's Five Forces assessment of Cannae Holdings that uncovers competitive drivers, buyer and supplier leverage, substitute threats and entry barriers, highlighting strategic vulnerabilities and defensive opportunities.

A concise one-sheet Porter's Five Forces analysis for Cannae Holdings that clarifies strategic pressures and relieves decision-making friction; customize pressure levels or swap your own data to model scenarios (pre/post-regulation, new entrants) and drop straight into pitch decks.

Customers Bargaining Power

Price-sensitive consumer segments

Restaurant customers exhibit high price elasticity and low switching costs, forcing portfolio restaurants to rely on promotions and value menus to defend traffic. Aggregators and review platforms increase transparency on price and quality, enabling rapid comparison and deal-seeking. This elevated buyer power compresses margins during down cycles and raises the need for cost discipline and targeted loyalty programs.

Institutional and enterprise clients

Institutional and enterprise clients—notably the top 5 US payors controlling roughly 60% of commercial enrollment in 2024—exert strong bargaining power through formal RFPs and heavy compliance demands that shift leverage to buyers. Volume commitments are routinely exchanged for steep discounts and strict SLAs, and losing a single large account can materially worsen unit economics and margins for portfolio companies.

Digital comparison and multi-homing

Customers routinely use apps and online reviews to compare alternatives, reducing brand loyalty; multi-homing across banks, fintechs and payments providers is common. Low switching friction erodes pricing power, forcing margin compression. Cannae’s businesses must differentiate on experience, speed and trust to offset buyer leverage and protect wallet share.

Reimbursement and payor dynamics

Healthcare revenue for Cannae is tightly tied to insurers and government programs; the top three insurers control roughly 50% of the commercial market (2024), and public payors dominate specialty reimbursement. Fixed reimbursement schedules limit pricing flexibility, renegotiations often span 12–18 months and favor payors, and this dynamic can compress EBITDA margins by 200–400 basis points.

- Insurer concentration ~50%

- Renegotiation cycle 12–18 months

- Reimbursement-driven pricing limits

- Margin pressure 200–400 bps

Cross-selling and ecosystem value

Diversified holdings allow Cannae to bundle services and raise customer lifetime value; cross-selling and ecosystem plays have delivered double-digit uplifts in peer portfolios, with personalization initiatives shown by McKinsey to boost revenue by about 10–15%. Integrated offerings reduce churn and create switching costs, while loyalty programs plus data-driven personalization weaken buyer power; Bain estimates a 5% retention rise can lift profits 25–95%. Execution quality across subsidiaries determines how much buyer power is mitigated.

- Bundling: increases CLV; peer uplifts often 10%+

- Integration: raises switching costs, lowers churn

- Personalization: ~10–15% revenue uplift (McKinsey)

- Retention impact: 5% retention → 25–95% profit lift (Bain)

- Execution: primary determinant of realized gains

Payor Power Squeezes Margins: 12-18 month Renegs; Personalization adds 10-15%

Buyers exert high leverage across Cannae’s portfolio: consumer facing units face low switching costs and high price sensitivity, while institutional payors (top 5 payors ~60% commercial enrollment in 2024) extract steep discounts and SLAs. Reimbursement caps and 12–18 month renegotiations compress margins ~200–400 bps. Bundling and personalization (10–15% revenue uplift) can partially offset buyer power.

| Metric | Value (2024) |

|---|---|

| Top 5 payors | ~60% commercial enrollment |

| Insurer concentration | ~50% |

| Renegotiation cycle | 12–18 months |

| Margin pressure | 200–400 bps |

| Personalization uplift | 10–15% |

Preview the Actual Deliverable

Cannae Holdings Porter's Five Forces Analysis

This Porter's Five Forces analysis for Cannae Holdings evaluates supplier and buyer power, competitive rivalry, threat of entry and substitutes, and strategic positioning; the preview you see is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples—ready for download and use.

Don't Miss the Bigger Picture

Cannae Holdings faces complex competitive pressures from concentrated buyers, diversified rivals, and acquisition-driven strategy shifts; supplier leverage and low-cost substitutes vary across its portfolio. This snapshot teases the dynamics—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated critical vendors

Cannae’s portfolio depends on a small set of specialized vendors—core banking processors, healthcare IT platforms and major restaurant distributors—which concentrates supply risk and can give these providers leverage over pricing and contractual terms. Long-term contracts (often 3–7 years) reduce short-term volatility but commonly include annual escalators and CPI-linked increases. High switching costs and integration complexity further entrench supplier bargaining power; top three payment processors held over 60% of US merchant processing share in 2024.

Human capital and executive talent

Top management teams and sector experts are scarce and command premium compensation, with equity incentives commonly representing 10–30% of total pay and senior hires often priced 20–40% above peer averages. Retention packages and equity grants therefore raise the effective cost of leadership “supply,” compressing margins for acquirers like Cannae. Competition from PE-backed platforms intensified in 2024 as global private equity dry powder reached roughly $2.2 trillion, escalating bidding for talent. Dependence on proven operators increases supplier power of labor markets and deal execution risk.

Data, payments, and tech platforms

Cannae Holdings' financial services and healthcare units rely on regulated data feeds, payment rails, and cloud providers where AWS (32%), Microsoft Azure (22%) and Google Cloud (11%) dominated cloud market share in 2024, concentrating supplier power. Compliance and security mandates (HIPAA, PCI) restrict vendor pools, while card interchange in the US averaged about 1.8–2.5% in 2024. Tier-1 platforms can impose standardized contracts and pass-through fees, and vendor lock-in—often reflected in costly migrations—raises switching costs and strengthens supplier influence.

Food and commodity inputs

Restaurant holdings face volatile protein, grains, and packaging costs; four meat packers account for about 85% of US beef processing capacity (USDA), concentrating supplier leverage, while large distributors like Sysco and US Foods secure firm-wide contracts and pass-through pricing that squeeze margins; hedging and multi-sourcing mitigate but do not remove this pressure.

- Concentration: four packers ≈85% (USDA)

- Distributor dominance: Sysco, US Foods negotiate firm-wide terms

- Pass-through pricing: compresses margins

- Risk mitigation: hedging and multi-sourcing reduce but not eliminate supplier power

Regulatory and compliance services

- Specialization: concentrated vendors

- Rates: upward pressure in 2024

- Regulatory shocks: increase demand and leverage

- Relationships: mitigate but not remove power

Concentrated suppliers, long contracts and $2.2T PE dry powder compress margins

Cannae faces concentrated supplier power: top three payment processors held ~60% US share in 2024, four meat packers ≈85% capacity, and AWS/Azure/GCP = 32/22/11% cloud share. Long contracts, high switching costs, equity-heavy executive pay (10–30%), and PE competition ($2.2T dry powder) raise supplier leverage and compress margins.

| Metric | 2024 |

|---|---|

| Top3 processors | ~60% |

| Meat packers | ≈85% |

| Cloud (AWS/AZ/GCP) | 32/22/11% |

| PE dry powder | $2.2T |

What is included in the product

Tailored Porter's Five Forces assessment of Cannae Holdings that uncovers competitive drivers, buyer and supplier leverage, substitute threats and entry barriers, highlighting strategic vulnerabilities and defensive opportunities.

A concise one-sheet Porter's Five Forces analysis for Cannae Holdings that clarifies strategic pressures and relieves decision-making friction; customize pressure levels or swap your own data to model scenarios (pre/post-regulation, new entrants) and drop straight into pitch decks.

Customers Bargaining Power

Price-sensitive consumer segments

Restaurant customers exhibit high price elasticity and low switching costs, forcing portfolio restaurants to rely on promotions and value menus to defend traffic. Aggregators and review platforms increase transparency on price and quality, enabling rapid comparison and deal-seeking. This elevated buyer power compresses margins during down cycles and raises the need for cost discipline and targeted loyalty programs.

Institutional and enterprise clients

Institutional and enterprise clients—notably the top 5 US payors controlling roughly 60% of commercial enrollment in 2024—exert strong bargaining power through formal RFPs and heavy compliance demands that shift leverage to buyers. Volume commitments are routinely exchanged for steep discounts and strict SLAs, and losing a single large account can materially worsen unit economics and margins for portfolio companies.

Digital comparison and multi-homing

Customers routinely use apps and online reviews to compare alternatives, reducing brand loyalty; multi-homing across banks, fintechs and payments providers is common. Low switching friction erodes pricing power, forcing margin compression. Cannae’s businesses must differentiate on experience, speed and trust to offset buyer leverage and protect wallet share.

Reimbursement and payor dynamics

Healthcare revenue for Cannae is tightly tied to insurers and government programs; the top three insurers control roughly 50% of the commercial market (2024), and public payors dominate specialty reimbursement. Fixed reimbursement schedules limit pricing flexibility, renegotiations often span 12–18 months and favor payors, and this dynamic can compress EBITDA margins by 200–400 basis points.

- Insurer concentration ~50%

- Renegotiation cycle 12–18 months

- Reimbursement-driven pricing limits

- Margin pressure 200–400 bps

Cross-selling and ecosystem value

Diversified holdings allow Cannae to bundle services and raise customer lifetime value; cross-selling and ecosystem plays have delivered double-digit uplifts in peer portfolios, with personalization initiatives shown by McKinsey to boost revenue by about 10–15%. Integrated offerings reduce churn and create switching costs, while loyalty programs plus data-driven personalization weaken buyer power; Bain estimates a 5% retention rise can lift profits 25–95%. Execution quality across subsidiaries determines how much buyer power is mitigated.

- Bundling: increases CLV; peer uplifts often 10%+

- Integration: raises switching costs, lowers churn

- Personalization: ~10–15% revenue uplift (McKinsey)

- Retention impact: 5% retention → 25–95% profit lift (Bain)

- Execution: primary determinant of realized gains

Payor Power Squeezes Margins: 12-18 month Renegs; Personalization adds 10-15%

Buyers exert high leverage across Cannae’s portfolio: consumer facing units face low switching costs and high price sensitivity, while institutional payors (top 5 payors ~60% commercial enrollment in 2024) extract steep discounts and SLAs. Reimbursement caps and 12–18 month renegotiations compress margins ~200–400 bps. Bundling and personalization (10–15% revenue uplift) can partially offset buyer power.

| Metric | Value (2024) |

|---|---|

| Top 5 payors | ~60% commercial enrollment |

| Insurer concentration | ~50% |

| Renegotiation cycle | 12–18 months |

| Margin pressure | 200–400 bps |

| Personalization uplift | 10–15% |

Preview the Actual Deliverable

Cannae Holdings Porter's Five Forces Analysis

This Porter's Five Forces analysis for Cannae Holdings evaluates supplier and buyer power, competitive rivalry, threat of entry and substitutes, and strategic positioning; the preview you see is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples—ready for download and use.

Description

Don't Miss the Bigger Picture

Cannae Holdings faces complex competitive pressures from concentrated buyers, diversified rivals, and acquisition-driven strategy shifts; supplier leverage and low-cost substitutes vary across its portfolio. This snapshot teases the dynamics—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated critical vendors

Cannae’s portfolio depends on a small set of specialized vendors—core banking processors, healthcare IT platforms and major restaurant distributors—which concentrates supply risk and can give these providers leverage over pricing and contractual terms. Long-term contracts (often 3–7 years) reduce short-term volatility but commonly include annual escalators and CPI-linked increases. High switching costs and integration complexity further entrench supplier bargaining power; top three payment processors held over 60% of US merchant processing share in 2024.

Human capital and executive talent

Top management teams and sector experts are scarce and command premium compensation, with equity incentives commonly representing 10–30% of total pay and senior hires often priced 20–40% above peer averages. Retention packages and equity grants therefore raise the effective cost of leadership “supply,” compressing margins for acquirers like Cannae. Competition from PE-backed platforms intensified in 2024 as global private equity dry powder reached roughly $2.2 trillion, escalating bidding for talent. Dependence on proven operators increases supplier power of labor markets and deal execution risk.

Data, payments, and tech platforms

Cannae Holdings' financial services and healthcare units rely on regulated data feeds, payment rails, and cloud providers where AWS (32%), Microsoft Azure (22%) and Google Cloud (11%) dominated cloud market share in 2024, concentrating supplier power. Compliance and security mandates (HIPAA, PCI) restrict vendor pools, while card interchange in the US averaged about 1.8–2.5% in 2024. Tier-1 platforms can impose standardized contracts and pass-through fees, and vendor lock-in—often reflected in costly migrations—raises switching costs and strengthens supplier influence.

Food and commodity inputs

Restaurant holdings face volatile protein, grains, and packaging costs; four meat packers account for about 85% of US beef processing capacity (USDA), concentrating supplier leverage, while large distributors like Sysco and US Foods secure firm-wide contracts and pass-through pricing that squeeze margins; hedging and multi-sourcing mitigate but do not remove this pressure.

- Concentration: four packers ≈85% (USDA)

- Distributor dominance: Sysco, US Foods negotiate firm-wide terms

- Pass-through pricing: compresses margins

- Risk mitigation: hedging and multi-sourcing reduce but not eliminate supplier power

Regulatory and compliance services

- Specialization: concentrated vendors

- Rates: upward pressure in 2024

- Regulatory shocks: increase demand and leverage

- Relationships: mitigate but not remove power

Concentrated suppliers, long contracts and $2.2T PE dry powder compress margins

Cannae faces concentrated supplier power: top three payment processors held ~60% US share in 2024, four meat packers ≈85% capacity, and AWS/Azure/GCP = 32/22/11% cloud share. Long contracts, high switching costs, equity-heavy executive pay (10–30%), and PE competition ($2.2T dry powder) raise supplier leverage and compress margins.

| Metric | 2024 |

|---|---|

| Top3 processors | ~60% |

| Meat packers | ≈85% |

| Cloud (AWS/AZ/GCP) | 32/22/11% |

| PE dry powder | $2.2T |

What is included in the product

Tailored Porter's Five Forces assessment of Cannae Holdings that uncovers competitive drivers, buyer and supplier leverage, substitute threats and entry barriers, highlighting strategic vulnerabilities and defensive opportunities.

A concise one-sheet Porter's Five Forces analysis for Cannae Holdings that clarifies strategic pressures and relieves decision-making friction; customize pressure levels or swap your own data to model scenarios (pre/post-regulation, new entrants) and drop straight into pitch decks.

Customers Bargaining Power

Price-sensitive consumer segments

Restaurant customers exhibit high price elasticity and low switching costs, forcing portfolio restaurants to rely on promotions and value menus to defend traffic. Aggregators and review platforms increase transparency on price and quality, enabling rapid comparison and deal-seeking. This elevated buyer power compresses margins during down cycles and raises the need for cost discipline and targeted loyalty programs.

Institutional and enterprise clients

Institutional and enterprise clients—notably the top 5 US payors controlling roughly 60% of commercial enrollment in 2024—exert strong bargaining power through formal RFPs and heavy compliance demands that shift leverage to buyers. Volume commitments are routinely exchanged for steep discounts and strict SLAs, and losing a single large account can materially worsen unit economics and margins for portfolio companies.

Digital comparison and multi-homing

Customers routinely use apps and online reviews to compare alternatives, reducing brand loyalty; multi-homing across banks, fintechs and payments providers is common. Low switching friction erodes pricing power, forcing margin compression. Cannae’s businesses must differentiate on experience, speed and trust to offset buyer leverage and protect wallet share.

Reimbursement and payor dynamics

Healthcare revenue for Cannae is tightly tied to insurers and government programs; the top three insurers control roughly 50% of the commercial market (2024), and public payors dominate specialty reimbursement. Fixed reimbursement schedules limit pricing flexibility, renegotiations often span 12–18 months and favor payors, and this dynamic can compress EBITDA margins by 200–400 basis points.

- Insurer concentration ~50%

- Renegotiation cycle 12–18 months

- Reimbursement-driven pricing limits

- Margin pressure 200–400 bps

Cross-selling and ecosystem value

Diversified holdings allow Cannae to bundle services and raise customer lifetime value; cross-selling and ecosystem plays have delivered double-digit uplifts in peer portfolios, with personalization initiatives shown by McKinsey to boost revenue by about 10–15%. Integrated offerings reduce churn and create switching costs, while loyalty programs plus data-driven personalization weaken buyer power; Bain estimates a 5% retention rise can lift profits 25–95%. Execution quality across subsidiaries determines how much buyer power is mitigated.

- Bundling: increases CLV; peer uplifts often 10%+

- Integration: raises switching costs, lowers churn

- Personalization: ~10–15% revenue uplift (McKinsey)

- Retention impact: 5% retention → 25–95% profit lift (Bain)

- Execution: primary determinant of realized gains

Payor Power Squeezes Margins: 12-18 month Renegs; Personalization adds 10-15%

Buyers exert high leverage across Cannae’s portfolio: consumer facing units face low switching costs and high price sensitivity, while institutional payors (top 5 payors ~60% commercial enrollment in 2024) extract steep discounts and SLAs. Reimbursement caps and 12–18 month renegotiations compress margins ~200–400 bps. Bundling and personalization (10–15% revenue uplift) can partially offset buyer power.

| Metric | Value (2024) |

|---|---|

| Top 5 payors | ~60% commercial enrollment |

| Insurer concentration | ~50% |

| Renegotiation cycle | 12–18 months |

| Margin pressure | 200–400 bps |

| Personalization uplift | 10–15% |

Preview the Actual Deliverable

Cannae Holdings Porter's Five Forces Analysis

This Porter's Five Forces analysis for Cannae Holdings evaluates supplier and buyer power, competitive rivalry, threat of entry and substitutes, and strategic positioning; the preview you see is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples—ready for download and use.