Canon Electronics Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Canon Electronics faces strong competitive rivalry from global imaging and semiconductor players, with moderate supplier leverage and growing substitute risks as tech shifts accelerate. Buyer sophistication and innovation cycles squeeze margins, while entry barriers remain mixed. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Canon Electronics’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized optics and sensor suppliers hold niche leverage

Canon Electronics relies on specialty precision glass, coatings and image sensors from few qualified vendors; Sony held about 46% of the global image‑sensor market in 2023, with the top three suppliers controlling over 70%, concentrating supplier power. Supplier concentration raises switching costs and lead times, with qualification and metrology cycles commonly taking 6–18 months. Multi‑sourcing and in‑house process know‑how reduce but do not remove supplier leverage.

Advanced mechatronics components require tight tolerances

High-precision motors, actuators, bearings and micro-geartrains are sourced from specialized suppliers, with flight- and industrial-grade specs narrowing the pool; GEO satellite failures can cost upwards of $100 million, giving suppliers leverage on quality and delivery terms, so Canon Electronics relies on 3–5 year framework agreements to stabilize pricing and secure capacity.

Semiconductors and custom ICs face cyclical capacity risks

ASICs, FPGAs and high-reliability semis expose Canon Electronics to foundry cycles that drove lead times and shortage premiums of roughly 10–30% during 2021–24, boosting supplier leverage. Design lock-in to specific chipsets heightens switching costs and bargaining power. Rigorous lifecycle and last-time-buy planning cut obsolescence risk. Strategic inventories and dual-designs (alternative silicon) temper supplier influence.

Materials with export controls and compliance constraints

Space and defense-adjacent components remain subject to ITAR/EAR and Japan's tightened export controls as of 2024, narrowing eligible suppliers and increasing documentation and licensing burdens. Compliance bottlenecks lengthen lead times and raise switching costs, entrenching incumbents that already meet regulatory standards. Canon Electronics must invest in robust compliance systems and authorized supplier networks to preserve negotiating flexibility and supply continuity.

- Regulation: ITAR/EAR + Japan controls (2024)

- Impact: fewer eligible suppliers, higher documentation burden

- Result: incumbent entrenchment, increased switching cost

- Action: invest in compliance systems and authorized supplier base

Potential counterweights via Canon group scale and partnerships

Affiliation with the Canon group aggregates volumes and enables technology collaboration and co-development/JV tooling that lower per-unit costs and supplier dependency; Canon’s 2024 group procurement programs and multi-year demand visibility improve suppliers’ capacity planning and negotiating flexibility. However, highly specific component specs for imaging and semiconductor modules still cap gains in supplier bargaining power.

- Scale: group procurement and co-development

- Cost: JV tooling reduces per-unit cost risk

- Visibility: multi-year demand eases supplier capacity planning (2024)

- Limit: unique specs maintain supplier leverage

Supplier power high — sensors top-3 > 70%, lead times 6–18m

Supplier power is high: image‑sensor share (Sony ~46% in 2023; top‑3 >70%) and specialized optics/motion parts create concentration and long qualification lead times (6–18 months). Foundry cycles raised component premiums ~10–30% (2021–24), and ITAR/EAR + Japan controls (2024) shrink eligible vendors. Canon group procurement and multi‑year contracts mitigate but do not eliminate supplier leverage.

| Metric | Value |

|---|---|

| Image‑sensor market (2023) | Sony ~46%; top‑3 >70% |

| Qualification lead time | 6–18 months |

| Foundry premium (2021–24) | ~10–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Canon Electronics, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and disruptive technologies; highlights strategic vulnerabilities and defensive levers to protect market share and pricing power.

A concise, one-sheet Porter's Five Forces for Canon Electronics—perfect for quick strategic decisions, customizable to reflect supply‑chain shifts or new entrants, and ready to paste into decks or integrate with broader analysis.

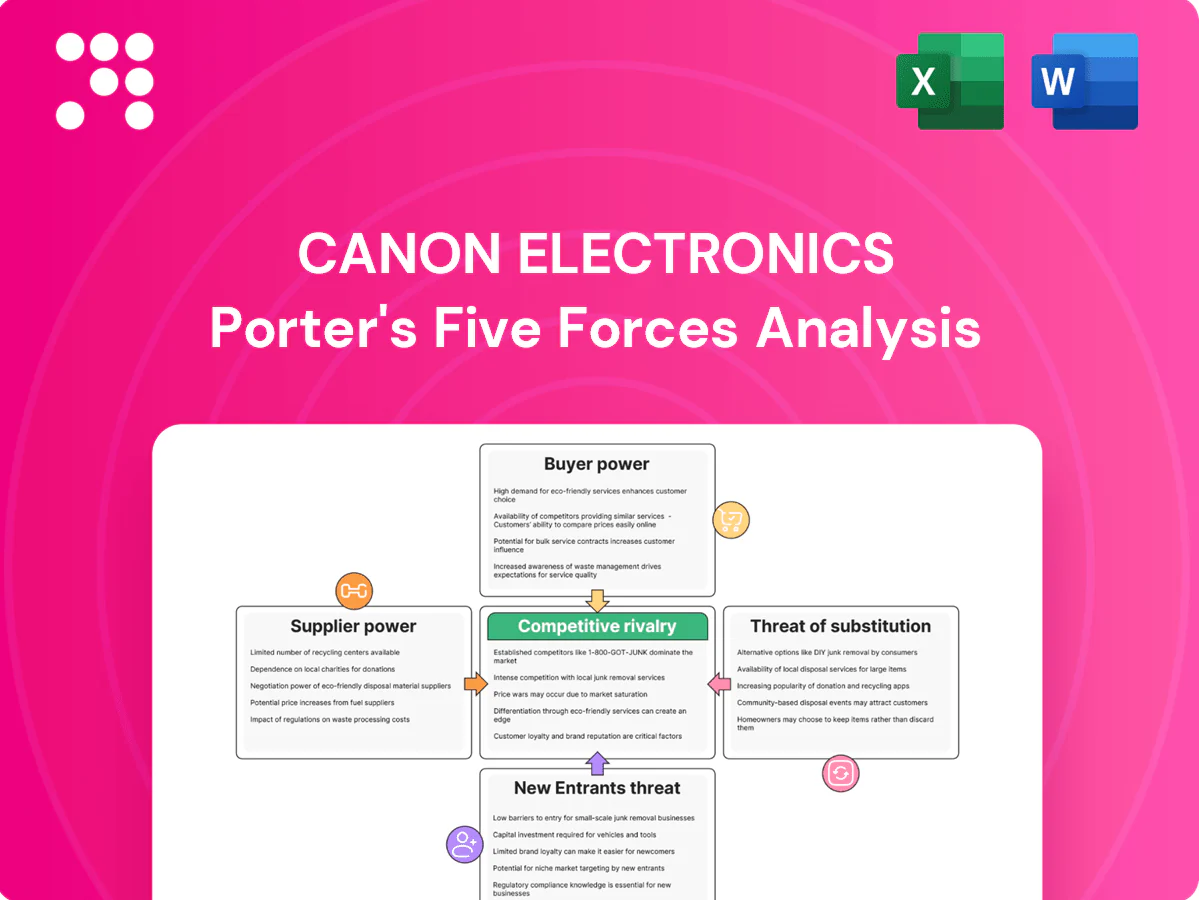

Customers Bargaining Power

Concentrated industrial and aerospace customers negotiate hard

Large OEMs and agencies purchase in sizable, recurring batches, leveraging program-scale buying power; US defense spending reached about 858 billion USD in FY2024, underscoring available procurement budgets. Their qualification authority and program budgets give them strong pricing influence and the ability to demand NRE amortization across production runs. They can enforce stringent SLAs, so Canon Electronics must rely on deep relationships and a proven performance track record to mitigate customer leverage.

High switching costs but formal requalification is a lever

Precision optics and mechatronics typically require long validation cycles (commonly 6–18 months), which raises switching costs for buyers. Customers still leverage dual-sourcing—used by roughly 40% of OEMs—to extract concessions and mitigate single-supplier risk. Lifecycle support, MTBF guarantees and detailed documentation frequently become bargaining chips in negotiations. Framing discussions around total cost of ownership lets Canon defend premium pricing with service and reliability evidence.

Custom engineering increases dependency yet invites target pricing

Tailored modules integrate buyer-specific interfaces and firmware, increasing dependency on Canon’s embedded IP while exposing projects to open-book target pricing during procurement. Buyers increasingly request design-to-cost and value-engineering rounds to trim unit costs, pressuring margins. Rigorous scope control and change-order discipline preserve profitability while meeting performance and customization needs.

Global buyers expect robust supply continuity and ESG

Global buyers demand resilient supply chains, traceability, and quantified sustainability; in 2024 the EU CSRD rollout raised reporting expectations, increasing buyer leverage if suppliers fail ESG or compliance checks.

Proactive third-party audits, standardized carbon reporting, and strict RoHS/REACH adherence strengthen Canon Electronics’ negotiating position and reduce price pressure through transparent risk mitigation.

- 2024: CSRD expanded corporate reporting

- Audits: third-party assurance reduces buyer leverage

- RoHS/REACH compliance: compliance lowers noncompliance risk

Aftermarket and service contracts moderate price sensitivity

Long-term service, calibration, and guaranteed spares bind customers to Canon Electronics, shifting negotiations from upfront hardware price to lifecycle value; performance-based contracts emphasize uptime and KPI payments, reducing buyer leverage over initial purchase. Data-driven predictive maintenance — with the global predictive maintenance market ~USD 8–9 billion in 2024 — increases switching costs by improving reliability and forecasting spare needs.

OEMs compress margins as ~858B US spend shifts procurement to lifecycle

Large OEMs (US defense budget ~858 billion USD FY2024) and ~40% dual-sourcing OEMs exert strong price and SLA pressure; long 6–18 month validations raise switching costs. Buyers push design-to-cost, lifecycle guarantees and ESG (CSRD 2024) compliance, squeezing margins. Service, calibration and predictive maintenance (market ~8–9B USD in 2024) shift negotiation toward lifecycle value.

| Metric | 2024 Data | Impact |

|---|---|---|

| US defense spend | ~858B USD | High procurement power |

| Dual-sourcing | ~40% | Pricing leverage |

| Predictive maintenance | 8–9B USD | Higher stickiness |

Preview Before You Purchase

Canon Electronics Porter's Five Forces Analysis

This preview is the exact Canon Electronics Porter's Five Forces analysis you’ll receive after purchase, containing the same in-depth competitive assessment, supplier and buyer power evaluation, threat analyses, and strategic implications. No placeholders or summaries—download the fully formatted file immediately upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Canon Electronics faces strong competitive rivalry from global imaging and semiconductor players, with moderate supplier leverage and growing substitute risks as tech shifts accelerate. Buyer sophistication and innovation cycles squeeze margins, while entry barriers remain mixed. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Canon Electronics’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized optics and sensor suppliers hold niche leverage

Canon Electronics relies on specialty precision glass, coatings and image sensors from few qualified vendors; Sony held about 46% of the global image‑sensor market in 2023, with the top three suppliers controlling over 70%, concentrating supplier power. Supplier concentration raises switching costs and lead times, with qualification and metrology cycles commonly taking 6–18 months. Multi‑sourcing and in‑house process know‑how reduce but do not remove supplier leverage.

Advanced mechatronics components require tight tolerances

High-precision motors, actuators, bearings and micro-geartrains are sourced from specialized suppliers, with flight- and industrial-grade specs narrowing the pool; GEO satellite failures can cost upwards of $100 million, giving suppliers leverage on quality and delivery terms, so Canon Electronics relies on 3–5 year framework agreements to stabilize pricing and secure capacity.

Semiconductors and custom ICs face cyclical capacity risks

ASICs, FPGAs and high-reliability semis expose Canon Electronics to foundry cycles that drove lead times and shortage premiums of roughly 10–30% during 2021–24, boosting supplier leverage. Design lock-in to specific chipsets heightens switching costs and bargaining power. Rigorous lifecycle and last-time-buy planning cut obsolescence risk. Strategic inventories and dual-designs (alternative silicon) temper supplier influence.

Materials with export controls and compliance constraints

Space and defense-adjacent components remain subject to ITAR/EAR and Japan's tightened export controls as of 2024, narrowing eligible suppliers and increasing documentation and licensing burdens. Compliance bottlenecks lengthen lead times and raise switching costs, entrenching incumbents that already meet regulatory standards. Canon Electronics must invest in robust compliance systems and authorized supplier networks to preserve negotiating flexibility and supply continuity.

- Regulation: ITAR/EAR + Japan controls (2024)

- Impact: fewer eligible suppliers, higher documentation burden

- Result: incumbent entrenchment, increased switching cost

- Action: invest in compliance systems and authorized supplier base

Potential counterweights via Canon group scale and partnerships

Affiliation with the Canon group aggregates volumes and enables technology collaboration and co-development/JV tooling that lower per-unit costs and supplier dependency; Canon’s 2024 group procurement programs and multi-year demand visibility improve suppliers’ capacity planning and negotiating flexibility. However, highly specific component specs for imaging and semiconductor modules still cap gains in supplier bargaining power.

- Scale: group procurement and co-development

- Cost: JV tooling reduces per-unit cost risk

- Visibility: multi-year demand eases supplier capacity planning (2024)

- Limit: unique specs maintain supplier leverage

Supplier power high — sensors top-3 > 70%, lead times 6–18m

Supplier power is high: image‑sensor share (Sony ~46% in 2023; top‑3 >70%) and specialized optics/motion parts create concentration and long qualification lead times (6–18 months). Foundry cycles raised component premiums ~10–30% (2021–24), and ITAR/EAR + Japan controls (2024) shrink eligible vendors. Canon group procurement and multi‑year contracts mitigate but do not eliminate supplier leverage.

| Metric | Value |

|---|---|

| Image‑sensor market (2023) | Sony ~46%; top‑3 >70% |

| Qualification lead time | 6–18 months |

| Foundry premium (2021–24) | ~10–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Canon Electronics, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and disruptive technologies; highlights strategic vulnerabilities and defensive levers to protect market share and pricing power.

A concise, one-sheet Porter's Five Forces for Canon Electronics—perfect for quick strategic decisions, customizable to reflect supply‑chain shifts or new entrants, and ready to paste into decks or integrate with broader analysis.

Customers Bargaining Power

Concentrated industrial and aerospace customers negotiate hard

Large OEMs and agencies purchase in sizable, recurring batches, leveraging program-scale buying power; US defense spending reached about 858 billion USD in FY2024, underscoring available procurement budgets. Their qualification authority and program budgets give them strong pricing influence and the ability to demand NRE amortization across production runs. They can enforce stringent SLAs, so Canon Electronics must rely on deep relationships and a proven performance track record to mitigate customer leverage.

High switching costs but formal requalification is a lever

Precision optics and mechatronics typically require long validation cycles (commonly 6–18 months), which raises switching costs for buyers. Customers still leverage dual-sourcing—used by roughly 40% of OEMs—to extract concessions and mitigate single-supplier risk. Lifecycle support, MTBF guarantees and detailed documentation frequently become bargaining chips in negotiations. Framing discussions around total cost of ownership lets Canon defend premium pricing with service and reliability evidence.

Custom engineering increases dependency yet invites target pricing

Tailored modules integrate buyer-specific interfaces and firmware, increasing dependency on Canon’s embedded IP while exposing projects to open-book target pricing during procurement. Buyers increasingly request design-to-cost and value-engineering rounds to trim unit costs, pressuring margins. Rigorous scope control and change-order discipline preserve profitability while meeting performance and customization needs.

Global buyers expect robust supply continuity and ESG

Global buyers demand resilient supply chains, traceability, and quantified sustainability; in 2024 the EU CSRD rollout raised reporting expectations, increasing buyer leverage if suppliers fail ESG or compliance checks.

Proactive third-party audits, standardized carbon reporting, and strict RoHS/REACH adherence strengthen Canon Electronics’ negotiating position and reduce price pressure through transparent risk mitigation.

- 2024: CSRD expanded corporate reporting

- Audits: third-party assurance reduces buyer leverage

- RoHS/REACH compliance: compliance lowers noncompliance risk

Aftermarket and service contracts moderate price sensitivity

Long-term service, calibration, and guaranteed spares bind customers to Canon Electronics, shifting negotiations from upfront hardware price to lifecycle value; performance-based contracts emphasize uptime and KPI payments, reducing buyer leverage over initial purchase. Data-driven predictive maintenance — with the global predictive maintenance market ~USD 8–9 billion in 2024 — increases switching costs by improving reliability and forecasting spare needs.

OEMs compress margins as ~858B US spend shifts procurement to lifecycle

Large OEMs (US defense budget ~858 billion USD FY2024) and ~40% dual-sourcing OEMs exert strong price and SLA pressure; long 6–18 month validations raise switching costs. Buyers push design-to-cost, lifecycle guarantees and ESG (CSRD 2024) compliance, squeezing margins. Service, calibration and predictive maintenance (market ~8–9B USD in 2024) shift negotiation toward lifecycle value.

| Metric | 2024 Data | Impact |

|---|---|---|

| US defense spend | ~858B USD | High procurement power |

| Dual-sourcing | ~40% | Pricing leverage |

| Predictive maintenance | 8–9B USD | Higher stickiness |

Preview Before You Purchase

Canon Electronics Porter's Five Forces Analysis

This preview is the exact Canon Electronics Porter's Five Forces analysis you’ll receive after purchase, containing the same in-depth competitive assessment, supplier and buyer power evaluation, threat analyses, and strategic implications. No placeholders or summaries—download the fully formatted file immediately upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Canon Electronics faces strong competitive rivalry from global imaging and semiconductor players, with moderate supplier leverage and growing substitute risks as tech shifts accelerate. Buyer sophistication and innovation cycles squeeze margins, while entry barriers remain mixed. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Canon Electronics’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized optics and sensor suppliers hold niche leverage

Canon Electronics relies on specialty precision glass, coatings and image sensors from few qualified vendors; Sony held about 46% of the global image‑sensor market in 2023, with the top three suppliers controlling over 70%, concentrating supplier power. Supplier concentration raises switching costs and lead times, with qualification and metrology cycles commonly taking 6–18 months. Multi‑sourcing and in‑house process know‑how reduce but do not remove supplier leverage.

Advanced mechatronics components require tight tolerances

High-precision motors, actuators, bearings and micro-geartrains are sourced from specialized suppliers, with flight- and industrial-grade specs narrowing the pool; GEO satellite failures can cost upwards of $100 million, giving suppliers leverage on quality and delivery terms, so Canon Electronics relies on 3–5 year framework agreements to stabilize pricing and secure capacity.

Semiconductors and custom ICs face cyclical capacity risks

ASICs, FPGAs and high-reliability semis expose Canon Electronics to foundry cycles that drove lead times and shortage premiums of roughly 10–30% during 2021–24, boosting supplier leverage. Design lock-in to specific chipsets heightens switching costs and bargaining power. Rigorous lifecycle and last-time-buy planning cut obsolescence risk. Strategic inventories and dual-designs (alternative silicon) temper supplier influence.

Materials with export controls and compliance constraints

Space and defense-adjacent components remain subject to ITAR/EAR and Japan's tightened export controls as of 2024, narrowing eligible suppliers and increasing documentation and licensing burdens. Compliance bottlenecks lengthen lead times and raise switching costs, entrenching incumbents that already meet regulatory standards. Canon Electronics must invest in robust compliance systems and authorized supplier networks to preserve negotiating flexibility and supply continuity.

- Regulation: ITAR/EAR + Japan controls (2024)

- Impact: fewer eligible suppliers, higher documentation burden

- Result: incumbent entrenchment, increased switching cost

- Action: invest in compliance systems and authorized supplier base

Potential counterweights via Canon group scale and partnerships

Affiliation with the Canon group aggregates volumes and enables technology collaboration and co-development/JV tooling that lower per-unit costs and supplier dependency; Canon’s 2024 group procurement programs and multi-year demand visibility improve suppliers’ capacity planning and negotiating flexibility. However, highly specific component specs for imaging and semiconductor modules still cap gains in supplier bargaining power.

- Scale: group procurement and co-development

- Cost: JV tooling reduces per-unit cost risk

- Visibility: multi-year demand eases supplier capacity planning (2024)

- Limit: unique specs maintain supplier leverage

Supplier power high — sensors top-3 > 70%, lead times 6–18m

Supplier power is high: image‑sensor share (Sony ~46% in 2023; top‑3 >70%) and specialized optics/motion parts create concentration and long qualification lead times (6–18 months). Foundry cycles raised component premiums ~10–30% (2021–24), and ITAR/EAR + Japan controls (2024) shrink eligible vendors. Canon group procurement and multi‑year contracts mitigate but do not eliminate supplier leverage.

| Metric | Value |

|---|---|

| Image‑sensor market (2023) | Sony ~46%; top‑3 >70% |

| Qualification lead time | 6–18 months |

| Foundry premium (2021–24) | ~10–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Canon Electronics, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and disruptive technologies; highlights strategic vulnerabilities and defensive levers to protect market share and pricing power.

A concise, one-sheet Porter's Five Forces for Canon Electronics—perfect for quick strategic decisions, customizable to reflect supply‑chain shifts or new entrants, and ready to paste into decks or integrate with broader analysis.

Customers Bargaining Power

Concentrated industrial and aerospace customers negotiate hard

Large OEMs and agencies purchase in sizable, recurring batches, leveraging program-scale buying power; US defense spending reached about 858 billion USD in FY2024, underscoring available procurement budgets. Their qualification authority and program budgets give them strong pricing influence and the ability to demand NRE amortization across production runs. They can enforce stringent SLAs, so Canon Electronics must rely on deep relationships and a proven performance track record to mitigate customer leverage.

High switching costs but formal requalification is a lever

Precision optics and mechatronics typically require long validation cycles (commonly 6–18 months), which raises switching costs for buyers. Customers still leverage dual-sourcing—used by roughly 40% of OEMs—to extract concessions and mitigate single-supplier risk. Lifecycle support, MTBF guarantees and detailed documentation frequently become bargaining chips in negotiations. Framing discussions around total cost of ownership lets Canon defend premium pricing with service and reliability evidence.

Custom engineering increases dependency yet invites target pricing

Tailored modules integrate buyer-specific interfaces and firmware, increasing dependency on Canon’s embedded IP while exposing projects to open-book target pricing during procurement. Buyers increasingly request design-to-cost and value-engineering rounds to trim unit costs, pressuring margins. Rigorous scope control and change-order discipline preserve profitability while meeting performance and customization needs.

Global buyers expect robust supply continuity and ESG

Global buyers demand resilient supply chains, traceability, and quantified sustainability; in 2024 the EU CSRD rollout raised reporting expectations, increasing buyer leverage if suppliers fail ESG or compliance checks.

Proactive third-party audits, standardized carbon reporting, and strict RoHS/REACH adherence strengthen Canon Electronics’ negotiating position and reduce price pressure through transparent risk mitigation.

- 2024: CSRD expanded corporate reporting

- Audits: third-party assurance reduces buyer leverage

- RoHS/REACH compliance: compliance lowers noncompliance risk

Aftermarket and service contracts moderate price sensitivity

Long-term service, calibration, and guaranteed spares bind customers to Canon Electronics, shifting negotiations from upfront hardware price to lifecycle value; performance-based contracts emphasize uptime and KPI payments, reducing buyer leverage over initial purchase. Data-driven predictive maintenance — with the global predictive maintenance market ~USD 8–9 billion in 2024 — increases switching costs by improving reliability and forecasting spare needs.

OEMs compress margins as ~858B US spend shifts procurement to lifecycle

Large OEMs (US defense budget ~858 billion USD FY2024) and ~40% dual-sourcing OEMs exert strong price and SLA pressure; long 6–18 month validations raise switching costs. Buyers push design-to-cost, lifecycle guarantees and ESG (CSRD 2024) compliance, squeezing margins. Service, calibration and predictive maintenance (market ~8–9B USD in 2024) shift negotiation toward lifecycle value.

| Metric | 2024 Data | Impact |

|---|---|---|

| US defense spend | ~858B USD | High procurement power |

| Dual-sourcing | ~40% | Pricing leverage |

| Predictive maintenance | 8–9B USD | Higher stickiness |

Preview Before You Purchase

Canon Electronics Porter's Five Forces Analysis

This preview is the exact Canon Electronics Porter's Five Forces analysis you’ll receive after purchase, containing the same in-depth competitive assessment, supplier and buyer power evaluation, threat analyses, and strategic implications. No placeholders or summaries—download the fully formatted file immediately upon payment.