Canon Electronics PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

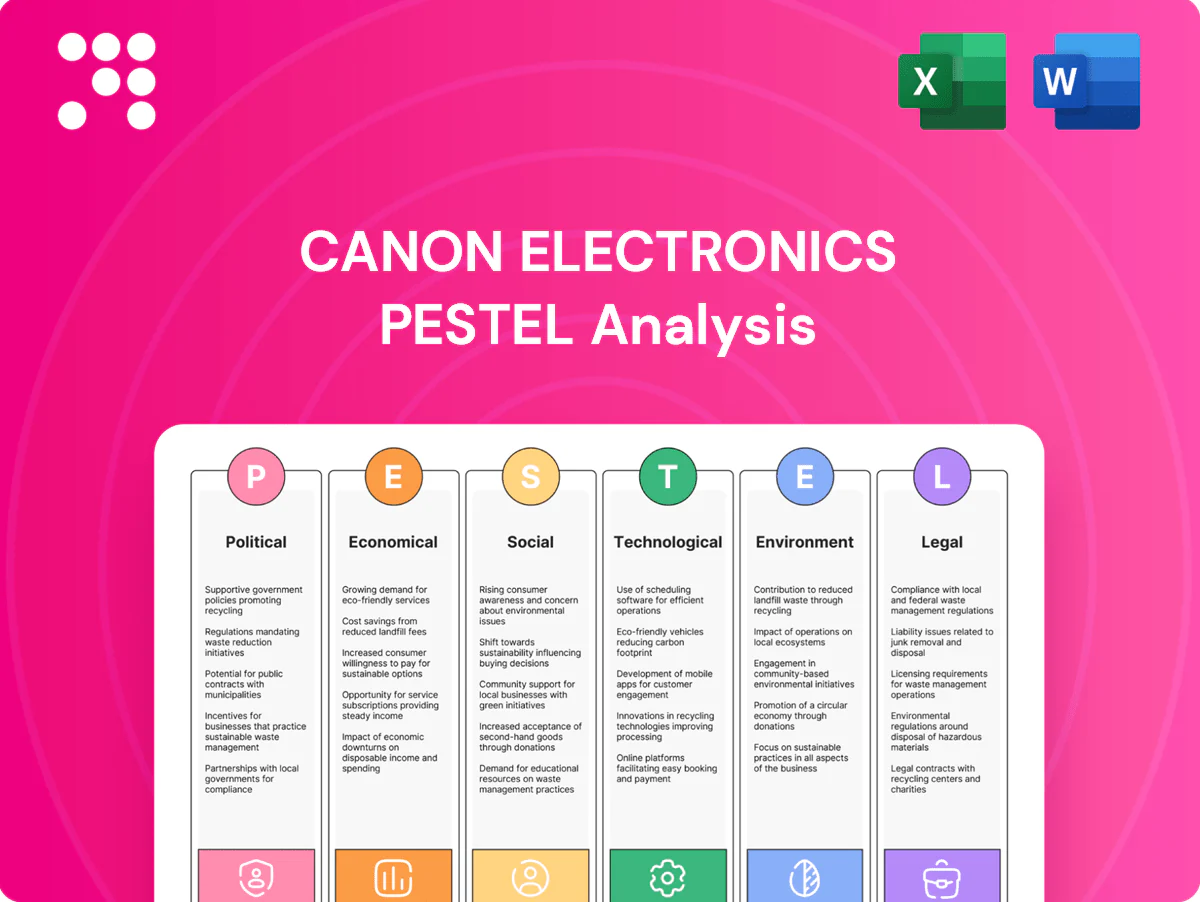

Gain a strategic edge with our PESTLE Analysis of Canon Electronics—three concise sections reveal political, economic, social, technological, legal, and environmental forces reshaping the company; ideal for investors and strategists. Purchase the full report to access detailed risks, forecasts, and actionable recommendations instantly.

Political factors

Export controls on space and dual-use tech

Canon Electronics’ satellites and precision components can fall under Japan METI export controls (expanded in Oct 2023) and US EAR/ITAR when US-origin tech is embedded, exposing cross-border sales to licensing reviews that can delay deals by months. Compliance can raise program costs via added legal, documentation and testing burdens. Proactive classification and design-to-decontrol reduce risk, while partnerships need technology firewalls and strict end-use certification.

Geopolitical tensions and supply chain reshoring

US–China tech decoupling and East Asia security risks threaten access to Chinese manufacturing and critical inputs, pushing customers toward Japan/ally onshoring; 2024 surveys show roughly 60% of manufacturers prioritizing friend-shoring. Incentives such as the US CHIPS Act (about $52bn) and US IRA programs (~$369bn) can help Canon Electronics localize capacity, but with higher operating costs, making dual-sourcing and friend-shoring key differentiators.

Government procurement in space and defense

Space and secure-data systems depend heavily on government budgets and procurement cycles, with Japan's FY2024 defense budget near ¥6.9 trillion and allied markets like the US at roughly $858 billion, steering demand toward Earth observation and defense modernization; long vendor qualification and certification lead times raise barriers but lock revenues, and alignment with national programs stabilizes order books.

Trade agreements and tariff regimes

Membership in CPTPP (~13% of global GDP), RCEP (~30% of world GDP and ~30% of trade) and the Japan–EU EPA (tariff removal on ~99% of tariff lines) lowers duties and eases rules-of-origin for Canon Electronics' components, boosting price competitiveness versus non-member rivals; shifting tariff lists and origin documentation add compliance overhead, so continuous monitoring preserves margin advantages across export corridors.

- Preferential tariffs: lower landed costs

- Rules-of-origin: simpler component sourcing

- Overhead: increased documentation and monitoring

Industrial policy and subsidies

Japan’s industrial policy backs advanced manufacturing, semiconductors and space with grants, tax credits and accelerated depreciation—programs that can cover up to 50% of capex and yield 10–20% effective tax relief; firms tapping these (2024–25) funds must show automation, clean-energy investment and R&D scaling. Canon Electronics can secure funding for robotics, EV component lines and sensor R&D, but competition favors local content and consortiums; KPI scrutiny will focus on productivity gains and emissions cuts aligned with Japan’s 46% GHG reduction by 2030 target.

- up to 50% capex support

- 10–20% effective tax incentives

- localization/consortium required

- KPI focus: productivity % and emissions reduction vs 2013 baseline

Export controls and friend-shoring; $52B CHIPS, 50% capex support

Export controls (Japan METI Oct 2023; US EAR/ITAR) and US–China decoupling raise licensing delays and supply risks, while friend-shoring incentives (US CHIPS $52bn; IRA ~$369bn) push localization with higher Opex. Government demand (Japan defense ¥6.9T FY2024; US ~$858B) stabilizes space/secure-systems orders. Japan support can cover up to 50% capex; KPI scrutiny ties funds to productivity and emissions cuts (46% by 2030).

| Policy | Key 2024–25 Figure |

|---|---|

| METI export controls | expanded Oct 2023 |

| US CHIPS/IRA | $52B / ~$369B |

| Japan defense FY2024 | ¥6.9T |

| Capex support | up to 50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Canon Electronics, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, decks, or internal reports.

A clean, summarized Canon Electronics PESTLE analysis organized by PESTEL categories for quick reference, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Currency volatility (JPY)

Yen weakness (USD/JPY surged to about 155 in Oct 2022 and remained above 150 through much of 2023) boosts Canon Electronics export competitiveness but raises import costs for components and capital equipment; hedging programs and increased local‑currency sourcing are used to reduce P&L swings. Pricing clauses indexed to FX help stabilize margins on long‑cycle contracts; managing the mix of export revenue versus foreign procurement is therefore critical.

Capital expenditure cycles in industrial markets

Customers’ capex for automation, instrumentation and satellites is cyclical and highly rate-sensitive; with policy rates near 5.25–5.50% in 2024–25, many projects face delays that elongate sales cycles. Diversification across space, factory automation and medical reduces revenue volatility, while service and aftermarket contracts—often recurring and margin-accretive—help cushion downturns and stabilize cash flow.

Semiconductor and optics supply dynamics

Optical/mechatronics builds depend on semiconductors, specialty glass and precision metals, and chip supply shocks have pushed some components to 20+ week lead times and double‑digit price jumps in recent cycles. Shortages compress margins and extend delivery; manufacturers mitigate with strategic inventories and 3–5 year supplier agreements to secure continuity. Active value engineering programs have cut bill‑of‑material inflation by several percentage points in comparable OEMs.

Energy prices and operating costs

Manufacturing precision parts is energy-intensive and power-price volatility materially alters unit economics; IEA data show global electricity market volatility surged after 2021, stressing margins for component-makers. Onsite renewables and efficiency upgrades—solar LCOE declines of roughly 80–90% since 2010 per IEA—can cut exposure and stabilize costs. Passing surcharges to buyers depends on strong customer contracts and trust. Location strategy near lower-cost, reliable grids (regional industrial rates vary widely) enhances competitiveness.

- Energy intensity: high for precision manufacturing

- Volatility: post-2021 market swings impact margins

- Mitigation: onsite renewables + efficiency

- Commercial: surcharges need customer alignment

- Site choice: lower-cost, reliable grids = edge

Global growth and industrial production indices

Demand for Canon Electronics products tracks PMI and IPI in key export markets: China manufacturing PMI 49.6 (June 2025) and IPI +3.2% YoY (May 2025), Eurozone PMI 47.8 with IPI -1.1% YoY, while US PMI 52.1 and IPI +2.5% YoY; slowdowns in Europe/China can reduce orders, but US and Japan capex—US business investment +6% YoY Q1 2025, Japan machinery orders +8% YoY—may offset. Scenario planning ties inventory and staffing to these macro signals; flexible production scheduling preserves cash and service levels.

- Align production to PMI/IPI shifts

- Reduce inventory risk in Europe/China

- Scale for US/Japan capex tailwinds

- Use flexible shifts to protect margins

Export controls and friend-shoring; $52B CHIPS, 50% capex support

Yen weakness (USD/JPY ~155 in Oct 2022; >150 through 2023) helps exports but raises input costs; hedging and local sourcing are key. High policy rates (~5.25–5.50% in 2024–25) slow capex, lengthening sales cycles; services cushion revenue. Semiconductor/energy shocks lengthen lead times and raise margins; onsite renewables and supplier contracts mitigate risk.

| Metric | Value |

|---|---|

| USD/JPY (peak) | ~155 |

| Policy rates | 5.25–5.50% |

| China PMI (Jun 2025) | 49.6 |

| US PMI (Jun 2025) | 52.1 |

Preview the Actual Deliverable

Canon Electronics PESTLE Analysis

The preview shown here is the exact Canon Electronics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file delivered immediately after checkout. No placeholders, no surprises—this is the final, professional document.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE Analysis of Canon Electronics—three concise sections reveal political, economic, social, technological, legal, and environmental forces reshaping the company; ideal for investors and strategists. Purchase the full report to access detailed risks, forecasts, and actionable recommendations instantly.

Political factors

Export controls on space and dual-use tech

Canon Electronics’ satellites and precision components can fall under Japan METI export controls (expanded in Oct 2023) and US EAR/ITAR when US-origin tech is embedded, exposing cross-border sales to licensing reviews that can delay deals by months. Compliance can raise program costs via added legal, documentation and testing burdens. Proactive classification and design-to-decontrol reduce risk, while partnerships need technology firewalls and strict end-use certification.

Geopolitical tensions and supply chain reshoring

US–China tech decoupling and East Asia security risks threaten access to Chinese manufacturing and critical inputs, pushing customers toward Japan/ally onshoring; 2024 surveys show roughly 60% of manufacturers prioritizing friend-shoring. Incentives such as the US CHIPS Act (about $52bn) and US IRA programs (~$369bn) can help Canon Electronics localize capacity, but with higher operating costs, making dual-sourcing and friend-shoring key differentiators.

Government procurement in space and defense

Space and secure-data systems depend heavily on government budgets and procurement cycles, with Japan's FY2024 defense budget near ¥6.9 trillion and allied markets like the US at roughly $858 billion, steering demand toward Earth observation and defense modernization; long vendor qualification and certification lead times raise barriers but lock revenues, and alignment with national programs stabilizes order books.

Trade agreements and tariff regimes

Membership in CPTPP (~13% of global GDP), RCEP (~30% of world GDP and ~30% of trade) and the Japan–EU EPA (tariff removal on ~99% of tariff lines) lowers duties and eases rules-of-origin for Canon Electronics' components, boosting price competitiveness versus non-member rivals; shifting tariff lists and origin documentation add compliance overhead, so continuous monitoring preserves margin advantages across export corridors.

- Preferential tariffs: lower landed costs

- Rules-of-origin: simpler component sourcing

- Overhead: increased documentation and monitoring

Industrial policy and subsidies

Japan’s industrial policy backs advanced manufacturing, semiconductors and space with grants, tax credits and accelerated depreciation—programs that can cover up to 50% of capex and yield 10–20% effective tax relief; firms tapping these (2024–25) funds must show automation, clean-energy investment and R&D scaling. Canon Electronics can secure funding for robotics, EV component lines and sensor R&D, but competition favors local content and consortiums; KPI scrutiny will focus on productivity gains and emissions cuts aligned with Japan’s 46% GHG reduction by 2030 target.

- up to 50% capex support

- 10–20% effective tax incentives

- localization/consortium required

- KPI focus: productivity % and emissions reduction vs 2013 baseline

Export controls and friend-shoring; $52B CHIPS, 50% capex support

Export controls (Japan METI Oct 2023; US EAR/ITAR) and US–China decoupling raise licensing delays and supply risks, while friend-shoring incentives (US CHIPS $52bn; IRA ~$369bn) push localization with higher Opex. Government demand (Japan defense ¥6.9T FY2024; US ~$858B) stabilizes space/secure-systems orders. Japan support can cover up to 50% capex; KPI scrutiny ties funds to productivity and emissions cuts (46% by 2030).

| Policy | Key 2024–25 Figure |

|---|---|

| METI export controls | expanded Oct 2023 |

| US CHIPS/IRA | $52B / ~$369B |

| Japan defense FY2024 | ¥6.9T |

| Capex support | up to 50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Canon Electronics, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, decks, or internal reports.

A clean, summarized Canon Electronics PESTLE analysis organized by PESTEL categories for quick reference, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Currency volatility (JPY)

Yen weakness (USD/JPY surged to about 155 in Oct 2022 and remained above 150 through much of 2023) boosts Canon Electronics export competitiveness but raises import costs for components and capital equipment; hedging programs and increased local‑currency sourcing are used to reduce P&L swings. Pricing clauses indexed to FX help stabilize margins on long‑cycle contracts; managing the mix of export revenue versus foreign procurement is therefore critical.

Capital expenditure cycles in industrial markets

Customers’ capex for automation, instrumentation and satellites is cyclical and highly rate-sensitive; with policy rates near 5.25–5.50% in 2024–25, many projects face delays that elongate sales cycles. Diversification across space, factory automation and medical reduces revenue volatility, while service and aftermarket contracts—often recurring and margin-accretive—help cushion downturns and stabilize cash flow.

Semiconductor and optics supply dynamics

Optical/mechatronics builds depend on semiconductors, specialty glass and precision metals, and chip supply shocks have pushed some components to 20+ week lead times and double‑digit price jumps in recent cycles. Shortages compress margins and extend delivery; manufacturers mitigate with strategic inventories and 3–5 year supplier agreements to secure continuity. Active value engineering programs have cut bill‑of‑material inflation by several percentage points in comparable OEMs.

Energy prices and operating costs

Manufacturing precision parts is energy-intensive and power-price volatility materially alters unit economics; IEA data show global electricity market volatility surged after 2021, stressing margins for component-makers. Onsite renewables and efficiency upgrades—solar LCOE declines of roughly 80–90% since 2010 per IEA—can cut exposure and stabilize costs. Passing surcharges to buyers depends on strong customer contracts and trust. Location strategy near lower-cost, reliable grids (regional industrial rates vary widely) enhances competitiveness.

- Energy intensity: high for precision manufacturing

- Volatility: post-2021 market swings impact margins

- Mitigation: onsite renewables + efficiency

- Commercial: surcharges need customer alignment

- Site choice: lower-cost, reliable grids = edge

Global growth and industrial production indices

Demand for Canon Electronics products tracks PMI and IPI in key export markets: China manufacturing PMI 49.6 (June 2025) and IPI +3.2% YoY (May 2025), Eurozone PMI 47.8 with IPI -1.1% YoY, while US PMI 52.1 and IPI +2.5% YoY; slowdowns in Europe/China can reduce orders, but US and Japan capex—US business investment +6% YoY Q1 2025, Japan machinery orders +8% YoY—may offset. Scenario planning ties inventory and staffing to these macro signals; flexible production scheduling preserves cash and service levels.

- Align production to PMI/IPI shifts

- Reduce inventory risk in Europe/China

- Scale for US/Japan capex tailwinds

- Use flexible shifts to protect margins

Export controls and friend-shoring; $52B CHIPS, 50% capex support

Yen weakness (USD/JPY ~155 in Oct 2022; >150 through 2023) helps exports but raises input costs; hedging and local sourcing are key. High policy rates (~5.25–5.50% in 2024–25) slow capex, lengthening sales cycles; services cushion revenue. Semiconductor/energy shocks lengthen lead times and raise margins; onsite renewables and supplier contracts mitigate risk.

| Metric | Value |

|---|---|

| USD/JPY (peak) | ~155 |

| Policy rates | 5.25–5.50% |

| China PMI (Jun 2025) | 49.6 |

| US PMI (Jun 2025) | 52.1 |

Preview the Actual Deliverable

Canon Electronics PESTLE Analysis

The preview shown here is the exact Canon Electronics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file delivered immediately after checkout. No placeholders, no surprises—this is the final, professional document.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE Analysis of Canon Electronics—three concise sections reveal political, economic, social, technological, legal, and environmental forces reshaping the company; ideal for investors and strategists. Purchase the full report to access detailed risks, forecasts, and actionable recommendations instantly.

Political factors

Export controls on space and dual-use tech

Canon Electronics’ satellites and precision components can fall under Japan METI export controls (expanded in Oct 2023) and US EAR/ITAR when US-origin tech is embedded, exposing cross-border sales to licensing reviews that can delay deals by months. Compliance can raise program costs via added legal, documentation and testing burdens. Proactive classification and design-to-decontrol reduce risk, while partnerships need technology firewalls and strict end-use certification.

Geopolitical tensions and supply chain reshoring

US–China tech decoupling and East Asia security risks threaten access to Chinese manufacturing and critical inputs, pushing customers toward Japan/ally onshoring; 2024 surveys show roughly 60% of manufacturers prioritizing friend-shoring. Incentives such as the US CHIPS Act (about $52bn) and US IRA programs (~$369bn) can help Canon Electronics localize capacity, but with higher operating costs, making dual-sourcing and friend-shoring key differentiators.

Government procurement in space and defense

Space and secure-data systems depend heavily on government budgets and procurement cycles, with Japan's FY2024 defense budget near ¥6.9 trillion and allied markets like the US at roughly $858 billion, steering demand toward Earth observation and defense modernization; long vendor qualification and certification lead times raise barriers but lock revenues, and alignment with national programs stabilizes order books.

Trade agreements and tariff regimes

Membership in CPTPP (~13% of global GDP), RCEP (~30% of world GDP and ~30% of trade) and the Japan–EU EPA (tariff removal on ~99% of tariff lines) lowers duties and eases rules-of-origin for Canon Electronics' components, boosting price competitiveness versus non-member rivals; shifting tariff lists and origin documentation add compliance overhead, so continuous monitoring preserves margin advantages across export corridors.

- Preferential tariffs: lower landed costs

- Rules-of-origin: simpler component sourcing

- Overhead: increased documentation and monitoring

Industrial policy and subsidies

Japan’s industrial policy backs advanced manufacturing, semiconductors and space with grants, tax credits and accelerated depreciation—programs that can cover up to 50% of capex and yield 10–20% effective tax relief; firms tapping these (2024–25) funds must show automation, clean-energy investment and R&D scaling. Canon Electronics can secure funding for robotics, EV component lines and sensor R&D, but competition favors local content and consortiums; KPI scrutiny will focus on productivity gains and emissions cuts aligned with Japan’s 46% GHG reduction by 2030 target.

- up to 50% capex support

- 10–20% effective tax incentives

- localization/consortium required

- KPI focus: productivity % and emissions reduction vs 2013 baseline

Export controls and friend-shoring; $52B CHIPS, 50% capex support

Export controls (Japan METI Oct 2023; US EAR/ITAR) and US–China decoupling raise licensing delays and supply risks, while friend-shoring incentives (US CHIPS $52bn; IRA ~$369bn) push localization with higher Opex. Government demand (Japan defense ¥6.9T FY2024; US ~$858B) stabilizes space/secure-systems orders. Japan support can cover up to 50% capex; KPI scrutiny ties funds to productivity and emissions cuts (46% by 2030).

| Policy | Key 2024–25 Figure |

|---|---|

| METI export controls | expanded Oct 2023 |

| US CHIPS/IRA | $52B / ~$369B |

| Japan defense FY2024 | ¥6.9T |

| Capex support | up to 50% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Canon Electronics, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, decks, or internal reports.

A clean, summarized Canon Electronics PESTLE analysis organized by PESTEL categories for quick reference, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Currency volatility (JPY)

Yen weakness (USD/JPY surged to about 155 in Oct 2022 and remained above 150 through much of 2023) boosts Canon Electronics export competitiveness but raises import costs for components and capital equipment; hedging programs and increased local‑currency sourcing are used to reduce P&L swings. Pricing clauses indexed to FX help stabilize margins on long‑cycle contracts; managing the mix of export revenue versus foreign procurement is therefore critical.

Capital expenditure cycles in industrial markets

Customers’ capex for automation, instrumentation and satellites is cyclical and highly rate-sensitive; with policy rates near 5.25–5.50% in 2024–25, many projects face delays that elongate sales cycles. Diversification across space, factory automation and medical reduces revenue volatility, while service and aftermarket contracts—often recurring and margin-accretive—help cushion downturns and stabilize cash flow.

Semiconductor and optics supply dynamics

Optical/mechatronics builds depend on semiconductors, specialty glass and precision metals, and chip supply shocks have pushed some components to 20+ week lead times and double‑digit price jumps in recent cycles. Shortages compress margins and extend delivery; manufacturers mitigate with strategic inventories and 3–5 year supplier agreements to secure continuity. Active value engineering programs have cut bill‑of‑material inflation by several percentage points in comparable OEMs.

Energy prices and operating costs

Manufacturing precision parts is energy-intensive and power-price volatility materially alters unit economics; IEA data show global electricity market volatility surged after 2021, stressing margins for component-makers. Onsite renewables and efficiency upgrades—solar LCOE declines of roughly 80–90% since 2010 per IEA—can cut exposure and stabilize costs. Passing surcharges to buyers depends on strong customer contracts and trust. Location strategy near lower-cost, reliable grids (regional industrial rates vary widely) enhances competitiveness.

- Energy intensity: high for precision manufacturing

- Volatility: post-2021 market swings impact margins

- Mitigation: onsite renewables + efficiency

- Commercial: surcharges need customer alignment

- Site choice: lower-cost, reliable grids = edge

Global growth and industrial production indices

Demand for Canon Electronics products tracks PMI and IPI in key export markets: China manufacturing PMI 49.6 (June 2025) and IPI +3.2% YoY (May 2025), Eurozone PMI 47.8 with IPI -1.1% YoY, while US PMI 52.1 and IPI +2.5% YoY; slowdowns in Europe/China can reduce orders, but US and Japan capex—US business investment +6% YoY Q1 2025, Japan machinery orders +8% YoY—may offset. Scenario planning ties inventory and staffing to these macro signals; flexible production scheduling preserves cash and service levels.

- Align production to PMI/IPI shifts

- Reduce inventory risk in Europe/China

- Scale for US/Japan capex tailwinds

- Use flexible shifts to protect margins

Export controls and friend-shoring; $52B CHIPS, 50% capex support

Yen weakness (USD/JPY ~155 in Oct 2022; >150 through 2023) helps exports but raises input costs; hedging and local sourcing are key. High policy rates (~5.25–5.50% in 2024–25) slow capex, lengthening sales cycles; services cushion revenue. Semiconductor/energy shocks lengthen lead times and raise margins; onsite renewables and supplier contracts mitigate risk.

| Metric | Value |

|---|---|

| USD/JPY (peak) | ~155 |

| Policy rates | 5.25–5.50% |

| China PMI (Jun 2025) | 49.6 |

| US PMI (Jun 2025) | 52.1 |

Preview the Actual Deliverable

Canon Electronics PESTLE Analysis

The preview shown here is the exact Canon Electronics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file delivered immediately after checkout. No placeholders, no surprises—this is the final, professional document.