Canon Porter's Five Forces Analysis

Don't Miss the Bigger Picture

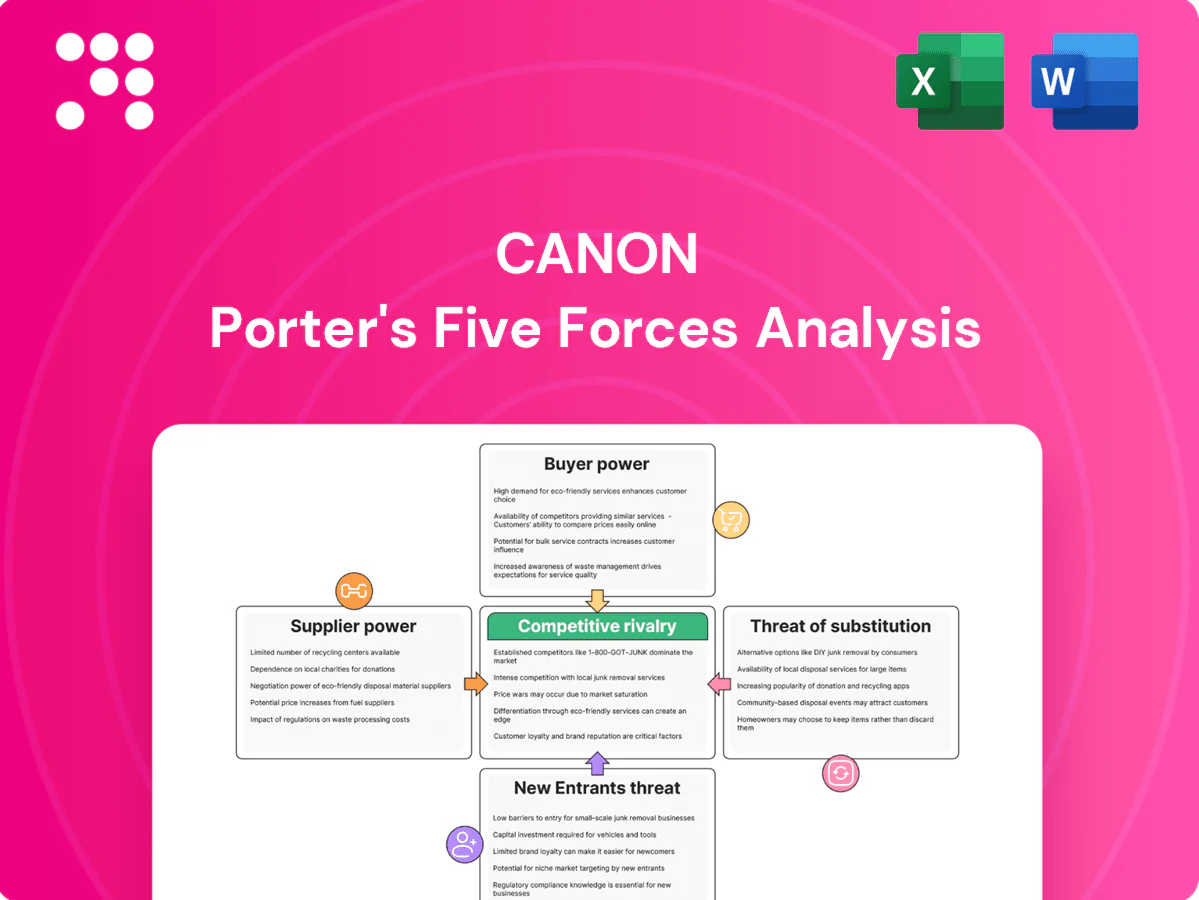

Canon's Porter's Five Forces snapshot highlights competitive rivalry across imaging and office equipment, supplier and buyer leverage, threat of substitutes from smartphone imaging and new entrants, and industry-specific regulatory pressures. This brief overview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy recommendations. Get the complete consultant-grade report to inform investment or strategic decisions.

Suppliers Bargaining Power

Key component concentration

High-spec image sensors, optics glass and precision mechatronics come from a narrow tier-1 base—Sony held about 45% of the global image‑sensor market in 2024, with Samsung and OmniVision rounding out roughly another 30–35%—concentrating supply and raising switching costs and lead‑time risk. Supplier leverage spikes during capacity tightness, historically widening component lead times to multiple months and pressuring margins. Canon uses dual‑sourcing where feasible, but achieving technical equivalence across suppliers is difficult.

Vertical integration buffer

Canon designs and manufactures critical modules — lenses, engines and controllers — internally, creating a vertical integration buffer that lowers supplier bargaining power and safeguards proprietary know-how. This integration supports Canon’s ~40% global share in interchangeable-lens cameras (2024), helping it negotiate better terms and stabilize quality. Nevertheless, dependence on upstream semiconductors and specialty materials remains a vulnerability.

Semiconductor dependency

Advanced sensors, memory and processors face cyclical supply and foundry constraints, with TSMC and Samsung holding roughly three-quarters of leading-edge foundry capacity in 2024, shifting allocation and pricing power to chip suppliers. Long design cycles and requalification (typically 12–24 months) limit rapid substitution. Strategic inventories of 3–6 months and multi‑year supply agreements mitigate but do not eliminate volatility.

Consumables and materials

Consumables like toner, inks and specialty coatings require consistent formulations from qualified suppliers; in 2024 the global printer consumables market was estimated at $23 billion, concentrating leverage with certified vendors.

Quality variance degrades device performance and brand perception, so Canon restricts substitution via approved-vendor lists, increasing supplier influence and switching costs.

Volume commitments and multi-year contracts secure availability and often deliver double-digit cost concessions for OEMs.

- 2024 market: $23B

- Approved-vendor lists: high switching costs

- Quality variance: direct brand/performance impact

- Volume commitments: secure supply, cost leverage

Geo-political and logistics risk

Complex cross-border supply chains expose Canon to tariff, export-control and transport disruption risks; suppliers concentrated in East Asia — Taiwan supplies about 63% of global semiconductor capacity — amplify systemic exposure. Currency swings alter input costs and negotiation leverage. Canon mitigates by diversifying suppliers and localizing production in Japan, the Philippines and Malaysia.

- Tariffs & export controls: higher compliance costs

- Regional concentration: ~63% semiconductor risk

- FX volatility: impacts input pricing

- Mitigation: diversification + local production

Sensor and foundry concentration increases supplier leverage; vertical integration reduces risk

Narrow tier‑1 supply (Sony ~45% image sensors, TSMC+Samsung ~75% leading foundry capacity, Taiwan ~63% semiconductor capacity) raises switching costs and price/lead‑time leverage; Canon's vertical integration (≈40% ILC share) plus dual‑sourcing and 3–6m inventories mitigate but not eliminate supplier power. Consumables market ~$23B concentrates vendor influence.

| Metric | 2024 value |

|---|---|

| Image sensor share (Sony) | 45% |

| Canon ILC share | ≈40% |

| Foundry concentration (TSMC+Samsung) | ≈75% |

| Semiconductor capacity (Taiwan) | ≈63% |

| Printer consumables market | $23B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Canon, uncovering key drivers of competition, buyer and supplier power, substitute threats, and barriers to entry; identifies disruptive technologies and emerging substitutes that could erode market share and provides strategic commentary to inform pricing, positioning, and defensive moves.

A concise Canon Porter's Five Forces sheet that standardizes assessments, lets you toggle scenario inputs, and outputs a radar chart—cutting analysis time and making strategic trade-offs obvious for decks and boardroom discussions.

Customers Bargaining Power

Diverse customer segments

Buyer sophistication ranges from price-sensitive consumers to hospitals, fabs and enterprises; Canon reported consolidated revenue of ¥3.9 trillion in FY2024, highlighting scale across segments. Large B2B accounts—often via tenders and SLAs—can represent double-digit share of unit-line sales and exert strong negotiating leverage. Consumers remain price-sensitive but brand and ecosystem lock-in (printers, EOS, imageRUNNER) reduce churn, creating uneven buyer power across lines.

Price transparency

Price transparency via online comparison sites and reviews compresses margins on Canon's mainstream cameras and printers, forcing greater reliance on volume; Canon reported group net sales of about ¥3.78 trillion in FY2023, with imaging contributing materially to that top line. Frequent promotions set low reference prices and buyers often delay purchases awaiting discounts, pressuring ASPs. Canon counteracts by bundling features, offering subscription service plans and extended warranties to preserve value and margin.

Switching costs and ecosystems

Lens mounts, accessories, and workflow software create high switching frictions for professional users, locking them into Canon RF/EF ecosystems and accessory investments. Managed print services and fleet management commonly use multi-year (3–5 year) contracts that embed Canon into enterprise processes. Medical and industrial product validation requires regulatory approvals (FDA/CE) and months of staff training, further raising costs to switch. These factors materially reduce buyer bargaining power in entrenched accounts.

Aftermarket leverage

Aftermarket leverage: consumables and maintenance contracts drive lifetime value and negotiation power; enterprise buyers in 2024 pushed harder on cost-per-page reductions and uptime SLAs, while third-party inks/toners — representing an estimated 20–30% of cartridge volumes — pressured pricing; Canon responded with strict chip authentication, documented quality assurance, and bundled service agreements to protect margins.

- Consumables focus: lifetime revenue stream

- Enterprise demands: CPP cuts & uptime guarantees

- Aftermarket threat: 20–30% third-party cartridge share (2024)

- Canon defenses: chip auth, QA, service bundles

Demand cyclicality

Camera and printer demand tracks macro cycles and replacement waves, so in downturns buyers delay upgrades and exert price pressure; Canon reported approximately 3.6 trillion yen in revenue for fiscal 2023, underscoring sensitivity to volume swings in 2024.

- Replacement waves intensify seasonal bargaining

- Health/education budget cycles drive purchase timing

- Canon times launches and financing to smooth demand

Buyer power skews to large B2B; consumables and MPS drive sustained lifetime value

Buyer power is uneven: large B2B accounts exert strong leverage via tenders/SLAs, while consumer price sensitivity is offset by Canon ecosystem lock-in. Price transparency and promotions compress ASPs on mainstream cameras/printers, increasing reliance on volume and services. Aftermarket consumables and multi-year MPS contracts (3–5 yrs) sustain lifetime value and reduce switching.

| Metric | 2024 |

|---|---|

| Consolidated revenue | ¥3.9 trillion |

| Third-party cartridge share | 20–30% |

| Typical MPS contract | 3–5 years |

Preview Before You Purchase

Canon Porter's Five Forces Analysis

This Canon Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, and the threat of new entrants and substitutes, with actionable strategic implications for Canon. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It's professionally formatted and ready for download and use the moment you buy.

Don't Miss the Bigger Picture

Canon's Porter's Five Forces snapshot highlights competitive rivalry across imaging and office equipment, supplier and buyer leverage, threat of substitutes from smartphone imaging and new entrants, and industry-specific regulatory pressures. This brief overview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy recommendations. Get the complete consultant-grade report to inform investment or strategic decisions.

Suppliers Bargaining Power

Key component concentration

High-spec image sensors, optics glass and precision mechatronics come from a narrow tier-1 base—Sony held about 45% of the global image‑sensor market in 2024, with Samsung and OmniVision rounding out roughly another 30–35%—concentrating supply and raising switching costs and lead‑time risk. Supplier leverage spikes during capacity tightness, historically widening component lead times to multiple months and pressuring margins. Canon uses dual‑sourcing where feasible, but achieving technical equivalence across suppliers is difficult.

Vertical integration buffer

Canon designs and manufactures critical modules — lenses, engines and controllers — internally, creating a vertical integration buffer that lowers supplier bargaining power and safeguards proprietary know-how. This integration supports Canon’s ~40% global share in interchangeable-lens cameras (2024), helping it negotiate better terms and stabilize quality. Nevertheless, dependence on upstream semiconductors and specialty materials remains a vulnerability.

Semiconductor dependency

Advanced sensors, memory and processors face cyclical supply and foundry constraints, with TSMC and Samsung holding roughly three-quarters of leading-edge foundry capacity in 2024, shifting allocation and pricing power to chip suppliers. Long design cycles and requalification (typically 12–24 months) limit rapid substitution. Strategic inventories of 3–6 months and multi‑year supply agreements mitigate but do not eliminate volatility.

Consumables and materials

Consumables like toner, inks and specialty coatings require consistent formulations from qualified suppliers; in 2024 the global printer consumables market was estimated at $23 billion, concentrating leverage with certified vendors.

Quality variance degrades device performance and brand perception, so Canon restricts substitution via approved-vendor lists, increasing supplier influence and switching costs.

Volume commitments and multi-year contracts secure availability and often deliver double-digit cost concessions for OEMs.

- 2024 market: $23B

- Approved-vendor lists: high switching costs

- Quality variance: direct brand/performance impact

- Volume commitments: secure supply, cost leverage

Geo-political and logistics risk

Complex cross-border supply chains expose Canon to tariff, export-control and transport disruption risks; suppliers concentrated in East Asia — Taiwan supplies about 63% of global semiconductor capacity — amplify systemic exposure. Currency swings alter input costs and negotiation leverage. Canon mitigates by diversifying suppliers and localizing production in Japan, the Philippines and Malaysia.

- Tariffs & export controls: higher compliance costs

- Regional concentration: ~63% semiconductor risk

- FX volatility: impacts input pricing

- Mitigation: diversification + local production

Sensor and foundry concentration increases supplier leverage; vertical integration reduces risk

Narrow tier‑1 supply (Sony ~45% image sensors, TSMC+Samsung ~75% leading foundry capacity, Taiwan ~63% semiconductor capacity) raises switching costs and price/lead‑time leverage; Canon's vertical integration (≈40% ILC share) plus dual‑sourcing and 3–6m inventories mitigate but not eliminate supplier power. Consumables market ~$23B concentrates vendor influence.

| Metric | 2024 value |

|---|---|

| Image sensor share (Sony) | 45% |

| Canon ILC share | ≈40% |

| Foundry concentration (TSMC+Samsung) | ≈75% |

| Semiconductor capacity (Taiwan) | ≈63% |

| Printer consumables market | $23B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Canon, uncovering key drivers of competition, buyer and supplier power, substitute threats, and barriers to entry; identifies disruptive technologies and emerging substitutes that could erode market share and provides strategic commentary to inform pricing, positioning, and defensive moves.

A concise Canon Porter's Five Forces sheet that standardizes assessments, lets you toggle scenario inputs, and outputs a radar chart—cutting analysis time and making strategic trade-offs obvious for decks and boardroom discussions.

Customers Bargaining Power

Diverse customer segments

Buyer sophistication ranges from price-sensitive consumers to hospitals, fabs and enterprises; Canon reported consolidated revenue of ¥3.9 trillion in FY2024, highlighting scale across segments. Large B2B accounts—often via tenders and SLAs—can represent double-digit share of unit-line sales and exert strong negotiating leverage. Consumers remain price-sensitive but brand and ecosystem lock-in (printers, EOS, imageRUNNER) reduce churn, creating uneven buyer power across lines.

Price transparency

Price transparency via online comparison sites and reviews compresses margins on Canon's mainstream cameras and printers, forcing greater reliance on volume; Canon reported group net sales of about ¥3.78 trillion in FY2023, with imaging contributing materially to that top line. Frequent promotions set low reference prices and buyers often delay purchases awaiting discounts, pressuring ASPs. Canon counteracts by bundling features, offering subscription service plans and extended warranties to preserve value and margin.

Switching costs and ecosystems

Lens mounts, accessories, and workflow software create high switching frictions for professional users, locking them into Canon RF/EF ecosystems and accessory investments. Managed print services and fleet management commonly use multi-year (3–5 year) contracts that embed Canon into enterprise processes. Medical and industrial product validation requires regulatory approvals (FDA/CE) and months of staff training, further raising costs to switch. These factors materially reduce buyer bargaining power in entrenched accounts.

Aftermarket leverage

Aftermarket leverage: consumables and maintenance contracts drive lifetime value and negotiation power; enterprise buyers in 2024 pushed harder on cost-per-page reductions and uptime SLAs, while third-party inks/toners — representing an estimated 20–30% of cartridge volumes — pressured pricing; Canon responded with strict chip authentication, documented quality assurance, and bundled service agreements to protect margins.

- Consumables focus: lifetime revenue stream

- Enterprise demands: CPP cuts & uptime guarantees

- Aftermarket threat: 20–30% third-party cartridge share (2024)

- Canon defenses: chip auth, QA, service bundles

Demand cyclicality

Camera and printer demand tracks macro cycles and replacement waves, so in downturns buyers delay upgrades and exert price pressure; Canon reported approximately 3.6 trillion yen in revenue for fiscal 2023, underscoring sensitivity to volume swings in 2024.

- Replacement waves intensify seasonal bargaining

- Health/education budget cycles drive purchase timing

- Canon times launches and financing to smooth demand

Buyer power skews to large B2B; consumables and MPS drive sustained lifetime value

Buyer power is uneven: large B2B accounts exert strong leverage via tenders/SLAs, while consumer price sensitivity is offset by Canon ecosystem lock-in. Price transparency and promotions compress ASPs on mainstream cameras/printers, increasing reliance on volume and services. Aftermarket consumables and multi-year MPS contracts (3–5 yrs) sustain lifetime value and reduce switching.

| Metric | 2024 |

|---|---|

| Consolidated revenue | ¥3.9 trillion |

| Third-party cartridge share | 20–30% |

| Typical MPS contract | 3–5 years |

Preview Before You Purchase

Canon Porter's Five Forces Analysis

This Canon Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, and the threat of new entrants and substitutes, with actionable strategic implications for Canon. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It's professionally formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Canon's Porter's Five Forces snapshot highlights competitive rivalry across imaging and office equipment, supplier and buyer leverage, threat of substitutes from smartphone imaging and new entrants, and industry-specific regulatory pressures. This brief overview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy recommendations. Get the complete consultant-grade report to inform investment or strategic decisions.

Suppliers Bargaining Power

Key component concentration

High-spec image sensors, optics glass and precision mechatronics come from a narrow tier-1 base—Sony held about 45% of the global image‑sensor market in 2024, with Samsung and OmniVision rounding out roughly another 30–35%—concentrating supply and raising switching costs and lead‑time risk. Supplier leverage spikes during capacity tightness, historically widening component lead times to multiple months and pressuring margins. Canon uses dual‑sourcing where feasible, but achieving technical equivalence across suppliers is difficult.

Vertical integration buffer

Canon designs and manufactures critical modules — lenses, engines and controllers — internally, creating a vertical integration buffer that lowers supplier bargaining power and safeguards proprietary know-how. This integration supports Canon’s ~40% global share in interchangeable-lens cameras (2024), helping it negotiate better terms and stabilize quality. Nevertheless, dependence on upstream semiconductors and specialty materials remains a vulnerability.

Semiconductor dependency

Advanced sensors, memory and processors face cyclical supply and foundry constraints, with TSMC and Samsung holding roughly three-quarters of leading-edge foundry capacity in 2024, shifting allocation and pricing power to chip suppliers. Long design cycles and requalification (typically 12–24 months) limit rapid substitution. Strategic inventories of 3–6 months and multi‑year supply agreements mitigate but do not eliminate volatility.

Consumables and materials

Consumables like toner, inks and specialty coatings require consistent formulations from qualified suppliers; in 2024 the global printer consumables market was estimated at $23 billion, concentrating leverage with certified vendors.

Quality variance degrades device performance and brand perception, so Canon restricts substitution via approved-vendor lists, increasing supplier influence and switching costs.

Volume commitments and multi-year contracts secure availability and often deliver double-digit cost concessions for OEMs.

- 2024 market: $23B

- Approved-vendor lists: high switching costs

- Quality variance: direct brand/performance impact

- Volume commitments: secure supply, cost leverage

Geo-political and logistics risk

Complex cross-border supply chains expose Canon to tariff, export-control and transport disruption risks; suppliers concentrated in East Asia — Taiwan supplies about 63% of global semiconductor capacity — amplify systemic exposure. Currency swings alter input costs and negotiation leverage. Canon mitigates by diversifying suppliers and localizing production in Japan, the Philippines and Malaysia.

- Tariffs & export controls: higher compliance costs

- Regional concentration: ~63% semiconductor risk

- FX volatility: impacts input pricing

- Mitigation: diversification + local production

Sensor and foundry concentration increases supplier leverage; vertical integration reduces risk

Narrow tier‑1 supply (Sony ~45% image sensors, TSMC+Samsung ~75% leading foundry capacity, Taiwan ~63% semiconductor capacity) raises switching costs and price/lead‑time leverage; Canon's vertical integration (≈40% ILC share) plus dual‑sourcing and 3–6m inventories mitigate but not eliminate supplier power. Consumables market ~$23B concentrates vendor influence.

| Metric | 2024 value |

|---|---|

| Image sensor share (Sony) | 45% |

| Canon ILC share | ≈40% |

| Foundry concentration (TSMC+Samsung) | ≈75% |

| Semiconductor capacity (Taiwan) | ≈63% |

| Printer consumables market | $23B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Canon, uncovering key drivers of competition, buyer and supplier power, substitute threats, and barriers to entry; identifies disruptive technologies and emerging substitutes that could erode market share and provides strategic commentary to inform pricing, positioning, and defensive moves.

A concise Canon Porter's Five Forces sheet that standardizes assessments, lets you toggle scenario inputs, and outputs a radar chart—cutting analysis time and making strategic trade-offs obvious for decks and boardroom discussions.

Customers Bargaining Power

Diverse customer segments

Buyer sophistication ranges from price-sensitive consumers to hospitals, fabs and enterprises; Canon reported consolidated revenue of ¥3.9 trillion in FY2024, highlighting scale across segments. Large B2B accounts—often via tenders and SLAs—can represent double-digit share of unit-line sales and exert strong negotiating leverage. Consumers remain price-sensitive but brand and ecosystem lock-in (printers, EOS, imageRUNNER) reduce churn, creating uneven buyer power across lines.

Price transparency

Price transparency via online comparison sites and reviews compresses margins on Canon's mainstream cameras and printers, forcing greater reliance on volume; Canon reported group net sales of about ¥3.78 trillion in FY2023, with imaging contributing materially to that top line. Frequent promotions set low reference prices and buyers often delay purchases awaiting discounts, pressuring ASPs. Canon counteracts by bundling features, offering subscription service plans and extended warranties to preserve value and margin.

Switching costs and ecosystems

Lens mounts, accessories, and workflow software create high switching frictions for professional users, locking them into Canon RF/EF ecosystems and accessory investments. Managed print services and fleet management commonly use multi-year (3–5 year) contracts that embed Canon into enterprise processes. Medical and industrial product validation requires regulatory approvals (FDA/CE) and months of staff training, further raising costs to switch. These factors materially reduce buyer bargaining power in entrenched accounts.

Aftermarket leverage

Aftermarket leverage: consumables and maintenance contracts drive lifetime value and negotiation power; enterprise buyers in 2024 pushed harder on cost-per-page reductions and uptime SLAs, while third-party inks/toners — representing an estimated 20–30% of cartridge volumes — pressured pricing; Canon responded with strict chip authentication, documented quality assurance, and bundled service agreements to protect margins.

- Consumables focus: lifetime revenue stream

- Enterprise demands: CPP cuts & uptime guarantees

- Aftermarket threat: 20–30% third-party cartridge share (2024)

- Canon defenses: chip auth, QA, service bundles

Demand cyclicality

Camera and printer demand tracks macro cycles and replacement waves, so in downturns buyers delay upgrades and exert price pressure; Canon reported approximately 3.6 trillion yen in revenue for fiscal 2023, underscoring sensitivity to volume swings in 2024.

- Replacement waves intensify seasonal bargaining

- Health/education budget cycles drive purchase timing

- Canon times launches and financing to smooth demand

Buyer power skews to large B2B; consumables and MPS drive sustained lifetime value

Buyer power is uneven: large B2B accounts exert strong leverage via tenders/SLAs, while consumer price sensitivity is offset by Canon ecosystem lock-in. Price transparency and promotions compress ASPs on mainstream cameras/printers, increasing reliance on volume and services. Aftermarket consumables and multi-year MPS contracts (3–5 yrs) sustain lifetime value and reduce switching.

| Metric | 2024 |

|---|---|

| Consolidated revenue | ¥3.9 trillion |

| Third-party cartridge share | 20–30% |

| Typical MPS contract | 3–5 years |

Preview Before You Purchase

Canon Porter's Five Forces Analysis

This Canon Porter's Five Forces analysis evaluates competitive rivalry, supplier and buyer power, and the threat of new entrants and substitutes, with actionable strategic implications for Canon. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It's professionally formatted and ready for download and use the moment you buy.