Capgemini Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

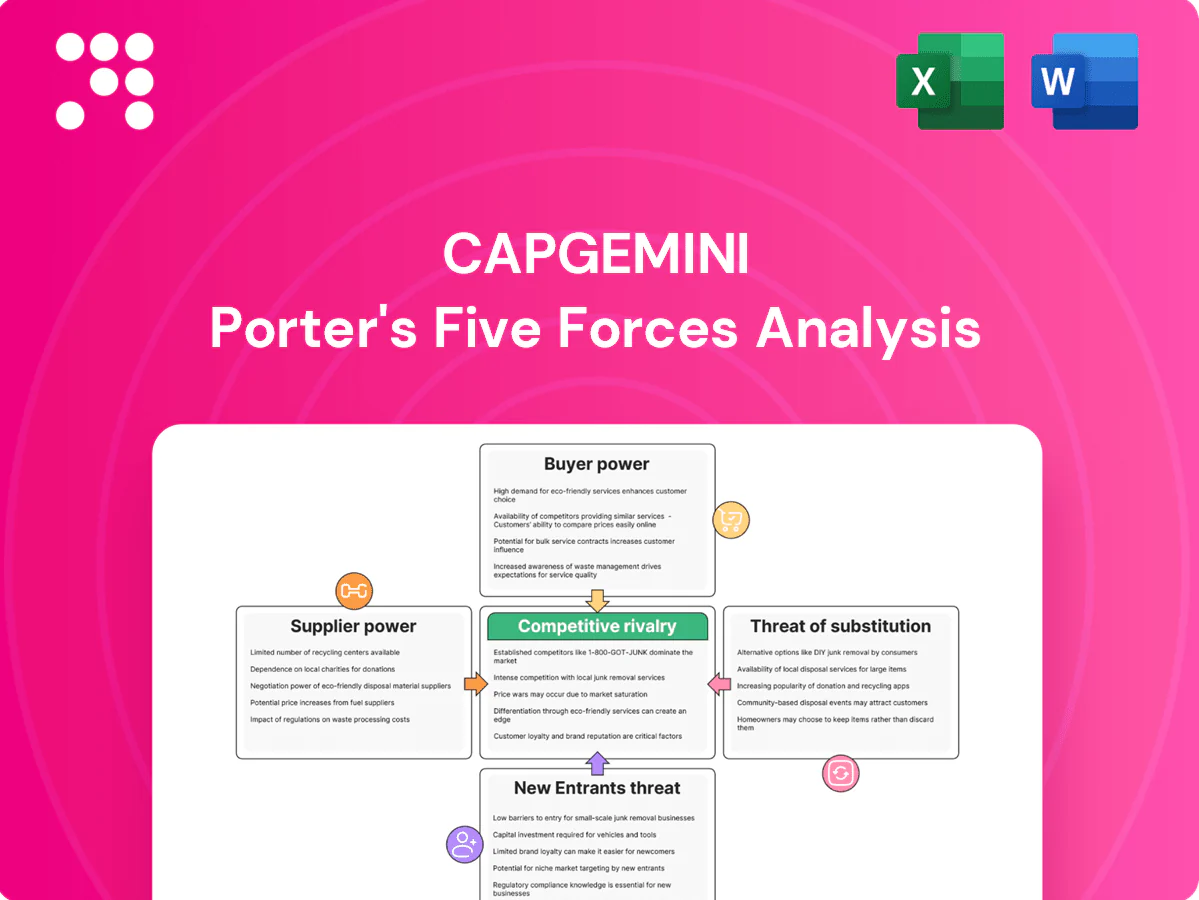

Capgemini’s Porter's Five Forces snapshot highlights competitive rivalry, buyer power, supplier influence, threat of substitutes, and new entrants shaping its consulting and tech-services edge. This brief teases strategic risks and opportunities across markets. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

Capgemini relies on AWS, Microsoft Azure and Google Cloud for many solutions, giving hyperscalers leverage on pricing, certifications and partner terms; as of 2024 AWS ~31%, Azure ~23% and GCP ~12% (Canalys). Multi-cloud architectures and client-preference diversification temper this supplier power. Co-selling and partner incentives often rebalance economics, while volume commitments secure discounts but reduce flexibility.

Specialized talent scarcity

Highly skilled engineers, data scientists and AI specialists are critical suppliers for Capgemini, which reported about 340,000 employees in 2024, yet AI roles grew roughly 25% year‑over‑year in 2024 increasing wage pressure. Competition from hyperscalers, startups and consulting peers intensifies bargaining power as big tech continued aggressive AI hiring in 2024. Global delivery centers and upskilling programs reduce but do not eliminate scarcity. Strong employer brand and clear career pathways remain key retention levers.

Enterprise software licensors

Enterprise licensors SAP, Salesforce, Microsoft, Oracle and ServiceNow control certification tracks, training access and implementation margins, with preferred-partner tiers unlocking demand but imposing compliance and multi‑million euro investment requirements; 2024 roadmap shifts have forced partner retooling at providers’ cost, though Capgemini’s diversified ISV portfolio reduces single‑vendor exposure.

Offshore delivery ecosystems

Offshore delivery ecosystems rely heavily on local universities, staffing firms and subcontractors, which influence rate cards and capacity; Capgemini had about 340,000 employees across roughly 50 countries in 2024, diluting single-market supplier leverage.

Wage inflation, attrition and regulatory shifts in key hubs like India and the Philippines can raise local supplier power, while multi-country footprints and internal academies plus long-term vendor frameworks stabilize supply.

- Local talent dependence

- 340,000 employees ~50 countries

- Wage/attrition risk

- Academies & multi-country dilution

- Long-term vendor contracts

Data, tools, and IP providers

Access to data sets, model APIs, cybersecurity tools and niche platforms remain key bottlenecks in AI and analytics deals, with 2024 surveys reporting 60% of enterprises naming data access as a top constraint. Usage-based pricing for model APIs can compress project margins by 10–30% on typical proofs-of-value. Building proprietary accelerators and adopting open-source models reduces supplier dependence, while strategic co-development deals align incentives and share risk.

- Data access risk: 60% (2024)

- Margin impact: usage fees 10–30%

- Mitigants: proprietary accelerators, open-source

- Strategy: co-development agreements

IT services face hyperscaler power, talent squeeze and data-cost margin pressure

Capgemini faces strong supplier power from hyperscalers (AWS 31%, Azure 23%, GCP 12% in 2024) and enterprise ISVs, but multi-cloud, co-selling and partner tiers mitigate leverage. Talent scarcity (340,000 employees, AI roles +25% YoY in 2024) and wage inflation increase costs; academies and offshore scale dilute risk. Data access cited by 60% of enterprises (2024); model API fees can cut margins 10–30%.

| Metric | 2024 |

|---|---|

| Hyperscaler share | AWS 31%/Azure 23%/GCP 12% |

| Employees | 340,000 |

| AI roles growth | +25% YoY |

| Data access risk | 60% |

| API fee margin hit | 10–30% |

What is included in the product

Concise Porter's Five Forces assessment of Capgemini, detailing competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and highlighting disruptive technologies and market barriers affecting its pricing power and profitability.

A clear, one-sheet Capgemini Porter's Five Forces summary that visualizes strategic pressure with an editable spider chart for quick decisions, customizable with your own data and ready to drop into pitch decks, Excel dashboards or boardroom reports.

Customers Bargaining Power

Large enterprise procurement

Large enterprise procurement runs competitive RFPs and master services agreements that exert strong price and term pressure; Gartner 2024 estimates the global IT services market near $1.5 trillion, intensifying supplier competition. Their scale and multi-year deals—often spanning 3–5 years and tens of millions in contract value—raise bargaining power. Outcome-based pricing and strict SLAs shift risk to suppliers, though strong references and niche expertise can command premiums.

Multi-sourcing and vendor rotation

Clients split portfolios among multiple integrators—over 60% of enterprises multi-source by 2024—driving continuous price and performance benchmarking that forces Capgemini to defend share through delivery excellence and innovation; recent vendor consolidation waves (M&A deal value up ~35% in 2023–24) can rapidly swing bargaining power, tightening margins when buyers consolidate suppliers.

Moderate switching costs

While client system knowledge creates stickiness, extensive documentation and standardized cloud stacks lower lock-in and make switching feasible; transition services and knowledge-transfer clauses further ease moves. In 2024 Capgemini, with about 340,000 employees and FY2023 revenue €20.1bn, counters churn by embedding IP, accelerators and managed services. Its trusted-advisor status raises perceived switching costs despite moderate actual barriers.

Demand for rapid digital outcomes

Clients demand rapid AI, data and cloud outcomes, forcing Capgemini into fixed-price, agile and value-based contracts; compressed timelines increase delivery risk and pricing pressure. Reusable accelerators and IP are essential to protect margins and meet SLAs. PoCs must convert to scaled engagements quickly; 2024 surveys show about 56% of firms accelerated AI/cloud deployment.

- Fixed-price/value contracts pressure pricing

- 56% accelerated AI/cloud in 2024

- Accelerators/IP preserve margins

ESG, security, and compliance requirements

Buyers impose stringent data, privacy and sustainability criteria that reshape Capgemini delivery models and increase total cost of ownership; GDPR fines exceeded €1.3bn in 2023, underscoring penalty risk. Meeting ESG and security standards can be a differentiator but often requires non-billable compliance effort, while certifications and attestations reduce procurement friction. Failure to comply can lead to disqualification from bids and regulatory penalties.

- Data/privacy: GDPR fines €1.3bn (2023)

- ESG demand: >60% of buyers require ESG attestations (2024 surveys)

- Cost: compliance adds non-billable hours

- Procurement: certifications reduce bid friction

Buyers gain leverage in €1.5T IT services market; 60% multi-source, 56% AI/cloud adoption

Clients exert strong price and term pressure via competitive RFPs and multi-year, multi-million deals; Gartner 2024 IT services market ~1.5T increases buyer leverage. 60%+ enterprises multi-source (2024) and 56% accelerated AI/cloud, compressing timelines and shifting risk to firms like Capgemini (FY2023 rev €20.1bn, 340k emp). Compliance (GDPR fines €1.3bn 2023) raises non-billable costs.

| Metric | Value |

|---|---|

| Market size 2024 | €1.5T |

| Multi-source | 60%+ |

| AI/cloud accel | 56% |

| Capgemini FY2023 | €20.1bn |

| GDPR fines 2023 | €1.3bn |

Preview the Actual Deliverable

Capgemini Porter's Five Forces Analysis

This Capgemini Porter's Five Forces Analysis delivers a thorough evaluation of industry rivalry, supplier and buyer power, threat of new entrants, and substitute pressures, tailored to Capgemini's business model and market dynamics. This preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples—ready for download and use as-is.

A Must-Have Tool for Decision-Makers

Capgemini’s Porter's Five Forces snapshot highlights competitive rivalry, buyer power, supplier influence, threat of substitutes, and new entrants shaping its consulting and tech-services edge. This brief teases strategic risks and opportunities across markets. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

Capgemini relies on AWS, Microsoft Azure and Google Cloud for many solutions, giving hyperscalers leverage on pricing, certifications and partner terms; as of 2024 AWS ~31%, Azure ~23% and GCP ~12% (Canalys). Multi-cloud architectures and client-preference diversification temper this supplier power. Co-selling and partner incentives often rebalance economics, while volume commitments secure discounts but reduce flexibility.

Specialized talent scarcity

Highly skilled engineers, data scientists and AI specialists are critical suppliers for Capgemini, which reported about 340,000 employees in 2024, yet AI roles grew roughly 25% year‑over‑year in 2024 increasing wage pressure. Competition from hyperscalers, startups and consulting peers intensifies bargaining power as big tech continued aggressive AI hiring in 2024. Global delivery centers and upskilling programs reduce but do not eliminate scarcity. Strong employer brand and clear career pathways remain key retention levers.

Enterprise software licensors

Enterprise licensors SAP, Salesforce, Microsoft, Oracle and ServiceNow control certification tracks, training access and implementation margins, with preferred-partner tiers unlocking demand but imposing compliance and multi‑million euro investment requirements; 2024 roadmap shifts have forced partner retooling at providers’ cost, though Capgemini’s diversified ISV portfolio reduces single‑vendor exposure.

Offshore delivery ecosystems

Offshore delivery ecosystems rely heavily on local universities, staffing firms and subcontractors, which influence rate cards and capacity; Capgemini had about 340,000 employees across roughly 50 countries in 2024, diluting single-market supplier leverage.

Wage inflation, attrition and regulatory shifts in key hubs like India and the Philippines can raise local supplier power, while multi-country footprints and internal academies plus long-term vendor frameworks stabilize supply.

- Local talent dependence

- 340,000 employees ~50 countries

- Wage/attrition risk

- Academies & multi-country dilution

- Long-term vendor contracts

Data, tools, and IP providers

Access to data sets, model APIs, cybersecurity tools and niche platforms remain key bottlenecks in AI and analytics deals, with 2024 surveys reporting 60% of enterprises naming data access as a top constraint. Usage-based pricing for model APIs can compress project margins by 10–30% on typical proofs-of-value. Building proprietary accelerators and adopting open-source models reduces supplier dependence, while strategic co-development deals align incentives and share risk.

- Data access risk: 60% (2024)

- Margin impact: usage fees 10–30%

- Mitigants: proprietary accelerators, open-source

- Strategy: co-development agreements

IT services face hyperscaler power, talent squeeze and data-cost margin pressure

Capgemini faces strong supplier power from hyperscalers (AWS 31%, Azure 23%, GCP 12% in 2024) and enterprise ISVs, but multi-cloud, co-selling and partner tiers mitigate leverage. Talent scarcity (340,000 employees, AI roles +25% YoY in 2024) and wage inflation increase costs; academies and offshore scale dilute risk. Data access cited by 60% of enterprises (2024); model API fees can cut margins 10–30%.

| Metric | 2024 |

|---|---|

| Hyperscaler share | AWS 31%/Azure 23%/GCP 12% |

| Employees | 340,000 |

| AI roles growth | +25% YoY |

| Data access risk | 60% |

| API fee margin hit | 10–30% |

What is included in the product

Concise Porter's Five Forces assessment of Capgemini, detailing competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and highlighting disruptive technologies and market barriers affecting its pricing power and profitability.

A clear, one-sheet Capgemini Porter's Five Forces summary that visualizes strategic pressure with an editable spider chart for quick decisions, customizable with your own data and ready to drop into pitch decks, Excel dashboards or boardroom reports.

Customers Bargaining Power

Large enterprise procurement

Large enterprise procurement runs competitive RFPs and master services agreements that exert strong price and term pressure; Gartner 2024 estimates the global IT services market near $1.5 trillion, intensifying supplier competition. Their scale and multi-year deals—often spanning 3–5 years and tens of millions in contract value—raise bargaining power. Outcome-based pricing and strict SLAs shift risk to suppliers, though strong references and niche expertise can command premiums.

Multi-sourcing and vendor rotation

Clients split portfolios among multiple integrators—over 60% of enterprises multi-source by 2024—driving continuous price and performance benchmarking that forces Capgemini to defend share through delivery excellence and innovation; recent vendor consolidation waves (M&A deal value up ~35% in 2023–24) can rapidly swing bargaining power, tightening margins when buyers consolidate suppliers.

Moderate switching costs

While client system knowledge creates stickiness, extensive documentation and standardized cloud stacks lower lock-in and make switching feasible; transition services and knowledge-transfer clauses further ease moves. In 2024 Capgemini, with about 340,000 employees and FY2023 revenue €20.1bn, counters churn by embedding IP, accelerators and managed services. Its trusted-advisor status raises perceived switching costs despite moderate actual barriers.

Demand for rapid digital outcomes

Clients demand rapid AI, data and cloud outcomes, forcing Capgemini into fixed-price, agile and value-based contracts; compressed timelines increase delivery risk and pricing pressure. Reusable accelerators and IP are essential to protect margins and meet SLAs. PoCs must convert to scaled engagements quickly; 2024 surveys show about 56% of firms accelerated AI/cloud deployment.

- Fixed-price/value contracts pressure pricing

- 56% accelerated AI/cloud in 2024

- Accelerators/IP preserve margins

ESG, security, and compliance requirements

Buyers impose stringent data, privacy and sustainability criteria that reshape Capgemini delivery models and increase total cost of ownership; GDPR fines exceeded €1.3bn in 2023, underscoring penalty risk. Meeting ESG and security standards can be a differentiator but often requires non-billable compliance effort, while certifications and attestations reduce procurement friction. Failure to comply can lead to disqualification from bids and regulatory penalties.

- Data/privacy: GDPR fines €1.3bn (2023)

- ESG demand: >60% of buyers require ESG attestations (2024 surveys)

- Cost: compliance adds non-billable hours

- Procurement: certifications reduce bid friction

Buyers gain leverage in €1.5T IT services market; 60% multi-source, 56% AI/cloud adoption

Clients exert strong price and term pressure via competitive RFPs and multi-year, multi-million deals; Gartner 2024 IT services market ~1.5T increases buyer leverage. 60%+ enterprises multi-source (2024) and 56% accelerated AI/cloud, compressing timelines and shifting risk to firms like Capgemini (FY2023 rev €20.1bn, 340k emp). Compliance (GDPR fines €1.3bn 2023) raises non-billable costs.

| Metric | Value |

|---|---|

| Market size 2024 | €1.5T |

| Multi-source | 60%+ |

| AI/cloud accel | 56% |

| Capgemini FY2023 | €20.1bn |

| GDPR fines 2023 | €1.3bn |

Preview the Actual Deliverable

Capgemini Porter's Five Forces Analysis

This Capgemini Porter's Five Forces Analysis delivers a thorough evaluation of industry rivalry, supplier and buyer power, threat of new entrants, and substitute pressures, tailored to Capgemini's business model and market dynamics. This preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples—ready for download and use as-is.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Capgemini’s Porter's Five Forces snapshot highlights competitive rivalry, buyer power, supplier influence, threat of substitutes, and new entrants shaping its consulting and tech-services edge. This brief teases strategic risks and opportunities across markets. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

Capgemini relies on AWS, Microsoft Azure and Google Cloud for many solutions, giving hyperscalers leverage on pricing, certifications and partner terms; as of 2024 AWS ~31%, Azure ~23% and GCP ~12% (Canalys). Multi-cloud architectures and client-preference diversification temper this supplier power. Co-selling and partner incentives often rebalance economics, while volume commitments secure discounts but reduce flexibility.

Specialized talent scarcity

Highly skilled engineers, data scientists and AI specialists are critical suppliers for Capgemini, which reported about 340,000 employees in 2024, yet AI roles grew roughly 25% year‑over‑year in 2024 increasing wage pressure. Competition from hyperscalers, startups and consulting peers intensifies bargaining power as big tech continued aggressive AI hiring in 2024. Global delivery centers and upskilling programs reduce but do not eliminate scarcity. Strong employer brand and clear career pathways remain key retention levers.

Enterprise software licensors

Enterprise licensors SAP, Salesforce, Microsoft, Oracle and ServiceNow control certification tracks, training access and implementation margins, with preferred-partner tiers unlocking demand but imposing compliance and multi‑million euro investment requirements; 2024 roadmap shifts have forced partner retooling at providers’ cost, though Capgemini’s diversified ISV portfolio reduces single‑vendor exposure.

Offshore delivery ecosystems

Offshore delivery ecosystems rely heavily on local universities, staffing firms and subcontractors, which influence rate cards and capacity; Capgemini had about 340,000 employees across roughly 50 countries in 2024, diluting single-market supplier leverage.

Wage inflation, attrition and regulatory shifts in key hubs like India and the Philippines can raise local supplier power, while multi-country footprints and internal academies plus long-term vendor frameworks stabilize supply.

- Local talent dependence

- 340,000 employees ~50 countries

- Wage/attrition risk

- Academies & multi-country dilution

- Long-term vendor contracts

Data, tools, and IP providers

Access to data sets, model APIs, cybersecurity tools and niche platforms remain key bottlenecks in AI and analytics deals, with 2024 surveys reporting 60% of enterprises naming data access as a top constraint. Usage-based pricing for model APIs can compress project margins by 10–30% on typical proofs-of-value. Building proprietary accelerators and adopting open-source models reduces supplier dependence, while strategic co-development deals align incentives and share risk.

- Data access risk: 60% (2024)

- Margin impact: usage fees 10–30%

- Mitigants: proprietary accelerators, open-source

- Strategy: co-development agreements

IT services face hyperscaler power, talent squeeze and data-cost margin pressure

Capgemini faces strong supplier power from hyperscalers (AWS 31%, Azure 23%, GCP 12% in 2024) and enterprise ISVs, but multi-cloud, co-selling and partner tiers mitigate leverage. Talent scarcity (340,000 employees, AI roles +25% YoY in 2024) and wage inflation increase costs; academies and offshore scale dilute risk. Data access cited by 60% of enterprises (2024); model API fees can cut margins 10–30%.

| Metric | 2024 |

|---|---|

| Hyperscaler share | AWS 31%/Azure 23%/GCP 12% |

| Employees | 340,000 |

| AI roles growth | +25% YoY |

| Data access risk | 60% |

| API fee margin hit | 10–30% |

What is included in the product

Concise Porter's Five Forces assessment of Capgemini, detailing competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and highlighting disruptive technologies and market barriers affecting its pricing power and profitability.

A clear, one-sheet Capgemini Porter's Five Forces summary that visualizes strategic pressure with an editable spider chart for quick decisions, customizable with your own data and ready to drop into pitch decks, Excel dashboards or boardroom reports.

Customers Bargaining Power

Large enterprise procurement

Large enterprise procurement runs competitive RFPs and master services agreements that exert strong price and term pressure; Gartner 2024 estimates the global IT services market near $1.5 trillion, intensifying supplier competition. Their scale and multi-year deals—often spanning 3–5 years and tens of millions in contract value—raise bargaining power. Outcome-based pricing and strict SLAs shift risk to suppliers, though strong references and niche expertise can command premiums.

Multi-sourcing and vendor rotation

Clients split portfolios among multiple integrators—over 60% of enterprises multi-source by 2024—driving continuous price and performance benchmarking that forces Capgemini to defend share through delivery excellence and innovation; recent vendor consolidation waves (M&A deal value up ~35% in 2023–24) can rapidly swing bargaining power, tightening margins when buyers consolidate suppliers.

Moderate switching costs

While client system knowledge creates stickiness, extensive documentation and standardized cloud stacks lower lock-in and make switching feasible; transition services and knowledge-transfer clauses further ease moves. In 2024 Capgemini, with about 340,000 employees and FY2023 revenue €20.1bn, counters churn by embedding IP, accelerators and managed services. Its trusted-advisor status raises perceived switching costs despite moderate actual barriers.

Demand for rapid digital outcomes

Clients demand rapid AI, data and cloud outcomes, forcing Capgemini into fixed-price, agile and value-based contracts; compressed timelines increase delivery risk and pricing pressure. Reusable accelerators and IP are essential to protect margins and meet SLAs. PoCs must convert to scaled engagements quickly; 2024 surveys show about 56% of firms accelerated AI/cloud deployment.

- Fixed-price/value contracts pressure pricing

- 56% accelerated AI/cloud in 2024

- Accelerators/IP preserve margins

ESG, security, and compliance requirements

Buyers impose stringent data, privacy and sustainability criteria that reshape Capgemini delivery models and increase total cost of ownership; GDPR fines exceeded €1.3bn in 2023, underscoring penalty risk. Meeting ESG and security standards can be a differentiator but often requires non-billable compliance effort, while certifications and attestations reduce procurement friction. Failure to comply can lead to disqualification from bids and regulatory penalties.

- Data/privacy: GDPR fines €1.3bn (2023)

- ESG demand: >60% of buyers require ESG attestations (2024 surveys)

- Cost: compliance adds non-billable hours

- Procurement: certifications reduce bid friction

Buyers gain leverage in €1.5T IT services market; 60% multi-source, 56% AI/cloud adoption

Clients exert strong price and term pressure via competitive RFPs and multi-year, multi-million deals; Gartner 2024 IT services market ~1.5T increases buyer leverage. 60%+ enterprises multi-source (2024) and 56% accelerated AI/cloud, compressing timelines and shifting risk to firms like Capgemini (FY2023 rev €20.1bn, 340k emp). Compliance (GDPR fines €1.3bn 2023) raises non-billable costs.

| Metric | Value |

|---|---|

| Market size 2024 | €1.5T |

| Multi-source | 60%+ |

| AI/cloud accel | 56% |

| Capgemini FY2023 | €20.1bn |

| GDPR fines 2023 | €1.3bn |

Preview the Actual Deliverable

Capgemini Porter's Five Forces Analysis

This Capgemini Porter's Five Forces Analysis delivers a thorough evaluation of industry rivalry, supplier and buyer power, threat of new entrants, and substitute pressures, tailored to Capgemini's business model and market dynamics. This preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples—ready for download and use as-is.