Capstone Infrastructure Boston Consulting Group Matrix

See the Bigger Picture

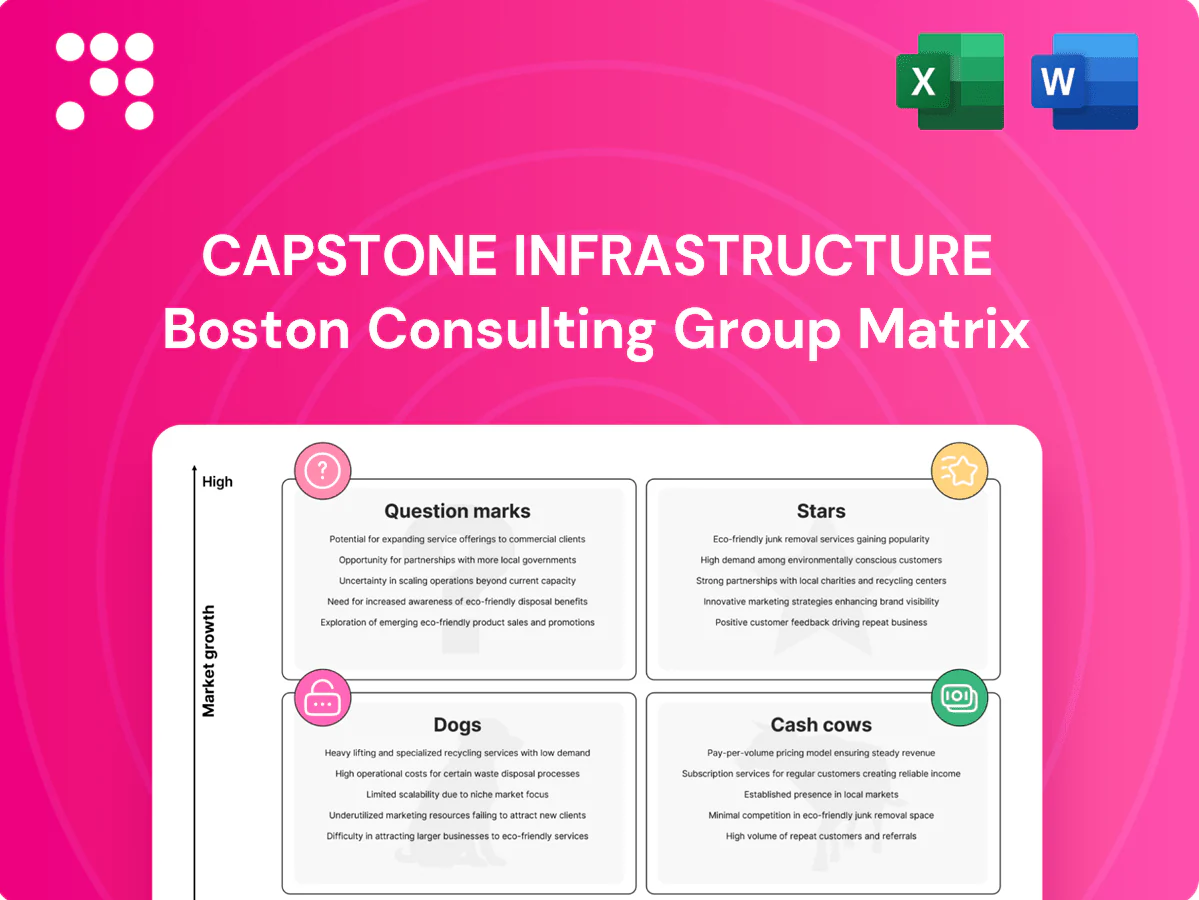

Curious where Capstone Infrastructure’s offerings land — Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full BCG Matrix lays out quadrant-by-quadrant placements, data-backed recommendations, and clear strategic moves you can act on. Buy the complete report for a polished Word document plus an Excel summary you can use in board decks and planning sessions. Get instant access and stop guessing—make decisions with confidence.

Stars

Contracted Wind in Growth Provinces

High-share contracted wind assets in growth provinces (where 2024 provincial procurements rose ~35% year-over-year) dominate local pockets, absorbing capital for repowers, grid upgrades and O&M; they convert investment into rising generation and higher availability. Maintain share and targeted reinvestment and these Stars typically transition into cash cows with improving EBITDA margins; miss the 2024 window and you offload opportunity to competitors.

Utility-Scale Solar Expansions on Existing Sites

Brownfield utility-scale solar add-ons leverage sites where permits, interconnection and land are pre-secured, tapping a market that followed global PV additions topping 200 GW in 2023 and stayed brisk into 2024. Capstone’s platform advantage preserves share versus new entrants, though projects are capital-hungry now; margins improve as scale dilutes fixed costs. Hold the ground and it matures into a dependable cash engine.

Renewables with Long-Dated PPAs in Tight Power Markets

Markets with rising load and retiring thermal plants give long‑dated PPAs (10–25 years) real pricing power on extensions as scarcity tightens; global electricity demand rose about 2% in 2023 (IEA). Share is strong, growth runway intact, and counterparties increasingly pay for firm, contracted renewable supply. It consumes cash today for repowers, life extensions and tech upgrades but throws off predictable returns. The path to cow status is straight.

Portfolio-Level Operations Excellence (O&M Edge)

Portfolio-Level Operations Excellence (O&M Edge) delivers >99.5% fleet uptime and data-driven dispatch boosting effective megawatt output by ~2–4% (2024 industry benchmarks), creating a durable bidding moat in growth markets. Doing more with the same MW wins bids and extensions. Steady investment in talent and tech compounds payoff across the fleet.

- Uptime >99.5% (2024)

- +2–4% effective MW output

- Higher revenue/MW, more contract wins

- Requires sustained talent & tech investment

Selective M&A of Bolt-On Renewables

Capstone’s repeatable playbook targets mid-market renewables (5–50 MW), enabling rapid scale in high-growth corridors; share gains come from disciplined bids rather than trophy deals. Integration costs are real (commonly ~5–10% of deal capex), but operating synergies and tax attributes typically offset that burn, and steady acquisition cadence makes the platform self-funding.

- Tag: repeatable playbook

- Tag: mid-market 5–50 MW

- Tag: disciplined bids not trophies

- Tag: integration ~5–10% capex

- Tag: self-funding cadence

Repowered wind & brownfield solar scale in 2024 — +35% procurements, uptime >99.5%

High-share contracted wind and brownfield solar in 2024 growth provinces (provincial procurements +35% YoY) consume repower/grid capex but lift generation and margins; uptime >99.5% and +2–4% effective MW output (2024) compound wins. Long PPAs (10–25y) capture scarcity pricing as demand rose ~2% (2023). Repeatable mid-market play (5–50 MW) scales; integration ~5–10% capex.

| Tag | Metric |

|---|---|

| Share | High |

| Growth | +35% procurements (2024) |

| Uptime | >99.5% (2024) |

| MW impact | +2–4% (2024) |

| Integration | ~5–10% capex |

What is included in the product

Comprehensive BCG review of Capstone Infrastructure, mapping units to Stars, Cash Cows, Question Marks and Dogs with clear strategic actions.

One-page Capstone Infrastructure BCG Matrix pinpoints underperformers and winners, simplifying strategic decisions for founders and CFOs.

Cash Cows

Legacy Solar under FIT/Contracted Regimes

Legacy solar under FIT/contracted regimes delivers steady, low-volatility cash from long-term tenors (typically 15–25 years) and PV capacity factors ~20–25%, requiring minimal promotional spend and negligible growth capex; as of 2024 these assets routinely support DSCR targets of ~1.2–1.5, making them ideal to service debt, pay dividends and fund higher-growth bets—maintain, optimize, and quietly milk.

Run-of-River Hydro with Stable Hydrology

Proven run-of-river assets deliver predictable output with industry 2024 capacity factors around 40–60% and availability exceeding 95%, producing steady cash flows and low variable costs (O&M commonly in the $10–20/MWh range). Little promotion is needed—focus on reliability to sustain high utilization; incremental capex (turbine upgrades, control systems) can raise efficiency by several percentage points and extend life by 10–20 years. Classic cash-cow dynamics: net operating cash inflows typically exceed maintenance and financing outflows, supporting dividend-like distributions or reinvestment.

Regulated or Quasi-Regulated Utility Stakes

Regulated or quasi-regulated utility stakes deliver rate-based returns in mature markets with low growth (typically 0–2% volumetric demand), providing predictable revenue streams. Once capex cycles normalize these assets can convert well over 70% of EBITDA to free cash flow, ideal for funding development pipelines and corporate overhead. Maintain tight compliance and lean operations to protect cash generation and credit metrics.

Contracted Natural Gas CHP with Residual Term

Contracted natural gas CHP with residual term remains cash generative in 2024, delivering stable free cash flow despite muted volume growth; predictable opex and comprehensive fuel hedges implemented in 2024 enhance revenue visibility. Surplus cash is earmarked to finance renewables and battery storage rollouts, while management prepares orderly end-of-term strategies to preserve asset value.

- Still contracted — steady cash flow (2024)

- Opex known; 2024 fuel hedges improve predictability

- Surplus funds to bankroll renewables & storage

- Plan end-of-term strategies to preserve value

Long-Tenor O&M/Asset Management Contracts

Long-tenor O&M and asset management contracts deliver service revenues tied to operating assets across Capstone's portfolio, providing high-margin, low-growth and sticky cash flows that support the corporate engine without large capital calls; in 2024 these contracts continued to quietly compound while higher-growth assets attract active investment.

- Service revenues tied to operating assets

- High-margin, low-growth, sticky

- Supports corporate cashflow with minimal capex

- Quiet compounding in 2024 while stars run hard

Low-volatility renewables + regulated assets deliver reliable cash & strong FCF (2024)

Legacy FIT solar, run-of-river hydro, regulated utility stakes, contracted CHP and long-tenor O&M contracts form Capstone's cash cows, delivering low-volatility, high-conversion cash (2024) to fund growth. Typical 2024 DSCR/FCF conversion ranges: solar 1.2–1.5, hydro 60–80% EBITDA→FCF, utilities >70%, CHP stable via hedges. Prioritize reliability, selective life-extension capex, and dividend-style distributions.

| Asset | CF profile 2024 | Cap fac | DSCR/FCF conv |

|---|---|---|---|

| FIT solar | Steady contracted cash | 20–25% | DSCR 1.2–1.5 |

| Run-of-river | Predictable output | 40–60% | 60–80% |

| Regulated utilities | Rate-based | n/a | >70% |

| CHP | Contracted, hedged | n/a | Stable |

| O&M contracts | Sticky service rev | n/a | High-margin |

What You’re Viewing Is Included

Capstone Infrastructure BCG Matrix

The Capstone Infrastructure BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholders—just the full, professionally formatted strategic report. It's ready to edit, print, or present to stakeholders immediately. Buy once and get the complete, analysis-ready document straight to your inbox.

See the Bigger Picture

Curious where Capstone Infrastructure’s offerings land — Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full BCG Matrix lays out quadrant-by-quadrant placements, data-backed recommendations, and clear strategic moves you can act on. Buy the complete report for a polished Word document plus an Excel summary you can use in board decks and planning sessions. Get instant access and stop guessing—make decisions with confidence.

Stars

Contracted Wind in Growth Provinces

High-share contracted wind assets in growth provinces (where 2024 provincial procurements rose ~35% year-over-year) dominate local pockets, absorbing capital for repowers, grid upgrades and O&M; they convert investment into rising generation and higher availability. Maintain share and targeted reinvestment and these Stars typically transition into cash cows with improving EBITDA margins; miss the 2024 window and you offload opportunity to competitors.

Utility-Scale Solar Expansions on Existing Sites

Brownfield utility-scale solar add-ons leverage sites where permits, interconnection and land are pre-secured, tapping a market that followed global PV additions topping 200 GW in 2023 and stayed brisk into 2024. Capstone’s platform advantage preserves share versus new entrants, though projects are capital-hungry now; margins improve as scale dilutes fixed costs. Hold the ground and it matures into a dependable cash engine.

Renewables with Long-Dated PPAs in Tight Power Markets

Markets with rising load and retiring thermal plants give long‑dated PPAs (10–25 years) real pricing power on extensions as scarcity tightens; global electricity demand rose about 2% in 2023 (IEA). Share is strong, growth runway intact, and counterparties increasingly pay for firm, contracted renewable supply. It consumes cash today for repowers, life extensions and tech upgrades but throws off predictable returns. The path to cow status is straight.

Portfolio-Level Operations Excellence (O&M Edge)

Portfolio-Level Operations Excellence (O&M Edge) delivers >99.5% fleet uptime and data-driven dispatch boosting effective megawatt output by ~2–4% (2024 industry benchmarks), creating a durable bidding moat in growth markets. Doing more with the same MW wins bids and extensions. Steady investment in talent and tech compounds payoff across the fleet.

- Uptime >99.5% (2024)

- +2–4% effective MW output

- Higher revenue/MW, more contract wins

- Requires sustained talent & tech investment

Selective M&A of Bolt-On Renewables

Capstone’s repeatable playbook targets mid-market renewables (5–50 MW), enabling rapid scale in high-growth corridors; share gains come from disciplined bids rather than trophy deals. Integration costs are real (commonly ~5–10% of deal capex), but operating synergies and tax attributes typically offset that burn, and steady acquisition cadence makes the platform self-funding.

- Tag: repeatable playbook

- Tag: mid-market 5–50 MW

- Tag: disciplined bids not trophies

- Tag: integration ~5–10% capex

- Tag: self-funding cadence

Repowered wind & brownfield solar scale in 2024 — +35% procurements, uptime >99.5%

High-share contracted wind and brownfield solar in 2024 growth provinces (provincial procurements +35% YoY) consume repower/grid capex but lift generation and margins; uptime >99.5% and +2–4% effective MW output (2024) compound wins. Long PPAs (10–25y) capture scarcity pricing as demand rose ~2% (2023). Repeatable mid-market play (5–50 MW) scales; integration ~5–10% capex.

| Tag | Metric |

|---|---|

| Share | High |

| Growth | +35% procurements (2024) |

| Uptime | >99.5% (2024) |

| MW impact | +2–4% (2024) |

| Integration | ~5–10% capex |

What is included in the product

Comprehensive BCG review of Capstone Infrastructure, mapping units to Stars, Cash Cows, Question Marks and Dogs with clear strategic actions.

One-page Capstone Infrastructure BCG Matrix pinpoints underperformers and winners, simplifying strategic decisions for founders and CFOs.

Cash Cows

Legacy Solar under FIT/Contracted Regimes

Legacy solar under FIT/contracted regimes delivers steady, low-volatility cash from long-term tenors (typically 15–25 years) and PV capacity factors ~20–25%, requiring minimal promotional spend and negligible growth capex; as of 2024 these assets routinely support DSCR targets of ~1.2–1.5, making them ideal to service debt, pay dividends and fund higher-growth bets—maintain, optimize, and quietly milk.

Run-of-River Hydro with Stable Hydrology

Proven run-of-river assets deliver predictable output with industry 2024 capacity factors around 40–60% and availability exceeding 95%, producing steady cash flows and low variable costs (O&M commonly in the $10–20/MWh range). Little promotion is needed—focus on reliability to sustain high utilization; incremental capex (turbine upgrades, control systems) can raise efficiency by several percentage points and extend life by 10–20 years. Classic cash-cow dynamics: net operating cash inflows typically exceed maintenance and financing outflows, supporting dividend-like distributions or reinvestment.

Regulated or Quasi-Regulated Utility Stakes

Regulated or quasi-regulated utility stakes deliver rate-based returns in mature markets with low growth (typically 0–2% volumetric demand), providing predictable revenue streams. Once capex cycles normalize these assets can convert well over 70% of EBITDA to free cash flow, ideal for funding development pipelines and corporate overhead. Maintain tight compliance and lean operations to protect cash generation and credit metrics.

Contracted Natural Gas CHP with Residual Term

Contracted natural gas CHP with residual term remains cash generative in 2024, delivering stable free cash flow despite muted volume growth; predictable opex and comprehensive fuel hedges implemented in 2024 enhance revenue visibility. Surplus cash is earmarked to finance renewables and battery storage rollouts, while management prepares orderly end-of-term strategies to preserve asset value.

- Still contracted — steady cash flow (2024)

- Opex known; 2024 fuel hedges improve predictability

- Surplus funds to bankroll renewables & storage

- Plan end-of-term strategies to preserve value

Long-Tenor O&M/Asset Management Contracts

Long-tenor O&M and asset management contracts deliver service revenues tied to operating assets across Capstone's portfolio, providing high-margin, low-growth and sticky cash flows that support the corporate engine without large capital calls; in 2024 these contracts continued to quietly compound while higher-growth assets attract active investment.

- Service revenues tied to operating assets

- High-margin, low-growth, sticky

- Supports corporate cashflow with minimal capex

- Quiet compounding in 2024 while stars run hard

Low-volatility renewables + regulated assets deliver reliable cash & strong FCF (2024)

Legacy FIT solar, run-of-river hydro, regulated utility stakes, contracted CHP and long-tenor O&M contracts form Capstone's cash cows, delivering low-volatility, high-conversion cash (2024) to fund growth. Typical 2024 DSCR/FCF conversion ranges: solar 1.2–1.5, hydro 60–80% EBITDA→FCF, utilities >70%, CHP stable via hedges. Prioritize reliability, selective life-extension capex, and dividend-style distributions.

| Asset | CF profile 2024 | Cap fac | DSCR/FCF conv |

|---|---|---|---|

| FIT solar | Steady contracted cash | 20–25% | DSCR 1.2–1.5 |

| Run-of-river | Predictable output | 40–60% | 60–80% |

| Regulated utilities | Rate-based | n/a | >70% |

| CHP | Contracted, hedged | n/a | Stable |

| O&M contracts | Sticky service rev | n/a | High-margin |

What You’re Viewing Is Included

Capstone Infrastructure BCG Matrix

The Capstone Infrastructure BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholders—just the full, professionally formatted strategic report. It's ready to edit, print, or present to stakeholders immediately. Buy once and get the complete, analysis-ready document straight to your inbox.

Description

See the Bigger Picture

Curious where Capstone Infrastructure’s offerings land — Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full BCG Matrix lays out quadrant-by-quadrant placements, data-backed recommendations, and clear strategic moves you can act on. Buy the complete report for a polished Word document plus an Excel summary you can use in board decks and planning sessions. Get instant access and stop guessing—make decisions with confidence.

Stars

Contracted Wind in Growth Provinces

High-share contracted wind assets in growth provinces (where 2024 provincial procurements rose ~35% year-over-year) dominate local pockets, absorbing capital for repowers, grid upgrades and O&M; they convert investment into rising generation and higher availability. Maintain share and targeted reinvestment and these Stars typically transition into cash cows with improving EBITDA margins; miss the 2024 window and you offload opportunity to competitors.

Utility-Scale Solar Expansions on Existing Sites

Brownfield utility-scale solar add-ons leverage sites where permits, interconnection and land are pre-secured, tapping a market that followed global PV additions topping 200 GW in 2023 and stayed brisk into 2024. Capstone’s platform advantage preserves share versus new entrants, though projects are capital-hungry now; margins improve as scale dilutes fixed costs. Hold the ground and it matures into a dependable cash engine.

Renewables with Long-Dated PPAs in Tight Power Markets

Markets with rising load and retiring thermal plants give long‑dated PPAs (10–25 years) real pricing power on extensions as scarcity tightens; global electricity demand rose about 2% in 2023 (IEA). Share is strong, growth runway intact, and counterparties increasingly pay for firm, contracted renewable supply. It consumes cash today for repowers, life extensions and tech upgrades but throws off predictable returns. The path to cow status is straight.

Portfolio-Level Operations Excellence (O&M Edge)

Portfolio-Level Operations Excellence (O&M Edge) delivers >99.5% fleet uptime and data-driven dispatch boosting effective megawatt output by ~2–4% (2024 industry benchmarks), creating a durable bidding moat in growth markets. Doing more with the same MW wins bids and extensions. Steady investment in talent and tech compounds payoff across the fleet.

- Uptime >99.5% (2024)

- +2–4% effective MW output

- Higher revenue/MW, more contract wins

- Requires sustained talent & tech investment

Selective M&A of Bolt-On Renewables

Capstone’s repeatable playbook targets mid-market renewables (5–50 MW), enabling rapid scale in high-growth corridors; share gains come from disciplined bids rather than trophy deals. Integration costs are real (commonly ~5–10% of deal capex), but operating synergies and tax attributes typically offset that burn, and steady acquisition cadence makes the platform self-funding.

- Tag: repeatable playbook

- Tag: mid-market 5–50 MW

- Tag: disciplined bids not trophies

- Tag: integration ~5–10% capex

- Tag: self-funding cadence

Repowered wind & brownfield solar scale in 2024 — +35% procurements, uptime >99.5%

High-share contracted wind and brownfield solar in 2024 growth provinces (provincial procurements +35% YoY) consume repower/grid capex but lift generation and margins; uptime >99.5% and +2–4% effective MW output (2024) compound wins. Long PPAs (10–25y) capture scarcity pricing as demand rose ~2% (2023). Repeatable mid-market play (5–50 MW) scales; integration ~5–10% capex.

| Tag | Metric |

|---|---|

| Share | High |

| Growth | +35% procurements (2024) |

| Uptime | >99.5% (2024) |

| MW impact | +2–4% (2024) |

| Integration | ~5–10% capex |

What is included in the product

Comprehensive BCG review of Capstone Infrastructure, mapping units to Stars, Cash Cows, Question Marks and Dogs with clear strategic actions.

One-page Capstone Infrastructure BCG Matrix pinpoints underperformers and winners, simplifying strategic decisions for founders and CFOs.

Cash Cows

Legacy Solar under FIT/Contracted Regimes

Legacy solar under FIT/contracted regimes delivers steady, low-volatility cash from long-term tenors (typically 15–25 years) and PV capacity factors ~20–25%, requiring minimal promotional spend and negligible growth capex; as of 2024 these assets routinely support DSCR targets of ~1.2–1.5, making them ideal to service debt, pay dividends and fund higher-growth bets—maintain, optimize, and quietly milk.

Run-of-River Hydro with Stable Hydrology

Proven run-of-river assets deliver predictable output with industry 2024 capacity factors around 40–60% and availability exceeding 95%, producing steady cash flows and low variable costs (O&M commonly in the $10–20/MWh range). Little promotion is needed—focus on reliability to sustain high utilization; incremental capex (turbine upgrades, control systems) can raise efficiency by several percentage points and extend life by 10–20 years. Classic cash-cow dynamics: net operating cash inflows typically exceed maintenance and financing outflows, supporting dividend-like distributions or reinvestment.

Regulated or Quasi-Regulated Utility Stakes

Regulated or quasi-regulated utility stakes deliver rate-based returns in mature markets with low growth (typically 0–2% volumetric demand), providing predictable revenue streams. Once capex cycles normalize these assets can convert well over 70% of EBITDA to free cash flow, ideal for funding development pipelines and corporate overhead. Maintain tight compliance and lean operations to protect cash generation and credit metrics.

Contracted Natural Gas CHP with Residual Term

Contracted natural gas CHP with residual term remains cash generative in 2024, delivering stable free cash flow despite muted volume growth; predictable opex and comprehensive fuel hedges implemented in 2024 enhance revenue visibility. Surplus cash is earmarked to finance renewables and battery storage rollouts, while management prepares orderly end-of-term strategies to preserve asset value.

- Still contracted — steady cash flow (2024)

- Opex known; 2024 fuel hedges improve predictability

- Surplus funds to bankroll renewables & storage

- Plan end-of-term strategies to preserve value

Long-Tenor O&M/Asset Management Contracts

Long-tenor O&M and asset management contracts deliver service revenues tied to operating assets across Capstone's portfolio, providing high-margin, low-growth and sticky cash flows that support the corporate engine without large capital calls; in 2024 these contracts continued to quietly compound while higher-growth assets attract active investment.

- Service revenues tied to operating assets

- High-margin, low-growth, sticky

- Supports corporate cashflow with minimal capex

- Quiet compounding in 2024 while stars run hard

Low-volatility renewables + regulated assets deliver reliable cash & strong FCF (2024)

Legacy FIT solar, run-of-river hydro, regulated utility stakes, contracted CHP and long-tenor O&M contracts form Capstone's cash cows, delivering low-volatility, high-conversion cash (2024) to fund growth. Typical 2024 DSCR/FCF conversion ranges: solar 1.2–1.5, hydro 60–80% EBITDA→FCF, utilities >70%, CHP stable via hedges. Prioritize reliability, selective life-extension capex, and dividend-style distributions.

| Asset | CF profile 2024 | Cap fac | DSCR/FCF conv |

|---|---|---|---|

| FIT solar | Steady contracted cash | 20–25% | DSCR 1.2–1.5 |

| Run-of-river | Predictable output | 40–60% | 60–80% |

| Regulated utilities | Rate-based | n/a | >70% |

| CHP | Contracted, hedged | n/a | Stable |

| O&M contracts | Sticky service rev | n/a | High-margin |

What You’re Viewing Is Included

Capstone Infrastructure BCG Matrix

The Capstone Infrastructure BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholders—just the full, professionally formatted strategic report. It's ready to edit, print, or present to stakeholders immediately. Buy once and get the complete, analysis-ready document straight to your inbox.