Carahsoft PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our focused PESTLE Analysis of Carahsoft—three to five actionable insights on political, economic, and technological pressures that matter now. Ideal for investors and strategists, it saves hours of research and informs smarter decisions. Purchase the full, editable report for the complete deep-dive and immediate use.

Political factors

Federal budget cycles

Annual appropriations and frequent continuing resolutions (multiple CRs in 2023–24) directly shift demand timing and cash flows, with federal discretionary spending around $1.7 trillion in FY2024. Agencies typically obligate roughly 30–40% of IT buys in Q4, so Carahsoft must align pipeline and marketing to those spikes. Election outcomes (Nov 2024) can reset priorities across cybersecurity, cloud, and AI. Robust scenario planning mitigates policy whiplash.

Contract vehicle primacy

GSA, SEWP, CIO-SP, NASPO and OMNIA drive access to the federal IT spend market, with total federal IT budgets near $100B in FY2024, making vehicle primacy critical. Maintaining breadth and compliance across these vehicles protects market share and accelerates procurement. Shifts to best-in-class or category management can rapidly redirect traffic. Proactive expansion into new vehicles limits exposure and revenue volatility.

National security focus

Bipartisan support for cyber defense, embodied in OMB memo M-22-09 on Zero Trust, sustains federal investments and procurement priorities tied to supply-chain security.

Geopolitical tensions since 2022 have driven greater demand for secure cloud, analytics, and incident response as agencies and DoD (FY2025 budget request ~$842B) prioritize resilience.

Carahsoft’s aggregator role concentrates mission-ready vendors; messaging should map directly to DoD and civilian strategic priorities and procurement timelines.

Industrial policy shifts

Industrial policy shifts—Buy American, TAA compliance, and CHIPS-era incentives (CHIPS Act authorized roughly 52 billion USD for semiconductor incentives)—are tightening product eligibility and affecting pricing for federal IT buys. Domestic sourcing rules force vendors to reconfigure portfolios; Carahsoft must curate compliant SKUs and steer vendors through certifications to retain bids. Ongoing policy monitoring reduces award risk and post-award deobligations.

- Buy American/TAA: impacts eligibility

- CHIPS: 52 billion USD incentives

- SKU curation: compliance-first

- Vendor certification: advisory role

- Monitoring: lowers award risk

State and local dynamics

Governors’ agendas, bond measures and $75B in federal pass-through COVID/ARPA and broadband funds continue to drive SLED IT spend, with U.S. state and local IT budgets estimated at about $132B in 2024 and forecast growth near 3% in 2025; education and health grants (over $40B combined in recent cycles) create windows for rapid rollout that Carahsoft can target by aligning offers to regional priorities and timing.

- Target: align to governors’ priorities and bond timelines

- Funding: leverage $75B federal pass-through and $40B+ education/health grants

- Scale: use cooperative purchasing to reach multiple jurisdictions

Federal funding shifts, industrial policy, and SLED dollars reshape IT procurement timing

Political drivers—annual appropriations/CRs (federal discretionary ~1.7T FY2024) and election shifts—create timing and priority risk for Carahsoft; federal IT ~100B (FY2024) and DoD request ~842B (FY2025) shape demand. Industrial policy (Buy American, TAA, CHIPS 52B) and SLED funds (state/local IT ~132B; 75B ARPA pass-through) constrain eligibility and create targeted opportunities.

| Item | 2024/25 Value |

|---|---|

| Federal discretionary | ~1.7T |

| Federal IT | ~100B |

| DoD request | ~842B |

| CHIPS | 52B |

| State/local IT | ~132B |

| ARPA pass-through | 75B |

What is included in the product

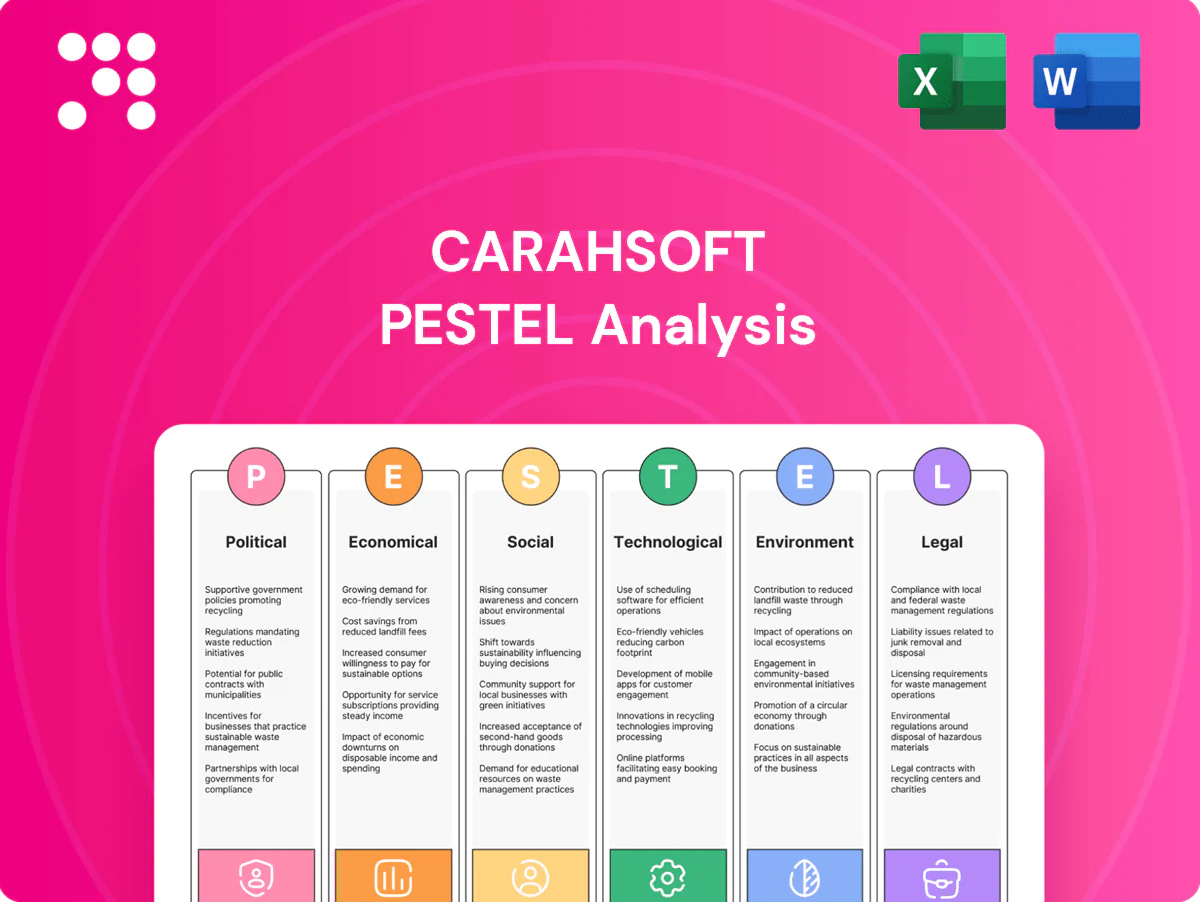

Explores how external macro-environmental factors uniquely affect Carahsoft across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by relevant data and current trends. Designed for executives, consultants, and entrepreneurs, the analysis offers forward-looking insights, scenario planning support, and clean formatting ready for business plans or investor materials.

Carahsoft's PESTLE analysis delivers a clean, visually segmented summary that’s easily dropped into presentations or shared across teams, while allowing quick note-taking and regional customization to streamline risk discussions and planning sessions.

Economic factors

Public spend resilience

Government IT outlays are relatively countercyclical, helping stabilize Carahsoft revenue as federal IT spending remained elevated into 2024–25 (federal civilian IT budgets reported above $80 billion range), but inflationary pressure and agency hiring freezes have deferred some multi-year projects. Episodic stimulus and dedicated cybersecurity appropriations (notably increased since 2021) create sharp bursts of demand. Carahsoft should balance multi-year, long-cycle program wins with capacity for quick-turn buys to capture surge funding.

Rate and cost pressures

Rising US policy rates (June 2025 federal funds target 5.25–5.50%) lift vendor financing costs and elevate discount expectations, adding roughly 100–200 bps to borrowing costs for suppliers. Agencies push TCO savings by shifting to SaaS and managed services; Carahsoft can win by packaging cost‑optimized bundles and multi‑year agreements. Flexible, efficient payment terms improve partner competitiveness in procurement.

Supply chain variability

Hardware lead times that peaked at 20–28 weeks during 2021–22 eased to roughly 12–16 weeks by 2024, yet semiconductor constraints—despite ~10% capacity growth in 2024—plus episodic logistics shocks (container rates volatility from ~$10,000/FEU peak to ~$2,000 in 2024) continue to threaten SLAs; transparent ETA management preserves CPARS scores and repeat awards, while shifting to software/cloud, alternative suppliers, and 4–8 weeks buffer inventory on high-velocity SKUs reduces disruption.

Vendor ecosystem scale

Carahsoft represents over 1,300 vendor partners, and a large catalog fuels price competition and solution breadth; aggregated demand across the US federal IT market (exceeding $90B in 2024) supports tiered pricing and volume discounts. The firm leverages vendor rebates and MDF to lower total cost of ownership, while data-driven cross-sell lifts per-award value.

- 1,300+ vendor partners

- US federal IT market >90B (2024)

- Rebates/MDF + data cross-sell = higher per-award revenue

SLED budget health

State tax receipts and roughly $190 billion in federal ESSER aid through 2023 continue to shape education and local IT refresh cycles, with variable 2024–25 state revenue trends tightening capital budgets. Tight SLED budgets push procurement toward cybersecurity, identity, and modernization projects with demonstrable ROI. Carahsoft can position offerings around efficiency gains and quantifiable risk reduction, while cooperative contracts speed obligating funds.

- Tag: federal-aid ESSER ~$190B

- Tag: priority Cybersecurity, Identity, Modernization

- Tag: ROI-driven procurement

- Tag: cooperative-contracts accelerate obligations

Federal funding shifts, industrial policy, and SLED dollars reshape IT procurement timing

Federal IT spending >$90B (2024) and 1,300+ vendor partners stabilize Carahsoft revenue but drive price competition; federal funds target 5.25–5.50% (June 2025) increases vendor financing costs. Semiconductor relief cut lead times to ~12–16 weeks (2024) but logistics volatility persists; ESSER ~$190B shapes SLED demand toward ROI-focused cybersecurity and modernization.

| Metric | Value |

|---|---|

| Federal IT market | >$90B (2024) |

| Vendor partners | 1,300+ |

| Fed funds target | 5.25–5.50% (Jun 2025) |

| ESSER | ~$190B |

| Lead times | 12–16 wks (2024) |

Preview Before You Purchase

Carahsoft PESTLE Analysis

The Carahsoft PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this preview are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file you’ll own upon checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our focused PESTLE Analysis of Carahsoft—three to five actionable insights on political, economic, and technological pressures that matter now. Ideal for investors and strategists, it saves hours of research and informs smarter decisions. Purchase the full, editable report for the complete deep-dive and immediate use.

Political factors

Federal budget cycles

Annual appropriations and frequent continuing resolutions (multiple CRs in 2023–24) directly shift demand timing and cash flows, with federal discretionary spending around $1.7 trillion in FY2024. Agencies typically obligate roughly 30–40% of IT buys in Q4, so Carahsoft must align pipeline and marketing to those spikes. Election outcomes (Nov 2024) can reset priorities across cybersecurity, cloud, and AI. Robust scenario planning mitigates policy whiplash.

Contract vehicle primacy

GSA, SEWP, CIO-SP, NASPO and OMNIA drive access to the federal IT spend market, with total federal IT budgets near $100B in FY2024, making vehicle primacy critical. Maintaining breadth and compliance across these vehicles protects market share and accelerates procurement. Shifts to best-in-class or category management can rapidly redirect traffic. Proactive expansion into new vehicles limits exposure and revenue volatility.

National security focus

Bipartisan support for cyber defense, embodied in OMB memo M-22-09 on Zero Trust, sustains federal investments and procurement priorities tied to supply-chain security.

Geopolitical tensions since 2022 have driven greater demand for secure cloud, analytics, and incident response as agencies and DoD (FY2025 budget request ~$842B) prioritize resilience.

Carahsoft’s aggregator role concentrates mission-ready vendors; messaging should map directly to DoD and civilian strategic priorities and procurement timelines.

Industrial policy shifts

Industrial policy shifts—Buy American, TAA compliance, and CHIPS-era incentives (CHIPS Act authorized roughly 52 billion USD for semiconductor incentives)—are tightening product eligibility and affecting pricing for federal IT buys. Domestic sourcing rules force vendors to reconfigure portfolios; Carahsoft must curate compliant SKUs and steer vendors through certifications to retain bids. Ongoing policy monitoring reduces award risk and post-award deobligations.

- Buy American/TAA: impacts eligibility

- CHIPS: 52 billion USD incentives

- SKU curation: compliance-first

- Vendor certification: advisory role

- Monitoring: lowers award risk

State and local dynamics

Governors’ agendas, bond measures and $75B in federal pass-through COVID/ARPA and broadband funds continue to drive SLED IT spend, with U.S. state and local IT budgets estimated at about $132B in 2024 and forecast growth near 3% in 2025; education and health grants (over $40B combined in recent cycles) create windows for rapid rollout that Carahsoft can target by aligning offers to regional priorities and timing.

- Target: align to governors’ priorities and bond timelines

- Funding: leverage $75B federal pass-through and $40B+ education/health grants

- Scale: use cooperative purchasing to reach multiple jurisdictions

Federal funding shifts, industrial policy, and SLED dollars reshape IT procurement timing

Political drivers—annual appropriations/CRs (federal discretionary ~1.7T FY2024) and election shifts—create timing and priority risk for Carahsoft; federal IT ~100B (FY2024) and DoD request ~842B (FY2025) shape demand. Industrial policy (Buy American, TAA, CHIPS 52B) and SLED funds (state/local IT ~132B; 75B ARPA pass-through) constrain eligibility and create targeted opportunities.

| Item | 2024/25 Value |

|---|---|

| Federal discretionary | ~1.7T |

| Federal IT | ~100B |

| DoD request | ~842B |

| CHIPS | 52B |

| State/local IT | ~132B |

| ARPA pass-through | 75B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Carahsoft across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by relevant data and current trends. Designed for executives, consultants, and entrepreneurs, the analysis offers forward-looking insights, scenario planning support, and clean formatting ready for business plans or investor materials.

Carahsoft's PESTLE analysis delivers a clean, visually segmented summary that’s easily dropped into presentations or shared across teams, while allowing quick note-taking and regional customization to streamline risk discussions and planning sessions.

Economic factors

Public spend resilience

Government IT outlays are relatively countercyclical, helping stabilize Carahsoft revenue as federal IT spending remained elevated into 2024–25 (federal civilian IT budgets reported above $80 billion range), but inflationary pressure and agency hiring freezes have deferred some multi-year projects. Episodic stimulus and dedicated cybersecurity appropriations (notably increased since 2021) create sharp bursts of demand. Carahsoft should balance multi-year, long-cycle program wins with capacity for quick-turn buys to capture surge funding.

Rate and cost pressures

Rising US policy rates (June 2025 federal funds target 5.25–5.50%) lift vendor financing costs and elevate discount expectations, adding roughly 100–200 bps to borrowing costs for suppliers. Agencies push TCO savings by shifting to SaaS and managed services; Carahsoft can win by packaging cost‑optimized bundles and multi‑year agreements. Flexible, efficient payment terms improve partner competitiveness in procurement.

Supply chain variability

Hardware lead times that peaked at 20–28 weeks during 2021–22 eased to roughly 12–16 weeks by 2024, yet semiconductor constraints—despite ~10% capacity growth in 2024—plus episodic logistics shocks (container rates volatility from ~$10,000/FEU peak to ~$2,000 in 2024) continue to threaten SLAs; transparent ETA management preserves CPARS scores and repeat awards, while shifting to software/cloud, alternative suppliers, and 4–8 weeks buffer inventory on high-velocity SKUs reduces disruption.

Vendor ecosystem scale

Carahsoft represents over 1,300 vendor partners, and a large catalog fuels price competition and solution breadth; aggregated demand across the US federal IT market (exceeding $90B in 2024) supports tiered pricing and volume discounts. The firm leverages vendor rebates and MDF to lower total cost of ownership, while data-driven cross-sell lifts per-award value.

- 1,300+ vendor partners

- US federal IT market >90B (2024)

- Rebates/MDF + data cross-sell = higher per-award revenue

SLED budget health

State tax receipts and roughly $190 billion in federal ESSER aid through 2023 continue to shape education and local IT refresh cycles, with variable 2024–25 state revenue trends tightening capital budgets. Tight SLED budgets push procurement toward cybersecurity, identity, and modernization projects with demonstrable ROI. Carahsoft can position offerings around efficiency gains and quantifiable risk reduction, while cooperative contracts speed obligating funds.

- Tag: federal-aid ESSER ~$190B

- Tag: priority Cybersecurity, Identity, Modernization

- Tag: ROI-driven procurement

- Tag: cooperative-contracts accelerate obligations

Federal funding shifts, industrial policy, and SLED dollars reshape IT procurement timing

Federal IT spending >$90B (2024) and 1,300+ vendor partners stabilize Carahsoft revenue but drive price competition; federal funds target 5.25–5.50% (June 2025) increases vendor financing costs. Semiconductor relief cut lead times to ~12–16 weeks (2024) but logistics volatility persists; ESSER ~$190B shapes SLED demand toward ROI-focused cybersecurity and modernization.

| Metric | Value |

|---|---|

| Federal IT market | >$90B (2024) |

| Vendor partners | 1,300+ |

| Fed funds target | 5.25–5.50% (Jun 2025) |

| ESSER | ~$190B |

| Lead times | 12–16 wks (2024) |

Preview Before You Purchase

Carahsoft PESTLE Analysis

The Carahsoft PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this preview are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file you’ll own upon checkout.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our focused PESTLE Analysis of Carahsoft—three to five actionable insights on political, economic, and technological pressures that matter now. Ideal for investors and strategists, it saves hours of research and informs smarter decisions. Purchase the full, editable report for the complete deep-dive and immediate use.

Political factors

Federal budget cycles

Annual appropriations and frequent continuing resolutions (multiple CRs in 2023–24) directly shift demand timing and cash flows, with federal discretionary spending around $1.7 trillion in FY2024. Agencies typically obligate roughly 30–40% of IT buys in Q4, so Carahsoft must align pipeline and marketing to those spikes. Election outcomes (Nov 2024) can reset priorities across cybersecurity, cloud, and AI. Robust scenario planning mitigates policy whiplash.

Contract vehicle primacy

GSA, SEWP, CIO-SP, NASPO and OMNIA drive access to the federal IT spend market, with total federal IT budgets near $100B in FY2024, making vehicle primacy critical. Maintaining breadth and compliance across these vehicles protects market share and accelerates procurement. Shifts to best-in-class or category management can rapidly redirect traffic. Proactive expansion into new vehicles limits exposure and revenue volatility.

National security focus

Bipartisan support for cyber defense, embodied in OMB memo M-22-09 on Zero Trust, sustains federal investments and procurement priorities tied to supply-chain security.

Geopolitical tensions since 2022 have driven greater demand for secure cloud, analytics, and incident response as agencies and DoD (FY2025 budget request ~$842B) prioritize resilience.

Carahsoft’s aggregator role concentrates mission-ready vendors; messaging should map directly to DoD and civilian strategic priorities and procurement timelines.

Industrial policy shifts

Industrial policy shifts—Buy American, TAA compliance, and CHIPS-era incentives (CHIPS Act authorized roughly 52 billion USD for semiconductor incentives)—are tightening product eligibility and affecting pricing for federal IT buys. Domestic sourcing rules force vendors to reconfigure portfolios; Carahsoft must curate compliant SKUs and steer vendors through certifications to retain bids. Ongoing policy monitoring reduces award risk and post-award deobligations.

- Buy American/TAA: impacts eligibility

- CHIPS: 52 billion USD incentives

- SKU curation: compliance-first

- Vendor certification: advisory role

- Monitoring: lowers award risk

State and local dynamics

Governors’ agendas, bond measures and $75B in federal pass-through COVID/ARPA and broadband funds continue to drive SLED IT spend, with U.S. state and local IT budgets estimated at about $132B in 2024 and forecast growth near 3% in 2025; education and health grants (over $40B combined in recent cycles) create windows for rapid rollout that Carahsoft can target by aligning offers to regional priorities and timing.

- Target: align to governors’ priorities and bond timelines

- Funding: leverage $75B federal pass-through and $40B+ education/health grants

- Scale: use cooperative purchasing to reach multiple jurisdictions

Federal funding shifts, industrial policy, and SLED dollars reshape IT procurement timing

Political drivers—annual appropriations/CRs (federal discretionary ~1.7T FY2024) and election shifts—create timing and priority risk for Carahsoft; federal IT ~100B (FY2024) and DoD request ~842B (FY2025) shape demand. Industrial policy (Buy American, TAA, CHIPS 52B) and SLED funds (state/local IT ~132B; 75B ARPA pass-through) constrain eligibility and create targeted opportunities.

| Item | 2024/25 Value |

|---|---|

| Federal discretionary | ~1.7T |

| Federal IT | ~100B |

| DoD request | ~842B |

| CHIPS | 52B |

| State/local IT | ~132B |

| ARPA pass-through | 75B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Carahsoft across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by relevant data and current trends. Designed for executives, consultants, and entrepreneurs, the analysis offers forward-looking insights, scenario planning support, and clean formatting ready for business plans or investor materials.

Carahsoft's PESTLE analysis delivers a clean, visually segmented summary that’s easily dropped into presentations or shared across teams, while allowing quick note-taking and regional customization to streamline risk discussions and planning sessions.

Economic factors

Public spend resilience

Government IT outlays are relatively countercyclical, helping stabilize Carahsoft revenue as federal IT spending remained elevated into 2024–25 (federal civilian IT budgets reported above $80 billion range), but inflationary pressure and agency hiring freezes have deferred some multi-year projects. Episodic stimulus and dedicated cybersecurity appropriations (notably increased since 2021) create sharp bursts of demand. Carahsoft should balance multi-year, long-cycle program wins with capacity for quick-turn buys to capture surge funding.

Rate and cost pressures

Rising US policy rates (June 2025 federal funds target 5.25–5.50%) lift vendor financing costs and elevate discount expectations, adding roughly 100–200 bps to borrowing costs for suppliers. Agencies push TCO savings by shifting to SaaS and managed services; Carahsoft can win by packaging cost‑optimized bundles and multi‑year agreements. Flexible, efficient payment terms improve partner competitiveness in procurement.

Supply chain variability

Hardware lead times that peaked at 20–28 weeks during 2021–22 eased to roughly 12–16 weeks by 2024, yet semiconductor constraints—despite ~10% capacity growth in 2024—plus episodic logistics shocks (container rates volatility from ~$10,000/FEU peak to ~$2,000 in 2024) continue to threaten SLAs; transparent ETA management preserves CPARS scores and repeat awards, while shifting to software/cloud, alternative suppliers, and 4–8 weeks buffer inventory on high-velocity SKUs reduces disruption.

Vendor ecosystem scale

Carahsoft represents over 1,300 vendor partners, and a large catalog fuels price competition and solution breadth; aggregated demand across the US federal IT market (exceeding $90B in 2024) supports tiered pricing and volume discounts. The firm leverages vendor rebates and MDF to lower total cost of ownership, while data-driven cross-sell lifts per-award value.

- 1,300+ vendor partners

- US federal IT market >90B (2024)

- Rebates/MDF + data cross-sell = higher per-award revenue

SLED budget health

State tax receipts and roughly $190 billion in federal ESSER aid through 2023 continue to shape education and local IT refresh cycles, with variable 2024–25 state revenue trends tightening capital budgets. Tight SLED budgets push procurement toward cybersecurity, identity, and modernization projects with demonstrable ROI. Carahsoft can position offerings around efficiency gains and quantifiable risk reduction, while cooperative contracts speed obligating funds.

- Tag: federal-aid ESSER ~$190B

- Tag: priority Cybersecurity, Identity, Modernization

- Tag: ROI-driven procurement

- Tag: cooperative-contracts accelerate obligations

Federal funding shifts, industrial policy, and SLED dollars reshape IT procurement timing

Federal IT spending >$90B (2024) and 1,300+ vendor partners stabilize Carahsoft revenue but drive price competition; federal funds target 5.25–5.50% (June 2025) increases vendor financing costs. Semiconductor relief cut lead times to ~12–16 weeks (2024) but logistics volatility persists; ESSER ~$190B shapes SLED demand toward ROI-focused cybersecurity and modernization.

| Metric | Value |

|---|---|

| Federal IT market | >$90B (2024) |

| Vendor partners | 1,300+ |

| Fed funds target | 5.25–5.50% (Jun 2025) |

| ESSER | ~$190B |

| Lead times | 12–16 wks (2024) |

Preview Before You Purchase

Carahsoft PESTLE Analysis

The Carahsoft PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this preview are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file you’ll own upon checkout.