Cardinal Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

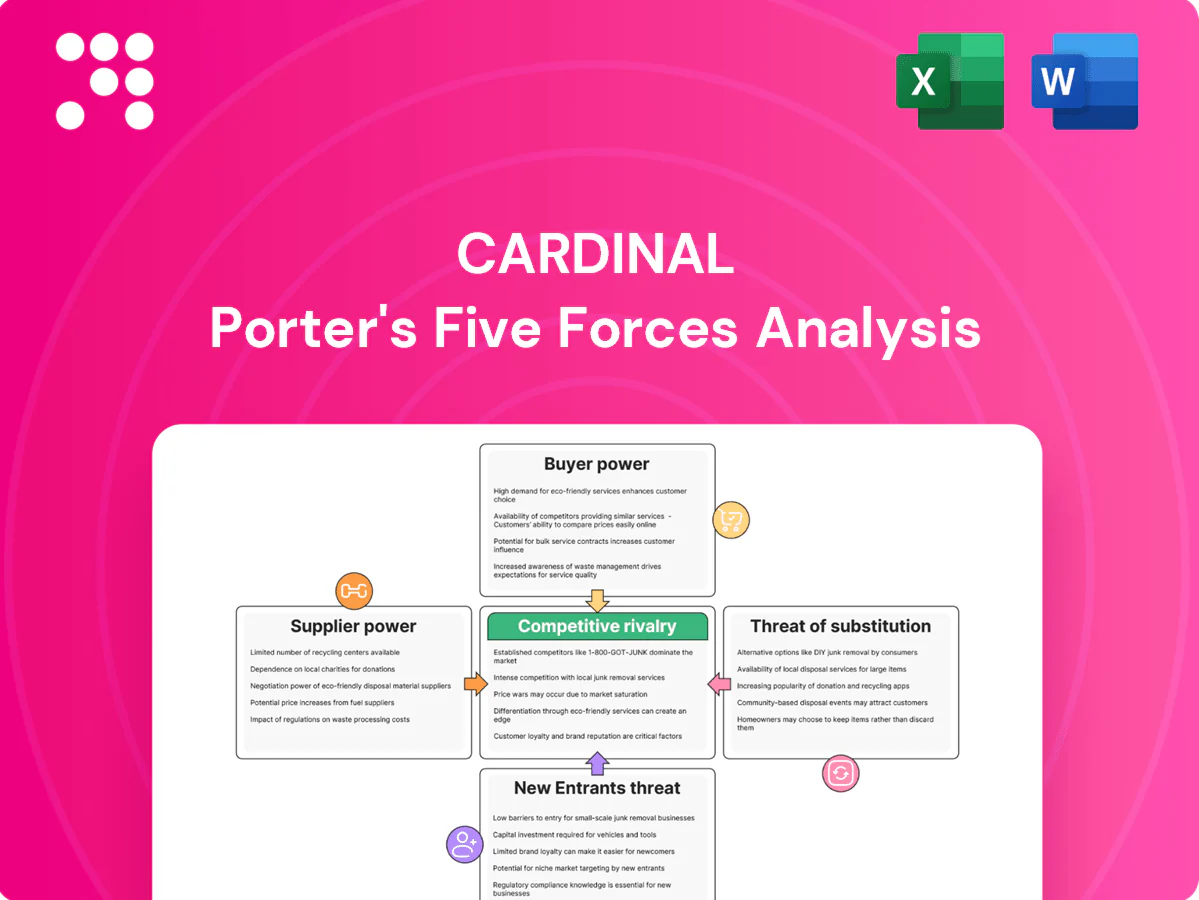

Cardinal’s Porter's Five Forces snapshot highlights supplier and buyer power, threat of entrants and substitutes, and competitive rivalry to frame strategic risks and opportunities. This brief overview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cardinal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated oilfield services

Drilling, completion and workover services in Western Canada are concentrated among a handful of mid-to-large firms, and in 2024 those suppliers exerted notable pricing power as activity upcycles lifted service dayrates and tightened capacity.

Cardinal’s multi-sourcing reduces exposure, but limited available rigs and crews shifted leverage to suppliers during peak 2024 activity; long-term contracts and scheduling priority helped moderate acute spikes.

Cyclicality tied to commodity prices means supplier power rose in 2024 and can fall quickly if oil and gas pricing weakens.

Pipeline and midstream dependence

Access to gathering, processing and egress is concentrated among a few midstream players, with take-or-pay or firm service contracts typically covering up to 100% of contracted volumes, giving operators tariff and contract leverage.

Takeaway constraints in 2023–24 widened differentials into double-digit dollars per barrel, indirectly strengthening midstream bargaining power by raising shippers’ costs for alternative routes.

Firm contracts reduce volume risk for operators but lock shippers into fees; once committed capacity is scarce, renegotiation options are materially limited.

Skilled labor tightness

Field crews, engineers and HSE specialists see acute scarcity at peak activity, driving wage uplifts of 15–30% and constrained availability in 2024; remote Alberta/Saskatchewan sites amplify recruitment and retention costs through travel and accommodation premiums. Automation reduces headcount but cannot replace safety-critical roles, and limited unionization does not prevent market-driven supplier-like power.

Specialized equipment and tech

Standardization efforts and cloud-based analytics are reducing dependence gradually, while OEM lead times and parts scarcity during recent supply-chain shocks have given suppliers elevated leverage.

Energy, water, and compliance inputs

Energy, water and emissions-compliance suppliers exert meaningful bargaining power as energy rates (~CAD 0.08/kWh for industrial users in 2024), water sourcing/disposal capacity is regionally constrained (notably Prairies/Alberta) and carbon pricing trajectories (federal plan to CAD 170/tCO2e by 2030) lift compliance-linked supplier fees; multi-year contracts and recycling cut but do not eliminate input sensitivity.

- Energy: ~CAD 0.08/kWh (2024)

- Carbon: CAD 170/t target by 2030

- Water: regional disposal capacity tight

- Mitigation: long-term contracts + recycling reduce volatility

Supplier squeeze: higher wages, energy costs and carbon charges tighten margins

Supplier power was elevated in 2024 as concentrated drilling, midstream and niche OEMs tightened capacity, raising costs and switching barriers.

Field labour shortages drove wage uplifts of 15–30% and remote site premiums; take-or-pay midstream contracts and double‑digit USD/bbl differentials amplified leverage.

Energy (~CAD 0.08/kWh) and carbon policy (CAD 170/tCO2e by 2030) add sustained input pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Energy | ~CAD 0.08/kWh | ↑ operating costs |

| Wage uplift | 15–30% | labour cost pressure |

| Carbon | CAD 170/t target by 2030 | ↑ compliance fees |

What is included in the product

Tailored Porter's Five Forces analysis for Cardinal that uncovers competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive threats and strategic protections to inform pricing, positioning, and growth decisions.

A single, editable one-sheet that quantifies and visualizes Porter’s Five Forces—instantly revealing strategic pain points with a clear radar chart so teams can prioritize fixes and update pressure levels as market conditions change.

Customers Bargaining Power

Commodity price-takers

Cardinal is a commodity price-taker as sales are tied to benchmarks WTI/WCS/AECO, with 2024 WTI averaging roughly $80/bbl, constraining pricing discretion. Buyers can switch producers at low cost when specs match, making differentials and transportation often more decisive than brand. Pipeline and rail options plus WCS differentials (wide in 2024) drive netbacks. Producers hedge to lock realized prices, but hedging does not increase buyer bargaining power.

Concentrated refiners and marketers

A limited set of refiners, traders and midstream marketers purchase large volumes—US petroleum consumption averaged about 20.5 mbpd in 2024—concentrating demand and enabling tougher terms on quality, delivery and penalties. Cardinal’s diversified product slate broadens outlet options across fuels, petrochemicals and feedstocks, while forward sales and multi-year term contracts partly blunt counterparty leverage and stabilize margins.

Quality and specification sensitivity

Light/medium versus heavy crude narrows the buyer pool and in 2024 Western Canadian Select traded at roughly a US$25/bbl discount to WTI, illustrating material price haircuts for heavy grades; failure to meet specs risks further discounts or rejection. Investments in blending and treating lift API and lower sulfur, improving marketability and realized price. Upgrading gas processing to meet AECO benchmarks (AECO ~CAD2.10/GJ in 2024) cuts buyers’ bargaining edge.

Logistics optionality

Access to multiple hubs, pipelines and rail (2024: 3+ accessible hubs in major basins) broadens buyer sets and typically narrows differentials, while constrained takeaway drives location discounts and buyer leverage. On-site and regional storage gives timing flexibility to avoid distressed sales, and marketing partnerships in 2024 unlocked incremental demand channels for spot and term volumes.

- Hubs: 3+ (2024)

- Takeaway discounts: ↑ buyer leverage

- Storage: avoids distressed exits

- Marketing deals: unlock demand

ESG and certification demands

Buyers increasingly demand emissions data and ESG assurances, raising negotiation levers; CDP reported 18,700 company disclosures in 2023 and EU CSRD expands mandatory reporting to ~50,000 firms from 2024. Certified responsible production can secure price premiums or access to select buyers, while non-compliance risks exclusion or contract discounts. Transparent reporting and methane-reduction measures (Global Methane Pledge: 150+ countries) strengthen seller leverage.

- ESG disclosures: CDP 2023: 18,700 companies

- Regulation: CSRD ~50,000 firms from 2024

- Methane focus: 150+ countries pledge

- Impact: certification = premiums/access; non-compliance = discounts/exclusion

Energy producer price-taker vs WTI/WCS/AECO; hubs, storage and ESG shift buyer dynamics

Cardinal is a price-taker tied to WTI/WCS/AECO (WTI ~US$80/bbl, WCS ~US$25/bbl discount in 2024), limiting pricing power. Large refiners/traders (~US consumption 20.5 mbpd in 2024) concentrate buying power, but diversified slate, term contracts and storage mitigate leverage. Infrastructure (3+ hubs) and takeaway constraints drive differentials; ESG/ESR reporting (CDP 18,700 in 2023; CSRD ~50,000) adds new buyer levers.

| Metric | 2024 Value |

|---|---|

| WTI | ~US$80/bbl |

| WCS discount | ~US$25/bbl |

| US demand | 20.5 mbpd |

| AECO | ~CAD2.10/GJ |

| Hubs accessible | 3+ |

| CDP disclosures | 18,700 (2023) |

Preview the Actual Deliverable

Cardinal Porter's Five Forces Analysis

This Cardinal Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It contains the complete industry evaluation, competitive insights, and strategic implications ready for download and use. What you see is precisely what you get.

Go Beyond the Preview—Access the Full Strategic Report

Cardinal’s Porter's Five Forces snapshot highlights supplier and buyer power, threat of entrants and substitutes, and competitive rivalry to frame strategic risks and opportunities. This brief overview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cardinal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated oilfield services

Drilling, completion and workover services in Western Canada are concentrated among a handful of mid-to-large firms, and in 2024 those suppliers exerted notable pricing power as activity upcycles lifted service dayrates and tightened capacity.

Cardinal’s multi-sourcing reduces exposure, but limited available rigs and crews shifted leverage to suppliers during peak 2024 activity; long-term contracts and scheduling priority helped moderate acute spikes.

Cyclicality tied to commodity prices means supplier power rose in 2024 and can fall quickly if oil and gas pricing weakens.

Pipeline and midstream dependence

Access to gathering, processing and egress is concentrated among a few midstream players, with take-or-pay or firm service contracts typically covering up to 100% of contracted volumes, giving operators tariff and contract leverage.

Takeaway constraints in 2023–24 widened differentials into double-digit dollars per barrel, indirectly strengthening midstream bargaining power by raising shippers’ costs for alternative routes.

Firm contracts reduce volume risk for operators but lock shippers into fees; once committed capacity is scarce, renegotiation options are materially limited.

Skilled labor tightness

Field crews, engineers and HSE specialists see acute scarcity at peak activity, driving wage uplifts of 15–30% and constrained availability in 2024; remote Alberta/Saskatchewan sites amplify recruitment and retention costs through travel and accommodation premiums. Automation reduces headcount but cannot replace safety-critical roles, and limited unionization does not prevent market-driven supplier-like power.

Specialized equipment and tech

Standardization efforts and cloud-based analytics are reducing dependence gradually, while OEM lead times and parts scarcity during recent supply-chain shocks have given suppliers elevated leverage.

Energy, water, and compliance inputs

Energy, water and emissions-compliance suppliers exert meaningful bargaining power as energy rates (~CAD 0.08/kWh for industrial users in 2024), water sourcing/disposal capacity is regionally constrained (notably Prairies/Alberta) and carbon pricing trajectories (federal plan to CAD 170/tCO2e by 2030) lift compliance-linked supplier fees; multi-year contracts and recycling cut but do not eliminate input sensitivity.

- Energy: ~CAD 0.08/kWh (2024)

- Carbon: CAD 170/t target by 2030

- Water: regional disposal capacity tight

- Mitigation: long-term contracts + recycling reduce volatility

Supplier squeeze: higher wages, energy costs and carbon charges tighten margins

Supplier power was elevated in 2024 as concentrated drilling, midstream and niche OEMs tightened capacity, raising costs and switching barriers.

Field labour shortages drove wage uplifts of 15–30% and remote site premiums; take-or-pay midstream contracts and double‑digit USD/bbl differentials amplified leverage.

Energy (~CAD 0.08/kWh) and carbon policy (CAD 170/tCO2e by 2030) add sustained input pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Energy | ~CAD 0.08/kWh | ↑ operating costs |

| Wage uplift | 15–30% | labour cost pressure |

| Carbon | CAD 170/t target by 2030 | ↑ compliance fees |

What is included in the product

Tailored Porter's Five Forces analysis for Cardinal that uncovers competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive threats and strategic protections to inform pricing, positioning, and growth decisions.

A single, editable one-sheet that quantifies and visualizes Porter’s Five Forces—instantly revealing strategic pain points with a clear radar chart so teams can prioritize fixes and update pressure levels as market conditions change.

Customers Bargaining Power

Commodity price-takers

Cardinal is a commodity price-taker as sales are tied to benchmarks WTI/WCS/AECO, with 2024 WTI averaging roughly $80/bbl, constraining pricing discretion. Buyers can switch producers at low cost when specs match, making differentials and transportation often more decisive than brand. Pipeline and rail options plus WCS differentials (wide in 2024) drive netbacks. Producers hedge to lock realized prices, but hedging does not increase buyer bargaining power.

Concentrated refiners and marketers

A limited set of refiners, traders and midstream marketers purchase large volumes—US petroleum consumption averaged about 20.5 mbpd in 2024—concentrating demand and enabling tougher terms on quality, delivery and penalties. Cardinal’s diversified product slate broadens outlet options across fuels, petrochemicals and feedstocks, while forward sales and multi-year term contracts partly blunt counterparty leverage and stabilize margins.

Quality and specification sensitivity

Light/medium versus heavy crude narrows the buyer pool and in 2024 Western Canadian Select traded at roughly a US$25/bbl discount to WTI, illustrating material price haircuts for heavy grades; failure to meet specs risks further discounts or rejection. Investments in blending and treating lift API and lower sulfur, improving marketability and realized price. Upgrading gas processing to meet AECO benchmarks (AECO ~CAD2.10/GJ in 2024) cuts buyers’ bargaining edge.

Logistics optionality

Access to multiple hubs, pipelines and rail (2024: 3+ accessible hubs in major basins) broadens buyer sets and typically narrows differentials, while constrained takeaway drives location discounts and buyer leverage. On-site and regional storage gives timing flexibility to avoid distressed sales, and marketing partnerships in 2024 unlocked incremental demand channels for spot and term volumes.

- Hubs: 3+ (2024)

- Takeaway discounts: ↑ buyer leverage

- Storage: avoids distressed exits

- Marketing deals: unlock demand

ESG and certification demands

Buyers increasingly demand emissions data and ESG assurances, raising negotiation levers; CDP reported 18,700 company disclosures in 2023 and EU CSRD expands mandatory reporting to ~50,000 firms from 2024. Certified responsible production can secure price premiums or access to select buyers, while non-compliance risks exclusion or contract discounts. Transparent reporting and methane-reduction measures (Global Methane Pledge: 150+ countries) strengthen seller leverage.

- ESG disclosures: CDP 2023: 18,700 companies

- Regulation: CSRD ~50,000 firms from 2024

- Methane focus: 150+ countries pledge

- Impact: certification = premiums/access; non-compliance = discounts/exclusion

Energy producer price-taker vs WTI/WCS/AECO; hubs, storage and ESG shift buyer dynamics

Cardinal is a price-taker tied to WTI/WCS/AECO (WTI ~US$80/bbl, WCS ~US$25/bbl discount in 2024), limiting pricing power. Large refiners/traders (~US consumption 20.5 mbpd in 2024) concentrate buying power, but diversified slate, term contracts and storage mitigate leverage. Infrastructure (3+ hubs) and takeaway constraints drive differentials; ESG/ESR reporting (CDP 18,700 in 2023; CSRD ~50,000) adds new buyer levers.

| Metric | 2024 Value |

|---|---|

| WTI | ~US$80/bbl |

| WCS discount | ~US$25/bbl |

| US demand | 20.5 mbpd |

| AECO | ~CAD2.10/GJ |

| Hubs accessible | 3+ |

| CDP disclosures | 18,700 (2023) |

Preview the Actual Deliverable

Cardinal Porter's Five Forces Analysis

This Cardinal Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It contains the complete industry evaluation, competitive insights, and strategic implications ready for download and use. What you see is precisely what you get.

Description

Go Beyond the Preview—Access the Full Strategic Report

Cardinal’s Porter's Five Forces snapshot highlights supplier and buyer power, threat of entrants and substitutes, and competitive rivalry to frame strategic risks and opportunities. This brief overview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cardinal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated oilfield services

Drilling, completion and workover services in Western Canada are concentrated among a handful of mid-to-large firms, and in 2024 those suppliers exerted notable pricing power as activity upcycles lifted service dayrates and tightened capacity.

Cardinal’s multi-sourcing reduces exposure, but limited available rigs and crews shifted leverage to suppliers during peak 2024 activity; long-term contracts and scheduling priority helped moderate acute spikes.

Cyclicality tied to commodity prices means supplier power rose in 2024 and can fall quickly if oil and gas pricing weakens.

Pipeline and midstream dependence

Access to gathering, processing and egress is concentrated among a few midstream players, with take-or-pay or firm service contracts typically covering up to 100% of contracted volumes, giving operators tariff and contract leverage.

Takeaway constraints in 2023–24 widened differentials into double-digit dollars per barrel, indirectly strengthening midstream bargaining power by raising shippers’ costs for alternative routes.

Firm contracts reduce volume risk for operators but lock shippers into fees; once committed capacity is scarce, renegotiation options are materially limited.

Skilled labor tightness

Field crews, engineers and HSE specialists see acute scarcity at peak activity, driving wage uplifts of 15–30% and constrained availability in 2024; remote Alberta/Saskatchewan sites amplify recruitment and retention costs through travel and accommodation premiums. Automation reduces headcount but cannot replace safety-critical roles, and limited unionization does not prevent market-driven supplier-like power.

Specialized equipment and tech

Standardization efforts and cloud-based analytics are reducing dependence gradually, while OEM lead times and parts scarcity during recent supply-chain shocks have given suppliers elevated leverage.

Energy, water, and compliance inputs

Energy, water and emissions-compliance suppliers exert meaningful bargaining power as energy rates (~CAD 0.08/kWh for industrial users in 2024), water sourcing/disposal capacity is regionally constrained (notably Prairies/Alberta) and carbon pricing trajectories (federal plan to CAD 170/tCO2e by 2030) lift compliance-linked supplier fees; multi-year contracts and recycling cut but do not eliminate input sensitivity.

- Energy: ~CAD 0.08/kWh (2024)

- Carbon: CAD 170/t target by 2030

- Water: regional disposal capacity tight

- Mitigation: long-term contracts + recycling reduce volatility

Supplier squeeze: higher wages, energy costs and carbon charges tighten margins

Supplier power was elevated in 2024 as concentrated drilling, midstream and niche OEMs tightened capacity, raising costs and switching barriers.

Field labour shortages drove wage uplifts of 15–30% and remote site premiums; take-or-pay midstream contracts and double‑digit USD/bbl differentials amplified leverage.

Energy (~CAD 0.08/kWh) and carbon policy (CAD 170/tCO2e by 2030) add sustained input pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Energy | ~CAD 0.08/kWh | ↑ operating costs |

| Wage uplift | 15–30% | labour cost pressure |

| Carbon | CAD 170/t target by 2030 | ↑ compliance fees |

What is included in the product

Tailored Porter's Five Forces analysis for Cardinal that uncovers competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive threats and strategic protections to inform pricing, positioning, and growth decisions.

A single, editable one-sheet that quantifies and visualizes Porter’s Five Forces—instantly revealing strategic pain points with a clear radar chart so teams can prioritize fixes and update pressure levels as market conditions change.

Customers Bargaining Power

Commodity price-takers

Cardinal is a commodity price-taker as sales are tied to benchmarks WTI/WCS/AECO, with 2024 WTI averaging roughly $80/bbl, constraining pricing discretion. Buyers can switch producers at low cost when specs match, making differentials and transportation often more decisive than brand. Pipeline and rail options plus WCS differentials (wide in 2024) drive netbacks. Producers hedge to lock realized prices, but hedging does not increase buyer bargaining power.

Concentrated refiners and marketers

A limited set of refiners, traders and midstream marketers purchase large volumes—US petroleum consumption averaged about 20.5 mbpd in 2024—concentrating demand and enabling tougher terms on quality, delivery and penalties. Cardinal’s diversified product slate broadens outlet options across fuels, petrochemicals and feedstocks, while forward sales and multi-year term contracts partly blunt counterparty leverage and stabilize margins.

Quality and specification sensitivity

Light/medium versus heavy crude narrows the buyer pool and in 2024 Western Canadian Select traded at roughly a US$25/bbl discount to WTI, illustrating material price haircuts for heavy grades; failure to meet specs risks further discounts or rejection. Investments in blending and treating lift API and lower sulfur, improving marketability and realized price. Upgrading gas processing to meet AECO benchmarks (AECO ~CAD2.10/GJ in 2024) cuts buyers’ bargaining edge.

Logistics optionality

Access to multiple hubs, pipelines and rail (2024: 3+ accessible hubs in major basins) broadens buyer sets and typically narrows differentials, while constrained takeaway drives location discounts and buyer leverage. On-site and regional storage gives timing flexibility to avoid distressed sales, and marketing partnerships in 2024 unlocked incremental demand channels for spot and term volumes.

- Hubs: 3+ (2024)

- Takeaway discounts: ↑ buyer leverage

- Storage: avoids distressed exits

- Marketing deals: unlock demand

ESG and certification demands

Buyers increasingly demand emissions data and ESG assurances, raising negotiation levers; CDP reported 18,700 company disclosures in 2023 and EU CSRD expands mandatory reporting to ~50,000 firms from 2024. Certified responsible production can secure price premiums or access to select buyers, while non-compliance risks exclusion or contract discounts. Transparent reporting and methane-reduction measures (Global Methane Pledge: 150+ countries) strengthen seller leverage.

- ESG disclosures: CDP 2023: 18,700 companies

- Regulation: CSRD ~50,000 firms from 2024

- Methane focus: 150+ countries pledge

- Impact: certification = premiums/access; non-compliance = discounts/exclusion

Energy producer price-taker vs WTI/WCS/AECO; hubs, storage and ESG shift buyer dynamics

Cardinal is a price-taker tied to WTI/WCS/AECO (WTI ~US$80/bbl, WCS ~US$25/bbl discount in 2024), limiting pricing power. Large refiners/traders (~US consumption 20.5 mbpd in 2024) concentrate buying power, but diversified slate, term contracts and storage mitigate leverage. Infrastructure (3+ hubs) and takeaway constraints drive differentials; ESG/ESR reporting (CDP 18,700 in 2023; CSRD ~50,000) adds new buyer levers.

| Metric | 2024 Value |

|---|---|

| WTI | ~US$80/bbl |

| WCS discount | ~US$25/bbl |

| US demand | 20.5 mbpd |

| AECO | ~CAD2.10/GJ |

| Hubs accessible | 3+ |

| CDP disclosures | 18,700 (2023) |

Preview the Actual Deliverable

Cardinal Porter's Five Forces Analysis

This Cardinal Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders or samples. It contains the complete industry evaluation, competitive insights, and strategic implications ready for download and use. What you see is precisely what you get.