CareCloud SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

CareCloud shows strong cloud-native EHR and revenue-cycle strengths, but faces competitive pressure and margin risks amid regulatory shifts. Want the full story on strengths, weaknesses, opportunities and threats? Purchase the complete SWOT analysis for an editable, investor-ready report and Excel matrix to plan and pitch with confidence.

Strengths

Integrated cloud platform

CareCloud’s integrated cloud platform unifies EHR, PM, RCM and patient engagement to reduce vendor sprawl and data silos, streamlining a single workflow that lowers handoffs and accelerates revenue capture. Interoperability across modules improves data accuracy and enables richer analytics for coding and billing. This cohesiveness enhances provider and staff productivity and reduces administrative burden.

Revenue cycle expertise

CareClouds deep RCM capabilities accelerate claim submission (≈30% faster), reduce denials (≈40% lower) and lift collections (≈25% improvement), directly improving practice cash flow and client ROI. Automation and rules engines standardize billing across large provider groups, cutting manual touches and scaling operations. Financial dashboards deliver real-time KPI visibility, enabling faster revenue decisions and higher client retention.

Healthcare-focused UX

CareCloud’s healthcare-focused UX delivers ambulatory-tailored clinical workflows and templates that speed charting and match specialty needs, reducing clicks and documentation burden. Patient-facing tools streamline scheduling, telehealth (telehealth rose to about 13% of outpatient visits by 2021) and payments, improving access and revenue capture. Strong usability drives faster adoption and higher clinician satisfaction, lowering burnout and support costs.

Scalable SaaS model

Cloud delivery reduces upfront IT capital and simplifies updates, while elastic infrastructure scales from solo practices to multi-site groups; CareCloud’s SaaS approach enables frequent regulatory releases and subscription pricing that smooths operating budgets for providers.

Data and analytics

Integrated datasets enable performance benchmarking and actionable care insights, while advanced reporting enhances coding accuracy and strengthens payer negotiations. Population health views support quality programs and transition to value-based care, and actionable analytics help practices optimize revenue cycles and clinical operations.

- benchmarking

- coding_accuracy

- population_health

- revenue_optimization

Cloud EHR+RCM: ≈30% faster claims, ≈40% fewer denials

CareCloud’s unified cloud EHR+RCM reduces vendor sprawl, boosting staff productivity and data accuracy. Deep RCM yields ≈30% faster claims, ≈40% fewer denials and ≈25% higher collections, improving cash flow. SaaS scalability and analytics enable benchmarking, population health and faster regulatory updates.

| Metric | Impact |

|---|---|

| Claims speed | ≈30% faster |

| Denials | ≈40% lower |

| Collections | ≈25% lift |

What is included in the product

Provides a concise strategic overview of CareCloud’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Tailored CareCloud SWOT matrix for fast, visual alignment of strategy and product priorities, reducing time spent reconciling stakeholder views.

Weaknesses

Competitive EHR market

Large incumbents and niche specialists crowd the EHR space. Epic (~34%) and Oracle Cerner (~26%) together exceed 50% of the US hospital EHR market, raising barriers to entry. Switching costs and entrenched systems mean replacements often exceed $100M and churn remains low. Feature parity expectations increase R&D burden, so differentiation requires sustained investment and clear messaging.

Interoperability constraints

Variability in payer and HIE connections can hinder seamless data exchange, and gaps risk clinician frustration and duplicate entry. Dependence on third-party APIs introduces fragility and potential per-call fees and vendor lock-in. Standards compliance is ongoing—HL7 FHIR R4 was made normative in 2019 and TEFCA pilots progressed in 2023—so integration work continues.

Provider change fatigue

Provider change fatigue: with roughly 50% of clinicians reporting burnout in recent 2024 surveys, resistance to new workflows rises; implementations and training consume months and often exceed $250k in direct costs; poor onboarding can reduce adoption by 20–30%, and extended go-lives commonly delay revenue realization by several months.

Margin pressure

Price-sensitive small practices push for steep discounts, squeezing CareClouds margins as competition and value-based contracting intensify. Support, compliance, and EHR/integration costs escalate with regulatory updates and interoperability demands, driving up operating expenses. RCM performance guarantees and contingency pricing compress profitability, while aggressive upsell or cross-sell risks churn if packaging lacks clear incremental ROI.

- Discount pressure from small practices

- Rising support, compliance & integration costs

- RCM guarantees compress margins

- Upsell requires careful ROI packaging to avoid churn

Regulatory burden

Frequent regulatory changes force CareCloud to pivot roadmaps, raising development costs and elongating time-to-market; HIPAA-related penalties can reach up to 1,500,000 per violation category annually, making delays and noncompliance materially risky for clients.

- Certification, audits, security overhead increasing operating costs

- Delays risk client penalties and churn

- Smaller vendors bear disproportionate compliance burden

Incumbents, >$100M switching costs and integration gaps; ~50% clinician burnout limits adoption

Dominant incumbents (Epic ~34%, Oracle Cerner ~26%) create high entry barriers and switching costs often >$100M. Integration gaps, third-party API fragility and ongoing FHIR/TEFCA work raise R&D and operational burden. Clinician burnout (~50% in 2024) and implementation costs (typ. >$250k) slow adoption and increase churn risk.

| Metric | Value |

|---|---|

| Top two EHR share | ~60% |

| Clinician burnout (2024) | ~50% |

| Typical implementation cost | >$250,000 |

| HIPAA max penalty | $1,500,000 per category |

Same Document Delivered

CareCloud SWOT Analysis

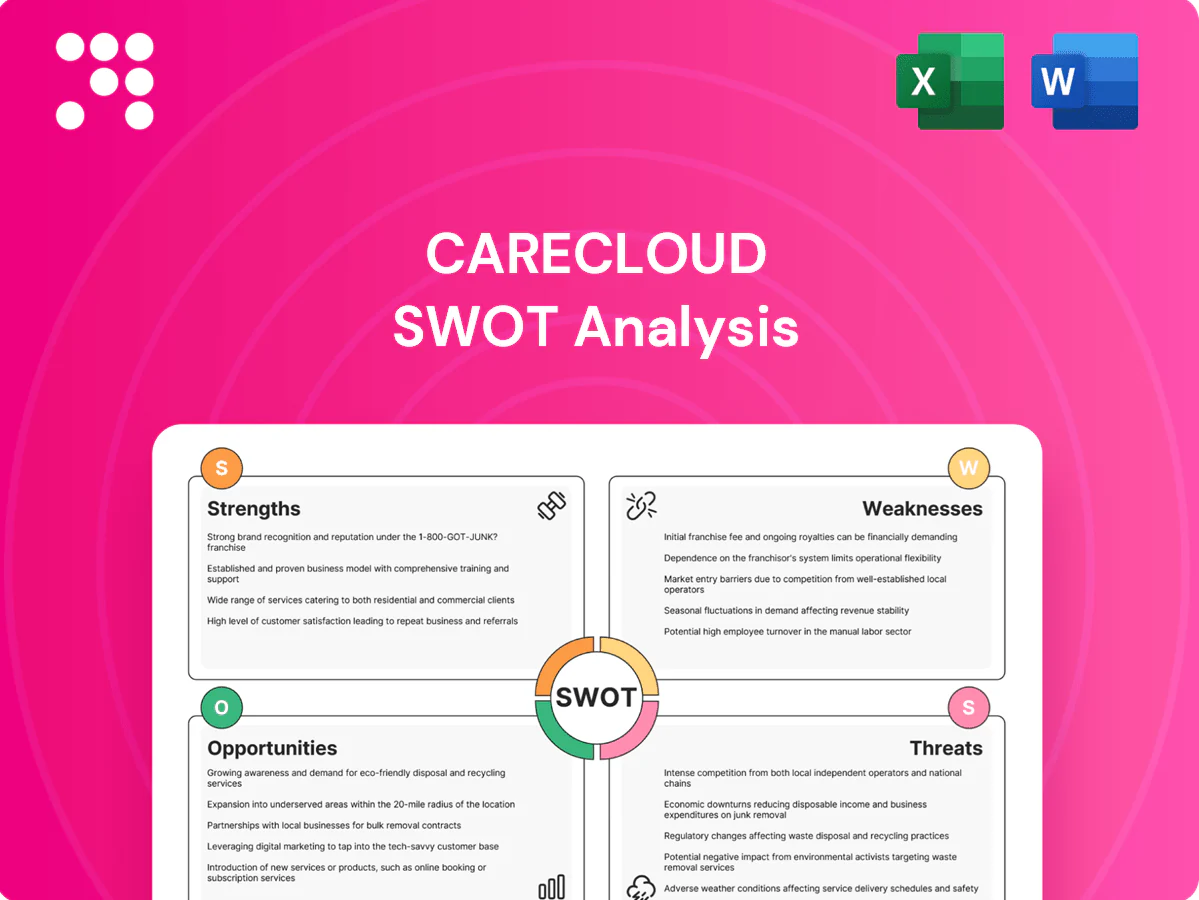

This is the actual CareCloud SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is drawn directly from the full report, and buying unlocks the complete, editable version with detailed strengths, weaknesses, opportunities, and threats. Use it as-is for presentations, strategy work, or further customization.

Elevate Your Analysis with the Complete SWOT Report

CareCloud shows strong cloud-native EHR and revenue-cycle strengths, but faces competitive pressure and margin risks amid regulatory shifts. Want the full story on strengths, weaknesses, opportunities and threats? Purchase the complete SWOT analysis for an editable, investor-ready report and Excel matrix to plan and pitch with confidence.

Strengths

Integrated cloud platform

CareCloud’s integrated cloud platform unifies EHR, PM, RCM and patient engagement to reduce vendor sprawl and data silos, streamlining a single workflow that lowers handoffs and accelerates revenue capture. Interoperability across modules improves data accuracy and enables richer analytics for coding and billing. This cohesiveness enhances provider and staff productivity and reduces administrative burden.

Revenue cycle expertise

CareClouds deep RCM capabilities accelerate claim submission (≈30% faster), reduce denials (≈40% lower) and lift collections (≈25% improvement), directly improving practice cash flow and client ROI. Automation and rules engines standardize billing across large provider groups, cutting manual touches and scaling operations. Financial dashboards deliver real-time KPI visibility, enabling faster revenue decisions and higher client retention.

Healthcare-focused UX

CareCloud’s healthcare-focused UX delivers ambulatory-tailored clinical workflows and templates that speed charting and match specialty needs, reducing clicks and documentation burden. Patient-facing tools streamline scheduling, telehealth (telehealth rose to about 13% of outpatient visits by 2021) and payments, improving access and revenue capture. Strong usability drives faster adoption and higher clinician satisfaction, lowering burnout and support costs.

Scalable SaaS model

Cloud delivery reduces upfront IT capital and simplifies updates, while elastic infrastructure scales from solo practices to multi-site groups; CareCloud’s SaaS approach enables frequent regulatory releases and subscription pricing that smooths operating budgets for providers.

Data and analytics

Integrated datasets enable performance benchmarking and actionable care insights, while advanced reporting enhances coding accuracy and strengthens payer negotiations. Population health views support quality programs and transition to value-based care, and actionable analytics help practices optimize revenue cycles and clinical operations.

- benchmarking

- coding_accuracy

- population_health

- revenue_optimization

Cloud EHR+RCM: ≈30% faster claims, ≈40% fewer denials

CareCloud’s unified cloud EHR+RCM reduces vendor sprawl, boosting staff productivity and data accuracy. Deep RCM yields ≈30% faster claims, ≈40% fewer denials and ≈25% higher collections, improving cash flow. SaaS scalability and analytics enable benchmarking, population health and faster regulatory updates.

| Metric | Impact |

|---|---|

| Claims speed | ≈30% faster |

| Denials | ≈40% lower |

| Collections | ≈25% lift |

What is included in the product

Provides a concise strategic overview of CareCloud’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Tailored CareCloud SWOT matrix for fast, visual alignment of strategy and product priorities, reducing time spent reconciling stakeholder views.

Weaknesses

Competitive EHR market

Large incumbents and niche specialists crowd the EHR space. Epic (~34%) and Oracle Cerner (~26%) together exceed 50% of the US hospital EHR market, raising barriers to entry. Switching costs and entrenched systems mean replacements often exceed $100M and churn remains low. Feature parity expectations increase R&D burden, so differentiation requires sustained investment and clear messaging.

Interoperability constraints

Variability in payer and HIE connections can hinder seamless data exchange, and gaps risk clinician frustration and duplicate entry. Dependence on third-party APIs introduces fragility and potential per-call fees and vendor lock-in. Standards compliance is ongoing—HL7 FHIR R4 was made normative in 2019 and TEFCA pilots progressed in 2023—so integration work continues.

Provider change fatigue

Provider change fatigue: with roughly 50% of clinicians reporting burnout in recent 2024 surveys, resistance to new workflows rises; implementations and training consume months and often exceed $250k in direct costs; poor onboarding can reduce adoption by 20–30%, and extended go-lives commonly delay revenue realization by several months.

Margin pressure

Price-sensitive small practices push for steep discounts, squeezing CareClouds margins as competition and value-based contracting intensify. Support, compliance, and EHR/integration costs escalate with regulatory updates and interoperability demands, driving up operating expenses. RCM performance guarantees and contingency pricing compress profitability, while aggressive upsell or cross-sell risks churn if packaging lacks clear incremental ROI.

- Discount pressure from small practices

- Rising support, compliance & integration costs

- RCM guarantees compress margins

- Upsell requires careful ROI packaging to avoid churn

Regulatory burden

Frequent regulatory changes force CareCloud to pivot roadmaps, raising development costs and elongating time-to-market; HIPAA-related penalties can reach up to 1,500,000 per violation category annually, making delays and noncompliance materially risky for clients.

- Certification, audits, security overhead increasing operating costs

- Delays risk client penalties and churn

- Smaller vendors bear disproportionate compliance burden

Incumbents, >$100M switching costs and integration gaps; ~50% clinician burnout limits adoption

Dominant incumbents (Epic ~34%, Oracle Cerner ~26%) create high entry barriers and switching costs often >$100M. Integration gaps, third-party API fragility and ongoing FHIR/TEFCA work raise R&D and operational burden. Clinician burnout (~50% in 2024) and implementation costs (typ. >$250k) slow adoption and increase churn risk.

| Metric | Value |

|---|---|

| Top two EHR share | ~60% |

| Clinician burnout (2024) | ~50% |

| Typical implementation cost | >$250,000 |

| HIPAA max penalty | $1,500,000 per category |

Same Document Delivered

CareCloud SWOT Analysis

This is the actual CareCloud SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is drawn directly from the full report, and buying unlocks the complete, editable version with detailed strengths, weaknesses, opportunities, and threats. Use it as-is for presentations, strategy work, or further customization.

Description

Elevate Your Analysis with the Complete SWOT Report

CareCloud shows strong cloud-native EHR and revenue-cycle strengths, but faces competitive pressure and margin risks amid regulatory shifts. Want the full story on strengths, weaknesses, opportunities and threats? Purchase the complete SWOT analysis for an editable, investor-ready report and Excel matrix to plan and pitch with confidence.

Strengths

Integrated cloud platform

CareCloud’s integrated cloud platform unifies EHR, PM, RCM and patient engagement to reduce vendor sprawl and data silos, streamlining a single workflow that lowers handoffs and accelerates revenue capture. Interoperability across modules improves data accuracy and enables richer analytics for coding and billing. This cohesiveness enhances provider and staff productivity and reduces administrative burden.

Revenue cycle expertise

CareClouds deep RCM capabilities accelerate claim submission (≈30% faster), reduce denials (≈40% lower) and lift collections (≈25% improvement), directly improving practice cash flow and client ROI. Automation and rules engines standardize billing across large provider groups, cutting manual touches and scaling operations. Financial dashboards deliver real-time KPI visibility, enabling faster revenue decisions and higher client retention.

Healthcare-focused UX

CareCloud’s healthcare-focused UX delivers ambulatory-tailored clinical workflows and templates that speed charting and match specialty needs, reducing clicks and documentation burden. Patient-facing tools streamline scheduling, telehealth (telehealth rose to about 13% of outpatient visits by 2021) and payments, improving access and revenue capture. Strong usability drives faster adoption and higher clinician satisfaction, lowering burnout and support costs.

Scalable SaaS model

Cloud delivery reduces upfront IT capital and simplifies updates, while elastic infrastructure scales from solo practices to multi-site groups; CareCloud’s SaaS approach enables frequent regulatory releases and subscription pricing that smooths operating budgets for providers.

Data and analytics

Integrated datasets enable performance benchmarking and actionable care insights, while advanced reporting enhances coding accuracy and strengthens payer negotiations. Population health views support quality programs and transition to value-based care, and actionable analytics help practices optimize revenue cycles and clinical operations.

- benchmarking

- coding_accuracy

- population_health

- revenue_optimization

Cloud EHR+RCM: ≈30% faster claims, ≈40% fewer denials

CareCloud’s unified cloud EHR+RCM reduces vendor sprawl, boosting staff productivity and data accuracy. Deep RCM yields ≈30% faster claims, ≈40% fewer denials and ≈25% higher collections, improving cash flow. SaaS scalability and analytics enable benchmarking, population health and faster regulatory updates.

| Metric | Impact |

|---|---|

| Claims speed | ≈30% faster |

| Denials | ≈40% lower |

| Collections | ≈25% lift |

What is included in the product

Provides a concise strategic overview of CareCloud’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Tailored CareCloud SWOT matrix for fast, visual alignment of strategy and product priorities, reducing time spent reconciling stakeholder views.

Weaknesses

Competitive EHR market

Large incumbents and niche specialists crowd the EHR space. Epic (~34%) and Oracle Cerner (~26%) together exceed 50% of the US hospital EHR market, raising barriers to entry. Switching costs and entrenched systems mean replacements often exceed $100M and churn remains low. Feature parity expectations increase R&D burden, so differentiation requires sustained investment and clear messaging.

Interoperability constraints

Variability in payer and HIE connections can hinder seamless data exchange, and gaps risk clinician frustration and duplicate entry. Dependence on third-party APIs introduces fragility and potential per-call fees and vendor lock-in. Standards compliance is ongoing—HL7 FHIR R4 was made normative in 2019 and TEFCA pilots progressed in 2023—so integration work continues.

Provider change fatigue

Provider change fatigue: with roughly 50% of clinicians reporting burnout in recent 2024 surveys, resistance to new workflows rises; implementations and training consume months and often exceed $250k in direct costs; poor onboarding can reduce adoption by 20–30%, and extended go-lives commonly delay revenue realization by several months.

Margin pressure

Price-sensitive small practices push for steep discounts, squeezing CareClouds margins as competition and value-based contracting intensify. Support, compliance, and EHR/integration costs escalate with regulatory updates and interoperability demands, driving up operating expenses. RCM performance guarantees and contingency pricing compress profitability, while aggressive upsell or cross-sell risks churn if packaging lacks clear incremental ROI.

- Discount pressure from small practices

- Rising support, compliance & integration costs

- RCM guarantees compress margins

- Upsell requires careful ROI packaging to avoid churn

Regulatory burden

Frequent regulatory changes force CareCloud to pivot roadmaps, raising development costs and elongating time-to-market; HIPAA-related penalties can reach up to 1,500,000 per violation category annually, making delays and noncompliance materially risky for clients.

- Certification, audits, security overhead increasing operating costs

- Delays risk client penalties and churn

- Smaller vendors bear disproportionate compliance burden

Incumbents, >$100M switching costs and integration gaps; ~50% clinician burnout limits adoption

Dominant incumbents (Epic ~34%, Oracle Cerner ~26%) create high entry barriers and switching costs often >$100M. Integration gaps, third-party API fragility and ongoing FHIR/TEFCA work raise R&D and operational burden. Clinician burnout (~50% in 2024) and implementation costs (typ. >$250k) slow adoption and increase churn risk.

| Metric | Value |

|---|---|

| Top two EHR share | ~60% |

| Clinician burnout (2024) | ~50% |

| Typical implementation cost | >$250,000 |

| HIPAA max penalty | $1,500,000 per category |

Same Document Delivered

CareCloud SWOT Analysis

This is the actual CareCloud SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is drawn directly from the full report, and buying unlocks the complete, editable version with detailed strengths, weaknesses, opportunities, and threats. Use it as-is for presentations, strategy work, or further customization.