CareDx Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

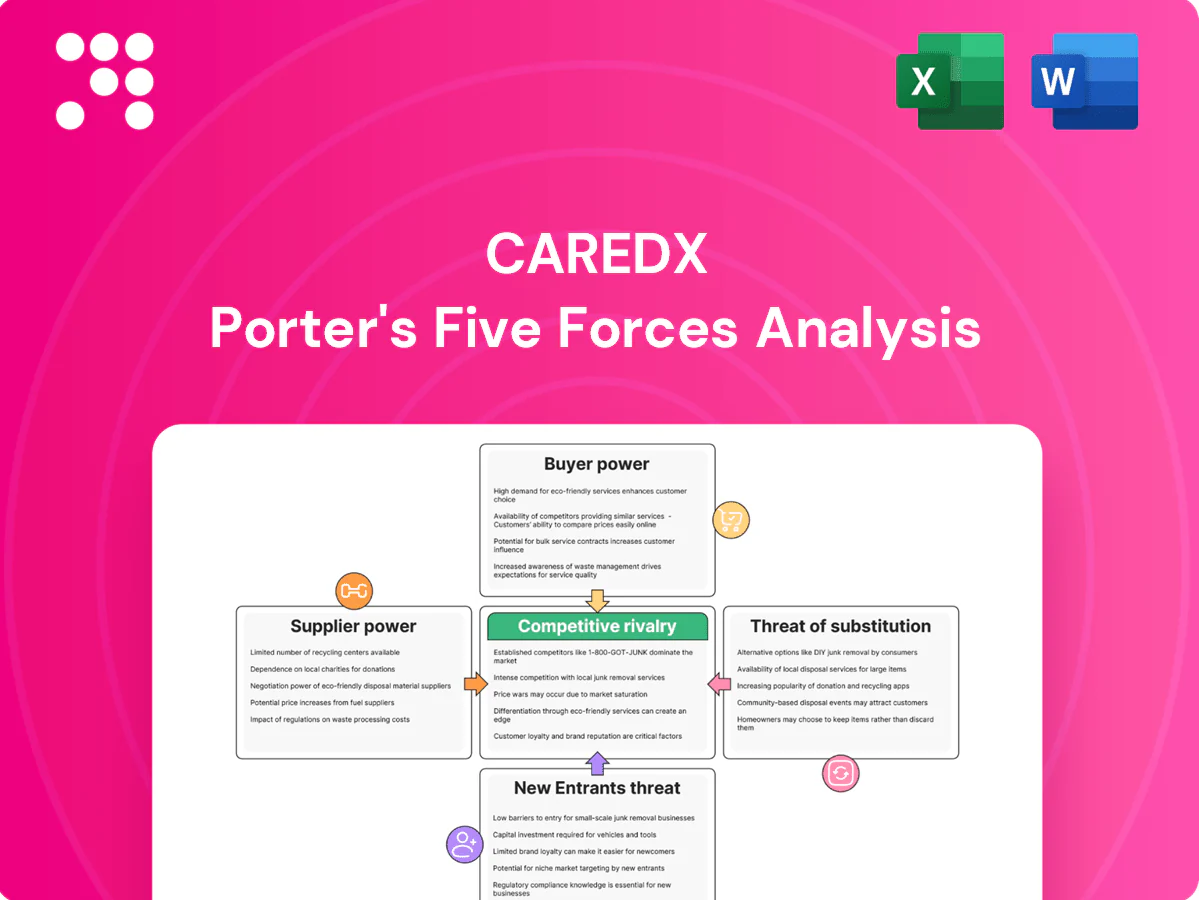

CareDx faces moderate buyer power, concentrated supplier relationships, strong competitive rivalry, niche substitute threats, and high regulatory barriers—each shaping margins and growth prospects. This snapshot only hints at the dynamics; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Specialized reagents concentration

In 2024 CareDx depends on a narrow set of high-quality NGS reagents, cfDNA kits and consumables supplied primarily by three global vendors (eg, Illumina, Thermo Fisher, QIAGEN), limiting substitutions and raising switching costs. Strict quality and validation requirements mean suppliers can exert pricing leverage during shortages. Dual-sourcing is feasible but adds technical validation, supply-chain complexity and lead-time risk.

Sequencing platforms dependency

Sequencing platform dependency raises supplier power: Illumina held roughly 70% of installed short‑read sequencers in 2024, creating platform lock‑in via service contracts and upgrade cycles. Performance validation tying CareDx assays to specific instruments limits switching; transplant testing represents under 5% of clinical NGS volume in 2024, so negotiating leverage from volume is weak. Any platform discontinuity can materially disrupt throughput and margins for CareDx, which reported ~$669M revenue in FY2024.

Bioinformatics and cloud inputs

Dependencies on specialized software, bioinformatics pipelines and major cloud providers expose CareDx to cost pass-through risk and margin pressure; in 2024 this dependency remained central to operations. Data security and regulatory compliance narrow vendor optionality, while proprietary algorithms reduce but do not remove reliance on external infrastructure. Vendor outages or price hikes can directly raise COGS and delay turnaround times.

Biobank and sample access

High-quality, longitudinal transplant cohorts and reference materials are scarce and often controlled by academic centers and consortia, increasing supplier leverage; for example, BBMRI-ERIC links over 600 biobanks in Europe (2024). Data-use agreements are frequently restrictive, add months to access timelines and can include material transfer or access fees, raising validation costs and supplier bargaining power.

- Scarcity: limited longitudinal transplant cohorts

- Gatekeepers: academic centers/consortia (BBMRI-ERIC >600 biobanks, 2024)

- DUAs: restrictive, months delay, fees

- Impact: higher supplier power over validation resources

Regulatory-grade components

Regulatory-grade components for CareDx must meet CLIA/CAP and often FDA requirements, concentrating sourcing to a small set of qualified suppliers and raising supplier bargaining power. Re-qualification of alternative suppliers typically requires 6–12 months and frequently $250k–$1M in validation costs, limiting rapid switches. Compliance timelines and audit readiness further constrain procurement flexibility and elevate supplier pricing leverage.

- Few qualified suppliers increases dependency

- 6–12 months & 250k–1M re-qualification burden

- CLIA/CAP/FDA compliance limits rapid switching

Transplant diagnostics firm faces supplier risk: Illumina ~70% share, costly requalification

CareDx faces high supplier power in 2024: concentrated reagents/platforms (Illumina ~70% short‑read share), three primary vendors (Illumina, Thermo Fisher, QIAGEN), transplant tests <5% of clinical NGS volume, and FY2024 revenue ~$669M. Requalification takes 6–12 months and typically costs $250k–$1M, constraining rapid supplier switches and raising COGS risk.

| Metric | 2024 Value |

|---|---|

| Illumina short‑read share | ~70% |

| CareDx FY2024 revenue | $669M |

| Transplant NGS volume | <5% |

| Requalification time/cost | 6–12 months / $250k–$1M |

What is included in the product

Tailored Porter's Five Forces analysis for CareDx that uncovers competitive intensity, supplier and buyer power, entry barriers, substitute threats, and emerging disruptors, with strategic commentary and editable Word format for use in investor decks, business plans, or internal strategy reviews.

A concise, one-sheet Porter's Five Forces for CareDx that instantly highlights competitive threats, supplier/payer bargaining pressures, and entrant risks—customizable for evolving transplant diagnostics data and ready to drop into decks or reports.

Customers Bargaining Power

Transplant centers as key accounts

Large transplant hospitals act as key accounts and concentrate purchasing power across roughly 41,000 U.S. solid-organ transplants annually (OPTN 2023), enabling aggressive negotiation on price and service. Clinical committees and KOLs within hospital networks drive testing adoption and protocol standardization. Contract wins or losses can materially shift regional share. High switching costs persist but are often reduced by parallel testing and formal evaluation protocols.

Payer coverage and pricing

In 2024 commercial insurers and government payers continued to set reimbursement levels and prior authorization rules that directly determine CareDx’s net price realization and create negotiating leverage. Coverage policies and prior auth requirements allow payers to demand stronger clinical evidence and discounts. Robust outcomes and real-world data can strengthen CareDx’s position with payers. Down-coding and claim denials remain persistent margin pressures.

Integrated delivery networks

Integrated delivery networks and GPOs bundle diagnostics contracts to extract better pricing and can standardize on a single vendor, raising retention stakes for CareDx; major IDNs control about two-thirds of U.S. hospital beds, magnifying account value. Value-based contracts increasingly shift reimbursement and clinical risk to the lab, while CareDx's demonstrated biopsy cost offsets strengthen negotiating leverage in contracting.

Clinician preference sensitivity

Physician confidence in clinical utility drives test ordering for transplant care; publications, guidelines and 2024 real-world cohorts increasingly shape preferences, and CareDx reported ~487M revenue in 2024 reflecting market uptake. Competing assays can be trialed in parallel for head-to-head comparison, while education and support services lower perceived switching risk and preserve pricing power.

- Physician-led ordering

- Guidelines/RWD influence

- Parallel assay trials

- Education reduces switching

Patient advocacy and adherence

Informed patients increasingly request specific CareDx assays, modestly countering buyer power, but ordering authority remains with transplant centers and payers; CareDx reported 2024 revenue of 624 million USD, underlining payer-driven volumes. Turnaround time, access and copays drive demand elasticity while CareDx financial assistance and payer contracts blunt out-of-pocket pushback.

- Patient requests ↑, but centers/payers control ordering

- 2024 revenue: 624M USD

- Turnaround, access, copays → demand elasticity

- Assistance programs reduce out-of-pocket resistance

Transplant purchasing: ≈41,000; IDNs ≈66% beds

Transplant centers concentrate purchasing power (≈41,000 U.S. transplants, OPTN 2023), enabling strong price/service negotiation. Payers set reimbursement and prior authorization, directly determining net price and creating leverage. IDNs/GPOs (≈two-thirds of U.S. hospital beds) bundle contracts, while patient requests have limited ordering impact; CareDx 2024 revenue: 624M USD.

| Metric | Value |

|---|---|

| U.S. solid-organ transplants (2023) | ≈41,000 |

| CareDx revenue (2024) | 624M USD |

| IDN hospital bed share | ≈66% |

What You See Is What You Get

CareDx Porter's Five Forces Analysis

This CareDx Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive upon purchase—no placeholders or samples. It contains the complete strategic assessment ready for immediate download and use. Purchase grants instant access to this same professional file, prepared for decision-making and presentation.

A Must-Have Tool for Decision-Makers

CareDx faces moderate buyer power, concentrated supplier relationships, strong competitive rivalry, niche substitute threats, and high regulatory barriers—each shaping margins and growth prospects. This snapshot only hints at the dynamics; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Specialized reagents concentration

In 2024 CareDx depends on a narrow set of high-quality NGS reagents, cfDNA kits and consumables supplied primarily by three global vendors (eg, Illumina, Thermo Fisher, QIAGEN), limiting substitutions and raising switching costs. Strict quality and validation requirements mean suppliers can exert pricing leverage during shortages. Dual-sourcing is feasible but adds technical validation, supply-chain complexity and lead-time risk.

Sequencing platforms dependency

Sequencing platform dependency raises supplier power: Illumina held roughly 70% of installed short‑read sequencers in 2024, creating platform lock‑in via service contracts and upgrade cycles. Performance validation tying CareDx assays to specific instruments limits switching; transplant testing represents under 5% of clinical NGS volume in 2024, so negotiating leverage from volume is weak. Any platform discontinuity can materially disrupt throughput and margins for CareDx, which reported ~$669M revenue in FY2024.

Bioinformatics and cloud inputs

Dependencies on specialized software, bioinformatics pipelines and major cloud providers expose CareDx to cost pass-through risk and margin pressure; in 2024 this dependency remained central to operations. Data security and regulatory compliance narrow vendor optionality, while proprietary algorithms reduce but do not remove reliance on external infrastructure. Vendor outages or price hikes can directly raise COGS and delay turnaround times.

Biobank and sample access

High-quality, longitudinal transplant cohorts and reference materials are scarce and often controlled by academic centers and consortia, increasing supplier leverage; for example, BBMRI-ERIC links over 600 biobanks in Europe (2024). Data-use agreements are frequently restrictive, add months to access timelines and can include material transfer or access fees, raising validation costs and supplier bargaining power.

- Scarcity: limited longitudinal transplant cohorts

- Gatekeepers: academic centers/consortia (BBMRI-ERIC >600 biobanks, 2024)

- DUAs: restrictive, months delay, fees

- Impact: higher supplier power over validation resources

Regulatory-grade components

Regulatory-grade components for CareDx must meet CLIA/CAP and often FDA requirements, concentrating sourcing to a small set of qualified suppliers and raising supplier bargaining power. Re-qualification of alternative suppliers typically requires 6–12 months and frequently $250k–$1M in validation costs, limiting rapid switches. Compliance timelines and audit readiness further constrain procurement flexibility and elevate supplier pricing leverage.

- Few qualified suppliers increases dependency

- 6–12 months & 250k–1M re-qualification burden

- CLIA/CAP/FDA compliance limits rapid switching

Transplant diagnostics firm faces supplier risk: Illumina ~70% share, costly requalification

CareDx faces high supplier power in 2024: concentrated reagents/platforms (Illumina ~70% short‑read share), three primary vendors (Illumina, Thermo Fisher, QIAGEN), transplant tests <5% of clinical NGS volume, and FY2024 revenue ~$669M. Requalification takes 6–12 months and typically costs $250k–$1M, constraining rapid supplier switches and raising COGS risk.

| Metric | 2024 Value |

|---|---|

| Illumina short‑read share | ~70% |

| CareDx FY2024 revenue | $669M |

| Transplant NGS volume | <5% |

| Requalification time/cost | 6–12 months / $250k–$1M |

What is included in the product

Tailored Porter's Five Forces analysis for CareDx that uncovers competitive intensity, supplier and buyer power, entry barriers, substitute threats, and emerging disruptors, with strategic commentary and editable Word format for use in investor decks, business plans, or internal strategy reviews.

A concise, one-sheet Porter's Five Forces for CareDx that instantly highlights competitive threats, supplier/payer bargaining pressures, and entrant risks—customizable for evolving transplant diagnostics data and ready to drop into decks or reports.

Customers Bargaining Power

Transplant centers as key accounts

Large transplant hospitals act as key accounts and concentrate purchasing power across roughly 41,000 U.S. solid-organ transplants annually (OPTN 2023), enabling aggressive negotiation on price and service. Clinical committees and KOLs within hospital networks drive testing adoption and protocol standardization. Contract wins or losses can materially shift regional share. High switching costs persist but are often reduced by parallel testing and formal evaluation protocols.

Payer coverage and pricing

In 2024 commercial insurers and government payers continued to set reimbursement levels and prior authorization rules that directly determine CareDx’s net price realization and create negotiating leverage. Coverage policies and prior auth requirements allow payers to demand stronger clinical evidence and discounts. Robust outcomes and real-world data can strengthen CareDx’s position with payers. Down-coding and claim denials remain persistent margin pressures.

Integrated delivery networks

Integrated delivery networks and GPOs bundle diagnostics contracts to extract better pricing and can standardize on a single vendor, raising retention stakes for CareDx; major IDNs control about two-thirds of U.S. hospital beds, magnifying account value. Value-based contracts increasingly shift reimbursement and clinical risk to the lab, while CareDx's demonstrated biopsy cost offsets strengthen negotiating leverage in contracting.

Clinician preference sensitivity

Physician confidence in clinical utility drives test ordering for transplant care; publications, guidelines and 2024 real-world cohorts increasingly shape preferences, and CareDx reported ~487M revenue in 2024 reflecting market uptake. Competing assays can be trialed in parallel for head-to-head comparison, while education and support services lower perceived switching risk and preserve pricing power.

- Physician-led ordering

- Guidelines/RWD influence

- Parallel assay trials

- Education reduces switching

Patient advocacy and adherence

Informed patients increasingly request specific CareDx assays, modestly countering buyer power, but ordering authority remains with transplant centers and payers; CareDx reported 2024 revenue of 624 million USD, underlining payer-driven volumes. Turnaround time, access and copays drive demand elasticity while CareDx financial assistance and payer contracts blunt out-of-pocket pushback.

- Patient requests ↑, but centers/payers control ordering

- 2024 revenue: 624M USD

- Turnaround, access, copays → demand elasticity

- Assistance programs reduce out-of-pocket resistance

Transplant purchasing: ≈41,000; IDNs ≈66% beds

Transplant centers concentrate purchasing power (≈41,000 U.S. transplants, OPTN 2023), enabling strong price/service negotiation. Payers set reimbursement and prior authorization, directly determining net price and creating leverage. IDNs/GPOs (≈two-thirds of U.S. hospital beds) bundle contracts, while patient requests have limited ordering impact; CareDx 2024 revenue: 624M USD.

| Metric | Value |

|---|---|

| U.S. solid-organ transplants (2023) | ≈41,000 |

| CareDx revenue (2024) | 624M USD |

| IDN hospital bed share | ≈66% |

What You See Is What You Get

CareDx Porter's Five Forces Analysis

This CareDx Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive upon purchase—no placeholders or samples. It contains the complete strategic assessment ready for immediate download and use. Purchase grants instant access to this same professional file, prepared for decision-making and presentation.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

CareDx faces moderate buyer power, concentrated supplier relationships, strong competitive rivalry, niche substitute threats, and high regulatory barriers—each shaping margins and growth prospects. This snapshot only hints at the dynamics; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Specialized reagents concentration

In 2024 CareDx depends on a narrow set of high-quality NGS reagents, cfDNA kits and consumables supplied primarily by three global vendors (eg, Illumina, Thermo Fisher, QIAGEN), limiting substitutions and raising switching costs. Strict quality and validation requirements mean suppliers can exert pricing leverage during shortages. Dual-sourcing is feasible but adds technical validation, supply-chain complexity and lead-time risk.

Sequencing platforms dependency

Sequencing platform dependency raises supplier power: Illumina held roughly 70% of installed short‑read sequencers in 2024, creating platform lock‑in via service contracts and upgrade cycles. Performance validation tying CareDx assays to specific instruments limits switching; transplant testing represents under 5% of clinical NGS volume in 2024, so negotiating leverage from volume is weak. Any platform discontinuity can materially disrupt throughput and margins for CareDx, which reported ~$669M revenue in FY2024.

Bioinformatics and cloud inputs

Dependencies on specialized software, bioinformatics pipelines and major cloud providers expose CareDx to cost pass-through risk and margin pressure; in 2024 this dependency remained central to operations. Data security and regulatory compliance narrow vendor optionality, while proprietary algorithms reduce but do not remove reliance on external infrastructure. Vendor outages or price hikes can directly raise COGS and delay turnaround times.

Biobank and sample access

High-quality, longitudinal transplant cohorts and reference materials are scarce and often controlled by academic centers and consortia, increasing supplier leverage; for example, BBMRI-ERIC links over 600 biobanks in Europe (2024). Data-use agreements are frequently restrictive, add months to access timelines and can include material transfer or access fees, raising validation costs and supplier bargaining power.

- Scarcity: limited longitudinal transplant cohorts

- Gatekeepers: academic centers/consortia (BBMRI-ERIC >600 biobanks, 2024)

- DUAs: restrictive, months delay, fees

- Impact: higher supplier power over validation resources

Regulatory-grade components

Regulatory-grade components for CareDx must meet CLIA/CAP and often FDA requirements, concentrating sourcing to a small set of qualified suppliers and raising supplier bargaining power. Re-qualification of alternative suppliers typically requires 6–12 months and frequently $250k–$1M in validation costs, limiting rapid switches. Compliance timelines and audit readiness further constrain procurement flexibility and elevate supplier pricing leverage.

- Few qualified suppliers increases dependency

- 6–12 months & 250k–1M re-qualification burden

- CLIA/CAP/FDA compliance limits rapid switching

Transplant diagnostics firm faces supplier risk: Illumina ~70% share, costly requalification

CareDx faces high supplier power in 2024: concentrated reagents/platforms (Illumina ~70% short‑read share), three primary vendors (Illumina, Thermo Fisher, QIAGEN), transplant tests <5% of clinical NGS volume, and FY2024 revenue ~$669M. Requalification takes 6–12 months and typically costs $250k–$1M, constraining rapid supplier switches and raising COGS risk.

| Metric | 2024 Value |

|---|---|

| Illumina short‑read share | ~70% |

| CareDx FY2024 revenue | $669M |

| Transplant NGS volume | <5% |

| Requalification time/cost | 6–12 months / $250k–$1M |

What is included in the product

Tailored Porter's Five Forces analysis for CareDx that uncovers competitive intensity, supplier and buyer power, entry barriers, substitute threats, and emerging disruptors, with strategic commentary and editable Word format for use in investor decks, business plans, or internal strategy reviews.

A concise, one-sheet Porter's Five Forces for CareDx that instantly highlights competitive threats, supplier/payer bargaining pressures, and entrant risks—customizable for evolving transplant diagnostics data and ready to drop into decks or reports.

Customers Bargaining Power

Transplant centers as key accounts

Large transplant hospitals act as key accounts and concentrate purchasing power across roughly 41,000 U.S. solid-organ transplants annually (OPTN 2023), enabling aggressive negotiation on price and service. Clinical committees and KOLs within hospital networks drive testing adoption and protocol standardization. Contract wins or losses can materially shift regional share. High switching costs persist but are often reduced by parallel testing and formal evaluation protocols.

Payer coverage and pricing

In 2024 commercial insurers and government payers continued to set reimbursement levels and prior authorization rules that directly determine CareDx’s net price realization and create negotiating leverage. Coverage policies and prior auth requirements allow payers to demand stronger clinical evidence and discounts. Robust outcomes and real-world data can strengthen CareDx’s position with payers. Down-coding and claim denials remain persistent margin pressures.

Integrated delivery networks

Integrated delivery networks and GPOs bundle diagnostics contracts to extract better pricing and can standardize on a single vendor, raising retention stakes for CareDx; major IDNs control about two-thirds of U.S. hospital beds, magnifying account value. Value-based contracts increasingly shift reimbursement and clinical risk to the lab, while CareDx's demonstrated biopsy cost offsets strengthen negotiating leverage in contracting.

Clinician preference sensitivity

Physician confidence in clinical utility drives test ordering for transplant care; publications, guidelines and 2024 real-world cohorts increasingly shape preferences, and CareDx reported ~487M revenue in 2024 reflecting market uptake. Competing assays can be trialed in parallel for head-to-head comparison, while education and support services lower perceived switching risk and preserve pricing power.

- Physician-led ordering

- Guidelines/RWD influence

- Parallel assay trials

- Education reduces switching

Patient advocacy and adherence

Informed patients increasingly request specific CareDx assays, modestly countering buyer power, but ordering authority remains with transplant centers and payers; CareDx reported 2024 revenue of 624 million USD, underlining payer-driven volumes. Turnaround time, access and copays drive demand elasticity while CareDx financial assistance and payer contracts blunt out-of-pocket pushback.

- Patient requests ↑, but centers/payers control ordering

- 2024 revenue: 624M USD

- Turnaround, access, copays → demand elasticity

- Assistance programs reduce out-of-pocket resistance

Transplant purchasing: ≈41,000; IDNs ≈66% beds

Transplant centers concentrate purchasing power (≈41,000 U.S. transplants, OPTN 2023), enabling strong price/service negotiation. Payers set reimbursement and prior authorization, directly determining net price and creating leverage. IDNs/GPOs (≈two-thirds of U.S. hospital beds) bundle contracts, while patient requests have limited ordering impact; CareDx 2024 revenue: 624M USD.

| Metric | Value |

|---|---|

| U.S. solid-organ transplants (2023) | ≈41,000 |

| CareDx revenue (2024) | 624M USD |

| IDN hospital bed share | ≈66% |

What You See Is What You Get

CareDx Porter's Five Forces Analysis

This CareDx Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive upon purchase—no placeholders or samples. It contains the complete strategic assessment ready for immediate download and use. Purchase grants instant access to this same professional file, prepared for decision-making and presentation.