Cargill Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

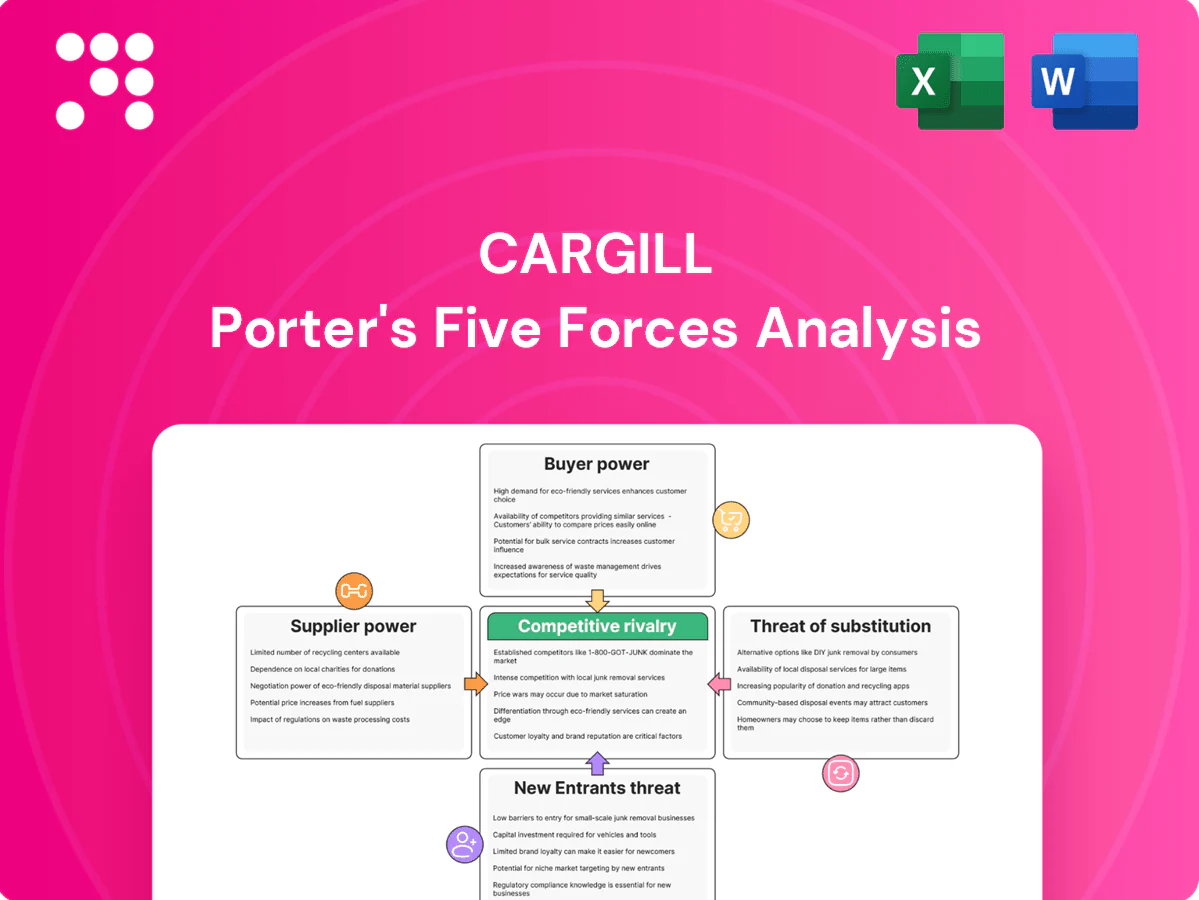

This snapshot highlights Cargill's bargaining power dynamics, supplier and buyer pressures, threat of substitutes, and competitive rivalry across agribusiness and food ingredients. It outlines entry barriers and regulatory risks shaping profit margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cargill’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented farm suppliers

Most agricultural inputs come from roughly 570 million small and mid‑size farms globally (FAO), diluting individual supplier leverage for buyers like Cargill. Cargill’s scale and global sourcing across 70+ countries lets it shift purchases by region and crop, reducing supplier hold. Long‑term contracts and agronomic support build loyalty and stabilize prices, but extreme weather and local policy shocks can temporarily increase supplier power.

Concentrated inputs in logistics and energy

Port access, rail, barge, trucking and fuel are concentrated among a few providers—top five ocean carriers control roughly 80% of container capacity and Class I railroads account for about 70% of US freight ton-miles in 2024—boosting supplier bargaining power. Congestion and capacity limits have raised logistics costs and reduced scheduling flexibility, at times adding days to transit. Cargill offsets this via owned terminals, long-term contracts and multimodal routing. Geopolitical shocks and 2024 oil-price swings (Brent ~86 USD/bbl) can still shift leverage to suppliers.

Seed, fertilizer, and crop protection majors

Upstream seed and agrochemical supply is concentrated, with the top four firms controlling roughly 60–70% of global seed and crop protection markets, supporting firmer pricing; fertilizer prices surged over 200% in 2021–22, tightening farm margins and increasing Cargill’s origination costs via lower farmer liquidity; Cargill is not the primary buyer but is exposed through yields and farmer economics; advisory and precision-ag services can boost efficiency and yields by ~5–10%, partly offsetting input shocks.

Specialty ingredients and additives

Certain specialty enzymes, cultures and functional ingredients have few qualified suppliers, with the top 3 enzyme firms holding about 60% of the market in 2024, raising dependency and regulatory-driven switching costs; Cargill reported roughly $165 billion revenue in 2024, enabling reformulation across its portfolio to reduce exposure. Co-development agreements with suppliers shift bargaining power via shared IP and volume commitments.

- Concentration: top-3 ~60% (2024)

- Switching costs: high due to qualification/regulatory

- Cargill scale: ~$165B revenue (2024)

- Mitigation: reformulation + co-development

Sustainability and certification gatekeepers

Certifiers and NGOs (RSPO, RTRS, deforestation-free initiatives) set what qualifies as acceptable supply, raising compliance costs and narrowing the supplier pool so certified producers gain pricing leverage; failure to meet standards can abruptly shift buying power to scarce certified sources. Cargill’s multi-year traceability investments have increased supplier access and reduced sourcing risk, supporting procurement flexibility in 2024.

- Certifier influence: shapes acceptability and premiums

- Compliance cost: reduces supplier pool, raises leverage

- Cargill traceability: expands access, lowers risk

Fragmented farms vs concentrated logistics and inputs create mixed power

Supplier power is mixed: fragmented farm supply (≈570M farms) limits individual leverage, but concentrated logistics (top-5 carriers ~80% capacity) and input suppliers (top-4 seeds 60–70%; top-3 enzymes ~60%) raise costs. Cargill scale (~$165B revenue in 2024) plus contracts, traceability and co-development lower vulnerability; fuel volatility (Brent ≈86 USD/bbl in 2024) can still shift power.

| Supplier | Concentration(2024) | Impact |

|---|---|---|

| Farms | Fragmented (~570M) | Low leverage |

| Ocean/Rail | Top-5 ~80% / Class I ~70% | High logistics power |

| Seeds/AgChem | Top-4 60–70% | Pricing pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Cargill that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform strategic and investment decisions.

One-sheet Porter's Five Forces for Cargill—instantly spot supply, buyer, and competitor pressures with a clean radar chart and customizable scores to guide strategic moves and reduce decision friction.

Customers Bargaining Power

Large multinational food manufacturers

Global CPGs and QSRs buy at scale and run competitive tenders that heighten price pressure, while insisting on consistent quality, service levels and sustainability credentials; multi-year contracts often trade margin for volume stability. Cargill, employing about 155,000 people in 2024, leverages product breadth and co-innovation to shift negotiations from pure price to value-added partnerships.

Commoditized product buyers

For commoditized grains, oils and basic ingredients switching costs are low and price transparency is high, letting buyers arbitrage among traders and origins; global grain trade remains large and liquid. Buyers push pricing down and agribusiness EBITDA margins are often slim, roughly 2–5% in 2024. Cargill offsets this with logistics reliability, hedging and risk-management services. Basis, freight and timing solutions can capture premiums despite thin unit margins.

Retailers and private label

Large retailers (top 3–4 chains controlling roughly 60% of grocery sales in key markets) exert strong negotiating power and impose strict compliance requirements. Private label growth, now about 20% of grocery sales in 2024, intensifies price sensitivity and margin pressure. Cargill differentiates through consistent supply, technical support and sustainability claims, but retailers demand OTIF >95%; missing on-time, in-full targets invites delisting pressure.

Animal producers and integrators

Large livestock and aquaculture integrators buy feed and premixes at scale and benchmark suppliers aggressively; in the US the top integrators account for over 50% of production, amplifying their negotiating leverage. Performance outcomes and strict biosecurity protocols create real switching frictions, while tailored formulations and on‑farm advisory services help Cargill retain high-volume accounts.

- Volume buyers: high purchase scale

- Benchmarking: aggressive price/performance comparison

- Switching frictions: biosecurity, performance risk

- Retention: tailored formulations, advisory services

Financial and risk management clients

Hedging and risk services buyers compare fees and analytics across banks and merchandisers, compressing margins. Sophisticated clients increasingly self-hedge, reducing pricing power for providers. Cargill reported about 174 billion dollars in 2023, so proprietary market insights and physical-derivatives integration create client stickiness. Regulatory compliance and credit terms, tightened post‑Basel III, drive negotiation leverage.

- Fee sensitivity: cross‑provider comparison

- Self‑hedging: lowers supplier pricing power

- Integration: physical+derivative analytics = retention

- Regulation/credit: key negotiation levers

Buyers squeeze prices as agribusiness margins tighten amid retail concentration

Buyers (global CPGs, QSRs, retailers, integrators) exert strong price and compliance pressure; Cargill (≈155,000 employees in 2024) shifts talks to value via breadth, co‑innovation and risk services. Commoditized grains/oils have low switching costs; agribusiness EBITDA margins ~2–5% in 2024, pushing basis/freight/timing premiums. Large retailers (top 3–4 ≈60% share) and private label (~20% of grocery sales in 2024) intensify margin pressure.

| Metric | 2024 |

|---|---|

| Employees | ≈155,000 |

| Agribusiness EBITDA | 2–5% |

| Retail concentration | Top3–4 ≈60% |

| Private label | ≈20% |

What You See Is What You Get

Cargill Porter's Five Forces Analysis

This Cargill Porter's Five Forces analysis delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Cargill’s agribusiness operations. The preview you see is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, no samples. It’s ready for download and use the moment you buy.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights Cargill's bargaining power dynamics, supplier and buyer pressures, threat of substitutes, and competitive rivalry across agribusiness and food ingredients. It outlines entry barriers and regulatory risks shaping profit margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cargill’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented farm suppliers

Most agricultural inputs come from roughly 570 million small and mid‑size farms globally (FAO), diluting individual supplier leverage for buyers like Cargill. Cargill’s scale and global sourcing across 70+ countries lets it shift purchases by region and crop, reducing supplier hold. Long‑term contracts and agronomic support build loyalty and stabilize prices, but extreme weather and local policy shocks can temporarily increase supplier power.

Concentrated inputs in logistics and energy

Port access, rail, barge, trucking and fuel are concentrated among a few providers—top five ocean carriers control roughly 80% of container capacity and Class I railroads account for about 70% of US freight ton-miles in 2024—boosting supplier bargaining power. Congestion and capacity limits have raised logistics costs and reduced scheduling flexibility, at times adding days to transit. Cargill offsets this via owned terminals, long-term contracts and multimodal routing. Geopolitical shocks and 2024 oil-price swings (Brent ~86 USD/bbl) can still shift leverage to suppliers.

Seed, fertilizer, and crop protection majors

Upstream seed and agrochemical supply is concentrated, with the top four firms controlling roughly 60–70% of global seed and crop protection markets, supporting firmer pricing; fertilizer prices surged over 200% in 2021–22, tightening farm margins and increasing Cargill’s origination costs via lower farmer liquidity; Cargill is not the primary buyer but is exposed through yields and farmer economics; advisory and precision-ag services can boost efficiency and yields by ~5–10%, partly offsetting input shocks.

Specialty ingredients and additives

Certain specialty enzymes, cultures and functional ingredients have few qualified suppliers, with the top 3 enzyme firms holding about 60% of the market in 2024, raising dependency and regulatory-driven switching costs; Cargill reported roughly $165 billion revenue in 2024, enabling reformulation across its portfolio to reduce exposure. Co-development agreements with suppliers shift bargaining power via shared IP and volume commitments.

- Concentration: top-3 ~60% (2024)

- Switching costs: high due to qualification/regulatory

- Cargill scale: ~$165B revenue (2024)

- Mitigation: reformulation + co-development

Sustainability and certification gatekeepers

Certifiers and NGOs (RSPO, RTRS, deforestation-free initiatives) set what qualifies as acceptable supply, raising compliance costs and narrowing the supplier pool so certified producers gain pricing leverage; failure to meet standards can abruptly shift buying power to scarce certified sources. Cargill’s multi-year traceability investments have increased supplier access and reduced sourcing risk, supporting procurement flexibility in 2024.

- Certifier influence: shapes acceptability and premiums

- Compliance cost: reduces supplier pool, raises leverage

- Cargill traceability: expands access, lowers risk

Fragmented farms vs concentrated logistics and inputs create mixed power

Supplier power is mixed: fragmented farm supply (≈570M farms) limits individual leverage, but concentrated logistics (top-5 carriers ~80% capacity) and input suppliers (top-4 seeds 60–70%; top-3 enzymes ~60%) raise costs. Cargill scale (~$165B revenue in 2024) plus contracts, traceability and co-development lower vulnerability; fuel volatility (Brent ≈86 USD/bbl in 2024) can still shift power.

| Supplier | Concentration(2024) | Impact |

|---|---|---|

| Farms | Fragmented (~570M) | Low leverage |

| Ocean/Rail | Top-5 ~80% / Class I ~70% | High logistics power |

| Seeds/AgChem | Top-4 60–70% | Pricing pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Cargill that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform strategic and investment decisions.

One-sheet Porter's Five Forces for Cargill—instantly spot supply, buyer, and competitor pressures with a clean radar chart and customizable scores to guide strategic moves and reduce decision friction.

Customers Bargaining Power

Large multinational food manufacturers

Global CPGs and QSRs buy at scale and run competitive tenders that heighten price pressure, while insisting on consistent quality, service levels and sustainability credentials; multi-year contracts often trade margin for volume stability. Cargill, employing about 155,000 people in 2024, leverages product breadth and co-innovation to shift negotiations from pure price to value-added partnerships.

Commoditized product buyers

For commoditized grains, oils and basic ingredients switching costs are low and price transparency is high, letting buyers arbitrage among traders and origins; global grain trade remains large and liquid. Buyers push pricing down and agribusiness EBITDA margins are often slim, roughly 2–5% in 2024. Cargill offsets this with logistics reliability, hedging and risk-management services. Basis, freight and timing solutions can capture premiums despite thin unit margins.

Retailers and private label

Large retailers (top 3–4 chains controlling roughly 60% of grocery sales in key markets) exert strong negotiating power and impose strict compliance requirements. Private label growth, now about 20% of grocery sales in 2024, intensifies price sensitivity and margin pressure. Cargill differentiates through consistent supply, technical support and sustainability claims, but retailers demand OTIF >95%; missing on-time, in-full targets invites delisting pressure.

Animal producers and integrators

Large livestock and aquaculture integrators buy feed and premixes at scale and benchmark suppliers aggressively; in the US the top integrators account for over 50% of production, amplifying their negotiating leverage. Performance outcomes and strict biosecurity protocols create real switching frictions, while tailored formulations and on‑farm advisory services help Cargill retain high-volume accounts.

- Volume buyers: high purchase scale

- Benchmarking: aggressive price/performance comparison

- Switching frictions: biosecurity, performance risk

- Retention: tailored formulations, advisory services

Financial and risk management clients

Hedging and risk services buyers compare fees and analytics across banks and merchandisers, compressing margins. Sophisticated clients increasingly self-hedge, reducing pricing power for providers. Cargill reported about 174 billion dollars in 2023, so proprietary market insights and physical-derivatives integration create client stickiness. Regulatory compliance and credit terms, tightened post‑Basel III, drive negotiation leverage.

- Fee sensitivity: cross‑provider comparison

- Self‑hedging: lowers supplier pricing power

- Integration: physical+derivative analytics = retention

- Regulation/credit: key negotiation levers

Buyers squeeze prices as agribusiness margins tighten amid retail concentration

Buyers (global CPGs, QSRs, retailers, integrators) exert strong price and compliance pressure; Cargill (≈155,000 employees in 2024) shifts talks to value via breadth, co‑innovation and risk services. Commoditized grains/oils have low switching costs; agribusiness EBITDA margins ~2–5% in 2024, pushing basis/freight/timing premiums. Large retailers (top 3–4 ≈60% share) and private label (~20% of grocery sales in 2024) intensify margin pressure.

| Metric | 2024 |

|---|---|

| Employees | ≈155,000 |

| Agribusiness EBITDA | 2–5% |

| Retail concentration | Top3–4 ≈60% |

| Private label | ≈20% |

What You See Is What You Get

Cargill Porter's Five Forces Analysis

This Cargill Porter's Five Forces analysis delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Cargill’s agribusiness operations. The preview you see is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, no samples. It’s ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights Cargill's bargaining power dynamics, supplier and buyer pressures, threat of substitutes, and competitive rivalry across agribusiness and food ingredients. It outlines entry barriers and regulatory risks shaping profit margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cargill’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented farm suppliers

Most agricultural inputs come from roughly 570 million small and mid‑size farms globally (FAO), diluting individual supplier leverage for buyers like Cargill. Cargill’s scale and global sourcing across 70+ countries lets it shift purchases by region and crop, reducing supplier hold. Long‑term contracts and agronomic support build loyalty and stabilize prices, but extreme weather and local policy shocks can temporarily increase supplier power.

Concentrated inputs in logistics and energy

Port access, rail, barge, trucking and fuel are concentrated among a few providers—top five ocean carriers control roughly 80% of container capacity and Class I railroads account for about 70% of US freight ton-miles in 2024—boosting supplier bargaining power. Congestion and capacity limits have raised logistics costs and reduced scheduling flexibility, at times adding days to transit. Cargill offsets this via owned terminals, long-term contracts and multimodal routing. Geopolitical shocks and 2024 oil-price swings (Brent ~86 USD/bbl) can still shift leverage to suppliers.

Seed, fertilizer, and crop protection majors

Upstream seed and agrochemical supply is concentrated, with the top four firms controlling roughly 60–70% of global seed and crop protection markets, supporting firmer pricing; fertilizer prices surged over 200% in 2021–22, tightening farm margins and increasing Cargill’s origination costs via lower farmer liquidity; Cargill is not the primary buyer but is exposed through yields and farmer economics; advisory and precision-ag services can boost efficiency and yields by ~5–10%, partly offsetting input shocks.

Specialty ingredients and additives

Certain specialty enzymes, cultures and functional ingredients have few qualified suppliers, with the top 3 enzyme firms holding about 60% of the market in 2024, raising dependency and regulatory-driven switching costs; Cargill reported roughly $165 billion revenue in 2024, enabling reformulation across its portfolio to reduce exposure. Co-development agreements with suppliers shift bargaining power via shared IP and volume commitments.

- Concentration: top-3 ~60% (2024)

- Switching costs: high due to qualification/regulatory

- Cargill scale: ~$165B revenue (2024)

- Mitigation: reformulation + co-development

Sustainability and certification gatekeepers

Certifiers and NGOs (RSPO, RTRS, deforestation-free initiatives) set what qualifies as acceptable supply, raising compliance costs and narrowing the supplier pool so certified producers gain pricing leverage; failure to meet standards can abruptly shift buying power to scarce certified sources. Cargill’s multi-year traceability investments have increased supplier access and reduced sourcing risk, supporting procurement flexibility in 2024.

- Certifier influence: shapes acceptability and premiums

- Compliance cost: reduces supplier pool, raises leverage

- Cargill traceability: expands access, lowers risk

Fragmented farms vs concentrated logistics and inputs create mixed power

Supplier power is mixed: fragmented farm supply (≈570M farms) limits individual leverage, but concentrated logistics (top-5 carriers ~80% capacity) and input suppliers (top-4 seeds 60–70%; top-3 enzymes ~60%) raise costs. Cargill scale (~$165B revenue in 2024) plus contracts, traceability and co-development lower vulnerability; fuel volatility (Brent ≈86 USD/bbl in 2024) can still shift power.

| Supplier | Concentration(2024) | Impact |

|---|---|---|

| Farms | Fragmented (~570M) | Low leverage |

| Ocean/Rail | Top-5 ~80% / Class I ~70% | High logistics power |

| Seeds/AgChem | Top-4 60–70% | Pricing pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Cargill that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform strategic and investment decisions.

One-sheet Porter's Five Forces for Cargill—instantly spot supply, buyer, and competitor pressures with a clean radar chart and customizable scores to guide strategic moves and reduce decision friction.

Customers Bargaining Power

Large multinational food manufacturers

Global CPGs and QSRs buy at scale and run competitive tenders that heighten price pressure, while insisting on consistent quality, service levels and sustainability credentials; multi-year contracts often trade margin for volume stability. Cargill, employing about 155,000 people in 2024, leverages product breadth and co-innovation to shift negotiations from pure price to value-added partnerships.

Commoditized product buyers

For commoditized grains, oils and basic ingredients switching costs are low and price transparency is high, letting buyers arbitrage among traders and origins; global grain trade remains large and liquid. Buyers push pricing down and agribusiness EBITDA margins are often slim, roughly 2–5% in 2024. Cargill offsets this with logistics reliability, hedging and risk-management services. Basis, freight and timing solutions can capture premiums despite thin unit margins.

Retailers and private label

Large retailers (top 3–4 chains controlling roughly 60% of grocery sales in key markets) exert strong negotiating power and impose strict compliance requirements. Private label growth, now about 20% of grocery sales in 2024, intensifies price sensitivity and margin pressure. Cargill differentiates through consistent supply, technical support and sustainability claims, but retailers demand OTIF >95%; missing on-time, in-full targets invites delisting pressure.

Animal producers and integrators

Large livestock and aquaculture integrators buy feed and premixes at scale and benchmark suppliers aggressively; in the US the top integrators account for over 50% of production, amplifying their negotiating leverage. Performance outcomes and strict biosecurity protocols create real switching frictions, while tailored formulations and on‑farm advisory services help Cargill retain high-volume accounts.

- Volume buyers: high purchase scale

- Benchmarking: aggressive price/performance comparison

- Switching frictions: biosecurity, performance risk

- Retention: tailored formulations, advisory services

Financial and risk management clients

Hedging and risk services buyers compare fees and analytics across banks and merchandisers, compressing margins. Sophisticated clients increasingly self-hedge, reducing pricing power for providers. Cargill reported about 174 billion dollars in 2023, so proprietary market insights and physical-derivatives integration create client stickiness. Regulatory compliance and credit terms, tightened post‑Basel III, drive negotiation leverage.

- Fee sensitivity: cross‑provider comparison

- Self‑hedging: lowers supplier pricing power

- Integration: physical+derivative analytics = retention

- Regulation/credit: key negotiation levers

Buyers squeeze prices as agribusiness margins tighten amid retail concentration

Buyers (global CPGs, QSRs, retailers, integrators) exert strong price and compliance pressure; Cargill (≈155,000 employees in 2024) shifts talks to value via breadth, co‑innovation and risk services. Commoditized grains/oils have low switching costs; agribusiness EBITDA margins ~2–5% in 2024, pushing basis/freight/timing premiums. Large retailers (top 3–4 ≈60% share) and private label (~20% of grocery sales in 2024) intensify margin pressure.

| Metric | 2024 |

|---|---|

| Employees | ≈155,000 |

| Agribusiness EBITDA | 2–5% |

| Retail concentration | Top3–4 ≈60% |

| Private label | ≈20% |

What You See Is What You Get

Cargill Porter's Five Forces Analysis

This Cargill Porter's Five Forces analysis delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Cargill’s agribusiness operations. The preview you see is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, no samples. It’s ready for download and use the moment you buy.