Carrefour Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

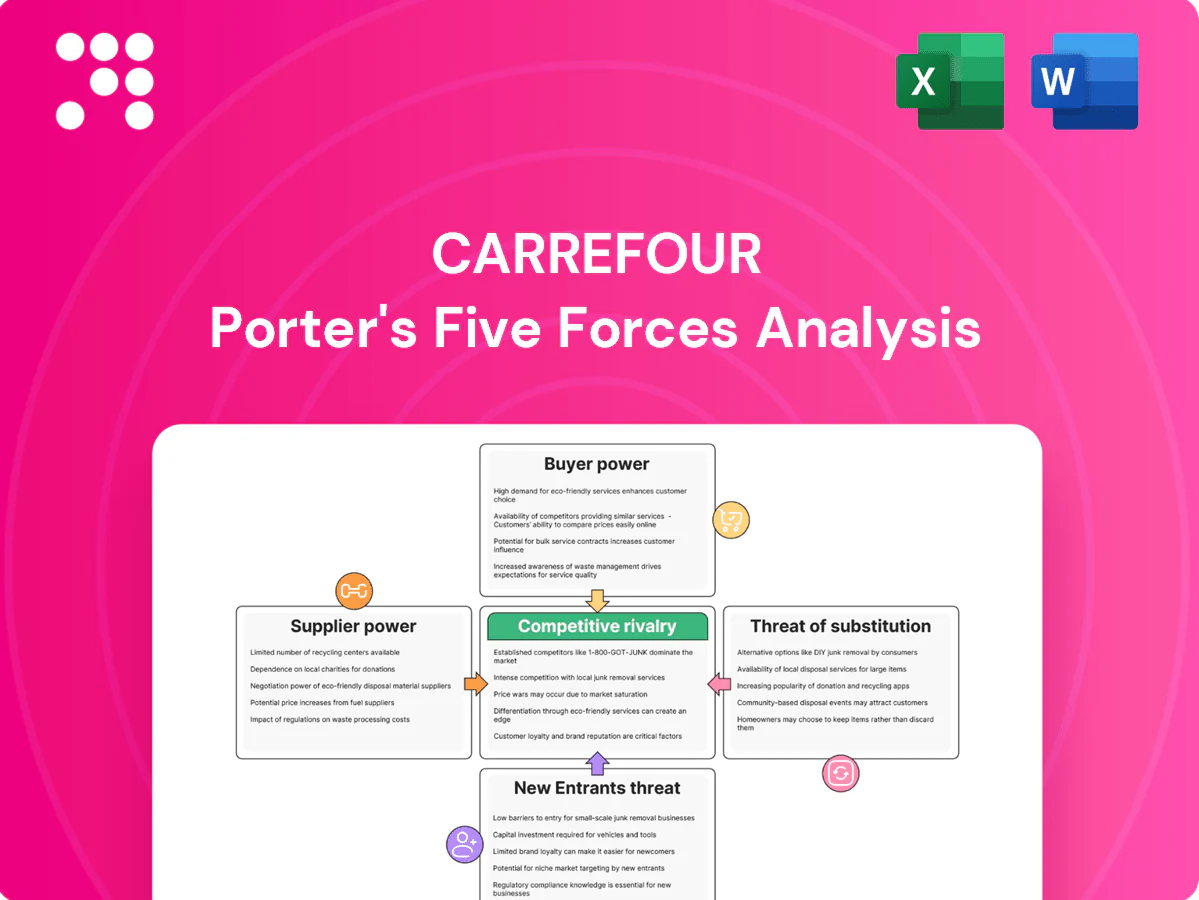

Carrefour faces intense competitive rivalry, strong buyer power in price-sensitive markets, moderate supplier influence for private-label growth, persistent threat from discount chains and e-commerce, and manageable barriers to entry in some regions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Carrefour’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse Sourcing Base

Carrefour sources from thousands of global, regional and local suppliers, diluting individual supplier leverage while supplying over 12,000 stores across roughly 30 countries (2024 footprint).

Wide category breadth — fresh, packaged and non‑food — enables rapid switching and mix optimization, with private labels representing about one‑third of sales (~33% in 2023–24), lowering dependence on branded vendors.

Specialty and premium niches, however, retain pricing power for select categories and limited‑volume suppliers.

Private Label Leverage

Strong private-label penetration—about one-third of Carrefour’s food and household sales in 2024—gives leverage to negotiate lower supplier prices and tougher terms. Carrefour can replace or benchmark national brands to pressure supplier margins and boost shelf share and differentiation. Quality assurance and supply continuity remain critical to avoid brand and sales risk.

Scale and Centralized Procurement

Carrefour’s international scale — operating over 10,000 stores worldwide (2024) — and participation in joint buying alliances strengthen bargaining, enabling better rebates and supplier terms. Centralized procurement standardizes contracts and reduces logistics costs, while volume commitments secure improved lead times and premium slotting. In smaller, fragmented markets this negotiating leverage is less pronounced, softening supplier pressure.

Supply Chain Constraints

- Commodity & ESG costs: 2024 rise pressured margins

- Agricultural seasonality: recurrent supply tightening

- OEM concentration: >60% assembly share

- Mitigants: multi-source + inventory buffers

Technology and Data Asymmetry

Carrefour leverages POS and demand-forecasting to strengthen negotiations, improving inventory turns relative to group sales of about €86.6bn in 2023; trade-spend optimization and category management align incentives with suppliers. EDI and vendor-managed inventory cut handling costs and shrinkage, while smaller, less digitized suppliers often accept stricter commercial terms to retain shelf space.

- Data-driven leverage

- Trade-spend alignment

- EDI/VMI efficiency

- Digital divide weakens small suppliers

Large retailer's scale and private labels limit supplier power amid commodity and OEM risks

Carrefour’s supplier power is limited by scale: ~12,000-store footprint (2024) and centralized buying that dilutes individual supplier leverage.

Private labels (~33% of sales 2023–24) and €86.6bn group sales (2023) strengthen Carrefour’s negotiating position.

Commodity/ESG cost rises and fresh-seasonality in 2024, plus >60% OEM assembly concentration, create pockets of supplier power.

Data-driven procurement, EDI/VMI and joint buying alliances offset shocks but power varies by category and market size.

| Metric | Value |

|---|---|

| Stores (2024) | ~12,000 |

| Private label | ~33% (2023–24) |

| Group sales (2023) | €86.6bn |

| OEM assembly share | >60% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry shaping Carrefour's profitability and strategic positioning. Highlights emerging threats (e‑commerce, discounters), supplier leverage, and customer bargaining to inform competitive responses and strategic planning.

A concise one-sheet Porter's Five Forces for Carrefour that visualizes competitive pressures with an editable spider chart—ideal for quick strategic decisions and pitch decks. No macros, fully customizable inputs let you model scenarios (new entrants, regulations) and drop into reports or Excel dashboards.

Customers Bargaining Power

Price Sensitivity

Consumers in groceries are highly price elastic, driving frequent switching and heavy response to promotions; Carrefour’s promotions and EDLP mix materially shape basket size and frequency. Loyalty benefits and targeted coupons lift retention while inflation—Euro area food inflation averaged about 3.2% in 2024 (Eurostat)—has accelerated trade-down to private labels. Carrefour must balance aggressive pricing to protect share with margin protection through assortment and private-label economics.

Multi-Channel Comparison

E-commerce and apps let shoppers compare prices and availability instantly; global e-commerce reached about 18% of retail sales in 2024 and smartphone penetration is ~85%, raising transparency. Click-and-collect and home delivery amplify comparison; Carrefour operates across 10 countries with broad omnichannel rollouts. Reviews and social signals shape preferences, making price matching and channel-consistent pricing essential.

Loyalty and Data Programs

Carrefour's loyalty program reported 21.3 million active members in 2024, with targeted offers and points raising switching costs and locking in frequency. Personalization can boost share of wallet by about 10% (McKinsey estimates), reducing buyer power through tailored promotions. However if perceived benefits erode customers churn quickly, and 74% of consumers in a 2024 survey said data privacy and trust are decisive for continued engagement.

Product Substitutability

High substitutability across brands and pack sizes gives customers leverage over Carrefour; private labels represented about 30% of Carrefour group food sales in 2024, offering lower‑cost alternatives and reducing price sensitivity. For premium or niche items (≈10% of assortment), buyers trade flexibility for brand/quality, so Carrefour’s assortment curation and quality assurance drive perceived value and margin protection.

- Substitutability: high

- Private label: ~30% of food sales (2024)

- Premium niche: ≈10% of assortment

- Value drivers: assortment curation, quality assurance

Service Expectations

- Delivery slots impact repeat purchases

- Returns speed affects NPS

- Stockouts increase churn

Customers' price power strong; p-label ~30%, e-comm ~18%

Customers hold strong bargaining power: price elasticity and promo sensitivity force frequent switching, with Euro area food inflation ~3.2% in 2024 accelerating private‑label uptake. Omnichannel transparency (global e‑commerce ~18% of retail, smartphone penetration ~85% in 2024) raises price comparison. Carrefour loyalty (21.3m members) and ~30% private‑label food sales blunt but do not eliminate buyer leverage.

| Metric | 2024 |

|---|---|

| Euro area food inflation | 3.2% |

| Carrefour active loyalty members | 21.3m |

| Private‑label food sales | ~30% |

| Global e‑commerce retail | ~18% |

Full Version Awaits

Carrefour Porter's Five Forces Analysis

This Carrefour Porter's Five Forces Analysis provides a detailed assessment of competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and strategic implications. This preview is the exact, fully formatted document you will receive immediately after purchase—no samples or placeholders. It’s ready for download and use the moment you buy.

A Must-Have Tool for Decision-Makers

Carrefour faces intense competitive rivalry, strong buyer power in price-sensitive markets, moderate supplier influence for private-label growth, persistent threat from discount chains and e-commerce, and manageable barriers to entry in some regions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Carrefour’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse Sourcing Base

Carrefour sources from thousands of global, regional and local suppliers, diluting individual supplier leverage while supplying over 12,000 stores across roughly 30 countries (2024 footprint).

Wide category breadth — fresh, packaged and non‑food — enables rapid switching and mix optimization, with private labels representing about one‑third of sales (~33% in 2023–24), lowering dependence on branded vendors.

Specialty and premium niches, however, retain pricing power for select categories and limited‑volume suppliers.

Private Label Leverage

Strong private-label penetration—about one-third of Carrefour’s food and household sales in 2024—gives leverage to negotiate lower supplier prices and tougher terms. Carrefour can replace or benchmark national brands to pressure supplier margins and boost shelf share and differentiation. Quality assurance and supply continuity remain critical to avoid brand and sales risk.

Scale and Centralized Procurement

Carrefour’s international scale — operating over 10,000 stores worldwide (2024) — and participation in joint buying alliances strengthen bargaining, enabling better rebates and supplier terms. Centralized procurement standardizes contracts and reduces logistics costs, while volume commitments secure improved lead times and premium slotting. In smaller, fragmented markets this negotiating leverage is less pronounced, softening supplier pressure.

Supply Chain Constraints

- Commodity & ESG costs: 2024 rise pressured margins

- Agricultural seasonality: recurrent supply tightening

- OEM concentration: >60% assembly share

- Mitigants: multi-source + inventory buffers

Technology and Data Asymmetry

Carrefour leverages POS and demand-forecasting to strengthen negotiations, improving inventory turns relative to group sales of about €86.6bn in 2023; trade-spend optimization and category management align incentives with suppliers. EDI and vendor-managed inventory cut handling costs and shrinkage, while smaller, less digitized suppliers often accept stricter commercial terms to retain shelf space.

- Data-driven leverage

- Trade-spend alignment

- EDI/VMI efficiency

- Digital divide weakens small suppliers

Large retailer's scale and private labels limit supplier power amid commodity and OEM risks

Carrefour’s supplier power is limited by scale: ~12,000-store footprint (2024) and centralized buying that dilutes individual supplier leverage.

Private labels (~33% of sales 2023–24) and €86.6bn group sales (2023) strengthen Carrefour’s negotiating position.

Commodity/ESG cost rises and fresh-seasonality in 2024, plus >60% OEM assembly concentration, create pockets of supplier power.

Data-driven procurement, EDI/VMI and joint buying alliances offset shocks but power varies by category and market size.

| Metric | Value |

|---|---|

| Stores (2024) | ~12,000 |

| Private label | ~33% (2023–24) |

| Group sales (2023) | €86.6bn |

| OEM assembly share | >60% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry shaping Carrefour's profitability and strategic positioning. Highlights emerging threats (e‑commerce, discounters), supplier leverage, and customer bargaining to inform competitive responses and strategic planning.

A concise one-sheet Porter's Five Forces for Carrefour that visualizes competitive pressures with an editable spider chart—ideal for quick strategic decisions and pitch decks. No macros, fully customizable inputs let you model scenarios (new entrants, regulations) and drop into reports or Excel dashboards.

Customers Bargaining Power

Price Sensitivity

Consumers in groceries are highly price elastic, driving frequent switching and heavy response to promotions; Carrefour’s promotions and EDLP mix materially shape basket size and frequency. Loyalty benefits and targeted coupons lift retention while inflation—Euro area food inflation averaged about 3.2% in 2024 (Eurostat)—has accelerated trade-down to private labels. Carrefour must balance aggressive pricing to protect share with margin protection through assortment and private-label economics.

Multi-Channel Comparison

E-commerce and apps let shoppers compare prices and availability instantly; global e-commerce reached about 18% of retail sales in 2024 and smartphone penetration is ~85%, raising transparency. Click-and-collect and home delivery amplify comparison; Carrefour operates across 10 countries with broad omnichannel rollouts. Reviews and social signals shape preferences, making price matching and channel-consistent pricing essential.

Loyalty and Data Programs

Carrefour's loyalty program reported 21.3 million active members in 2024, with targeted offers and points raising switching costs and locking in frequency. Personalization can boost share of wallet by about 10% (McKinsey estimates), reducing buyer power through tailored promotions. However if perceived benefits erode customers churn quickly, and 74% of consumers in a 2024 survey said data privacy and trust are decisive for continued engagement.

Product Substitutability

High substitutability across brands and pack sizes gives customers leverage over Carrefour; private labels represented about 30% of Carrefour group food sales in 2024, offering lower‑cost alternatives and reducing price sensitivity. For premium or niche items (≈10% of assortment), buyers trade flexibility for brand/quality, so Carrefour’s assortment curation and quality assurance drive perceived value and margin protection.

- Substitutability: high

- Private label: ~30% of food sales (2024)

- Premium niche: ≈10% of assortment

- Value drivers: assortment curation, quality assurance

Service Expectations

- Delivery slots impact repeat purchases

- Returns speed affects NPS

- Stockouts increase churn

Customers' price power strong; p-label ~30%, e-comm ~18%

Customers hold strong bargaining power: price elasticity and promo sensitivity force frequent switching, with Euro area food inflation ~3.2% in 2024 accelerating private‑label uptake. Omnichannel transparency (global e‑commerce ~18% of retail, smartphone penetration ~85% in 2024) raises price comparison. Carrefour loyalty (21.3m members) and ~30% private‑label food sales blunt but do not eliminate buyer leverage.

| Metric | 2024 |

|---|---|

| Euro area food inflation | 3.2% |

| Carrefour active loyalty members | 21.3m |

| Private‑label food sales | ~30% |

| Global e‑commerce retail | ~18% |

Full Version Awaits

Carrefour Porter's Five Forces Analysis

This Carrefour Porter's Five Forces Analysis provides a detailed assessment of competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and strategic implications. This preview is the exact, fully formatted document you will receive immediately after purchase—no samples or placeholders. It’s ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Carrefour faces intense competitive rivalry, strong buyer power in price-sensitive markets, moderate supplier influence for private-label growth, persistent threat from discount chains and e-commerce, and manageable barriers to entry in some regions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Carrefour’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse Sourcing Base

Carrefour sources from thousands of global, regional and local suppliers, diluting individual supplier leverage while supplying over 12,000 stores across roughly 30 countries (2024 footprint).

Wide category breadth — fresh, packaged and non‑food — enables rapid switching and mix optimization, with private labels representing about one‑third of sales (~33% in 2023–24), lowering dependence on branded vendors.

Specialty and premium niches, however, retain pricing power for select categories and limited‑volume suppliers.

Private Label Leverage

Strong private-label penetration—about one-third of Carrefour’s food and household sales in 2024—gives leverage to negotiate lower supplier prices and tougher terms. Carrefour can replace or benchmark national brands to pressure supplier margins and boost shelf share and differentiation. Quality assurance and supply continuity remain critical to avoid brand and sales risk.

Scale and Centralized Procurement

Carrefour’s international scale — operating over 10,000 stores worldwide (2024) — and participation in joint buying alliances strengthen bargaining, enabling better rebates and supplier terms. Centralized procurement standardizes contracts and reduces logistics costs, while volume commitments secure improved lead times and premium slotting. In smaller, fragmented markets this negotiating leverage is less pronounced, softening supplier pressure.

Supply Chain Constraints

- Commodity & ESG costs: 2024 rise pressured margins

- Agricultural seasonality: recurrent supply tightening

- OEM concentration: >60% assembly share

- Mitigants: multi-source + inventory buffers

Technology and Data Asymmetry

Carrefour leverages POS and demand-forecasting to strengthen negotiations, improving inventory turns relative to group sales of about €86.6bn in 2023; trade-spend optimization and category management align incentives with suppliers. EDI and vendor-managed inventory cut handling costs and shrinkage, while smaller, less digitized suppliers often accept stricter commercial terms to retain shelf space.

- Data-driven leverage

- Trade-spend alignment

- EDI/VMI efficiency

- Digital divide weakens small suppliers

Large retailer's scale and private labels limit supplier power amid commodity and OEM risks

Carrefour’s supplier power is limited by scale: ~12,000-store footprint (2024) and centralized buying that dilutes individual supplier leverage.

Private labels (~33% of sales 2023–24) and €86.6bn group sales (2023) strengthen Carrefour’s negotiating position.

Commodity/ESG cost rises and fresh-seasonality in 2024, plus >60% OEM assembly concentration, create pockets of supplier power.

Data-driven procurement, EDI/VMI and joint buying alliances offset shocks but power varies by category and market size.

| Metric | Value |

|---|---|

| Stores (2024) | ~12,000 |

| Private label | ~33% (2023–24) |

| Group sales (2023) | €86.6bn |

| OEM assembly share | >60% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry shaping Carrefour's profitability and strategic positioning. Highlights emerging threats (e‑commerce, discounters), supplier leverage, and customer bargaining to inform competitive responses and strategic planning.

A concise one-sheet Porter's Five Forces for Carrefour that visualizes competitive pressures with an editable spider chart—ideal for quick strategic decisions and pitch decks. No macros, fully customizable inputs let you model scenarios (new entrants, regulations) and drop into reports or Excel dashboards.

Customers Bargaining Power

Price Sensitivity

Consumers in groceries are highly price elastic, driving frequent switching and heavy response to promotions; Carrefour’s promotions and EDLP mix materially shape basket size and frequency. Loyalty benefits and targeted coupons lift retention while inflation—Euro area food inflation averaged about 3.2% in 2024 (Eurostat)—has accelerated trade-down to private labels. Carrefour must balance aggressive pricing to protect share with margin protection through assortment and private-label economics.

Multi-Channel Comparison

E-commerce and apps let shoppers compare prices and availability instantly; global e-commerce reached about 18% of retail sales in 2024 and smartphone penetration is ~85%, raising transparency. Click-and-collect and home delivery amplify comparison; Carrefour operates across 10 countries with broad omnichannel rollouts. Reviews and social signals shape preferences, making price matching and channel-consistent pricing essential.

Loyalty and Data Programs

Carrefour's loyalty program reported 21.3 million active members in 2024, with targeted offers and points raising switching costs and locking in frequency. Personalization can boost share of wallet by about 10% (McKinsey estimates), reducing buyer power through tailored promotions. However if perceived benefits erode customers churn quickly, and 74% of consumers in a 2024 survey said data privacy and trust are decisive for continued engagement.

Product Substitutability

High substitutability across brands and pack sizes gives customers leverage over Carrefour; private labels represented about 30% of Carrefour group food sales in 2024, offering lower‑cost alternatives and reducing price sensitivity. For premium or niche items (≈10% of assortment), buyers trade flexibility for brand/quality, so Carrefour’s assortment curation and quality assurance drive perceived value and margin protection.

- Substitutability: high

- Private label: ~30% of food sales (2024)

- Premium niche: ≈10% of assortment

- Value drivers: assortment curation, quality assurance

Service Expectations

- Delivery slots impact repeat purchases

- Returns speed affects NPS

- Stockouts increase churn

Customers' price power strong; p-label ~30%, e-comm ~18%

Customers hold strong bargaining power: price elasticity and promo sensitivity force frequent switching, with Euro area food inflation ~3.2% in 2024 accelerating private‑label uptake. Omnichannel transparency (global e‑commerce ~18% of retail, smartphone penetration ~85% in 2024) raises price comparison. Carrefour loyalty (21.3m members) and ~30% private‑label food sales blunt but do not eliminate buyer leverage.

| Metric | 2024 |

|---|---|

| Euro area food inflation | 3.2% |

| Carrefour active loyalty members | 21.3m |

| Private‑label food sales | ~30% |

| Global e‑commerce retail | ~18% |

Full Version Awaits

Carrefour Porter's Five Forces Analysis

This Carrefour Porter's Five Forces Analysis provides a detailed assessment of competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and strategic implications. This preview is the exact, fully formatted document you will receive immediately after purchase—no samples or placeholders. It’s ready for download and use the moment you buy.