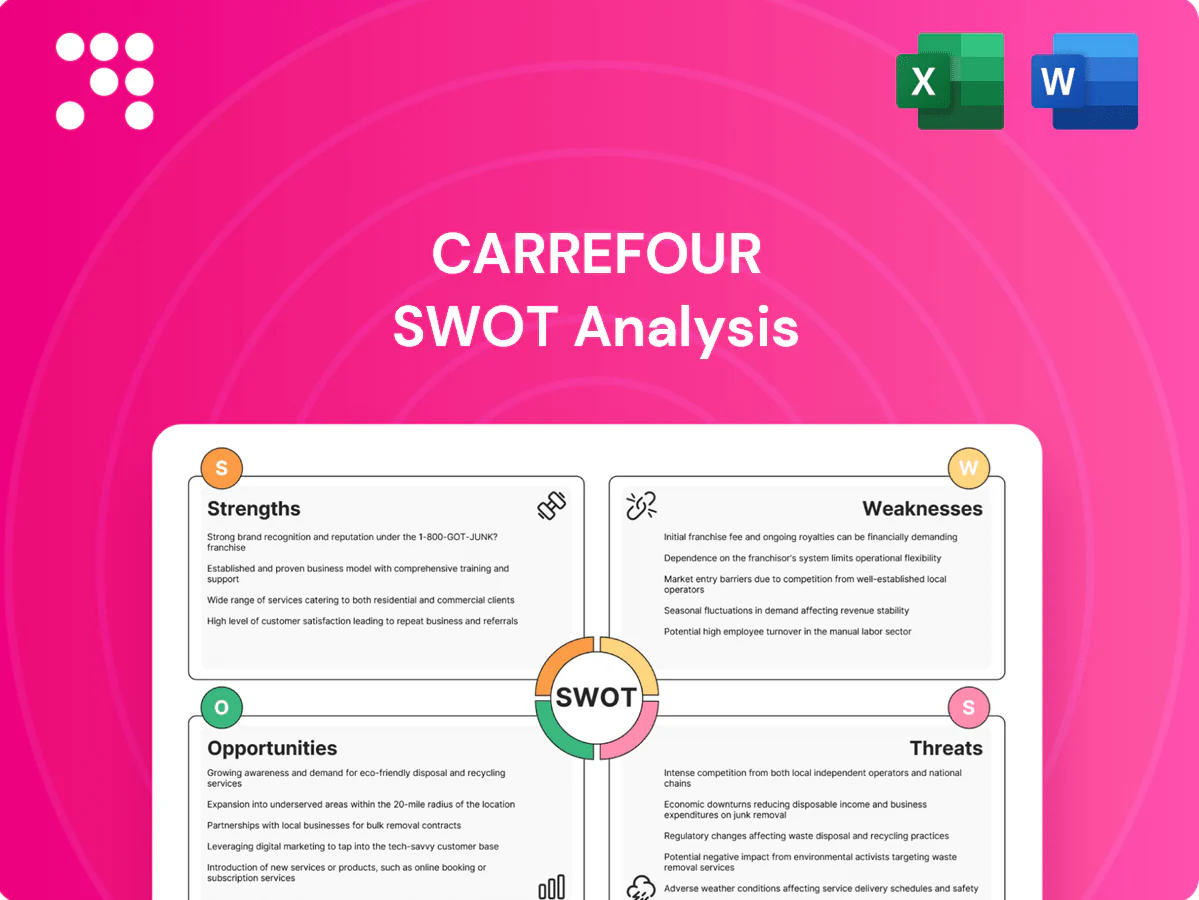

Carrefour SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Carrefour's global scale, omni‑channel presence and strong private labels underpin resilience, but margins face pressure from fierce competition and supply‑chain costs. Opportunities in digital expansion and emerging markets contrast with regulatory and sustainability risks. Purchase the full SWOT for a detailed, editable report with financial context and actionable strategic recommendations.

Strengths

Global footprint

Operating in more than 30 countries and generating €86.2bn in group sales in 2023, Carrefour’s global footprint provides scale and diversified revenue streams. The group leverages cross‑regional sourcing and best practices to lower costs and broaden assortment. Broad presence reduces reliance on any single economy and boosts bargaining power with suppliers, supporting margin resilience and procurement leverage.

Multi-format portfolio

Hypermarkets, supermarkets, convenience and cash-and-carry formats let Carrefour meet varied missions and price points, capturing both value and premium shoppers. Format flexibility optimizes urban, suburban and wholesale demand and supports weekly, top-up and bulk shopping patterns. This mix bolsters resilience through cycles; Carrefour operated over 12,000 stores in 30+ countries as of 2024.

Private label strength

Carrefour’s strong private-label portfolio boosts price perception and improves margin mix, with private brands accounting for around 25–30% of food sales in recent group disclosures (2023–24), delivering higher gross margins than national brands. Control over quality and sourcing reduces cost variability and strengthens supply resilience. Exclusive ranges deepen loyalty by driving repeat visits and differentiate Carrefour versus competitors. Private labels also increase negotiating leverage with national suppliers.

Omnichannel and e-commerce

Carrefour's omnichannel and e-commerce strategy—online grocery, marketplace tie-ins and click-and-collect—expand reach and basket size; e-commerce sales reached ~€7.0bn in 2023 and the marketplace had 5,000+ sellers by 2024. Digital platforms enable personalization and real-time inventory visibility, reducing friction between discovery and fulfillment and supporting varied last-mile options.

- Online grocery boosts basket size

- Marketplace +5,000 sellers (2024)

- Click-and-collect widens reach

- Real-time inventory & personalization

- Flexible last-mile options

Financial services ecosystem

Carrefour's integrated financial services—loyalty cards, Carrefour Pay, and consumer credit—boost customer stickiness, enable embedded offers and checkout credit to raise conversion, and generate ancillary revenue while producing rich transaction data for personalization; Carrefour reported c.20 million loyalty members and growing fintech usage across 2024–2025.

- Customer retention

- Ancillary revenue

- Data-driven insights

- Higher conversion via embedded credit

- Supports retail traffic & frequency

Scale & omnichannel: 12,000+ stores, ≈€7bn e-commerce, ≈20m members

Carrefour’s scale (€86.2bn sales 2023) and 12,000+ stores across 30+ countries diversify revenue and enhance supplier leverage. Multi-format network and 25–30% private‑label food mix improve margins and customer reach. Omnichannel strength (≈€7.0bn e‑commerce 2023, 5,000+ marketplace sellers) and ~20m loyalty members drive basket size and retention.

| Metric | Value |

|---|---|

| Group sales (2023) | €86.2bn |

| Stores (2024) | 12,000+ |

| E‑commerce (2023) | ≈€7.0bn |

| Private‑label share | 25–30% |

| Loyalty members | ≈20m |

What is included in the product

Provides a concise SWOT overview of Carrefour, highlighting its operational strengths, cost and scale advantages, key weaknesses like thin margins and digital transition needs, market opportunities in e‑commerce and emerging markets, and threats from intense competition and supply‑chain volatility.

Provides a concise Carrefour SWOT matrix for rapid strategic alignment across retail operations, streamlining stakeholder briefings and executive decision-making.

Weaknesses

Thin margins

Grocery retail economics limit Carrefour’s profitability headroom: supermarkets typically show gross margins around 20–25% but net margins compress to roughly 1–3% (European food retail median ~2% in 2024). Intense price competition and promotions drive gross-margin erosion, while cost inflation (energy, labor) in 2024 rose faster than Carrefour’s pricing power. That margin squeeze constrains capex and M&A unless offset by efficiency gains.

Operational complexity

Carrefour’s presence across c.12,200 stores in about 30 countries and roughly 320,000 employees creates supply-chain and governance complexity; differing assortments, pricing and compliance regimes per market raise overhead and execution risk, contributing to slower decision-making and reduced agility.

Exposure to mature markets

Carrefour's heavy footprint in roughly 30 countries and a revenue mix concentrated in mature European markets limits expansion, with comparable store growth typically in low single digits; demographics and market saturation constrain like-for-like upside. Consumer spending is cyclical and proved sensitive during the 2022–23 inflation spike, pressuring margins. Continuous reinvention—omnichannel, price competitiveness and private labels—is required to defend share.

Labor-intensive model

Carrefour's large store network—about 12,200 stores and over 320,000 employees at end-2023—requires substantial staffing, boosting operating costs. Wage inflation and collective bargaining in core markets like France pressure margins. Scheduling complexity and retention raise operational friction, while periodic industrial actions have caused store disruptions.

- High headcount: ~320,000 employees (2023)

- Extensive footprint: ~12,200 stores

- Wage/union pressure reducing margin

- Scheduling/retention operational friction

Legacy IT and supply rigidity

Older legacy IT stacks limit real-time analytics and automation across Carrefour’s ~13,000 stores in 30+ countries, constraining quick inventory and pricing decisions; integration across banners and geographies remains complex despite the Carrefour 2026 transformation plan (launched 2021). Supply chain modernization needs sustained capex and slow upgrades risk omnichannel service gaps and lost e‑commerce momentum.

- Legacy IT: impedes real-time analytics

- Integration: cross-banner/geography complexity

- Capex: modernization requires sustained investment

- Omnichannel: slow upgrades risk service gaps

Slim margins and high costs squeeze profitability; legacy IT slows omnichannel growth

Low net margins (~1–3%; European food retail median 2% in 2024) and promo/energy/wage inflation squeeze profitability; large footprint (~12,200 stores; ~320,000 employees) increases overhead, governance and labor/union risk; legacy IT and required capex slow omnichannel scaling and real‑time pricing/inventory responsiveness.

| Metric | Value |

|---|---|

| Stores (end‑2023) | ~12,200 |

| Employees (2023) | ~320,000 |

| Net margin (typical) | ~1–3% |

| EU retail median (2024) | ~2% |

Full Version Awaits

Carrefour SWOT Analysis

This is the actual Carrefour SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, showing strengths, weaknesses, opportunities and threats in concise, actionable format. Buy to unlock the complete, editable version for immediate download.

Make Insightful Decisions Backed by Expert Research

Carrefour's global scale, omni‑channel presence and strong private labels underpin resilience, but margins face pressure from fierce competition and supply‑chain costs. Opportunities in digital expansion and emerging markets contrast with regulatory and sustainability risks. Purchase the full SWOT for a detailed, editable report with financial context and actionable strategic recommendations.

Strengths

Global footprint

Operating in more than 30 countries and generating €86.2bn in group sales in 2023, Carrefour’s global footprint provides scale and diversified revenue streams. The group leverages cross‑regional sourcing and best practices to lower costs and broaden assortment. Broad presence reduces reliance on any single economy and boosts bargaining power with suppliers, supporting margin resilience and procurement leverage.

Multi-format portfolio

Hypermarkets, supermarkets, convenience and cash-and-carry formats let Carrefour meet varied missions and price points, capturing both value and premium shoppers. Format flexibility optimizes urban, suburban and wholesale demand and supports weekly, top-up and bulk shopping patterns. This mix bolsters resilience through cycles; Carrefour operated over 12,000 stores in 30+ countries as of 2024.

Private label strength

Carrefour’s strong private-label portfolio boosts price perception and improves margin mix, with private brands accounting for around 25–30% of food sales in recent group disclosures (2023–24), delivering higher gross margins than national brands. Control over quality and sourcing reduces cost variability and strengthens supply resilience. Exclusive ranges deepen loyalty by driving repeat visits and differentiate Carrefour versus competitors. Private labels also increase negotiating leverage with national suppliers.

Omnichannel and e-commerce

Carrefour's omnichannel and e-commerce strategy—online grocery, marketplace tie-ins and click-and-collect—expand reach and basket size; e-commerce sales reached ~€7.0bn in 2023 and the marketplace had 5,000+ sellers by 2024. Digital platforms enable personalization and real-time inventory visibility, reducing friction between discovery and fulfillment and supporting varied last-mile options.

- Online grocery boosts basket size

- Marketplace +5,000 sellers (2024)

- Click-and-collect widens reach

- Real-time inventory & personalization

- Flexible last-mile options

Financial services ecosystem

Carrefour's integrated financial services—loyalty cards, Carrefour Pay, and consumer credit—boost customer stickiness, enable embedded offers and checkout credit to raise conversion, and generate ancillary revenue while producing rich transaction data for personalization; Carrefour reported c.20 million loyalty members and growing fintech usage across 2024–2025.

- Customer retention

- Ancillary revenue

- Data-driven insights

- Higher conversion via embedded credit

- Supports retail traffic & frequency

Scale & omnichannel: 12,000+ stores, ≈€7bn e-commerce, ≈20m members

Carrefour’s scale (€86.2bn sales 2023) and 12,000+ stores across 30+ countries diversify revenue and enhance supplier leverage. Multi-format network and 25–30% private‑label food mix improve margins and customer reach. Omnichannel strength (≈€7.0bn e‑commerce 2023, 5,000+ marketplace sellers) and ~20m loyalty members drive basket size and retention.

| Metric | Value |

|---|---|

| Group sales (2023) | €86.2bn |

| Stores (2024) | 12,000+ |

| E‑commerce (2023) | ≈€7.0bn |

| Private‑label share | 25–30% |

| Loyalty members | ≈20m |

What is included in the product

Provides a concise SWOT overview of Carrefour, highlighting its operational strengths, cost and scale advantages, key weaknesses like thin margins and digital transition needs, market opportunities in e‑commerce and emerging markets, and threats from intense competition and supply‑chain volatility.

Provides a concise Carrefour SWOT matrix for rapid strategic alignment across retail operations, streamlining stakeholder briefings and executive decision-making.

Weaknesses

Thin margins

Grocery retail economics limit Carrefour’s profitability headroom: supermarkets typically show gross margins around 20–25% but net margins compress to roughly 1–3% (European food retail median ~2% in 2024). Intense price competition and promotions drive gross-margin erosion, while cost inflation (energy, labor) in 2024 rose faster than Carrefour’s pricing power. That margin squeeze constrains capex and M&A unless offset by efficiency gains.

Operational complexity

Carrefour’s presence across c.12,200 stores in about 30 countries and roughly 320,000 employees creates supply-chain and governance complexity; differing assortments, pricing and compliance regimes per market raise overhead and execution risk, contributing to slower decision-making and reduced agility.

Exposure to mature markets

Carrefour's heavy footprint in roughly 30 countries and a revenue mix concentrated in mature European markets limits expansion, with comparable store growth typically in low single digits; demographics and market saturation constrain like-for-like upside. Consumer spending is cyclical and proved sensitive during the 2022–23 inflation spike, pressuring margins. Continuous reinvention—omnichannel, price competitiveness and private labels—is required to defend share.

Labor-intensive model

Carrefour's large store network—about 12,200 stores and over 320,000 employees at end-2023—requires substantial staffing, boosting operating costs. Wage inflation and collective bargaining in core markets like France pressure margins. Scheduling complexity and retention raise operational friction, while periodic industrial actions have caused store disruptions.

- High headcount: ~320,000 employees (2023)

- Extensive footprint: ~12,200 stores

- Wage/union pressure reducing margin

- Scheduling/retention operational friction

Legacy IT and supply rigidity

Older legacy IT stacks limit real-time analytics and automation across Carrefour’s ~13,000 stores in 30+ countries, constraining quick inventory and pricing decisions; integration across banners and geographies remains complex despite the Carrefour 2026 transformation plan (launched 2021). Supply chain modernization needs sustained capex and slow upgrades risk omnichannel service gaps and lost e‑commerce momentum.

- Legacy IT: impedes real-time analytics

- Integration: cross-banner/geography complexity

- Capex: modernization requires sustained investment

- Omnichannel: slow upgrades risk service gaps

Slim margins and high costs squeeze profitability; legacy IT slows omnichannel growth

Low net margins (~1–3%; European food retail median 2% in 2024) and promo/energy/wage inflation squeeze profitability; large footprint (~12,200 stores; ~320,000 employees) increases overhead, governance and labor/union risk; legacy IT and required capex slow omnichannel scaling and real‑time pricing/inventory responsiveness.

| Metric | Value |

|---|---|

| Stores (end‑2023) | ~12,200 |

| Employees (2023) | ~320,000 |

| Net margin (typical) | ~1–3% |

| EU retail median (2024) | ~2% |

Full Version Awaits

Carrefour SWOT Analysis

This is the actual Carrefour SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, showing strengths, weaknesses, opportunities and threats in concise, actionable format. Buy to unlock the complete, editable version for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Carrefour's global scale, omni‑channel presence and strong private labels underpin resilience, but margins face pressure from fierce competition and supply‑chain costs. Opportunities in digital expansion and emerging markets contrast with regulatory and sustainability risks. Purchase the full SWOT for a detailed, editable report with financial context and actionable strategic recommendations.

Strengths

Global footprint

Operating in more than 30 countries and generating €86.2bn in group sales in 2023, Carrefour’s global footprint provides scale and diversified revenue streams. The group leverages cross‑regional sourcing and best practices to lower costs and broaden assortment. Broad presence reduces reliance on any single economy and boosts bargaining power with suppliers, supporting margin resilience and procurement leverage.

Multi-format portfolio

Hypermarkets, supermarkets, convenience and cash-and-carry formats let Carrefour meet varied missions and price points, capturing both value and premium shoppers. Format flexibility optimizes urban, suburban and wholesale demand and supports weekly, top-up and bulk shopping patterns. This mix bolsters resilience through cycles; Carrefour operated over 12,000 stores in 30+ countries as of 2024.

Private label strength

Carrefour’s strong private-label portfolio boosts price perception and improves margin mix, with private brands accounting for around 25–30% of food sales in recent group disclosures (2023–24), delivering higher gross margins than national brands. Control over quality and sourcing reduces cost variability and strengthens supply resilience. Exclusive ranges deepen loyalty by driving repeat visits and differentiate Carrefour versus competitors. Private labels also increase negotiating leverage with national suppliers.

Omnichannel and e-commerce

Carrefour's omnichannel and e-commerce strategy—online grocery, marketplace tie-ins and click-and-collect—expand reach and basket size; e-commerce sales reached ~€7.0bn in 2023 and the marketplace had 5,000+ sellers by 2024. Digital platforms enable personalization and real-time inventory visibility, reducing friction between discovery and fulfillment and supporting varied last-mile options.

- Online grocery boosts basket size

- Marketplace +5,000 sellers (2024)

- Click-and-collect widens reach

- Real-time inventory & personalization

- Flexible last-mile options

Financial services ecosystem

Carrefour's integrated financial services—loyalty cards, Carrefour Pay, and consumer credit—boost customer stickiness, enable embedded offers and checkout credit to raise conversion, and generate ancillary revenue while producing rich transaction data for personalization; Carrefour reported c.20 million loyalty members and growing fintech usage across 2024–2025.

- Customer retention

- Ancillary revenue

- Data-driven insights

- Higher conversion via embedded credit

- Supports retail traffic & frequency

Scale & omnichannel: 12,000+ stores, ≈€7bn e-commerce, ≈20m members

Carrefour’s scale (€86.2bn sales 2023) and 12,000+ stores across 30+ countries diversify revenue and enhance supplier leverage. Multi-format network and 25–30% private‑label food mix improve margins and customer reach. Omnichannel strength (≈€7.0bn e‑commerce 2023, 5,000+ marketplace sellers) and ~20m loyalty members drive basket size and retention.

| Metric | Value |

|---|---|

| Group sales (2023) | €86.2bn |

| Stores (2024) | 12,000+ |

| E‑commerce (2023) | ≈€7.0bn |

| Private‑label share | 25–30% |

| Loyalty members | ≈20m |

What is included in the product

Provides a concise SWOT overview of Carrefour, highlighting its operational strengths, cost and scale advantages, key weaknesses like thin margins and digital transition needs, market opportunities in e‑commerce and emerging markets, and threats from intense competition and supply‑chain volatility.

Provides a concise Carrefour SWOT matrix for rapid strategic alignment across retail operations, streamlining stakeholder briefings and executive decision-making.

Weaknesses

Thin margins

Grocery retail economics limit Carrefour’s profitability headroom: supermarkets typically show gross margins around 20–25% but net margins compress to roughly 1–3% (European food retail median ~2% in 2024). Intense price competition and promotions drive gross-margin erosion, while cost inflation (energy, labor) in 2024 rose faster than Carrefour’s pricing power. That margin squeeze constrains capex and M&A unless offset by efficiency gains.

Operational complexity

Carrefour’s presence across c.12,200 stores in about 30 countries and roughly 320,000 employees creates supply-chain and governance complexity; differing assortments, pricing and compliance regimes per market raise overhead and execution risk, contributing to slower decision-making and reduced agility.

Exposure to mature markets

Carrefour's heavy footprint in roughly 30 countries and a revenue mix concentrated in mature European markets limits expansion, with comparable store growth typically in low single digits; demographics and market saturation constrain like-for-like upside. Consumer spending is cyclical and proved sensitive during the 2022–23 inflation spike, pressuring margins. Continuous reinvention—omnichannel, price competitiveness and private labels—is required to defend share.

Labor-intensive model

Carrefour's large store network—about 12,200 stores and over 320,000 employees at end-2023—requires substantial staffing, boosting operating costs. Wage inflation and collective bargaining in core markets like France pressure margins. Scheduling complexity and retention raise operational friction, while periodic industrial actions have caused store disruptions.

- High headcount: ~320,000 employees (2023)

- Extensive footprint: ~12,200 stores

- Wage/union pressure reducing margin

- Scheduling/retention operational friction

Legacy IT and supply rigidity

Older legacy IT stacks limit real-time analytics and automation across Carrefour’s ~13,000 stores in 30+ countries, constraining quick inventory and pricing decisions; integration across banners and geographies remains complex despite the Carrefour 2026 transformation plan (launched 2021). Supply chain modernization needs sustained capex and slow upgrades risk omnichannel service gaps and lost e‑commerce momentum.

- Legacy IT: impedes real-time analytics

- Integration: cross-banner/geography complexity

- Capex: modernization requires sustained investment

- Omnichannel: slow upgrades risk service gaps

Slim margins and high costs squeeze profitability; legacy IT slows omnichannel growth

Low net margins (~1–3%; European food retail median 2% in 2024) and promo/energy/wage inflation squeeze profitability; large footprint (~12,200 stores; ~320,000 employees) increases overhead, governance and labor/union risk; legacy IT and required capex slow omnichannel scaling and real‑time pricing/inventory responsiveness.

| Metric | Value |

|---|---|

| Stores (end‑2023) | ~12,200 |

| Employees (2023) | ~320,000 |

| Net margin (typical) | ~1–3% |

| EU retail median (2024) | ~2% |

Full Version Awaits

Carrefour SWOT Analysis

This is the actual Carrefour SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, showing strengths, weaknesses, opportunities and threats in concise, actionable format. Buy to unlock the complete, editable version for immediate download.