Carrier Global Porter's Five Forces Analysis

From Overview to Strategy Blueprint

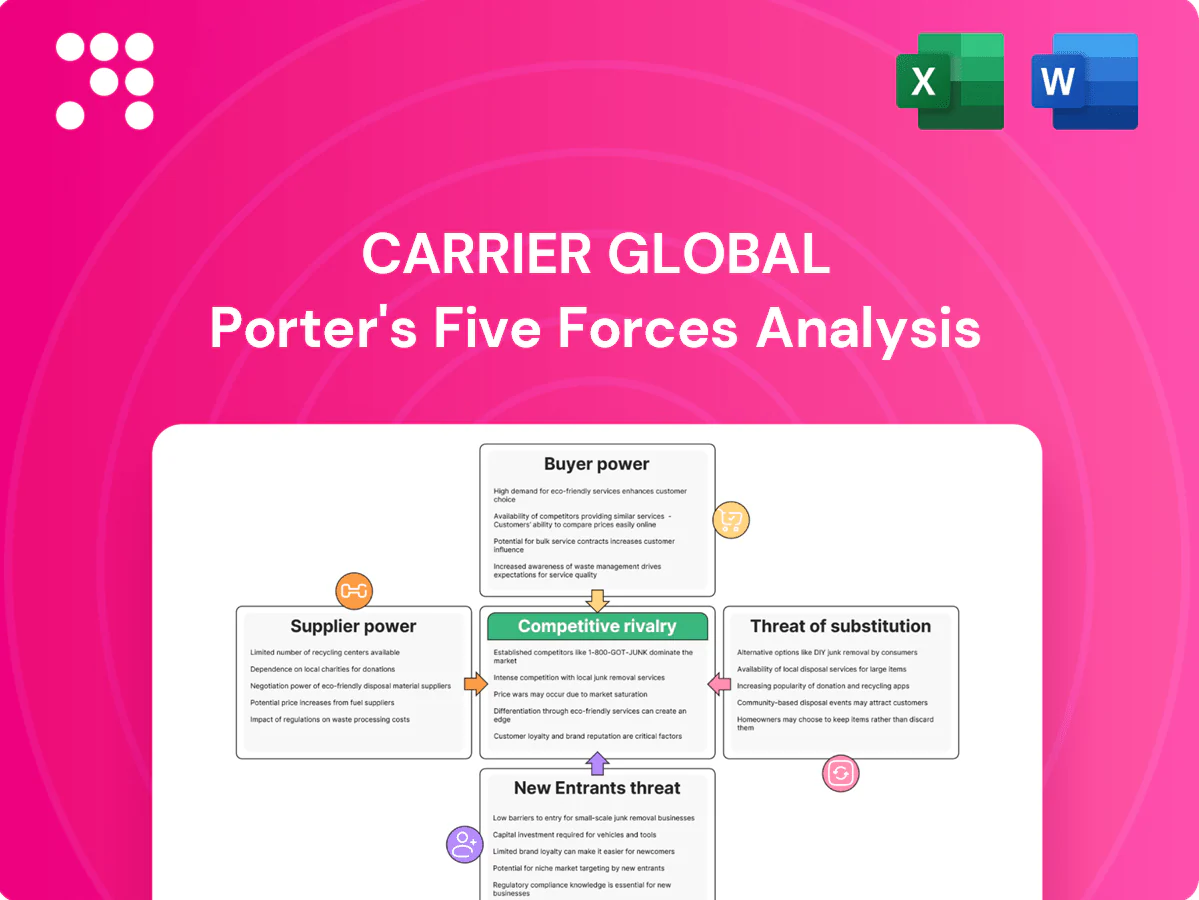

Carrier Global faces moderate buyer power, rising substitution pressures from integrated building systems, and steady supplier leverage—while scale and regulatory barriers curb new entrants. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy recommendations tailored to Carrier Global.

Suppliers Bargaining Power

Critical components concentration

Carrier depends on specialized suppliers for compressors, controls, sensors and semiconductors that are not perfectly substitutable, and limited qualified sources for variable-speed compressors and advanced electronics increase supplier leverage. Long qualification cycles driven by safety and reliability requirements extend lead times. In tight markets this concentration can push up pricing and delay deliveries, squeezing margins and inventory planning.

Refrigerant transition dynamics

Regulatory shifts to low-GWP refrigerants concentrate supply with a few producers—Chemours, Honeywell and several Chinese players dominate R-32/R-454B capacity by 2024—tightening terms and lead times. Suppliers of R-32/R-454B and compressors can influence availability during changeovers. Carrier must retool and co-develop designs, raising switching costs. Short-term scarcity can amplify supplier power despite expected long-term normalization.

Metals and energy cost pass-through

Steel (HRC ≈ $840/ton in 2024), copper (~$9,500/ton) and aluminum (~$2,300/ton) remained volatile in 2024 and are often passed through by upstream suppliers; hedges and contractual pricing help but timing mismatches can compress margins. Energy (Brent ≈ $80/bbl) and freight spikes also feed into component prices. Carrier’s scale (2024 revenue ≈ $21.8B) moderates but cannot eliminate these pressures.

Global logistics and risk concentration

Globalized supply chains expose Carrier to port congestion, geopolitics, and export controls; Carrier’s 2024 filings explicitly list logistics disruptions as a principal risk. Single-region supplier dependencies can magnify stoppages and boost supplier bargaining leverage. Dual-sourcing and localization lower probability of supply failure but do not eliminate systemic risks. Suppliers that maintained resilient multi-region footprints in 2024 secured stronger negotiating positions.

- High-risk: port congestion & export controls

- Concentration: single-region dependency raises leverage

- Mitigation: dual-sourcing/localization reduces but not removes risk

- Advantage: resilient suppliers gain pricing power (2024 observation)

Scale and partnership counterweights

Scale and partnership counterweights: Carrier’s purchasing scale (2024 revenue about $21B) and engineering co-development with key suppliers, plus multi-year supply agreements, reduce supplier bargaining power; joint development creates mutual dependency and priority allocation during shortages, while alternate qualification programs provide a credible switching threat.

- Purchasing scale: lowers costs

- Joint R&D: mutual dependency

- Long-term contracts: priority in shortages

- Alternate qualification: switching leverage

- IP/tooling lock-in: residual vendor power

Moderate-to-high supplier power: concentrated refrigerants, volatile metals, long qual cycles

Carrier faces moderate-to-high supplier power in 2024 due to specialized compressors/electronics, concentrated low-GWP refrigerant supply (Chemours, Honeywell dominant), and volatile metals/energy costs despite scale (2024 revenue ≈ $21.8B). Long qual cycles and logistics/port risks raise switching costs; dual-sourcing and long-term contracts partially mitigate.

| Item | 2024 | Impact |

|---|---|---|

| Revenue | $21.8B | Buying scale |

| HRC steel | $840/ton | Input cost volatility |

| R-32/R-454B | Concentrated | Supply leverage |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers protecting Carrier Global, highlighting disruptive forces and implications for pricing and profitability.

A concise, customizable one-sheet Porter’s Five Forces for Carrier Global—instantly visualize competitive pressure with a radar chart and tweak force levels for scenario analysis; clean layout ready for decks and seamless Excel integration.

Customers Bargaining Power

Fragmented residential demand

Individual homeowners have limited bargaining power in a fragmented residential market (US residential HVAC replacement market ≈ $16B in 2024); decisions lean on brand, warranties and efficiency ratings more than price. Installers and distributors — who drive roughly 70% of residential unit placements — strongly influence selections, softening direct buyer leverage. Promotional financing, used by about 30% of buyers, further reduces price sensitivity.

Powerful commercial and OEM buyers

Large contractors, developers and institutional buyers push hard on price and service when sourcing HVAC and refrigeration; Carrier reported roughly $22 billion revenue in fiscal 2024, reflecting exposure to such volume-driven contracts. Multi-site projects and framework agreements concentrate spend and give buyers leverage, with many tenders covering dozens to hundreds of sites. Buyers increasingly demand uptime SLAs, performance guarantees and customization, and routine competitive bidding intensifies price pressure.

Aftermarket and service stickiness

Aftermarket maintenance contracts, remote monitoring, and integrated parts ecosystems raise switching costs for building owners; as of 2024 Carrier and peers emphasize service-led offerings that lock in customers. Predictive service and control-system integration create operational lock-in for building managers, shifting focus to total cost of ownership over upfront price. Once installed, buyer leverage falls significantly.

Regulatory and incentive-driven choices

- Incentives: lower upfront barriers

- Savings: 30-50% energy reduction

- Compliance: fewer alternatives

- Pricing: value-based premiums

Price transparency and digital comparability

Online specs, ratings and peer benchmarks make HVAC and refrigeration offerings highly comparable, enabling buyers to solicit multiple quotes quickly and intensify negotiation; Carrier Global reported $20.6 billion revenue in 2023, underscoring scale where digital transparency matters. Complex system integrations and service contracts still require consultative selling, preserving solution differentiation.

- Comparability: increases buyer leverage

- Rapid quotes: accelerates price pressure

- Integration needs: sustain consultative sales

US replacement $16B; installers ≈70%, financing ≈30%, efficiency 30–50%

Buyers vary: fragmented homeowners (US residential replacement ≈ $16B in 2024) have limited price power; installers/distributors (~70% placements) and 30% promotional financing reduce direct leverage. Large contractors and institutions exert strong price/service pressure; Carrier revenue ≈ $22B FY2024 shows exposure. Aftermarket services and integrations raise switching costs; efficiency rules (30–50% savings) shift focus to lifecycle value.

| Metric | 2024 |

|---|---|

| US residential market | $16B |

| Carrier revenue | $22B |

| Installer share | ≈70% |

| Buyers using financing | ≈30% |

Preview Before You Purchase

Carrier Global Porter's Five Forces Analysis

This preview shows the exact Carrier Global Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. No mockups, samples, or placeholders are included. Upon payment you'll have instant access to this identical file for download and application.

From Overview to Strategy Blueprint

Carrier Global faces moderate buyer power, rising substitution pressures from integrated building systems, and steady supplier leverage—while scale and regulatory barriers curb new entrants. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy recommendations tailored to Carrier Global.

Suppliers Bargaining Power

Critical components concentration

Carrier depends on specialized suppliers for compressors, controls, sensors and semiconductors that are not perfectly substitutable, and limited qualified sources for variable-speed compressors and advanced electronics increase supplier leverage. Long qualification cycles driven by safety and reliability requirements extend lead times. In tight markets this concentration can push up pricing and delay deliveries, squeezing margins and inventory planning.

Refrigerant transition dynamics

Regulatory shifts to low-GWP refrigerants concentrate supply with a few producers—Chemours, Honeywell and several Chinese players dominate R-32/R-454B capacity by 2024—tightening terms and lead times. Suppliers of R-32/R-454B and compressors can influence availability during changeovers. Carrier must retool and co-develop designs, raising switching costs. Short-term scarcity can amplify supplier power despite expected long-term normalization.

Metals and energy cost pass-through

Steel (HRC ≈ $840/ton in 2024), copper (~$9,500/ton) and aluminum (~$2,300/ton) remained volatile in 2024 and are often passed through by upstream suppliers; hedges and contractual pricing help but timing mismatches can compress margins. Energy (Brent ≈ $80/bbl) and freight spikes also feed into component prices. Carrier’s scale (2024 revenue ≈ $21.8B) moderates but cannot eliminate these pressures.

Global logistics and risk concentration

Globalized supply chains expose Carrier to port congestion, geopolitics, and export controls; Carrier’s 2024 filings explicitly list logistics disruptions as a principal risk. Single-region supplier dependencies can magnify stoppages and boost supplier bargaining leverage. Dual-sourcing and localization lower probability of supply failure but do not eliminate systemic risks. Suppliers that maintained resilient multi-region footprints in 2024 secured stronger negotiating positions.

- High-risk: port congestion & export controls

- Concentration: single-region dependency raises leverage

- Mitigation: dual-sourcing/localization reduces but not removes risk

- Advantage: resilient suppliers gain pricing power (2024 observation)

Scale and partnership counterweights

Scale and partnership counterweights: Carrier’s purchasing scale (2024 revenue about $21B) and engineering co-development with key suppliers, plus multi-year supply agreements, reduce supplier bargaining power; joint development creates mutual dependency and priority allocation during shortages, while alternate qualification programs provide a credible switching threat.

- Purchasing scale: lowers costs

- Joint R&D: mutual dependency

- Long-term contracts: priority in shortages

- Alternate qualification: switching leverage

- IP/tooling lock-in: residual vendor power

Moderate-to-high supplier power: concentrated refrigerants, volatile metals, long qual cycles

Carrier faces moderate-to-high supplier power in 2024 due to specialized compressors/electronics, concentrated low-GWP refrigerant supply (Chemours, Honeywell dominant), and volatile metals/energy costs despite scale (2024 revenue ≈ $21.8B). Long qual cycles and logistics/port risks raise switching costs; dual-sourcing and long-term contracts partially mitigate.

| Item | 2024 | Impact |

|---|---|---|

| Revenue | $21.8B | Buying scale |

| HRC steel | $840/ton | Input cost volatility |

| R-32/R-454B | Concentrated | Supply leverage |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers protecting Carrier Global, highlighting disruptive forces and implications for pricing and profitability.

A concise, customizable one-sheet Porter’s Five Forces for Carrier Global—instantly visualize competitive pressure with a radar chart and tweak force levels for scenario analysis; clean layout ready for decks and seamless Excel integration.

Customers Bargaining Power

Fragmented residential demand

Individual homeowners have limited bargaining power in a fragmented residential market (US residential HVAC replacement market ≈ $16B in 2024); decisions lean on brand, warranties and efficiency ratings more than price. Installers and distributors — who drive roughly 70% of residential unit placements — strongly influence selections, softening direct buyer leverage. Promotional financing, used by about 30% of buyers, further reduces price sensitivity.

Powerful commercial and OEM buyers

Large contractors, developers and institutional buyers push hard on price and service when sourcing HVAC and refrigeration; Carrier reported roughly $22 billion revenue in fiscal 2024, reflecting exposure to such volume-driven contracts. Multi-site projects and framework agreements concentrate spend and give buyers leverage, with many tenders covering dozens to hundreds of sites. Buyers increasingly demand uptime SLAs, performance guarantees and customization, and routine competitive bidding intensifies price pressure.

Aftermarket and service stickiness

Aftermarket maintenance contracts, remote monitoring, and integrated parts ecosystems raise switching costs for building owners; as of 2024 Carrier and peers emphasize service-led offerings that lock in customers. Predictive service and control-system integration create operational lock-in for building managers, shifting focus to total cost of ownership over upfront price. Once installed, buyer leverage falls significantly.

Regulatory and incentive-driven choices

- Incentives: lower upfront barriers

- Savings: 30-50% energy reduction

- Compliance: fewer alternatives

- Pricing: value-based premiums

Price transparency and digital comparability

Online specs, ratings and peer benchmarks make HVAC and refrigeration offerings highly comparable, enabling buyers to solicit multiple quotes quickly and intensify negotiation; Carrier Global reported $20.6 billion revenue in 2023, underscoring scale where digital transparency matters. Complex system integrations and service contracts still require consultative selling, preserving solution differentiation.

- Comparability: increases buyer leverage

- Rapid quotes: accelerates price pressure

- Integration needs: sustain consultative sales

US replacement $16B; installers ≈70%, financing ≈30%, efficiency 30–50%

Buyers vary: fragmented homeowners (US residential replacement ≈ $16B in 2024) have limited price power; installers/distributors (~70% placements) and 30% promotional financing reduce direct leverage. Large contractors and institutions exert strong price/service pressure; Carrier revenue ≈ $22B FY2024 shows exposure. Aftermarket services and integrations raise switching costs; efficiency rules (30–50% savings) shift focus to lifecycle value.

| Metric | 2024 |

|---|---|

| US residential market | $16B |

| Carrier revenue | $22B |

| Installer share | ≈70% |

| Buyers using financing | ≈30% |

Preview Before You Purchase

Carrier Global Porter's Five Forces Analysis

This preview shows the exact Carrier Global Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. No mockups, samples, or placeholders are included. Upon payment you'll have instant access to this identical file for download and application.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Carrier Global faces moderate buyer power, rising substitution pressures from integrated building systems, and steady supplier leverage—while scale and regulatory barriers curb new entrants. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy recommendations tailored to Carrier Global.

Suppliers Bargaining Power

Critical components concentration

Carrier depends on specialized suppliers for compressors, controls, sensors and semiconductors that are not perfectly substitutable, and limited qualified sources for variable-speed compressors and advanced electronics increase supplier leverage. Long qualification cycles driven by safety and reliability requirements extend lead times. In tight markets this concentration can push up pricing and delay deliveries, squeezing margins and inventory planning.

Refrigerant transition dynamics

Regulatory shifts to low-GWP refrigerants concentrate supply with a few producers—Chemours, Honeywell and several Chinese players dominate R-32/R-454B capacity by 2024—tightening terms and lead times. Suppliers of R-32/R-454B and compressors can influence availability during changeovers. Carrier must retool and co-develop designs, raising switching costs. Short-term scarcity can amplify supplier power despite expected long-term normalization.

Metals and energy cost pass-through

Steel (HRC ≈ $840/ton in 2024), copper (~$9,500/ton) and aluminum (~$2,300/ton) remained volatile in 2024 and are often passed through by upstream suppliers; hedges and contractual pricing help but timing mismatches can compress margins. Energy (Brent ≈ $80/bbl) and freight spikes also feed into component prices. Carrier’s scale (2024 revenue ≈ $21.8B) moderates but cannot eliminate these pressures.

Global logistics and risk concentration

Globalized supply chains expose Carrier to port congestion, geopolitics, and export controls; Carrier’s 2024 filings explicitly list logistics disruptions as a principal risk. Single-region supplier dependencies can magnify stoppages and boost supplier bargaining leverage. Dual-sourcing and localization lower probability of supply failure but do not eliminate systemic risks. Suppliers that maintained resilient multi-region footprints in 2024 secured stronger negotiating positions.

- High-risk: port congestion & export controls

- Concentration: single-region dependency raises leverage

- Mitigation: dual-sourcing/localization reduces but not removes risk

- Advantage: resilient suppliers gain pricing power (2024 observation)

Scale and partnership counterweights

Scale and partnership counterweights: Carrier’s purchasing scale (2024 revenue about $21B) and engineering co-development with key suppliers, plus multi-year supply agreements, reduce supplier bargaining power; joint development creates mutual dependency and priority allocation during shortages, while alternate qualification programs provide a credible switching threat.

- Purchasing scale: lowers costs

- Joint R&D: mutual dependency

- Long-term contracts: priority in shortages

- Alternate qualification: switching leverage

- IP/tooling lock-in: residual vendor power

Moderate-to-high supplier power: concentrated refrigerants, volatile metals, long qual cycles

Carrier faces moderate-to-high supplier power in 2024 due to specialized compressors/electronics, concentrated low-GWP refrigerant supply (Chemours, Honeywell dominant), and volatile metals/energy costs despite scale (2024 revenue ≈ $21.8B). Long qual cycles and logistics/port risks raise switching costs; dual-sourcing and long-term contracts partially mitigate.

| Item | 2024 | Impact |

|---|---|---|

| Revenue | $21.8B | Buying scale |

| HRC steel | $840/ton | Input cost volatility |

| R-32/R-454B | Concentrated | Supply leverage |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers protecting Carrier Global, highlighting disruptive forces and implications for pricing and profitability.

A concise, customizable one-sheet Porter’s Five Forces for Carrier Global—instantly visualize competitive pressure with a radar chart and tweak force levels for scenario analysis; clean layout ready for decks and seamless Excel integration.

Customers Bargaining Power

Fragmented residential demand

Individual homeowners have limited bargaining power in a fragmented residential market (US residential HVAC replacement market ≈ $16B in 2024); decisions lean on brand, warranties and efficiency ratings more than price. Installers and distributors — who drive roughly 70% of residential unit placements — strongly influence selections, softening direct buyer leverage. Promotional financing, used by about 30% of buyers, further reduces price sensitivity.

Powerful commercial and OEM buyers

Large contractors, developers and institutional buyers push hard on price and service when sourcing HVAC and refrigeration; Carrier reported roughly $22 billion revenue in fiscal 2024, reflecting exposure to such volume-driven contracts. Multi-site projects and framework agreements concentrate spend and give buyers leverage, with many tenders covering dozens to hundreds of sites. Buyers increasingly demand uptime SLAs, performance guarantees and customization, and routine competitive bidding intensifies price pressure.

Aftermarket and service stickiness

Aftermarket maintenance contracts, remote monitoring, and integrated parts ecosystems raise switching costs for building owners; as of 2024 Carrier and peers emphasize service-led offerings that lock in customers. Predictive service and control-system integration create operational lock-in for building managers, shifting focus to total cost of ownership over upfront price. Once installed, buyer leverage falls significantly.

Regulatory and incentive-driven choices

- Incentives: lower upfront barriers

- Savings: 30-50% energy reduction

- Compliance: fewer alternatives

- Pricing: value-based premiums

Price transparency and digital comparability

Online specs, ratings and peer benchmarks make HVAC and refrigeration offerings highly comparable, enabling buyers to solicit multiple quotes quickly and intensify negotiation; Carrier Global reported $20.6 billion revenue in 2023, underscoring scale where digital transparency matters. Complex system integrations and service contracts still require consultative selling, preserving solution differentiation.

- Comparability: increases buyer leverage

- Rapid quotes: accelerates price pressure

- Integration needs: sustain consultative sales

US replacement $16B; installers ≈70%, financing ≈30%, efficiency 30–50%

Buyers vary: fragmented homeowners (US residential replacement ≈ $16B in 2024) have limited price power; installers/distributors (~70% placements) and 30% promotional financing reduce direct leverage. Large contractors and institutions exert strong price/service pressure; Carrier revenue ≈ $22B FY2024 shows exposure. Aftermarket services and integrations raise switching costs; efficiency rules (30–50% savings) shift focus to lifecycle value.

| Metric | 2024 |

|---|---|

| US residential market | $16B |

| Carrier revenue | $22B |

| Installer share | ≈70% |

| Buyers using financing | ≈30% |

Preview Before You Purchase

Carrier Global Porter's Five Forces Analysis

This preview shows the exact Carrier Global Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. No mockups, samples, or placeholders are included. Upon payment you'll have instant access to this identical file for download and application.