Carta Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

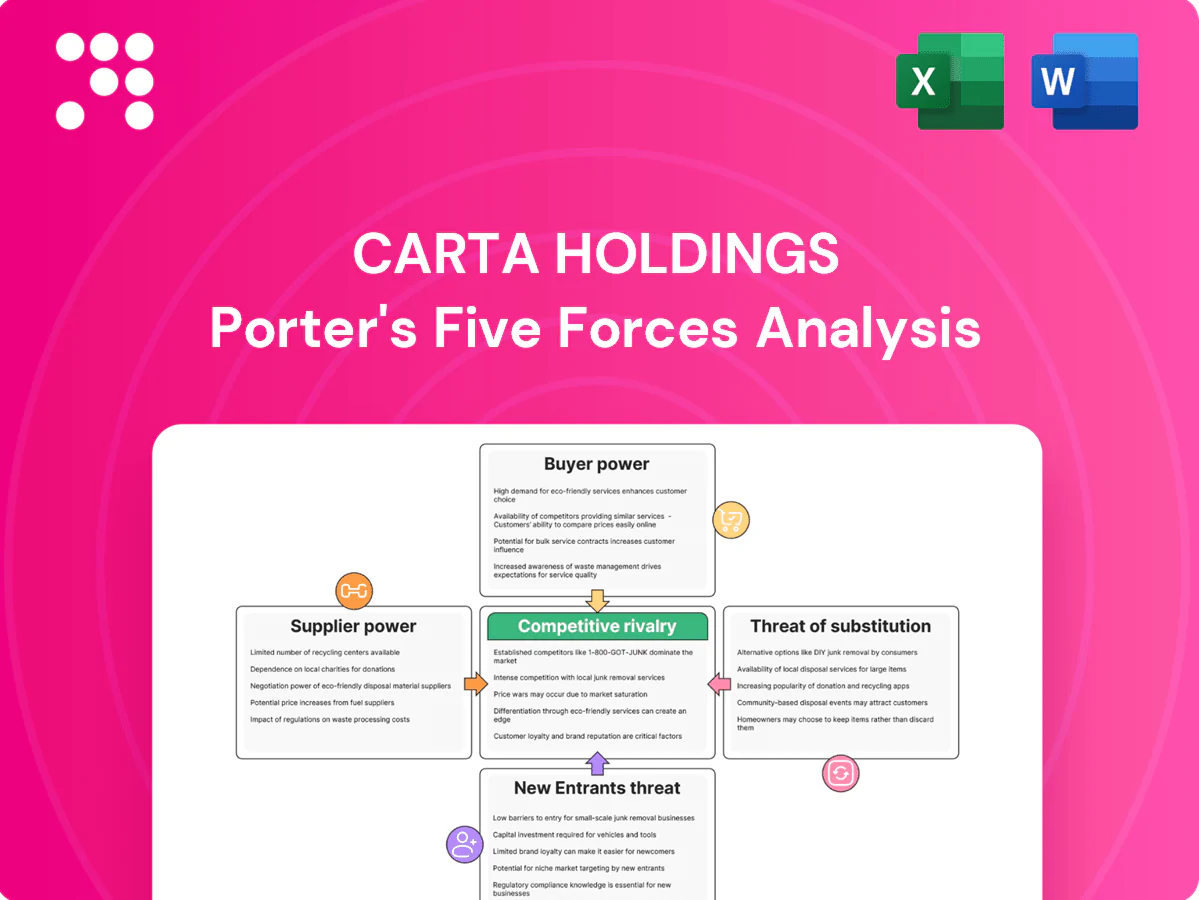

Carta Holdings faces nuanced competitive dynamics—moderate supplier influence, high buyer expectations, and evolving substitute threats—shaping its strategic choices and valuation. This snapshot highlights key pressure points but leaves force-by-force ratings, visuals, and implications unexplored. Unlock the full Porter's Five Forces Analysis to access a consultant-grade breakdown that informs investment and strategic decisions.

Suppliers Bargaining Power

Dependence on walled gardens

Major inventory and identity are concentrated in Google, Meta and Apple, with Google+Meta capturing roughly 65% of US digital ad spend in 2024, concentrating supplier power. Policy shifts—Apple’s IDFA opt‑in rates (~26% post‑iOS14.5) and browser cookie deprecation—can materially impair targeting and measurement. Carta must diversify supply, build first‑party/resolved IDs and pursue privileged API/access or priority integrations as strategic levers.

Premium publisher and CTV inventory

High-quality publishers and CTV/OTT platforms command scarcity premiums; US CTV ad spend reached roughly $23 billion in 2024 and CPMs are commonly 2–4x display, squeezing intermediary margins. As spend shifts to video, limited premium inventory forces Carta to build curated supply paths, private marketplaces, and revenue-share deals to secure access. Long-term guarantees can stabilize CPMs and revenue but curtail pricing flexibility and opportunistic yield management.

Data and martech vendors

Third-party data, verification and measurement vendors (DMPs, MMPs, IAS/MOAT) have gained pricing power as cookie/IDFA declines cut deterministic match rates by up to 70% in 2023–24, pushing firms toward modeled audiences and paid incrementality tests. Multi-vendor strategies and in-house analytics reduce vendor lock-in; volume commitments buy 10–30% discounts but lock 20–40% of media/tech budgets into fixed obligations.

Cloud and adtech infrastructure

Cloud compute, CDPs and ad‑serving tech are essential usage‑based inputs for Carta; hyperscalers held ~64% of cloud infra market in 2024 (AWS ~33%, Azure ~22%, GCP ~9%), so peak campaign cost spikes can compress margins materially. Optimizing workloads, committed‑use discounts and open‑source CDPs can rebalance supplier power, while EU/China data‑residency rules further concentrate supplier options.

- Usage‑based pricing: peak spikes raise COGS

- 2024 cloud share: AWS 33% / Azure 22% / GCP 9%

- Mitigation: committed discounts, workload optimization, open‑source

- Risk: regional data‑residency concentrates suppliers

Specialist talent as a supplier

Experienced ad ops, data science, and privacy engineers remain scarce, increasing supplier power for Carta despite broader 2024 tech layoffs; programmatic and measurement skills stayed tight per industry recruiting reports.

Robust retention programs and internal training pipelines materially reduce exposure, while offshoring and automation lower cost pressure and hiring lead times in practice.

- 2024: specialist talent scarcity elevated bargaining power

- Retention/training mitigate churn and wage inflation

- Offshoring + automation reduce marginal cost impact

- Programmatic/measurement skills persistently tight

Supplier power concentrated — 65% ad share; CTV $23B; cloud 64%

Supplier power is high: Google+Meta held ~65% of US digital ad spend in 2024, US CTV spend reached ~$23B, and hyperscalers held ~64% cloud share (AWS33/Azure22/GCP9). IDFA opt‑in ~26% reduced deterministic targeting; specialist ad/measurement talent remained scarce. Mitigants: first‑party IDs, committed cloud discounts, PMPs and revenue‑share deals.

| Metric | 2024 | Impact |

|---|---|---|

| Google+Meta ad share | ~65% | High concentration |

| US CTV spend | $23B | Premium CPMs |

| Cloud share | AWS33/AZ22/GCP9% | Supplier dependence |

| IDFA opt‑in | ~26% | Lower match rates |

What is included in the product

Tailored Porter's Five Forces analysis for Carta Holdings uncovers competitive drivers, buyer and supplier power, substitution risks, and barriers to entry, with strategic commentary on disruptive threats and market positioning.

A concise one-sheet Porter’s Five Forces for Carta Holdings—customize pressure levels and swap in your own data to neutralize strategic uncertainty; clean radar visualization and simplified layout ready to drop into decks or dashboards.

Customers Bargaining Power

Large advertisers and agencies

Large enterprise clients and holding-company agencies such as WPP, Omnicom, Publicis and IPG wield strong bargaining power via consolidated budgets and multi-year scopes.

They routinely run formal RFPs, demand outcome-based pricing and require deep integrations.

Carta must demonstrate unique performance lift or vertical expertise to defend rates; preferred-partner status and case-proven ROAS can offset discount pressure.

Low switching costs and multi‑homing

Low switching costs and widespread multi‑homing pressure Carta’s pricing power: 67% of advertisers run concurrent campaigns across platforms, reallocating budgets quickly when performance lags, and standardized APIs/data portability make migration easy. To reduce churn Carta must embed workflows, build proprietary audiences and deliver measurement that competitors cannot replicate. Strong SLAs and white‑glove onboarding increase perceived switching costs and lower churn risk.

Price transparency and procurement

In 2024 clients increasingly scrutinize take rates, tech fees and media markups, pushing procurement to demand unbundling and standardized rate cards; Carta must clarify value attribution, disclose all fees, and tie compensation to measurable KPIs to preserve trust. Transparent reporting, audited fee schedules and clean-room analytics bolster credibility and reduce churn.

Demand for privacy‑safe solutions

Buyers increasingly require compliance, consent management, and durable targeting; failure to meet standards can immediately disqualify vendors, so Carta must provide privacy‑enhancing tech and first‑party data strategies to retain enterprise clients.

- Certifications ISO/SOC lower perceived risk

- Privacy tech + first‑party data = stronger negotiation leverage

Performance and service expectations

Customers demand measurable lift, rapid optimizations, and 24/7 support during campaigns; underperformance triggers swift budget reallocation and heightened churn risk. Carta can differentiate with AI-driven optimization and industry-specific vertical playbooks to deliver faster lift. Dedicated account teams and proactive insights reduce buyer leverage by increasing switching costs and perceived value.

- Expectation: measurable lift, rapid optimization, 24/7 support

- Risk: fast budget shifts if underperforming

- Differentiators: AI optimization, vertical playbooks

- Retention: dedicated teams, proactive insights

Prove lift, tie fees to KPIs; counter 67% multi-homing and 70% first-party demand

Large agency clients and holding groups exert high bargaining power via consolidated budgets and formal RFPs; 67% of advertisers multi‑home campaigns, enabling rapid reallocation. Clients demand fee transparency and measurable ROI; 70% of marketers in 2024 prioritized first‑party data, raising requirements for privacy and integration. Carta must prove unique lift, tie fees to KPIs, and embed workflows to raise switching costs.

| Metric | 2024 Stat | Implication |

|---|---|---|

| Multi‑homing | 67% | Low switching cost, fast budget shifts |

| First‑party priority | 70% | Need for privacy + data solutions |

Preview the Actual Deliverable

Carta Holdings Porter's Five Forces Analysis

This preview shows the exact Carta Holdings Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, identical to the file provided on completion of payment.

From Overview to Strategy Blueprint

Carta Holdings faces nuanced competitive dynamics—moderate supplier influence, high buyer expectations, and evolving substitute threats—shaping its strategic choices and valuation. This snapshot highlights key pressure points but leaves force-by-force ratings, visuals, and implications unexplored. Unlock the full Porter's Five Forces Analysis to access a consultant-grade breakdown that informs investment and strategic decisions.

Suppliers Bargaining Power

Dependence on walled gardens

Major inventory and identity are concentrated in Google, Meta and Apple, with Google+Meta capturing roughly 65% of US digital ad spend in 2024, concentrating supplier power. Policy shifts—Apple’s IDFA opt‑in rates (~26% post‑iOS14.5) and browser cookie deprecation—can materially impair targeting and measurement. Carta must diversify supply, build first‑party/resolved IDs and pursue privileged API/access or priority integrations as strategic levers.

Premium publisher and CTV inventory

High-quality publishers and CTV/OTT platforms command scarcity premiums; US CTV ad spend reached roughly $23 billion in 2024 and CPMs are commonly 2–4x display, squeezing intermediary margins. As spend shifts to video, limited premium inventory forces Carta to build curated supply paths, private marketplaces, and revenue-share deals to secure access. Long-term guarantees can stabilize CPMs and revenue but curtail pricing flexibility and opportunistic yield management.

Data and martech vendors

Third-party data, verification and measurement vendors (DMPs, MMPs, IAS/MOAT) have gained pricing power as cookie/IDFA declines cut deterministic match rates by up to 70% in 2023–24, pushing firms toward modeled audiences and paid incrementality tests. Multi-vendor strategies and in-house analytics reduce vendor lock-in; volume commitments buy 10–30% discounts but lock 20–40% of media/tech budgets into fixed obligations.

Cloud and adtech infrastructure

Cloud compute, CDPs and ad‑serving tech are essential usage‑based inputs for Carta; hyperscalers held ~64% of cloud infra market in 2024 (AWS ~33%, Azure ~22%, GCP ~9%), so peak campaign cost spikes can compress margins materially. Optimizing workloads, committed‑use discounts and open‑source CDPs can rebalance supplier power, while EU/China data‑residency rules further concentrate supplier options.

- Usage‑based pricing: peak spikes raise COGS

- 2024 cloud share: AWS 33% / Azure 22% / GCP 9%

- Mitigation: committed discounts, workload optimization, open‑source

- Risk: regional data‑residency concentrates suppliers

Specialist talent as a supplier

Experienced ad ops, data science, and privacy engineers remain scarce, increasing supplier power for Carta despite broader 2024 tech layoffs; programmatic and measurement skills stayed tight per industry recruiting reports.

Robust retention programs and internal training pipelines materially reduce exposure, while offshoring and automation lower cost pressure and hiring lead times in practice.

- 2024: specialist talent scarcity elevated bargaining power

- Retention/training mitigate churn and wage inflation

- Offshoring + automation reduce marginal cost impact

- Programmatic/measurement skills persistently tight

Supplier power concentrated — 65% ad share; CTV $23B; cloud 64%

Supplier power is high: Google+Meta held ~65% of US digital ad spend in 2024, US CTV spend reached ~$23B, and hyperscalers held ~64% cloud share (AWS33/Azure22/GCP9). IDFA opt‑in ~26% reduced deterministic targeting; specialist ad/measurement talent remained scarce. Mitigants: first‑party IDs, committed cloud discounts, PMPs and revenue‑share deals.

| Metric | 2024 | Impact |

|---|---|---|

| Google+Meta ad share | ~65% | High concentration |

| US CTV spend | $23B | Premium CPMs |

| Cloud share | AWS33/AZ22/GCP9% | Supplier dependence |

| IDFA opt‑in | ~26% | Lower match rates |

What is included in the product

Tailored Porter's Five Forces analysis for Carta Holdings uncovers competitive drivers, buyer and supplier power, substitution risks, and barriers to entry, with strategic commentary on disruptive threats and market positioning.

A concise one-sheet Porter’s Five Forces for Carta Holdings—customize pressure levels and swap in your own data to neutralize strategic uncertainty; clean radar visualization and simplified layout ready to drop into decks or dashboards.

Customers Bargaining Power

Large advertisers and agencies

Large enterprise clients and holding-company agencies such as WPP, Omnicom, Publicis and IPG wield strong bargaining power via consolidated budgets and multi-year scopes.

They routinely run formal RFPs, demand outcome-based pricing and require deep integrations.

Carta must demonstrate unique performance lift or vertical expertise to defend rates; preferred-partner status and case-proven ROAS can offset discount pressure.

Low switching costs and multi‑homing

Low switching costs and widespread multi‑homing pressure Carta’s pricing power: 67% of advertisers run concurrent campaigns across platforms, reallocating budgets quickly when performance lags, and standardized APIs/data portability make migration easy. To reduce churn Carta must embed workflows, build proprietary audiences and deliver measurement that competitors cannot replicate. Strong SLAs and white‑glove onboarding increase perceived switching costs and lower churn risk.

Price transparency and procurement

In 2024 clients increasingly scrutinize take rates, tech fees and media markups, pushing procurement to demand unbundling and standardized rate cards; Carta must clarify value attribution, disclose all fees, and tie compensation to measurable KPIs to preserve trust. Transparent reporting, audited fee schedules and clean-room analytics bolster credibility and reduce churn.

Demand for privacy‑safe solutions

Buyers increasingly require compliance, consent management, and durable targeting; failure to meet standards can immediately disqualify vendors, so Carta must provide privacy‑enhancing tech and first‑party data strategies to retain enterprise clients.

- Certifications ISO/SOC lower perceived risk

- Privacy tech + first‑party data = stronger negotiation leverage

Performance and service expectations

Customers demand measurable lift, rapid optimizations, and 24/7 support during campaigns; underperformance triggers swift budget reallocation and heightened churn risk. Carta can differentiate with AI-driven optimization and industry-specific vertical playbooks to deliver faster lift. Dedicated account teams and proactive insights reduce buyer leverage by increasing switching costs and perceived value.

- Expectation: measurable lift, rapid optimization, 24/7 support

- Risk: fast budget shifts if underperforming

- Differentiators: AI optimization, vertical playbooks

- Retention: dedicated teams, proactive insights

Prove lift, tie fees to KPIs; counter 67% multi-homing and 70% first-party demand

Large agency clients and holding groups exert high bargaining power via consolidated budgets and formal RFPs; 67% of advertisers multi‑home campaigns, enabling rapid reallocation. Clients demand fee transparency and measurable ROI; 70% of marketers in 2024 prioritized first‑party data, raising requirements for privacy and integration. Carta must prove unique lift, tie fees to KPIs, and embed workflows to raise switching costs.

| Metric | 2024 Stat | Implication |

|---|---|---|

| Multi‑homing | 67% | Low switching cost, fast budget shifts |

| First‑party priority | 70% | Need for privacy + data solutions |

Preview the Actual Deliverable

Carta Holdings Porter's Five Forces Analysis

This preview shows the exact Carta Holdings Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, identical to the file provided on completion of payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Carta Holdings faces nuanced competitive dynamics—moderate supplier influence, high buyer expectations, and evolving substitute threats—shaping its strategic choices and valuation. This snapshot highlights key pressure points but leaves force-by-force ratings, visuals, and implications unexplored. Unlock the full Porter's Five Forces Analysis to access a consultant-grade breakdown that informs investment and strategic decisions.

Suppliers Bargaining Power

Dependence on walled gardens

Major inventory and identity are concentrated in Google, Meta and Apple, with Google+Meta capturing roughly 65% of US digital ad spend in 2024, concentrating supplier power. Policy shifts—Apple’s IDFA opt‑in rates (~26% post‑iOS14.5) and browser cookie deprecation—can materially impair targeting and measurement. Carta must diversify supply, build first‑party/resolved IDs and pursue privileged API/access or priority integrations as strategic levers.

Premium publisher and CTV inventory

High-quality publishers and CTV/OTT platforms command scarcity premiums; US CTV ad spend reached roughly $23 billion in 2024 and CPMs are commonly 2–4x display, squeezing intermediary margins. As spend shifts to video, limited premium inventory forces Carta to build curated supply paths, private marketplaces, and revenue-share deals to secure access. Long-term guarantees can stabilize CPMs and revenue but curtail pricing flexibility and opportunistic yield management.

Data and martech vendors

Third-party data, verification and measurement vendors (DMPs, MMPs, IAS/MOAT) have gained pricing power as cookie/IDFA declines cut deterministic match rates by up to 70% in 2023–24, pushing firms toward modeled audiences and paid incrementality tests. Multi-vendor strategies and in-house analytics reduce vendor lock-in; volume commitments buy 10–30% discounts but lock 20–40% of media/tech budgets into fixed obligations.

Cloud and adtech infrastructure

Cloud compute, CDPs and ad‑serving tech are essential usage‑based inputs for Carta; hyperscalers held ~64% of cloud infra market in 2024 (AWS ~33%, Azure ~22%, GCP ~9%), so peak campaign cost spikes can compress margins materially. Optimizing workloads, committed‑use discounts and open‑source CDPs can rebalance supplier power, while EU/China data‑residency rules further concentrate supplier options.

- Usage‑based pricing: peak spikes raise COGS

- 2024 cloud share: AWS 33% / Azure 22% / GCP 9%

- Mitigation: committed discounts, workload optimization, open‑source

- Risk: regional data‑residency concentrates suppliers

Specialist talent as a supplier

Experienced ad ops, data science, and privacy engineers remain scarce, increasing supplier power for Carta despite broader 2024 tech layoffs; programmatic and measurement skills stayed tight per industry recruiting reports.

Robust retention programs and internal training pipelines materially reduce exposure, while offshoring and automation lower cost pressure and hiring lead times in practice.

- 2024: specialist talent scarcity elevated bargaining power

- Retention/training mitigate churn and wage inflation

- Offshoring + automation reduce marginal cost impact

- Programmatic/measurement skills persistently tight

Supplier power concentrated — 65% ad share; CTV $23B; cloud 64%

Supplier power is high: Google+Meta held ~65% of US digital ad spend in 2024, US CTV spend reached ~$23B, and hyperscalers held ~64% cloud share (AWS33/Azure22/GCP9). IDFA opt‑in ~26% reduced deterministic targeting; specialist ad/measurement talent remained scarce. Mitigants: first‑party IDs, committed cloud discounts, PMPs and revenue‑share deals.

| Metric | 2024 | Impact |

|---|---|---|

| Google+Meta ad share | ~65% | High concentration |

| US CTV spend | $23B | Premium CPMs |

| Cloud share | AWS33/AZ22/GCP9% | Supplier dependence |

| IDFA opt‑in | ~26% | Lower match rates |

What is included in the product

Tailored Porter's Five Forces analysis for Carta Holdings uncovers competitive drivers, buyer and supplier power, substitution risks, and barriers to entry, with strategic commentary on disruptive threats and market positioning.

A concise one-sheet Porter’s Five Forces for Carta Holdings—customize pressure levels and swap in your own data to neutralize strategic uncertainty; clean radar visualization and simplified layout ready to drop into decks or dashboards.

Customers Bargaining Power

Large advertisers and agencies

Large enterprise clients and holding-company agencies such as WPP, Omnicom, Publicis and IPG wield strong bargaining power via consolidated budgets and multi-year scopes.

They routinely run formal RFPs, demand outcome-based pricing and require deep integrations.

Carta must demonstrate unique performance lift or vertical expertise to defend rates; preferred-partner status and case-proven ROAS can offset discount pressure.

Low switching costs and multi‑homing

Low switching costs and widespread multi‑homing pressure Carta’s pricing power: 67% of advertisers run concurrent campaigns across platforms, reallocating budgets quickly when performance lags, and standardized APIs/data portability make migration easy. To reduce churn Carta must embed workflows, build proprietary audiences and deliver measurement that competitors cannot replicate. Strong SLAs and white‑glove onboarding increase perceived switching costs and lower churn risk.

Price transparency and procurement

In 2024 clients increasingly scrutinize take rates, tech fees and media markups, pushing procurement to demand unbundling and standardized rate cards; Carta must clarify value attribution, disclose all fees, and tie compensation to measurable KPIs to preserve trust. Transparent reporting, audited fee schedules and clean-room analytics bolster credibility and reduce churn.

Demand for privacy‑safe solutions

Buyers increasingly require compliance, consent management, and durable targeting; failure to meet standards can immediately disqualify vendors, so Carta must provide privacy‑enhancing tech and first‑party data strategies to retain enterprise clients.

- Certifications ISO/SOC lower perceived risk

- Privacy tech + first‑party data = stronger negotiation leverage

Performance and service expectations

Customers demand measurable lift, rapid optimizations, and 24/7 support during campaigns; underperformance triggers swift budget reallocation and heightened churn risk. Carta can differentiate with AI-driven optimization and industry-specific vertical playbooks to deliver faster lift. Dedicated account teams and proactive insights reduce buyer leverage by increasing switching costs and perceived value.

- Expectation: measurable lift, rapid optimization, 24/7 support

- Risk: fast budget shifts if underperforming

- Differentiators: AI optimization, vertical playbooks

- Retention: dedicated teams, proactive insights

Prove lift, tie fees to KPIs; counter 67% multi-homing and 70% first-party demand

Large agency clients and holding groups exert high bargaining power via consolidated budgets and formal RFPs; 67% of advertisers multi‑home campaigns, enabling rapid reallocation. Clients demand fee transparency and measurable ROI; 70% of marketers in 2024 prioritized first‑party data, raising requirements for privacy and integration. Carta must prove unique lift, tie fees to KPIs, and embed workflows to raise switching costs.

| Metric | 2024 Stat | Implication |

|---|---|---|

| Multi‑homing | 67% | Low switching cost, fast budget shifts |

| First‑party priority | 70% | Need for privacy + data solutions |

Preview the Actual Deliverable

Carta Holdings Porter's Five Forces Analysis

This preview shows the exact Carta Holdings Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, identical to the file provided on completion of payment.