Carysil Porter's Five Forces Analysis

Don't Miss the Bigger Picture

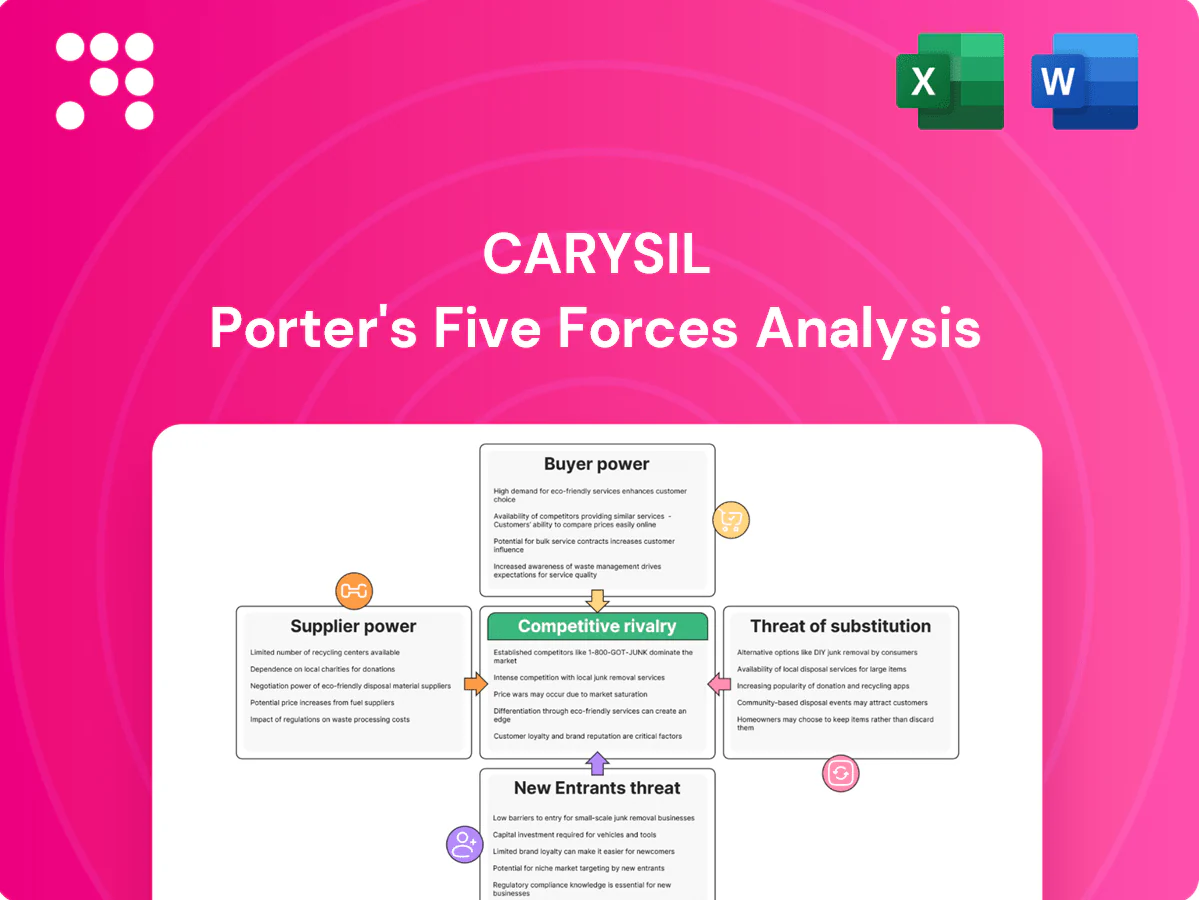

Carysil’s Porter's Five Forces snapshot highlights competitive intensity, supplier leverage, buyer power, threat of substitutes and entry barriers in clear terms. It teases strategic vulnerabilities and growth levers that matter to investors and managers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on quartz and resin inputs

Composite sinks depend on quartz granules and polymer resins from specialized mineral and chemical suppliers, giving those suppliers moderate bargaining power. These inputs are commoditized but cyclical, exposing Carysil to price volatility; long-term contracts and multi-sourcing reduce spikes but cannot eliminate shocks from sudden demand-supply imbalances. Any supplier-driven quality variance raises defect rates and warranty costs, directly hitting margins and brand reputation.

Stainless steel sheet and coil availability

Stainless steel sinks require steady access to specific grades and gauges, and in 2024 global stainless markets remained volatile with frequent alloy surcharges driving input-cost swings. Large mills retained negotiating leverage on small-lot orders, pressuring margins for smaller manufacturers. Scale purchases and vendor-managed inventory arrangements in 2024 helped Carysil mitigate supplier power and stabilize supply costs.

Specialty pigments, adhesives, and molds

Color pigments, bonding agents, and precision molds are niche inputs with concentrated supply—top five specialty pigment/mold suppliers account for roughly 40% of market share in 2024—giving suppliers elevated bargaining power. Switching suppliers requires 4–6 week qualification runs and potential downtime, increasing supplier stickiness. Strategic ownership of tooling and maintaining dual-approval supplier lists materially reduce this sourcing risk and mitigate price/lead-time exposure.

Logistics and energy cost pass-through

Energy-intensive curing and export-heavy shipments expose costs to fuel and freight volatility; Brent averaged about 86 USD/barrel in 2024 and the Baltic Dry Index ran near 1,200, amplifying input-cost swings and enabling carriers/utilities to pass surcharges in tight markets.

Certification and compliance dependencies

Compliance with NSF, CE (covers the 27 EU member states plus EEA), and U.S. EPA WaterSense norms requires supplier data, material traceability and audit-ready documentation, raising switching barriers when certified inputs are scarce; certified suppliers can command better pricing and lead times. Co-developing specs with suppliers helps redistribute bargaining power and reduce premium markups.

- Certification dependence: CE/NSF/WaterSense required

- Geography: CE covers 27 EU states + EEA

- Supplier leverage: certified inputs scarce → higher terms

- Mitigation: co-developed specs share power

Moderate-to-high supplier power raises input-cost risk amid energy and freight surcharges

Suppliers exert moderate-to-high power: commoditized quartz/resins face price volatility (long-term contracts mitigate) while stainless mills and specialty pigment/mold suppliers command higher leverage. Energy and freight surcharges (Brent ~86 USD/bbl; BDI ~1,200 in 2024) amplify input-cost risk; certifications and co-development lower supplier stickiness.

| Input | 2024 metric | Supplier concentration | Mitigation |

|---|---|---|---|

| Quartz/Resin | Volatile pricing | Moderate | Multi-source/contracts |

| Stainless | Alloy surcharges | High | Scale/VMI |

| Pigments/Molds | Top5≈40% share | High | Tooling ownership |

What is included in the product

Tailored exclusively for Carysil, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces that influence pricing, profitability, and market share.

A concise one-sheet Carysil Porter Five Forces summary for quick decision-making, with customizable pressure levels to reflect new data or market shifts. Includes an instant spider/radar chart and clean layout ready to copy into pitch decks, integrate into Excel dashboards, or share with non-finance stakeholders.

Customers Bargaining Power

Diverse channels dilute leverage

In 2024 Carysil sells through distributors, kitchen studios, builders and retailers across multiple countries, reducing dependence on any single buyer. This four-channel mix means no single channel dominates globally in most periods, lowering concentration risk. The diversified network softens take-it-or-leave-it demands from large accounts and preserves negotiating leverage for Carysil.

Project buyers negotiate hard

Developers and OEMs place bulk, standardized orders with high price sensitivity, driving discounts and extended credit demands—global engineered stone buyers accounted for an estimated 7.8 billion USD market in 2024, pressuring margins. Buyers push for longer payment terms and volume rebates, but suppliers counter with customization, installation support and reliable delivery, which reduce churn. Offering value-added bundles (warranty, logistics, installation) shifts buying focus from unit price to TCO, improving realizations by 3–7% on typical projects.

Retail end-users have low switching costs

Retail end-users face low switching costs and can change brands in-store or online based on aesthetics and price; over 70% of shoppers consult reviews before purchase, raising buyer power. Transparent comparison tools and ratings magnify this effect, while differentiated designs, extended warranties and brand equity help Carysil defend pricing. Robust after-sales service and installation support further reduce propensity to switch.

International distributors seek exclusivity

International distributors demanding exclusivity increase customer bargaining power because regional distributors leverage local market access to seek territory protection and rebates, pressuring margins; aligning incentives via performance-based exclusivity and joint marketing can mitigate this, while multi-distributor strategies in large markets limit any single distributor's leverage.

- Regional access: drives bargaining power

- Territory protection & rebates: common leverage

- Performance-based exclusivity: aligns incentives

- Joint marketing: shares growth incentives

- Multi-distributor: caps individual leverage

Information parity via e-commerce

Online pricing and spec sheets let buyers benchmark Carysil SKUs instantly, and with global e-commerce at about 23% of retail sales in 2024 (eMarketer) price transparency compresses margins on standard SKUs. Differentiation via unique finishes, branded accessories and quick-ship programs helps reclaim margin and reduce churn. Content-rich listings and AR visualization can preserve perceived value, with AR driving up to 40% higher conversion in some 2024 retail studies.

- benchmarking: faster cross-brand comparison

- margin pressure: common SKUs see compression

- differentiation: finishes, accessories, quick-ship

- content/AR: preserves value, boosts conversion

Engineered stone: moderate buyer power; market 7.8bn USD, e-commerce 23%, AR ~40%

Carysil faces moderate buyer power in 2024: diversified channels limit dominance, but builders/OEMs drive price sensitivity in a global engineered stone market ~7.8bn USD. E‑commerce at ~23% raises transparency; value-add bundles lift realizations 3–7% and AR can boost conversion ~40%.

| Metric | 2024 |

|---|---|

| Market size | 7.8bn USD |

| E‑commerce share | 23% |

| Realization uplift | 3–7% |

| AR conversion gain | ~40% |

What You See Is What You Get

Carysil Porter's Five Forces Analysis

This preview shows the exact Carysil Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use the moment you buy. What you see is the deliverable, instantly accessible and complete.

Don't Miss the Bigger Picture

Carysil’s Porter's Five Forces snapshot highlights competitive intensity, supplier leverage, buyer power, threat of substitutes and entry barriers in clear terms. It teases strategic vulnerabilities and growth levers that matter to investors and managers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on quartz and resin inputs

Composite sinks depend on quartz granules and polymer resins from specialized mineral and chemical suppliers, giving those suppliers moderate bargaining power. These inputs are commoditized but cyclical, exposing Carysil to price volatility; long-term contracts and multi-sourcing reduce spikes but cannot eliminate shocks from sudden demand-supply imbalances. Any supplier-driven quality variance raises defect rates and warranty costs, directly hitting margins and brand reputation.

Stainless steel sheet and coil availability

Stainless steel sinks require steady access to specific grades and gauges, and in 2024 global stainless markets remained volatile with frequent alloy surcharges driving input-cost swings. Large mills retained negotiating leverage on small-lot orders, pressuring margins for smaller manufacturers. Scale purchases and vendor-managed inventory arrangements in 2024 helped Carysil mitigate supplier power and stabilize supply costs.

Specialty pigments, adhesives, and molds

Color pigments, bonding agents, and precision molds are niche inputs with concentrated supply—top five specialty pigment/mold suppliers account for roughly 40% of market share in 2024—giving suppliers elevated bargaining power. Switching suppliers requires 4–6 week qualification runs and potential downtime, increasing supplier stickiness. Strategic ownership of tooling and maintaining dual-approval supplier lists materially reduce this sourcing risk and mitigate price/lead-time exposure.

Logistics and energy cost pass-through

Energy-intensive curing and export-heavy shipments expose costs to fuel and freight volatility; Brent averaged about 86 USD/barrel in 2024 and the Baltic Dry Index ran near 1,200, amplifying input-cost swings and enabling carriers/utilities to pass surcharges in tight markets.

Certification and compliance dependencies

Compliance with NSF, CE (covers the 27 EU member states plus EEA), and U.S. EPA WaterSense norms requires supplier data, material traceability and audit-ready documentation, raising switching barriers when certified inputs are scarce; certified suppliers can command better pricing and lead times. Co-developing specs with suppliers helps redistribute bargaining power and reduce premium markups.

- Certification dependence: CE/NSF/WaterSense required

- Geography: CE covers 27 EU states + EEA

- Supplier leverage: certified inputs scarce → higher terms

- Mitigation: co-developed specs share power

Moderate-to-high supplier power raises input-cost risk amid energy and freight surcharges

Suppliers exert moderate-to-high power: commoditized quartz/resins face price volatility (long-term contracts mitigate) while stainless mills and specialty pigment/mold suppliers command higher leverage. Energy and freight surcharges (Brent ~86 USD/bbl; BDI ~1,200 in 2024) amplify input-cost risk; certifications and co-development lower supplier stickiness.

| Input | 2024 metric | Supplier concentration | Mitigation |

|---|---|---|---|

| Quartz/Resin | Volatile pricing | Moderate | Multi-source/contracts |

| Stainless | Alloy surcharges | High | Scale/VMI |

| Pigments/Molds | Top5≈40% share | High | Tooling ownership |

What is included in the product

Tailored exclusively for Carysil, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces that influence pricing, profitability, and market share.

A concise one-sheet Carysil Porter Five Forces summary for quick decision-making, with customizable pressure levels to reflect new data or market shifts. Includes an instant spider/radar chart and clean layout ready to copy into pitch decks, integrate into Excel dashboards, or share with non-finance stakeholders.

Customers Bargaining Power

Diverse channels dilute leverage

In 2024 Carysil sells through distributors, kitchen studios, builders and retailers across multiple countries, reducing dependence on any single buyer. This four-channel mix means no single channel dominates globally in most periods, lowering concentration risk. The diversified network softens take-it-or-leave-it demands from large accounts and preserves negotiating leverage for Carysil.

Project buyers negotiate hard

Developers and OEMs place bulk, standardized orders with high price sensitivity, driving discounts and extended credit demands—global engineered stone buyers accounted for an estimated 7.8 billion USD market in 2024, pressuring margins. Buyers push for longer payment terms and volume rebates, but suppliers counter with customization, installation support and reliable delivery, which reduce churn. Offering value-added bundles (warranty, logistics, installation) shifts buying focus from unit price to TCO, improving realizations by 3–7% on typical projects.

Retail end-users have low switching costs

Retail end-users face low switching costs and can change brands in-store or online based on aesthetics and price; over 70% of shoppers consult reviews before purchase, raising buyer power. Transparent comparison tools and ratings magnify this effect, while differentiated designs, extended warranties and brand equity help Carysil defend pricing. Robust after-sales service and installation support further reduce propensity to switch.

International distributors seek exclusivity

International distributors demanding exclusivity increase customer bargaining power because regional distributors leverage local market access to seek territory protection and rebates, pressuring margins; aligning incentives via performance-based exclusivity and joint marketing can mitigate this, while multi-distributor strategies in large markets limit any single distributor's leverage.

- Regional access: drives bargaining power

- Territory protection & rebates: common leverage

- Performance-based exclusivity: aligns incentives

- Joint marketing: shares growth incentives

- Multi-distributor: caps individual leverage

Information parity via e-commerce

Online pricing and spec sheets let buyers benchmark Carysil SKUs instantly, and with global e-commerce at about 23% of retail sales in 2024 (eMarketer) price transparency compresses margins on standard SKUs. Differentiation via unique finishes, branded accessories and quick-ship programs helps reclaim margin and reduce churn. Content-rich listings and AR visualization can preserve perceived value, with AR driving up to 40% higher conversion in some 2024 retail studies.

- benchmarking: faster cross-brand comparison

- margin pressure: common SKUs see compression

- differentiation: finishes, accessories, quick-ship

- content/AR: preserves value, boosts conversion

Engineered stone: moderate buyer power; market 7.8bn USD, e-commerce 23%, AR ~40%

Carysil faces moderate buyer power in 2024: diversified channels limit dominance, but builders/OEMs drive price sensitivity in a global engineered stone market ~7.8bn USD. E‑commerce at ~23% raises transparency; value-add bundles lift realizations 3–7% and AR can boost conversion ~40%.

| Metric | 2024 |

|---|---|

| Market size | 7.8bn USD |

| E‑commerce share | 23% |

| Realization uplift | 3–7% |

| AR conversion gain | ~40% |

What You See Is What You Get

Carysil Porter's Five Forces Analysis

This preview shows the exact Carysil Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use the moment you buy. What you see is the deliverable, instantly accessible and complete.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Carysil’s Porter's Five Forces snapshot highlights competitive intensity, supplier leverage, buyer power, threat of substitutes and entry barriers in clear terms. It teases strategic vulnerabilities and growth levers that matter to investors and managers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on quartz and resin inputs

Composite sinks depend on quartz granules and polymer resins from specialized mineral and chemical suppliers, giving those suppliers moderate bargaining power. These inputs are commoditized but cyclical, exposing Carysil to price volatility; long-term contracts and multi-sourcing reduce spikes but cannot eliminate shocks from sudden demand-supply imbalances. Any supplier-driven quality variance raises defect rates and warranty costs, directly hitting margins and brand reputation.

Stainless steel sheet and coil availability

Stainless steel sinks require steady access to specific grades and gauges, and in 2024 global stainless markets remained volatile with frequent alloy surcharges driving input-cost swings. Large mills retained negotiating leverage on small-lot orders, pressuring margins for smaller manufacturers. Scale purchases and vendor-managed inventory arrangements in 2024 helped Carysil mitigate supplier power and stabilize supply costs.

Specialty pigments, adhesives, and molds

Color pigments, bonding agents, and precision molds are niche inputs with concentrated supply—top five specialty pigment/mold suppliers account for roughly 40% of market share in 2024—giving suppliers elevated bargaining power. Switching suppliers requires 4–6 week qualification runs and potential downtime, increasing supplier stickiness. Strategic ownership of tooling and maintaining dual-approval supplier lists materially reduce this sourcing risk and mitigate price/lead-time exposure.

Logistics and energy cost pass-through

Energy-intensive curing and export-heavy shipments expose costs to fuel and freight volatility; Brent averaged about 86 USD/barrel in 2024 and the Baltic Dry Index ran near 1,200, amplifying input-cost swings and enabling carriers/utilities to pass surcharges in tight markets.

Certification and compliance dependencies

Compliance with NSF, CE (covers the 27 EU member states plus EEA), and U.S. EPA WaterSense norms requires supplier data, material traceability and audit-ready documentation, raising switching barriers when certified inputs are scarce; certified suppliers can command better pricing and lead times. Co-developing specs with suppliers helps redistribute bargaining power and reduce premium markups.

- Certification dependence: CE/NSF/WaterSense required

- Geography: CE covers 27 EU states + EEA

- Supplier leverage: certified inputs scarce → higher terms

- Mitigation: co-developed specs share power

Moderate-to-high supplier power raises input-cost risk amid energy and freight surcharges

Suppliers exert moderate-to-high power: commoditized quartz/resins face price volatility (long-term contracts mitigate) while stainless mills and specialty pigment/mold suppliers command higher leverage. Energy and freight surcharges (Brent ~86 USD/bbl; BDI ~1,200 in 2024) amplify input-cost risk; certifications and co-development lower supplier stickiness.

| Input | 2024 metric | Supplier concentration | Mitigation |

|---|---|---|---|

| Quartz/Resin | Volatile pricing | Moderate | Multi-source/contracts |

| Stainless | Alloy surcharges | High | Scale/VMI |

| Pigments/Molds | Top5≈40% share | High | Tooling ownership |

What is included in the product

Tailored exclusively for Carysil, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces that influence pricing, profitability, and market share.

A concise one-sheet Carysil Porter Five Forces summary for quick decision-making, with customizable pressure levels to reflect new data or market shifts. Includes an instant spider/radar chart and clean layout ready to copy into pitch decks, integrate into Excel dashboards, or share with non-finance stakeholders.

Customers Bargaining Power

Diverse channels dilute leverage

In 2024 Carysil sells through distributors, kitchen studios, builders and retailers across multiple countries, reducing dependence on any single buyer. This four-channel mix means no single channel dominates globally in most periods, lowering concentration risk. The diversified network softens take-it-or-leave-it demands from large accounts and preserves negotiating leverage for Carysil.

Project buyers negotiate hard

Developers and OEMs place bulk, standardized orders with high price sensitivity, driving discounts and extended credit demands—global engineered stone buyers accounted for an estimated 7.8 billion USD market in 2024, pressuring margins. Buyers push for longer payment terms and volume rebates, but suppliers counter with customization, installation support and reliable delivery, which reduce churn. Offering value-added bundles (warranty, logistics, installation) shifts buying focus from unit price to TCO, improving realizations by 3–7% on typical projects.

Retail end-users have low switching costs

Retail end-users face low switching costs and can change brands in-store or online based on aesthetics and price; over 70% of shoppers consult reviews before purchase, raising buyer power. Transparent comparison tools and ratings magnify this effect, while differentiated designs, extended warranties and brand equity help Carysil defend pricing. Robust after-sales service and installation support further reduce propensity to switch.

International distributors seek exclusivity

International distributors demanding exclusivity increase customer bargaining power because regional distributors leverage local market access to seek territory protection and rebates, pressuring margins; aligning incentives via performance-based exclusivity and joint marketing can mitigate this, while multi-distributor strategies in large markets limit any single distributor's leverage.

- Regional access: drives bargaining power

- Territory protection & rebates: common leverage

- Performance-based exclusivity: aligns incentives

- Joint marketing: shares growth incentives

- Multi-distributor: caps individual leverage

Information parity via e-commerce

Online pricing and spec sheets let buyers benchmark Carysil SKUs instantly, and with global e-commerce at about 23% of retail sales in 2024 (eMarketer) price transparency compresses margins on standard SKUs. Differentiation via unique finishes, branded accessories and quick-ship programs helps reclaim margin and reduce churn. Content-rich listings and AR visualization can preserve perceived value, with AR driving up to 40% higher conversion in some 2024 retail studies.

- benchmarking: faster cross-brand comparison

- margin pressure: common SKUs see compression

- differentiation: finishes, accessories, quick-ship

- content/AR: preserves value, boosts conversion

Engineered stone: moderate buyer power; market 7.8bn USD, e-commerce 23%, AR ~40%

Carysil faces moderate buyer power in 2024: diversified channels limit dominance, but builders/OEMs drive price sensitivity in a global engineered stone market ~7.8bn USD. E‑commerce at ~23% raises transparency; value-add bundles lift realizations 3–7% and AR can boost conversion ~40%.

| Metric | 2024 |

|---|---|

| Market size | 7.8bn USD |

| E‑commerce share | 23% |

| Realization uplift | 3–7% |

| AR conversion gain | ~40% |

What You See Is What You Get

Carysil Porter's Five Forces Analysis

This preview shows the exact Carysil Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use the moment you buy. What you see is the deliverable, instantly accessible and complete.