Cascades Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

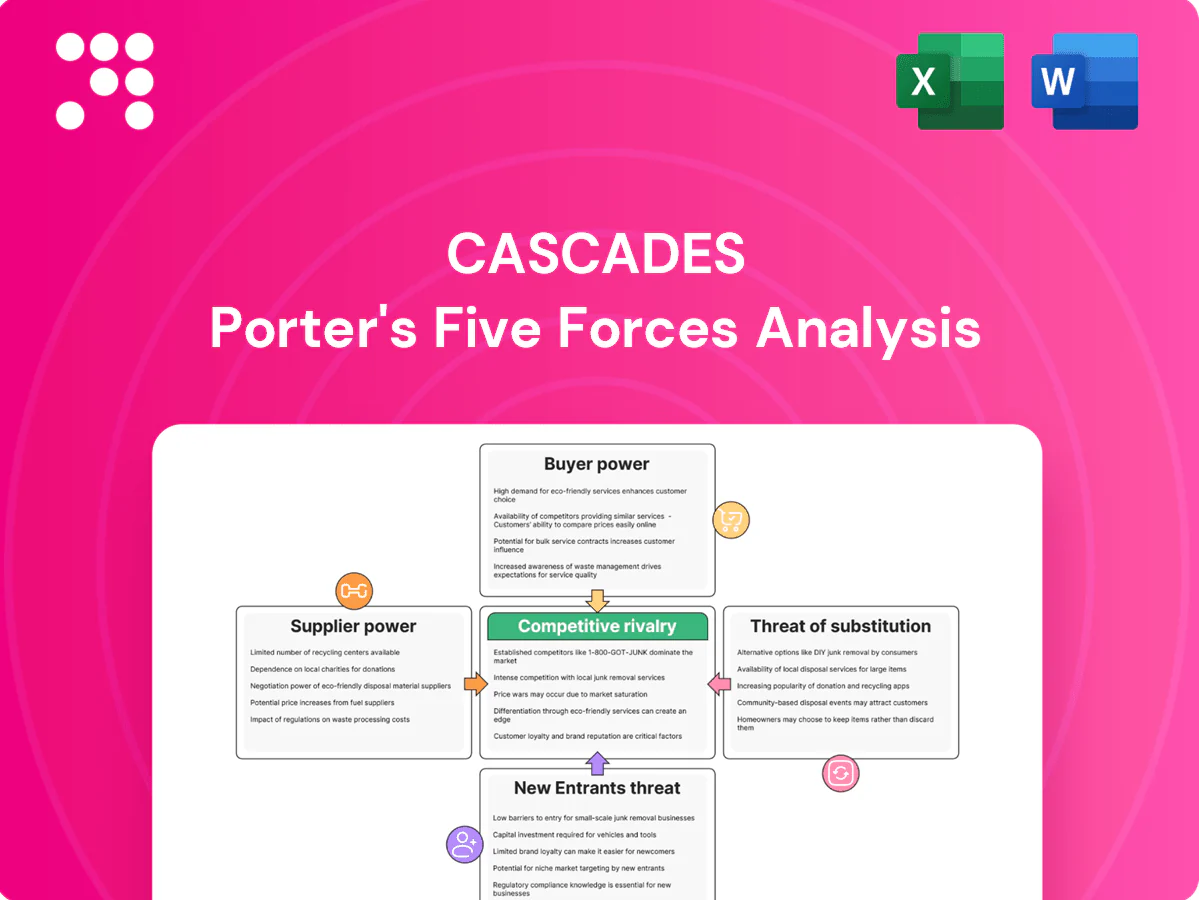

Cascades faces varied supplier leverage, moderate buyer power, and evolving substitute threats that shape its competitive landscape; this snapshot highlights key tensions but omits depth. Unlock the full Porter's Five Forces Analysis to explore Cascades’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Recovered fiber concentration

Cascades depends heavily on recovered paper streams, and regional concentration of supply gives local aggregators leverage over pricing and availability. When municipal collection programs or large MRFs consolidate, pricing power shifts upward despite Cascades’ own recovery operations and long-term contracts. Spot-market volatility—often showing double-digit percentage swings—can still pressure margins, with tight supply during economic upswings quickly elevating OCC and mixed-paper costs.

Energy and inputs exposure

Energy (electricity, natural gas, steam) and chemicals/starches are largely commoditized and available from multiple suppliers, keeping individual supplier power low; however, Canada’s federal carbon price rose to CAD 80/t in 2024, and regional electricity/gas spikes can materially lift input bills. Interruptible contracts and hedging mitigate exposure but customer pass-through lags, while plant location and local grid mix (renewables vs fossil) alter bargaining leverage with utilities.

Equipment and maintenance vendors

Paper machines, corrugators and tissue converting lines are supplied mainly by a few dominant OEMs (Valmet, Voith, Andritz), creating switching frictions. Specialized parts and multi-year service agreements lock in spend and give OEMs pricing latitude. Cascades leverages multi-plant scale and staggered overhauls to negotiate, but 12–24 month lead times and OEM technical IP constrain optionality. Upgrades for efficiency/emissions further entrench select suppliers.

Sustainability-certified inputs

Demand for FSC/PEFC and eco-chemistries narrows Cascades' supplier pool; global FSC-certified forest area ~220 million ha (2024) makes certified capacity tight and can boost supplier leverage. Cascades' circularity brand limits substitution to non‑certified inputs. Strategic partnerships secure availability but often embed price premia.

- Certified pool shrinks supplier options

- Capacity tightness raises supplier bargaining power

- Brand constraints reduce substitution

- Partnerships secure supply but add premia

Logistics and freight dependencies

Inbound fiber and outbound packaging depend heavily on trucking and rail, with 2024 US truckload spot rates roughly 5–10% above 2019 averages and Class I rail volumes down about 2% YoY in early 2024, shifting episodic leverage to carriers. Fuel surcharges and driver shortages drive cyclical carrier power, while regional mill proximity limits baseline costs but not disruption risk from strikes or weather. Cascades uses dedicated lanes and multi-carrier routing to partially offset this exposure.

- Spot rates +5–10% vs 2019

- Rail volumes −2% YoY (early 2024)

- Fuel surcharges amplify carrier leverage

- Dedicated lanes/multi-carrier reduce but don’t eliminate risk

Recovered-fiber concentration raises regional pricing; spot swings > 10%

Recovered-fiber concentration gives regional aggregators pricing leverage; spot-market swings often exceed 10% and raise OCC/mixed-paper costs. Energy/chemicals remain commoditized but Canada’s CAD 80/t carbon price (2024) and grid spikes lift input bills despite hedging. OEMs (Valmet/Voith/Andritz) and limited FSC pool (≈220M ha, 2024) constrain substitution and add service premia.

| Supplier | Leverage | 2024 metric |

|---|---|---|

| Recovered fiber | High | Spot ±>10% |

| Energy | Medium | Carbon CAD80/t |

| OEMs | High | Lead 12–24m |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry tailored to Cascades’ paper and packaging market position, identifying disruptive threats and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Cascades—instantly pinpoint competitive pain points with a customizable pressure scale and spider chart for quick strategic decisions.

Customers Bargaining Power

Large retail and CPG buyers

Major retailers, food processors and brand owners buy tissue in huge volumes and use centralized bid cycles to extract price concessions and service guarantees, compressing supplier margins. Private-label tissue customers are especially price-sensitive; private-label penetration in North American retail tissue reached about 30% in 2024. Losing a top account can materially reduce plant utilization and raise unit costs.

Low switching costs in commoditized SKUs

Standard corrugated and tissue SKUs are easily substituted among qualified vendors, with technical specs widely standardized and buyer firms commonly dual-sourcing to mitigate supply risk. Cascades leans on recycled-content credentials and service reliability, yet price competitiveness remains the dominant buying criterion. Short contract terms, typically 6–12 months, sustain persistent pricing pressure and frequent renegotiation.

ESG and innovation demands

Customers increasingly demand recycled content, recyclability and lower-carbon footprints, with 2024 procurement surveys showing over 60% of packaging buyers prioritize ESG; compliance forces Cascades into higher OPEX and capex yet buyers resist paying full premiums. Cascades’ sustainability credentials help win RFPs but raise the bar for continuous improvement. Co-development deals increase customer stickiness while introducing shared IP and strict KPIs.

Procurement digitalization and auctions

Procurement digitalization and reverse auctions increase price transparency and competitive pressure; industry studies in 2024 report eSourcing-driven price compression typically in the 5–15% range, forcing supplier margins down for like-for-like specs. Cascades must therefore shift sales conversations to total cost of ownership—service, quality, sustainability—and monetize value-added design and logistics to mitigate pure unit-price comparisons.

- eSourcing: higher price transparency

- Reverse auctions: 5–15% price compression (2024)

- Benchmarking: squeezes like-for-like margins

- TCO focus: design, logistics, sustainability soften price-only bids

Demand cyclicality and inventory tactics

Industrial customers shift orders with macro cycles, increasing bargaining power in downturns and forcing Cascades into deeper discounting to protect volumes; lean inventories and JIT delivery move working-capital burdens upstream, squeezing supplier margins. Consignment and vendor-managed inventory programs can secure share but transfer stock and obsolescence risk to Cascades.

- Demand cyclicality: higher buyer leverage

- JIT/lean inventory: upstream working-capital strain

- Discounting pressure: margin erosion

- Consignment/VMI: market share vs. supplier risk

Retailer bids squeeze margins: private-label 30%, eSourcing 5-15%, ESG >60%

Major retailers and brand owners drive price pressure via centralized bids; private-label penetration in North American retail tissue reached about 30% in 2024. eSourcing and reverse auctions drove 5–15% price compression in 2024 while >60% of packaging buyers prioritized ESG, raising OPEX/capex needs. Short contracts (6–12 months), dual-sourcing and demand cyclicality sustain strong buyer bargaining power.

| Metric | 2024 | Implication |

|---|---|---|

| Private-label share | 30% | Price sensitivity |

| eSourcing impact | 5–15% | Margin compression |

| ESG priority | >60% | Higher OPEX/capex |

Full Version Awaits

Cascades Porter's Five Forces Analysis

This preview shows Cascades Porter's Five Forces Analysis exactly as delivered upon purchase—no placeholders, no edits. The file is fully formatted, professionally written, and ready for immediate download and use. What you see is what you'll receive.

Go Beyond the Preview—Access the Full Strategic Report

Cascades faces varied supplier leverage, moderate buyer power, and evolving substitute threats that shape its competitive landscape; this snapshot highlights key tensions but omits depth. Unlock the full Porter's Five Forces Analysis to explore Cascades’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Recovered fiber concentration

Cascades depends heavily on recovered paper streams, and regional concentration of supply gives local aggregators leverage over pricing and availability. When municipal collection programs or large MRFs consolidate, pricing power shifts upward despite Cascades’ own recovery operations and long-term contracts. Spot-market volatility—often showing double-digit percentage swings—can still pressure margins, with tight supply during economic upswings quickly elevating OCC and mixed-paper costs.

Energy and inputs exposure

Energy (electricity, natural gas, steam) and chemicals/starches are largely commoditized and available from multiple suppliers, keeping individual supplier power low; however, Canada’s federal carbon price rose to CAD 80/t in 2024, and regional electricity/gas spikes can materially lift input bills. Interruptible contracts and hedging mitigate exposure but customer pass-through lags, while plant location and local grid mix (renewables vs fossil) alter bargaining leverage with utilities.

Equipment and maintenance vendors

Paper machines, corrugators and tissue converting lines are supplied mainly by a few dominant OEMs (Valmet, Voith, Andritz), creating switching frictions. Specialized parts and multi-year service agreements lock in spend and give OEMs pricing latitude. Cascades leverages multi-plant scale and staggered overhauls to negotiate, but 12–24 month lead times and OEM technical IP constrain optionality. Upgrades for efficiency/emissions further entrench select suppliers.

Sustainability-certified inputs

Demand for FSC/PEFC and eco-chemistries narrows Cascades' supplier pool; global FSC-certified forest area ~220 million ha (2024) makes certified capacity tight and can boost supplier leverage. Cascades' circularity brand limits substitution to non‑certified inputs. Strategic partnerships secure availability but often embed price premia.

- Certified pool shrinks supplier options

- Capacity tightness raises supplier bargaining power

- Brand constraints reduce substitution

- Partnerships secure supply but add premia

Logistics and freight dependencies

Inbound fiber and outbound packaging depend heavily on trucking and rail, with 2024 US truckload spot rates roughly 5–10% above 2019 averages and Class I rail volumes down about 2% YoY in early 2024, shifting episodic leverage to carriers. Fuel surcharges and driver shortages drive cyclical carrier power, while regional mill proximity limits baseline costs but not disruption risk from strikes or weather. Cascades uses dedicated lanes and multi-carrier routing to partially offset this exposure.

- Spot rates +5–10% vs 2019

- Rail volumes −2% YoY (early 2024)

- Fuel surcharges amplify carrier leverage

- Dedicated lanes/multi-carrier reduce but don’t eliminate risk

Recovered-fiber concentration raises regional pricing; spot swings > 10%

Recovered-fiber concentration gives regional aggregators pricing leverage; spot-market swings often exceed 10% and raise OCC/mixed-paper costs. Energy/chemicals remain commoditized but Canada’s CAD 80/t carbon price (2024) and grid spikes lift input bills despite hedging. OEMs (Valmet/Voith/Andritz) and limited FSC pool (≈220M ha, 2024) constrain substitution and add service premia.

| Supplier | Leverage | 2024 metric |

|---|---|---|

| Recovered fiber | High | Spot ±>10% |

| Energy | Medium | Carbon CAD80/t |

| OEMs | High | Lead 12–24m |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry tailored to Cascades’ paper and packaging market position, identifying disruptive threats and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Cascades—instantly pinpoint competitive pain points with a customizable pressure scale and spider chart for quick strategic decisions.

Customers Bargaining Power

Large retail and CPG buyers

Major retailers, food processors and brand owners buy tissue in huge volumes and use centralized bid cycles to extract price concessions and service guarantees, compressing supplier margins. Private-label tissue customers are especially price-sensitive; private-label penetration in North American retail tissue reached about 30% in 2024. Losing a top account can materially reduce plant utilization and raise unit costs.

Low switching costs in commoditized SKUs

Standard corrugated and tissue SKUs are easily substituted among qualified vendors, with technical specs widely standardized and buyer firms commonly dual-sourcing to mitigate supply risk. Cascades leans on recycled-content credentials and service reliability, yet price competitiveness remains the dominant buying criterion. Short contract terms, typically 6–12 months, sustain persistent pricing pressure and frequent renegotiation.

ESG and innovation demands

Customers increasingly demand recycled content, recyclability and lower-carbon footprints, with 2024 procurement surveys showing over 60% of packaging buyers prioritize ESG; compliance forces Cascades into higher OPEX and capex yet buyers resist paying full premiums. Cascades’ sustainability credentials help win RFPs but raise the bar for continuous improvement. Co-development deals increase customer stickiness while introducing shared IP and strict KPIs.

Procurement digitalization and auctions

Procurement digitalization and reverse auctions increase price transparency and competitive pressure; industry studies in 2024 report eSourcing-driven price compression typically in the 5–15% range, forcing supplier margins down for like-for-like specs. Cascades must therefore shift sales conversations to total cost of ownership—service, quality, sustainability—and monetize value-added design and logistics to mitigate pure unit-price comparisons.

- eSourcing: higher price transparency

- Reverse auctions: 5–15% price compression (2024)

- Benchmarking: squeezes like-for-like margins

- TCO focus: design, logistics, sustainability soften price-only bids

Demand cyclicality and inventory tactics

Industrial customers shift orders with macro cycles, increasing bargaining power in downturns and forcing Cascades into deeper discounting to protect volumes; lean inventories and JIT delivery move working-capital burdens upstream, squeezing supplier margins. Consignment and vendor-managed inventory programs can secure share but transfer stock and obsolescence risk to Cascades.

- Demand cyclicality: higher buyer leverage

- JIT/lean inventory: upstream working-capital strain

- Discounting pressure: margin erosion

- Consignment/VMI: market share vs. supplier risk

Retailer bids squeeze margins: private-label 30%, eSourcing 5-15%, ESG >60%

Major retailers and brand owners drive price pressure via centralized bids; private-label penetration in North American retail tissue reached about 30% in 2024. eSourcing and reverse auctions drove 5–15% price compression in 2024 while >60% of packaging buyers prioritized ESG, raising OPEX/capex needs. Short contracts (6–12 months), dual-sourcing and demand cyclicality sustain strong buyer bargaining power.

| Metric | 2024 | Implication |

|---|---|---|

| Private-label share | 30% | Price sensitivity |

| eSourcing impact | 5–15% | Margin compression |

| ESG priority | >60% | Higher OPEX/capex |

Full Version Awaits

Cascades Porter's Five Forces Analysis

This preview shows Cascades Porter's Five Forces Analysis exactly as delivered upon purchase—no placeholders, no edits. The file is fully formatted, professionally written, and ready for immediate download and use. What you see is what you'll receive.

Description

Go Beyond the Preview—Access the Full Strategic Report

Cascades faces varied supplier leverage, moderate buyer power, and evolving substitute threats that shape its competitive landscape; this snapshot highlights key tensions but omits depth. Unlock the full Porter's Five Forces Analysis to explore Cascades’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Recovered fiber concentration

Cascades depends heavily on recovered paper streams, and regional concentration of supply gives local aggregators leverage over pricing and availability. When municipal collection programs or large MRFs consolidate, pricing power shifts upward despite Cascades’ own recovery operations and long-term contracts. Spot-market volatility—often showing double-digit percentage swings—can still pressure margins, with tight supply during economic upswings quickly elevating OCC and mixed-paper costs.

Energy and inputs exposure

Energy (electricity, natural gas, steam) and chemicals/starches are largely commoditized and available from multiple suppliers, keeping individual supplier power low; however, Canada’s federal carbon price rose to CAD 80/t in 2024, and regional electricity/gas spikes can materially lift input bills. Interruptible contracts and hedging mitigate exposure but customer pass-through lags, while plant location and local grid mix (renewables vs fossil) alter bargaining leverage with utilities.

Equipment and maintenance vendors

Paper machines, corrugators and tissue converting lines are supplied mainly by a few dominant OEMs (Valmet, Voith, Andritz), creating switching frictions. Specialized parts and multi-year service agreements lock in spend and give OEMs pricing latitude. Cascades leverages multi-plant scale and staggered overhauls to negotiate, but 12–24 month lead times and OEM technical IP constrain optionality. Upgrades for efficiency/emissions further entrench select suppliers.

Sustainability-certified inputs

Demand for FSC/PEFC and eco-chemistries narrows Cascades' supplier pool; global FSC-certified forest area ~220 million ha (2024) makes certified capacity tight and can boost supplier leverage. Cascades' circularity brand limits substitution to non‑certified inputs. Strategic partnerships secure availability but often embed price premia.

- Certified pool shrinks supplier options

- Capacity tightness raises supplier bargaining power

- Brand constraints reduce substitution

- Partnerships secure supply but add premia

Logistics and freight dependencies

Inbound fiber and outbound packaging depend heavily on trucking and rail, with 2024 US truckload spot rates roughly 5–10% above 2019 averages and Class I rail volumes down about 2% YoY in early 2024, shifting episodic leverage to carriers. Fuel surcharges and driver shortages drive cyclical carrier power, while regional mill proximity limits baseline costs but not disruption risk from strikes or weather. Cascades uses dedicated lanes and multi-carrier routing to partially offset this exposure.

- Spot rates +5–10% vs 2019

- Rail volumes −2% YoY (early 2024)

- Fuel surcharges amplify carrier leverage

- Dedicated lanes/multi-carrier reduce but don’t eliminate risk

Recovered-fiber concentration raises regional pricing; spot swings > 10%

Recovered-fiber concentration gives regional aggregators pricing leverage; spot-market swings often exceed 10% and raise OCC/mixed-paper costs. Energy/chemicals remain commoditized but Canada’s CAD 80/t carbon price (2024) and grid spikes lift input bills despite hedging. OEMs (Valmet/Voith/Andritz) and limited FSC pool (≈220M ha, 2024) constrain substitution and add service premia.

| Supplier | Leverage | 2024 metric |

|---|---|---|

| Recovered fiber | High | Spot ±>10% |

| Energy | Medium | Carbon CAD80/t |

| OEMs | High | Lead 12–24m |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and rivalry tailored to Cascades’ paper and packaging market position, identifying disruptive threats and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Cascades—instantly pinpoint competitive pain points with a customizable pressure scale and spider chart for quick strategic decisions.

Customers Bargaining Power

Large retail and CPG buyers

Major retailers, food processors and brand owners buy tissue in huge volumes and use centralized bid cycles to extract price concessions and service guarantees, compressing supplier margins. Private-label tissue customers are especially price-sensitive; private-label penetration in North American retail tissue reached about 30% in 2024. Losing a top account can materially reduce plant utilization and raise unit costs.

Low switching costs in commoditized SKUs

Standard corrugated and tissue SKUs are easily substituted among qualified vendors, with technical specs widely standardized and buyer firms commonly dual-sourcing to mitigate supply risk. Cascades leans on recycled-content credentials and service reliability, yet price competitiveness remains the dominant buying criterion. Short contract terms, typically 6–12 months, sustain persistent pricing pressure and frequent renegotiation.

ESG and innovation demands

Customers increasingly demand recycled content, recyclability and lower-carbon footprints, with 2024 procurement surveys showing over 60% of packaging buyers prioritize ESG; compliance forces Cascades into higher OPEX and capex yet buyers resist paying full premiums. Cascades’ sustainability credentials help win RFPs but raise the bar for continuous improvement. Co-development deals increase customer stickiness while introducing shared IP and strict KPIs.

Procurement digitalization and auctions

Procurement digitalization and reverse auctions increase price transparency and competitive pressure; industry studies in 2024 report eSourcing-driven price compression typically in the 5–15% range, forcing supplier margins down for like-for-like specs. Cascades must therefore shift sales conversations to total cost of ownership—service, quality, sustainability—and monetize value-added design and logistics to mitigate pure unit-price comparisons.

- eSourcing: higher price transparency

- Reverse auctions: 5–15% price compression (2024)

- Benchmarking: squeezes like-for-like margins

- TCO focus: design, logistics, sustainability soften price-only bids

Demand cyclicality and inventory tactics

Industrial customers shift orders with macro cycles, increasing bargaining power in downturns and forcing Cascades into deeper discounting to protect volumes; lean inventories and JIT delivery move working-capital burdens upstream, squeezing supplier margins. Consignment and vendor-managed inventory programs can secure share but transfer stock and obsolescence risk to Cascades.

- Demand cyclicality: higher buyer leverage

- JIT/lean inventory: upstream working-capital strain

- Discounting pressure: margin erosion

- Consignment/VMI: market share vs. supplier risk

Retailer bids squeeze margins: private-label 30%, eSourcing 5-15%, ESG >60%

Major retailers and brand owners drive price pressure via centralized bids; private-label penetration in North American retail tissue reached about 30% in 2024. eSourcing and reverse auctions drove 5–15% price compression in 2024 while >60% of packaging buyers prioritized ESG, raising OPEX/capex needs. Short contracts (6–12 months), dual-sourcing and demand cyclicality sustain strong buyer bargaining power.

| Metric | 2024 | Implication |

|---|---|---|

| Private-label share | 30% | Price sensitivity |

| eSourcing impact | 5–15% | Margin compression |

| ESG priority | >60% | Higher OPEX/capex |

Full Version Awaits

Cascades Porter's Five Forces Analysis

This preview shows Cascades Porter's Five Forces Analysis exactly as delivered upon purchase—no placeholders, no edits. The file is fully formatted, professionally written, and ready for immediate download and use. What you see is what you'll receive.