Cathay Pacific Airways PESTLE Analysis

Your Shortcut to Market Insight Starts Here

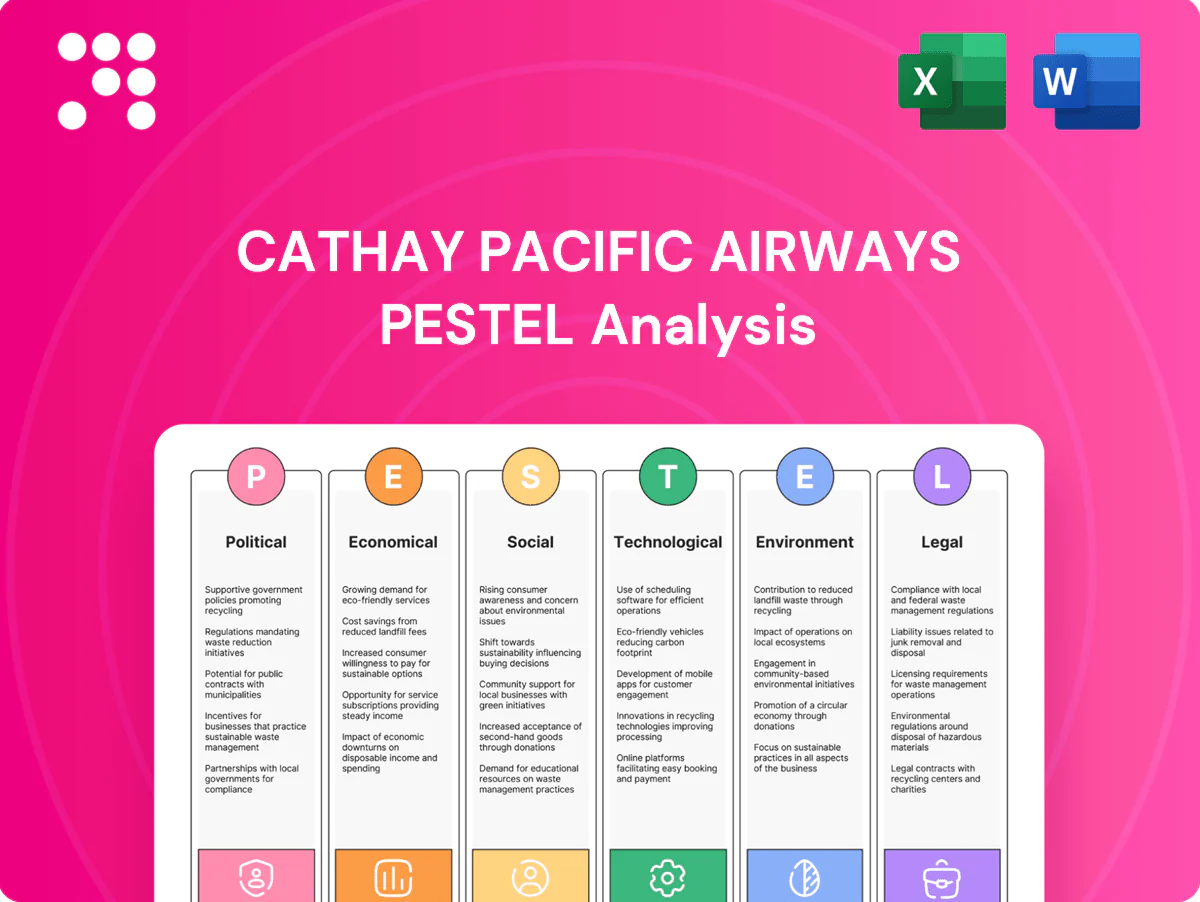

Stay ahead with a concise PESTLE snapshot of Cathay Pacific Airways—revealing how political shifts, economic cycles, social trends, technological advances, legal pressures, and environmental risks converge on its strategy. These insights highlight key vulnerabilities and growth levers for investors and planners. Purchase the full PESTLE for the complete, actionable breakdown.

Political factors

HK–Mainland relations

Access to Mainland routes for Cathay Pacific depends heavily on Hong Kong–Beijing policy alignment; favorable ties can accelerate traffic rights and slot allocations in Tier-1 cities like Beijing and Shanghai. Any political strain could delay approvals and constrain network growth and capacity recovery. Cross-border integration via the Greater Bay Area (≈86 million people, GDP ≈US$1.9tn) remains a strategic lever for market access and feeder traffic.

Geopolitical tensions

US–China rivalry and regional flashpoints dent demand and complicate overflight permissions, forcing Cathay Pacific—part of a group operating ~200 aircraft—to reroute and redeploy, raising unit costs; IATA reported 2024 global RPKs at about 94% of 2019 levels, showing sensitive demand recovery. Sanctions regimes increase compliance costs and routing complexity, while headlines can rapidly swing corporate travel sentiment. Scenario planning for sudden airspace shifts is essential.

Bilateral air service agreements

Bilateral air service agreements determine Cathay Pacific’s capacity, frequency and destination access, with Hong Kong international capacity still reported at about 70% of 2019 levels in late 2024, constraining route reinstatements. Negotiation outcomes shape competitive parity versus foreign carriers by granting or limiting frequencies and traffic rights. Post-pandemic entitlements remain uneven across markets, so strategic lobbying has become essential to secure advantageous rights.

Airspace restrictions

Limited access to Russian airspace forces Cathay Pacific to operate longer Asia–Europe sectors, often adding 1–2 hours and raising fuel burn by up to 10–15% on affected routes, reducing schedule resilience and increasing unit costs; competitors with Russia overflight rights retain cost/time advantages. Dynamic flight planning and payload adjustments are required to mitigate block-time and fuel impacts.

- Added block time: ~1–2h

- Fuel burn increase: ~10–15%

- Lower aircraft productivity

- Need for dynamic replanning

HK policy support

Hong Kong policy support for aviation, cargo and tourism—through targeted incentives, slot and fee policies—remains a key determinant of Cathay Pacific’s recovery pace and operating costs; the Three-Runway System expands HKIA capacity to about 100 million passengers p.a., unlocking growth potential, while stable governance sustains investor confidence.

GBA integration and HK TRS spur recovery; US-China tensions and airspace limits raise costs

Political alignment with Beijing, GBA integration (≈86M pop, GDP ≈US$1.9tn) and HK policy (TRS 100M pax p.a.) drive market access and recovery; US–China tensions and sanctions raise compliance costs and dent demand (IATA 2024 RPKs ≈94% of 2019). Bilateral ASAs and limited Russia overflight rights (adds ~1–2h, +10–15% fuel) constrain capacity versus competitors; govt support remains critical.

| Metric | Value |

|---|---|

| Group fleet | ~200 aircraft |

| HKIA capacity | TRS 100M pax p.a. |

| HK intl capacity (late 2024) | ~70% of 2019 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Cathay Pacific Airways across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by data and region-specific regulatory context. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios ready for business plans, pitch decks and strategic decision-making.

Condensed PESTLE summary for Cathay Pacific highlighting key political, economic, social, technological, legal and environmental risks with clear implications and mitigation ideas for each. Ready-to-drop into presentations or planning sessions to speed decision-making and cross-team alignment.

Economic factors

Global demand cycles

Premium and corporate travel for Cathay tracks global GDP, with IMF projecting ~3% world growth for 2024–25, so corporate demand remains cyclical.

Air freight correlates with e-commerce (global online retail ~5.7 trillion USD in 2023) and manufacturing activity, driving cargo tonne-km swings.

Downturns compress yields and reopenings lift load factors; regional diversification across Asia, Europe and North America smooths volatility for Cathay.

Fuel price volatility

Jet fuel typically represents roughly 20–30% of airline operating costs, making price swings a key driver of Cathay Pacific’s margin volatility; spikes in 2022–24 pushed industry jet fuel prices up by about 20–40% year-on-year at points. Hedging policies aim to smooth cash-flow but introduce basis risk when spot/backspread moves diverge from hedged benchmarks. Route-level profitability can flip within weeks during fuel spikes, and more fuel-efficient widebodies (lower L/100km) act as a durable competitive moat when prices rise.

FX and HKD peg

Revenues at Cathay Pacific are multi-currency while major costs—jet fuel, aircraft leases and many financing contracts—are USD-linked, with jet fuel typically 20–30% of airline operating costs. The HKD–USD peg (HKMA Convertibility Zone 7.75–7.85) stabilizes local financing and interest-rate transmission but forces foreign-exchange translation volatility on non-HKD earnings. Currency moves affect pricing power and demand across Greater China and long-haul routes, so active treasury hedging and USD liquidity management remain critical.

Interest rates and debt

Higher interest rates lift lease and borrowing costs, squeezing margins on fleet renewal and making lessors push higher rents; Cathay Pacific’s refinancing windows and access to export credit are therefore critical to maintaining fleet plans. Strong balance sheet resilience determines flexibility in taking delivery or deferring orders, while disciplined capex timing preserves ROIC through rate cycles.

- Lease/borrowing sensitivity

- Refinancing & export credit importance

- Balance-sheet order flexibility

- Capex timing to protect ROIC

Hong Kong tourism recovery

Hong Kong tourism recovery is driving Cathay Pacific seat factors and network breadth as inbound arrivals surged after reopening, with visitor numbers climbing sharply in 2023–24 and GBA day‑trip and leisure demand from the Mainland pivotal to load factors and frequency restoration; airport capacity ramp‑up at HKIA enables scale, but competitive fares remain necessary to rebuild market share.

- Inbound/outbound flows: Mainland leisure fuels peak loads

- GBA connectivity: critical for point‑to‑point demand

- HKIA capacity: enables scalability vs 2019

- Pricing: discounted fares likely to regain share

GBA integration and HK TRS spur recovery; US-China tensions and airspace limits raise costs

Premium and corporate travel ties to IMF-projected ~3% world GDP growth for 2024–25, keeping corporate demand cyclical.

Air freight aligns with global e-commerce of ~5.7 trillion USD in 2023, driving cargo tonne-km volatility.

Jet fuel is ~20–30% of costs with 2022–24 price spikes of ~20–40% y/y; HKD peg 7.75–7.85 stabilizes local financing but adds FX translation risk.

| Metric | Value |

|---|---|

| Global GDP (IMF) | ~3% (2024–25) |

| Global e‑commerce (2023) | ~5.7T USD |

| Jet fuel share | 20–30% |

| Fuel spike (2022–24) | ~20–40% y/y |

| HKD–USD peg | 7.75–7.85 |

Preview Before You Purchase

Cathay Pacific Airways PESTLE Analysis

This Cathay Pacific Airways PESTLE Analysis examines political, economic, social, technological, legal and environmental factors affecting the carrier and offers actionable insights for strategy and risk management. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. You’ll download this same, final file immediately after payment.

Your Shortcut to Market Insight Starts Here

Stay ahead with a concise PESTLE snapshot of Cathay Pacific Airways—revealing how political shifts, economic cycles, social trends, technological advances, legal pressures, and environmental risks converge on its strategy. These insights highlight key vulnerabilities and growth levers for investors and planners. Purchase the full PESTLE for the complete, actionable breakdown.

Political factors

HK–Mainland relations

Access to Mainland routes for Cathay Pacific depends heavily on Hong Kong–Beijing policy alignment; favorable ties can accelerate traffic rights and slot allocations in Tier-1 cities like Beijing and Shanghai. Any political strain could delay approvals and constrain network growth and capacity recovery. Cross-border integration via the Greater Bay Area (≈86 million people, GDP ≈US$1.9tn) remains a strategic lever for market access and feeder traffic.

Geopolitical tensions

US–China rivalry and regional flashpoints dent demand and complicate overflight permissions, forcing Cathay Pacific—part of a group operating ~200 aircraft—to reroute and redeploy, raising unit costs; IATA reported 2024 global RPKs at about 94% of 2019 levels, showing sensitive demand recovery. Sanctions regimes increase compliance costs and routing complexity, while headlines can rapidly swing corporate travel sentiment. Scenario planning for sudden airspace shifts is essential.

Bilateral air service agreements

Bilateral air service agreements determine Cathay Pacific’s capacity, frequency and destination access, with Hong Kong international capacity still reported at about 70% of 2019 levels in late 2024, constraining route reinstatements. Negotiation outcomes shape competitive parity versus foreign carriers by granting or limiting frequencies and traffic rights. Post-pandemic entitlements remain uneven across markets, so strategic lobbying has become essential to secure advantageous rights.

Airspace restrictions

Limited access to Russian airspace forces Cathay Pacific to operate longer Asia–Europe sectors, often adding 1–2 hours and raising fuel burn by up to 10–15% on affected routes, reducing schedule resilience and increasing unit costs; competitors with Russia overflight rights retain cost/time advantages. Dynamic flight planning and payload adjustments are required to mitigate block-time and fuel impacts.

- Added block time: ~1–2h

- Fuel burn increase: ~10–15%

- Lower aircraft productivity

- Need for dynamic replanning

HK policy support

Hong Kong policy support for aviation, cargo and tourism—through targeted incentives, slot and fee policies—remains a key determinant of Cathay Pacific’s recovery pace and operating costs; the Three-Runway System expands HKIA capacity to about 100 million passengers p.a., unlocking growth potential, while stable governance sustains investor confidence.

GBA integration and HK TRS spur recovery; US-China tensions and airspace limits raise costs

Political alignment with Beijing, GBA integration (≈86M pop, GDP ≈US$1.9tn) and HK policy (TRS 100M pax p.a.) drive market access and recovery; US–China tensions and sanctions raise compliance costs and dent demand (IATA 2024 RPKs ≈94% of 2019). Bilateral ASAs and limited Russia overflight rights (adds ~1–2h, +10–15% fuel) constrain capacity versus competitors; govt support remains critical.

| Metric | Value |

|---|---|

| Group fleet | ~200 aircraft |

| HKIA capacity | TRS 100M pax p.a. |

| HK intl capacity (late 2024) | ~70% of 2019 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Cathay Pacific Airways across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by data and region-specific regulatory context. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios ready for business plans, pitch decks and strategic decision-making.

Condensed PESTLE summary for Cathay Pacific highlighting key political, economic, social, technological, legal and environmental risks with clear implications and mitigation ideas for each. Ready-to-drop into presentations or planning sessions to speed decision-making and cross-team alignment.

Economic factors

Global demand cycles

Premium and corporate travel for Cathay tracks global GDP, with IMF projecting ~3% world growth for 2024–25, so corporate demand remains cyclical.

Air freight correlates with e-commerce (global online retail ~5.7 trillion USD in 2023) and manufacturing activity, driving cargo tonne-km swings.

Downturns compress yields and reopenings lift load factors; regional diversification across Asia, Europe and North America smooths volatility for Cathay.

Fuel price volatility

Jet fuel typically represents roughly 20–30% of airline operating costs, making price swings a key driver of Cathay Pacific’s margin volatility; spikes in 2022–24 pushed industry jet fuel prices up by about 20–40% year-on-year at points. Hedging policies aim to smooth cash-flow but introduce basis risk when spot/backspread moves diverge from hedged benchmarks. Route-level profitability can flip within weeks during fuel spikes, and more fuel-efficient widebodies (lower L/100km) act as a durable competitive moat when prices rise.

FX and HKD peg

Revenues at Cathay Pacific are multi-currency while major costs—jet fuel, aircraft leases and many financing contracts—are USD-linked, with jet fuel typically 20–30% of airline operating costs. The HKD–USD peg (HKMA Convertibility Zone 7.75–7.85) stabilizes local financing and interest-rate transmission but forces foreign-exchange translation volatility on non-HKD earnings. Currency moves affect pricing power and demand across Greater China and long-haul routes, so active treasury hedging and USD liquidity management remain critical.

Interest rates and debt

Higher interest rates lift lease and borrowing costs, squeezing margins on fleet renewal and making lessors push higher rents; Cathay Pacific’s refinancing windows and access to export credit are therefore critical to maintaining fleet plans. Strong balance sheet resilience determines flexibility in taking delivery or deferring orders, while disciplined capex timing preserves ROIC through rate cycles.

- Lease/borrowing sensitivity

- Refinancing & export credit importance

- Balance-sheet order flexibility

- Capex timing to protect ROIC

Hong Kong tourism recovery

Hong Kong tourism recovery is driving Cathay Pacific seat factors and network breadth as inbound arrivals surged after reopening, with visitor numbers climbing sharply in 2023–24 and GBA day‑trip and leisure demand from the Mainland pivotal to load factors and frequency restoration; airport capacity ramp‑up at HKIA enables scale, but competitive fares remain necessary to rebuild market share.

- Inbound/outbound flows: Mainland leisure fuels peak loads

- GBA connectivity: critical for point‑to‑point demand

- HKIA capacity: enables scalability vs 2019

- Pricing: discounted fares likely to regain share

GBA integration and HK TRS spur recovery; US-China tensions and airspace limits raise costs

Premium and corporate travel ties to IMF-projected ~3% world GDP growth for 2024–25, keeping corporate demand cyclical.

Air freight aligns with global e-commerce of ~5.7 trillion USD in 2023, driving cargo tonne-km volatility.

Jet fuel is ~20–30% of costs with 2022–24 price spikes of ~20–40% y/y; HKD peg 7.75–7.85 stabilizes local financing but adds FX translation risk.

| Metric | Value |

|---|---|

| Global GDP (IMF) | ~3% (2024–25) |

| Global e‑commerce (2023) | ~5.7T USD |

| Jet fuel share | 20–30% |

| Fuel spike (2022–24) | ~20–40% y/y |

| HKD–USD peg | 7.75–7.85 |

Preview Before You Purchase

Cathay Pacific Airways PESTLE Analysis

This Cathay Pacific Airways PESTLE Analysis examines political, economic, social, technological, legal and environmental factors affecting the carrier and offers actionable insights for strategy and risk management. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. You’ll download this same, final file immediately after payment.

Description

Your Shortcut to Market Insight Starts Here

Stay ahead with a concise PESTLE snapshot of Cathay Pacific Airways—revealing how political shifts, economic cycles, social trends, technological advances, legal pressures, and environmental risks converge on its strategy. These insights highlight key vulnerabilities and growth levers for investors and planners. Purchase the full PESTLE for the complete, actionable breakdown.

Political factors

HK–Mainland relations

Access to Mainland routes for Cathay Pacific depends heavily on Hong Kong–Beijing policy alignment; favorable ties can accelerate traffic rights and slot allocations in Tier-1 cities like Beijing and Shanghai. Any political strain could delay approvals and constrain network growth and capacity recovery. Cross-border integration via the Greater Bay Area (≈86 million people, GDP ≈US$1.9tn) remains a strategic lever for market access and feeder traffic.

Geopolitical tensions

US–China rivalry and regional flashpoints dent demand and complicate overflight permissions, forcing Cathay Pacific—part of a group operating ~200 aircraft—to reroute and redeploy, raising unit costs; IATA reported 2024 global RPKs at about 94% of 2019 levels, showing sensitive demand recovery. Sanctions regimes increase compliance costs and routing complexity, while headlines can rapidly swing corporate travel sentiment. Scenario planning for sudden airspace shifts is essential.

Bilateral air service agreements

Bilateral air service agreements determine Cathay Pacific’s capacity, frequency and destination access, with Hong Kong international capacity still reported at about 70% of 2019 levels in late 2024, constraining route reinstatements. Negotiation outcomes shape competitive parity versus foreign carriers by granting or limiting frequencies and traffic rights. Post-pandemic entitlements remain uneven across markets, so strategic lobbying has become essential to secure advantageous rights.

Airspace restrictions

Limited access to Russian airspace forces Cathay Pacific to operate longer Asia–Europe sectors, often adding 1–2 hours and raising fuel burn by up to 10–15% on affected routes, reducing schedule resilience and increasing unit costs; competitors with Russia overflight rights retain cost/time advantages. Dynamic flight planning and payload adjustments are required to mitigate block-time and fuel impacts.

- Added block time: ~1–2h

- Fuel burn increase: ~10–15%

- Lower aircraft productivity

- Need for dynamic replanning

HK policy support

Hong Kong policy support for aviation, cargo and tourism—through targeted incentives, slot and fee policies—remains a key determinant of Cathay Pacific’s recovery pace and operating costs; the Three-Runway System expands HKIA capacity to about 100 million passengers p.a., unlocking growth potential, while stable governance sustains investor confidence.

GBA integration and HK TRS spur recovery; US-China tensions and airspace limits raise costs

Political alignment with Beijing, GBA integration (≈86M pop, GDP ≈US$1.9tn) and HK policy (TRS 100M pax p.a.) drive market access and recovery; US–China tensions and sanctions raise compliance costs and dent demand (IATA 2024 RPKs ≈94% of 2019). Bilateral ASAs and limited Russia overflight rights (adds ~1–2h, +10–15% fuel) constrain capacity versus competitors; govt support remains critical.

| Metric | Value |

|---|---|

| Group fleet | ~200 aircraft |

| HKIA capacity | TRS 100M pax p.a. |

| HK intl capacity (late 2024) | ~70% of 2019 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Cathay Pacific Airways across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by data and region-specific regulatory context. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios ready for business plans, pitch decks and strategic decision-making.

Condensed PESTLE summary for Cathay Pacific highlighting key political, economic, social, technological, legal and environmental risks with clear implications and mitigation ideas for each. Ready-to-drop into presentations or planning sessions to speed decision-making and cross-team alignment.

Economic factors

Global demand cycles

Premium and corporate travel for Cathay tracks global GDP, with IMF projecting ~3% world growth for 2024–25, so corporate demand remains cyclical.

Air freight correlates with e-commerce (global online retail ~5.7 trillion USD in 2023) and manufacturing activity, driving cargo tonne-km swings.

Downturns compress yields and reopenings lift load factors; regional diversification across Asia, Europe and North America smooths volatility for Cathay.

Fuel price volatility

Jet fuel typically represents roughly 20–30% of airline operating costs, making price swings a key driver of Cathay Pacific’s margin volatility; spikes in 2022–24 pushed industry jet fuel prices up by about 20–40% year-on-year at points. Hedging policies aim to smooth cash-flow but introduce basis risk when spot/backspread moves diverge from hedged benchmarks. Route-level profitability can flip within weeks during fuel spikes, and more fuel-efficient widebodies (lower L/100km) act as a durable competitive moat when prices rise.

FX and HKD peg

Revenues at Cathay Pacific are multi-currency while major costs—jet fuel, aircraft leases and many financing contracts—are USD-linked, with jet fuel typically 20–30% of airline operating costs. The HKD–USD peg (HKMA Convertibility Zone 7.75–7.85) stabilizes local financing and interest-rate transmission but forces foreign-exchange translation volatility on non-HKD earnings. Currency moves affect pricing power and demand across Greater China and long-haul routes, so active treasury hedging and USD liquidity management remain critical.

Interest rates and debt

Higher interest rates lift lease and borrowing costs, squeezing margins on fleet renewal and making lessors push higher rents; Cathay Pacific’s refinancing windows and access to export credit are therefore critical to maintaining fleet plans. Strong balance sheet resilience determines flexibility in taking delivery or deferring orders, while disciplined capex timing preserves ROIC through rate cycles.

- Lease/borrowing sensitivity

- Refinancing & export credit importance

- Balance-sheet order flexibility

- Capex timing to protect ROIC

Hong Kong tourism recovery

Hong Kong tourism recovery is driving Cathay Pacific seat factors and network breadth as inbound arrivals surged after reopening, with visitor numbers climbing sharply in 2023–24 and GBA day‑trip and leisure demand from the Mainland pivotal to load factors and frequency restoration; airport capacity ramp‑up at HKIA enables scale, but competitive fares remain necessary to rebuild market share.

- Inbound/outbound flows: Mainland leisure fuels peak loads

- GBA connectivity: critical for point‑to‑point demand

- HKIA capacity: enables scalability vs 2019

- Pricing: discounted fares likely to regain share

GBA integration and HK TRS spur recovery; US-China tensions and airspace limits raise costs

Premium and corporate travel ties to IMF-projected ~3% world GDP growth for 2024–25, keeping corporate demand cyclical.

Air freight aligns with global e-commerce of ~5.7 trillion USD in 2023, driving cargo tonne-km volatility.

Jet fuel is ~20–30% of costs with 2022–24 price spikes of ~20–40% y/y; HKD peg 7.75–7.85 stabilizes local financing but adds FX translation risk.

| Metric | Value |

|---|---|

| Global GDP (IMF) | ~3% (2024–25) |

| Global e‑commerce (2023) | ~5.7T USD |

| Jet fuel share | 20–30% |

| Fuel spike (2022–24) | ~20–40% y/y |

| HKD–USD peg | 7.75–7.85 |

Preview Before You Purchase

Cathay Pacific Airways PESTLE Analysis

This Cathay Pacific Airways PESTLE Analysis examines political, economic, social, technological, legal and environmental factors affecting the carrier and offers actionable insights for strategy and risk management. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. You’ll download this same, final file immediately after payment.