China Distance Education Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

China Distance Education faces intense buyer bargaining, rising substitute threats from tech platforms, moderate supplier power for content and platforms, and steady pressure from new entrants and existing competitors. This snapshot highlights strategic risks and growth levers. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and tailored implications. Purchase the complete report to inform investment and strategy decisions.

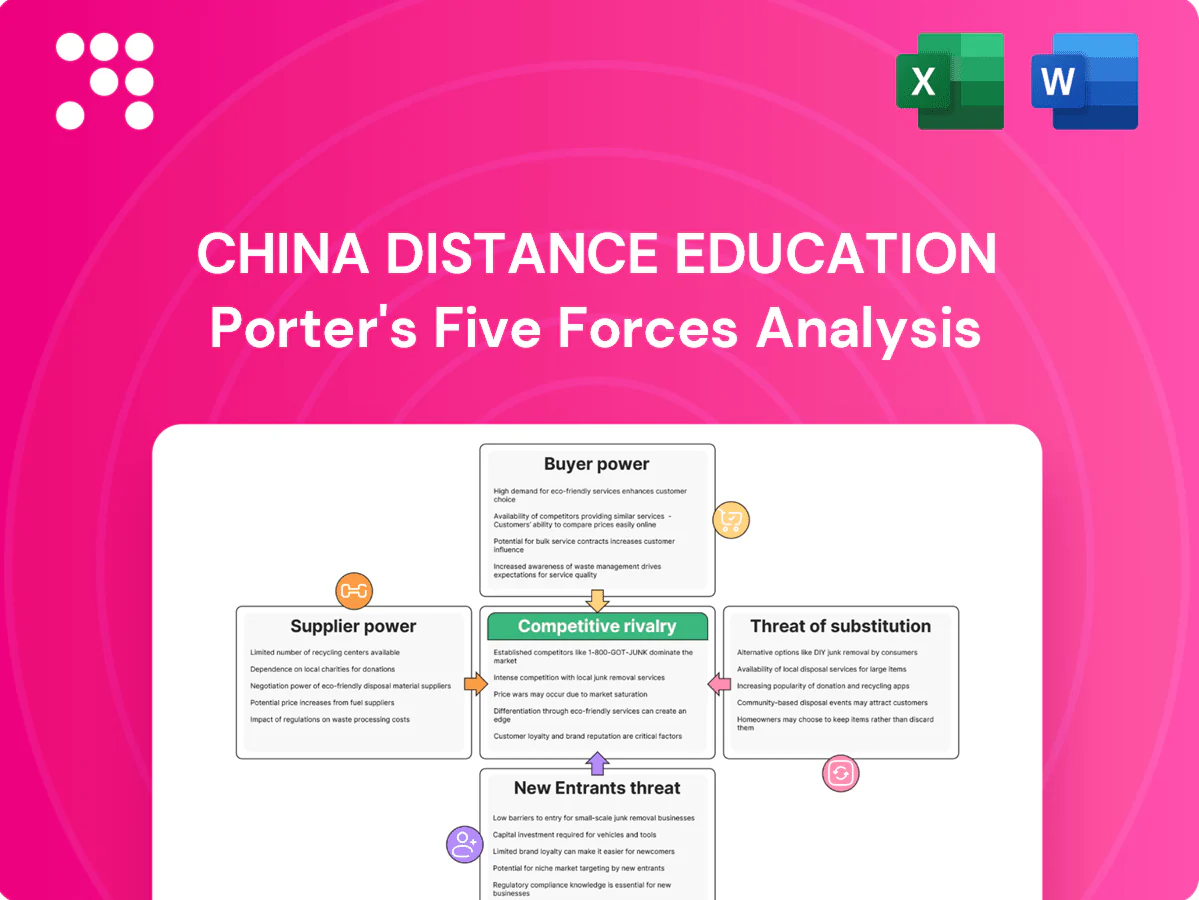

Suppliers Bargaining Power

Instructor and SME leverage

High-quality instructors and SMEs in accounting, healthcare and engineering are scarce, with 2024 industry data showing top specialists capture outsized demand. Leading SMEs can command premium fees or revenue shares up to ~40% on major platforms. Their reputation can double conversion and pass rates in marketing campaigns, raising platform dependence. Approximately 60% of top SMEs multi-home across platforms, increasing supplier bargaining power.

Exam body content alignment

Alignment with official syllabi and exam-authority updates is critical for China Distance Education given Gaokao 2024 registered about 12.07 million candidates, making content accuracy a revenue driver. Exam bodies, while not traditional suppliers, functionally supply inputs: delayed access to syllabus changes forces costly course rewrites and platform updates. Restricted or exclusive access deals competitors secure can raise relative supplier power and margin pressure.

Technology and cloud vendors

Reliance on CDN, cloud compute, streaming and proctoring vendors concentrates technical risk, as the top three cloud providers held about 67% of global IaaS/PaaS market in 2024 (AWS 33%, Azure 23%, GCP 11%), amplifying exposure to outages and price moves. Price escalations or tighter SLAs can compress margins; large customers report multi‑million-dollar annual cost increases when vendors reprice. Switching core infrastructure incurs significant migration costs and downtime risks, while vendor bundling of storage, AI and analytics deepens lock‑in and raises supplier influence.

Traffic platforms and app stores

Traffic platforms and app stores (Apple/Google commissions 15-30%) plus search engines and super-apps control distribution and fees for China distance-education players; algorithm shifts or higher ASA/SEM bids raise CAC and squeeze unit economics. Pay-to-play featured placements amplify platform leverage, and platform-mandated data/privacy rules increase compliance costs and dependency.

- Platform commission: 15-30%

- China mobile Internet users: ~1.07 billion (end 2023)

- ASA/SEM-driven CAC volatility: material impact on LTV/CAC

Content production tools and IP

Authoring tools, question banks and licensed textbooks are critical inputs for China distance education; in 2024 many K-12 must-have titles remained concentrated with state-backed publishers, boosting their leverage. License holders can raise royalties or restrict usage; proprietary item banks reduce supplier exposure but demand ongoing R&D and content refresh.

- Critical inputs: authoring tools, banks, textbooks

- 2024: must-have K-12 titles concentrated with few state publishers

- Risk: royalty hikes or usage limits

- Mitigation: build proprietary banks—higher capex/OPEX

Supplier power: top SMEs 60% multi-home; cloud fees squeeze margins

Supplier power is high: top SMEs capture outsized demand (60% multi-home; revenue shares up to ~40%), boosting fee and talent risk. Content access tied to exam bodies matters—Gaokao 2024 had 12.07M candidates—delays force costly rewrites. Tech and distribution concentration (AWS/Azure/GCP 33/23/11%; app-store fees 15–30%) raise switching costs and margin pressure.

| Supplier | Key metric (2024) |

|---|---|

| Top SMEs | 60% multi-home; rev share up to ~40% |

| Exam bodies | Gaokao candidates 12.07M |

| Cloud | AWS/Azure/GCP = 33/23/11% |

| Distribution | Commissions 15–30% |

What is included in the product

Tailored Porter's Five Forces analysis for China Distance Education uncovering key drivers of competition, customer influence, and market entry risks, with detailed assessment of supplier and buyer power. It identifies disruptive technologies, substitutes, and regulatory threats that shape pricing, profitability, and strategic positioning for investors and management.

A concise one-sheet Porter’s Five Forces for China distance education that visualizes competitive pressure with a spider chart and customizable inputs—easy to copy into decks and update for regulation or new entrants.

Customers Bargaining Power

Price-sensitive exam candidates

Individual learners routinely compare prices across platforms and offline centers, and with China hosting over 400 million online learners in 2024 buyers wield strong leverage; transparent pricing and concentrated promotions around Double 11/618 amplify this power. Elastic demand for non-mandatory certifications raises discount pressure, while bundles and financing help retention but many still anchor to budget options.

Low switching costs pre-commitment

Before enrolling, learners in China—part of a user base exceeding 200 million online learners—can freely trial multiple providers, keeping top-of-funnel churn high. Similar curricula across major platforms (K12, vocational, upskilling) make differentiation difficult, pressuring prices and promotions. Reported trial-to-paid conversion rates remain low, sustaining acquisition costs. Loyalty rises only after progress tracking and community features create measurable switching frictions.

Outcome-driven purchasing

Buyers prioritize pass rates, instructor pedigree and job outcomes, with 2024 industry surveys showing over 50% cite job placement or certification success as primary purchase drivers. Negative reviews or perceived low efficacy can shift demand rapidly; platforms report churn spikes up to 25% after high-profile failures. Refund guarantees tied to exam results, offered by about 30% of major providers in 2024, shift risk to providers, and transparent outcome data strengthens buyers’ negotiating leverage.

Institutional and enterprise clients

Institutional buyers such as hospitals, firms, and agencies buy cohort licenses, and large contracts—often structured as 3–5 year RFPs—raise buyer leverage through volume discounts and strict procurement terms that increase cost-to-serve via reporting and system integrations; however, multi-year deals stabilize revenue and typically lower CAC by locking renewal rates.

- High-volume RFPs drive discounting

- Procurement adds integration/reporting costs

- 3–5 year contracts reduce churn and CAC

Multi-homing and trial culture

Learners routinely multi-home, using apps, free videos and textbooks together, which reduces single-platform lock-in and raises customer bargaining power. Cross-platform note-taking and AI study tools accelerate switching and trial behaviour, forcing providers to compete on coaching, learning analytics and credential value. In 2024 China had about 1.04 billion mobile internet users, amplifying access to alternative resources.

- Multi-homing widespread

- AI tools enable switching

- Providers must offer coaching/analytics

Chinese learners wield pricing power: 400M+ users, 1.04B mobiles, 30% refund guarantees

Buyers in China exert strong leverage: 400M+ online learners in 2024 and 1.04B mobile users make price transparency and multi-homing widespread. About 30% of major providers offer refund-for-pass guarantees, shifting risk and raising negotiation power; churn can spike up to 25% after failures. Low trial-to-paid conversions keep acquisition costs high while institutional 3–5 year RFPs concentrate bargaining power.

| Metric | 2024 value | Implication |

|---|---|---|

| Online learners | 400M+ | High buyer base, price sensitivity |

| Mobile users | 1.04B | Easy switching/multi-homing |

| Refund guarantees | ~30% | Risk shifted to providers |

| Churn spike | Up to 25% | Reputation-sensitive demand |

Preview Before You Purchase

China Distance Education Porter's Five Forces Analysis

This preview shows the exact China Distance Education Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted, comprehensive and ready for immediate download and use. What you see here is precisely the deliverable you'll get instantly after buying.

Go Beyond the Preview—Access the Full Strategic Report

China Distance Education faces intense buyer bargaining, rising substitute threats from tech platforms, moderate supplier power for content and platforms, and steady pressure from new entrants and existing competitors. This snapshot highlights strategic risks and growth levers. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and tailored implications. Purchase the complete report to inform investment and strategy decisions.

Suppliers Bargaining Power

Instructor and SME leverage

High-quality instructors and SMEs in accounting, healthcare and engineering are scarce, with 2024 industry data showing top specialists capture outsized demand. Leading SMEs can command premium fees or revenue shares up to ~40% on major platforms. Their reputation can double conversion and pass rates in marketing campaigns, raising platform dependence. Approximately 60% of top SMEs multi-home across platforms, increasing supplier bargaining power.

Exam body content alignment

Alignment with official syllabi and exam-authority updates is critical for China Distance Education given Gaokao 2024 registered about 12.07 million candidates, making content accuracy a revenue driver. Exam bodies, while not traditional suppliers, functionally supply inputs: delayed access to syllabus changes forces costly course rewrites and platform updates. Restricted or exclusive access deals competitors secure can raise relative supplier power and margin pressure.

Technology and cloud vendors

Reliance on CDN, cloud compute, streaming and proctoring vendors concentrates technical risk, as the top three cloud providers held about 67% of global IaaS/PaaS market in 2024 (AWS 33%, Azure 23%, GCP 11%), amplifying exposure to outages and price moves. Price escalations or tighter SLAs can compress margins; large customers report multi‑million-dollar annual cost increases when vendors reprice. Switching core infrastructure incurs significant migration costs and downtime risks, while vendor bundling of storage, AI and analytics deepens lock‑in and raises supplier influence.

Traffic platforms and app stores

Traffic platforms and app stores (Apple/Google commissions 15-30%) plus search engines and super-apps control distribution and fees for China distance-education players; algorithm shifts or higher ASA/SEM bids raise CAC and squeeze unit economics. Pay-to-play featured placements amplify platform leverage, and platform-mandated data/privacy rules increase compliance costs and dependency.

- Platform commission: 15-30%

- China mobile Internet users: ~1.07 billion (end 2023)

- ASA/SEM-driven CAC volatility: material impact on LTV/CAC

Content production tools and IP

Authoring tools, question banks and licensed textbooks are critical inputs for China distance education; in 2024 many K-12 must-have titles remained concentrated with state-backed publishers, boosting their leverage. License holders can raise royalties or restrict usage; proprietary item banks reduce supplier exposure but demand ongoing R&D and content refresh.

- Critical inputs: authoring tools, banks, textbooks

- 2024: must-have K-12 titles concentrated with few state publishers

- Risk: royalty hikes or usage limits

- Mitigation: build proprietary banks—higher capex/OPEX

Supplier power: top SMEs 60% multi-home; cloud fees squeeze margins

Supplier power is high: top SMEs capture outsized demand (60% multi-home; revenue shares up to ~40%), boosting fee and talent risk. Content access tied to exam bodies matters—Gaokao 2024 had 12.07M candidates—delays force costly rewrites. Tech and distribution concentration (AWS/Azure/GCP 33/23/11%; app-store fees 15–30%) raise switching costs and margin pressure.

| Supplier | Key metric (2024) |

|---|---|

| Top SMEs | 60% multi-home; rev share up to ~40% |

| Exam bodies | Gaokao candidates 12.07M |

| Cloud | AWS/Azure/GCP = 33/23/11% |

| Distribution | Commissions 15–30% |

What is included in the product

Tailored Porter's Five Forces analysis for China Distance Education uncovering key drivers of competition, customer influence, and market entry risks, with detailed assessment of supplier and buyer power. It identifies disruptive technologies, substitutes, and regulatory threats that shape pricing, profitability, and strategic positioning for investors and management.

A concise one-sheet Porter’s Five Forces for China distance education that visualizes competitive pressure with a spider chart and customizable inputs—easy to copy into decks and update for regulation or new entrants.

Customers Bargaining Power

Price-sensitive exam candidates

Individual learners routinely compare prices across platforms and offline centers, and with China hosting over 400 million online learners in 2024 buyers wield strong leverage; transparent pricing and concentrated promotions around Double 11/618 amplify this power. Elastic demand for non-mandatory certifications raises discount pressure, while bundles and financing help retention but many still anchor to budget options.

Low switching costs pre-commitment

Before enrolling, learners in China—part of a user base exceeding 200 million online learners—can freely trial multiple providers, keeping top-of-funnel churn high. Similar curricula across major platforms (K12, vocational, upskilling) make differentiation difficult, pressuring prices and promotions. Reported trial-to-paid conversion rates remain low, sustaining acquisition costs. Loyalty rises only after progress tracking and community features create measurable switching frictions.

Outcome-driven purchasing

Buyers prioritize pass rates, instructor pedigree and job outcomes, with 2024 industry surveys showing over 50% cite job placement or certification success as primary purchase drivers. Negative reviews or perceived low efficacy can shift demand rapidly; platforms report churn spikes up to 25% after high-profile failures. Refund guarantees tied to exam results, offered by about 30% of major providers in 2024, shift risk to providers, and transparent outcome data strengthens buyers’ negotiating leverage.

Institutional and enterprise clients

Institutional buyers such as hospitals, firms, and agencies buy cohort licenses, and large contracts—often structured as 3–5 year RFPs—raise buyer leverage through volume discounts and strict procurement terms that increase cost-to-serve via reporting and system integrations; however, multi-year deals stabilize revenue and typically lower CAC by locking renewal rates.

- High-volume RFPs drive discounting

- Procurement adds integration/reporting costs

- 3–5 year contracts reduce churn and CAC

Multi-homing and trial culture

Learners routinely multi-home, using apps, free videos and textbooks together, which reduces single-platform lock-in and raises customer bargaining power. Cross-platform note-taking and AI study tools accelerate switching and trial behaviour, forcing providers to compete on coaching, learning analytics and credential value. In 2024 China had about 1.04 billion mobile internet users, amplifying access to alternative resources.

- Multi-homing widespread

- AI tools enable switching

- Providers must offer coaching/analytics

Chinese learners wield pricing power: 400M+ users, 1.04B mobiles, 30% refund guarantees

Buyers in China exert strong leverage: 400M+ online learners in 2024 and 1.04B mobile users make price transparency and multi-homing widespread. About 30% of major providers offer refund-for-pass guarantees, shifting risk and raising negotiation power; churn can spike up to 25% after failures. Low trial-to-paid conversions keep acquisition costs high while institutional 3–5 year RFPs concentrate bargaining power.

| Metric | 2024 value | Implication |

|---|---|---|

| Online learners | 400M+ | High buyer base, price sensitivity |

| Mobile users | 1.04B | Easy switching/multi-homing |

| Refund guarantees | ~30% | Risk shifted to providers |

| Churn spike | Up to 25% | Reputation-sensitive demand |

Preview Before You Purchase

China Distance Education Porter's Five Forces Analysis

This preview shows the exact China Distance Education Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted, comprehensive and ready for immediate download and use. What you see here is precisely the deliverable you'll get instantly after buying.

Description

Go Beyond the Preview—Access the Full Strategic Report

China Distance Education faces intense buyer bargaining, rising substitute threats from tech platforms, moderate supplier power for content and platforms, and steady pressure from new entrants and existing competitors. This snapshot highlights strategic risks and growth levers. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and tailored implications. Purchase the complete report to inform investment and strategy decisions.

Suppliers Bargaining Power

Instructor and SME leverage

High-quality instructors and SMEs in accounting, healthcare and engineering are scarce, with 2024 industry data showing top specialists capture outsized demand. Leading SMEs can command premium fees or revenue shares up to ~40% on major platforms. Their reputation can double conversion and pass rates in marketing campaigns, raising platform dependence. Approximately 60% of top SMEs multi-home across platforms, increasing supplier bargaining power.

Exam body content alignment

Alignment with official syllabi and exam-authority updates is critical for China Distance Education given Gaokao 2024 registered about 12.07 million candidates, making content accuracy a revenue driver. Exam bodies, while not traditional suppliers, functionally supply inputs: delayed access to syllabus changes forces costly course rewrites and platform updates. Restricted or exclusive access deals competitors secure can raise relative supplier power and margin pressure.

Technology and cloud vendors

Reliance on CDN, cloud compute, streaming and proctoring vendors concentrates technical risk, as the top three cloud providers held about 67% of global IaaS/PaaS market in 2024 (AWS 33%, Azure 23%, GCP 11%), amplifying exposure to outages and price moves. Price escalations or tighter SLAs can compress margins; large customers report multi‑million-dollar annual cost increases when vendors reprice. Switching core infrastructure incurs significant migration costs and downtime risks, while vendor bundling of storage, AI and analytics deepens lock‑in and raises supplier influence.

Traffic platforms and app stores

Traffic platforms and app stores (Apple/Google commissions 15-30%) plus search engines and super-apps control distribution and fees for China distance-education players; algorithm shifts or higher ASA/SEM bids raise CAC and squeeze unit economics. Pay-to-play featured placements amplify platform leverage, and platform-mandated data/privacy rules increase compliance costs and dependency.

- Platform commission: 15-30%

- China mobile Internet users: ~1.07 billion (end 2023)

- ASA/SEM-driven CAC volatility: material impact on LTV/CAC

Content production tools and IP

Authoring tools, question banks and licensed textbooks are critical inputs for China distance education; in 2024 many K-12 must-have titles remained concentrated with state-backed publishers, boosting their leverage. License holders can raise royalties or restrict usage; proprietary item banks reduce supplier exposure but demand ongoing R&D and content refresh.

- Critical inputs: authoring tools, banks, textbooks

- 2024: must-have K-12 titles concentrated with few state publishers

- Risk: royalty hikes or usage limits

- Mitigation: build proprietary banks—higher capex/OPEX

Supplier power: top SMEs 60% multi-home; cloud fees squeeze margins

Supplier power is high: top SMEs capture outsized demand (60% multi-home; revenue shares up to ~40%), boosting fee and talent risk. Content access tied to exam bodies matters—Gaokao 2024 had 12.07M candidates—delays force costly rewrites. Tech and distribution concentration (AWS/Azure/GCP 33/23/11%; app-store fees 15–30%) raise switching costs and margin pressure.

| Supplier | Key metric (2024) |

|---|---|

| Top SMEs | 60% multi-home; rev share up to ~40% |

| Exam bodies | Gaokao candidates 12.07M |

| Cloud | AWS/Azure/GCP = 33/23/11% |

| Distribution | Commissions 15–30% |

What is included in the product

Tailored Porter's Five Forces analysis for China Distance Education uncovering key drivers of competition, customer influence, and market entry risks, with detailed assessment of supplier and buyer power. It identifies disruptive technologies, substitutes, and regulatory threats that shape pricing, profitability, and strategic positioning for investors and management.

A concise one-sheet Porter’s Five Forces for China distance education that visualizes competitive pressure with a spider chart and customizable inputs—easy to copy into decks and update for regulation or new entrants.

Customers Bargaining Power

Price-sensitive exam candidates

Individual learners routinely compare prices across platforms and offline centers, and with China hosting over 400 million online learners in 2024 buyers wield strong leverage; transparent pricing and concentrated promotions around Double 11/618 amplify this power. Elastic demand for non-mandatory certifications raises discount pressure, while bundles and financing help retention but many still anchor to budget options.

Low switching costs pre-commitment

Before enrolling, learners in China—part of a user base exceeding 200 million online learners—can freely trial multiple providers, keeping top-of-funnel churn high. Similar curricula across major platforms (K12, vocational, upskilling) make differentiation difficult, pressuring prices and promotions. Reported trial-to-paid conversion rates remain low, sustaining acquisition costs. Loyalty rises only after progress tracking and community features create measurable switching frictions.

Outcome-driven purchasing

Buyers prioritize pass rates, instructor pedigree and job outcomes, with 2024 industry surveys showing over 50% cite job placement or certification success as primary purchase drivers. Negative reviews or perceived low efficacy can shift demand rapidly; platforms report churn spikes up to 25% after high-profile failures. Refund guarantees tied to exam results, offered by about 30% of major providers in 2024, shift risk to providers, and transparent outcome data strengthens buyers’ negotiating leverage.

Institutional and enterprise clients

Institutional buyers such as hospitals, firms, and agencies buy cohort licenses, and large contracts—often structured as 3–5 year RFPs—raise buyer leverage through volume discounts and strict procurement terms that increase cost-to-serve via reporting and system integrations; however, multi-year deals stabilize revenue and typically lower CAC by locking renewal rates.

- High-volume RFPs drive discounting

- Procurement adds integration/reporting costs

- 3–5 year contracts reduce churn and CAC

Multi-homing and trial culture

Learners routinely multi-home, using apps, free videos and textbooks together, which reduces single-platform lock-in and raises customer bargaining power. Cross-platform note-taking and AI study tools accelerate switching and trial behaviour, forcing providers to compete on coaching, learning analytics and credential value. In 2024 China had about 1.04 billion mobile internet users, amplifying access to alternative resources.

- Multi-homing widespread

- AI tools enable switching

- Providers must offer coaching/analytics

Chinese learners wield pricing power: 400M+ users, 1.04B mobiles, 30% refund guarantees

Buyers in China exert strong leverage: 400M+ online learners in 2024 and 1.04B mobile users make price transparency and multi-homing widespread. About 30% of major providers offer refund-for-pass guarantees, shifting risk and raising negotiation power; churn can spike up to 25% after failures. Low trial-to-paid conversions keep acquisition costs high while institutional 3–5 year RFPs concentrate bargaining power.

| Metric | 2024 value | Implication |

|---|---|---|

| Online learners | 400M+ | High buyer base, price sensitivity |

| Mobile users | 1.04B | Easy switching/multi-homing |

| Refund guarantees | ~30% | Risk shifted to providers |

| Churn spike | Up to 25% | Reputation-sensitive demand |

Preview Before You Purchase

China Distance Education Porter's Five Forces Analysis

This preview shows the exact China Distance Education Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted, comprehensive and ready for immediate download and use. What you see here is precisely the deliverable you'll get instantly after buying.