China Eastern Airlines Porter's Five Forces Analysis

From Overview to Strategy Blueprint

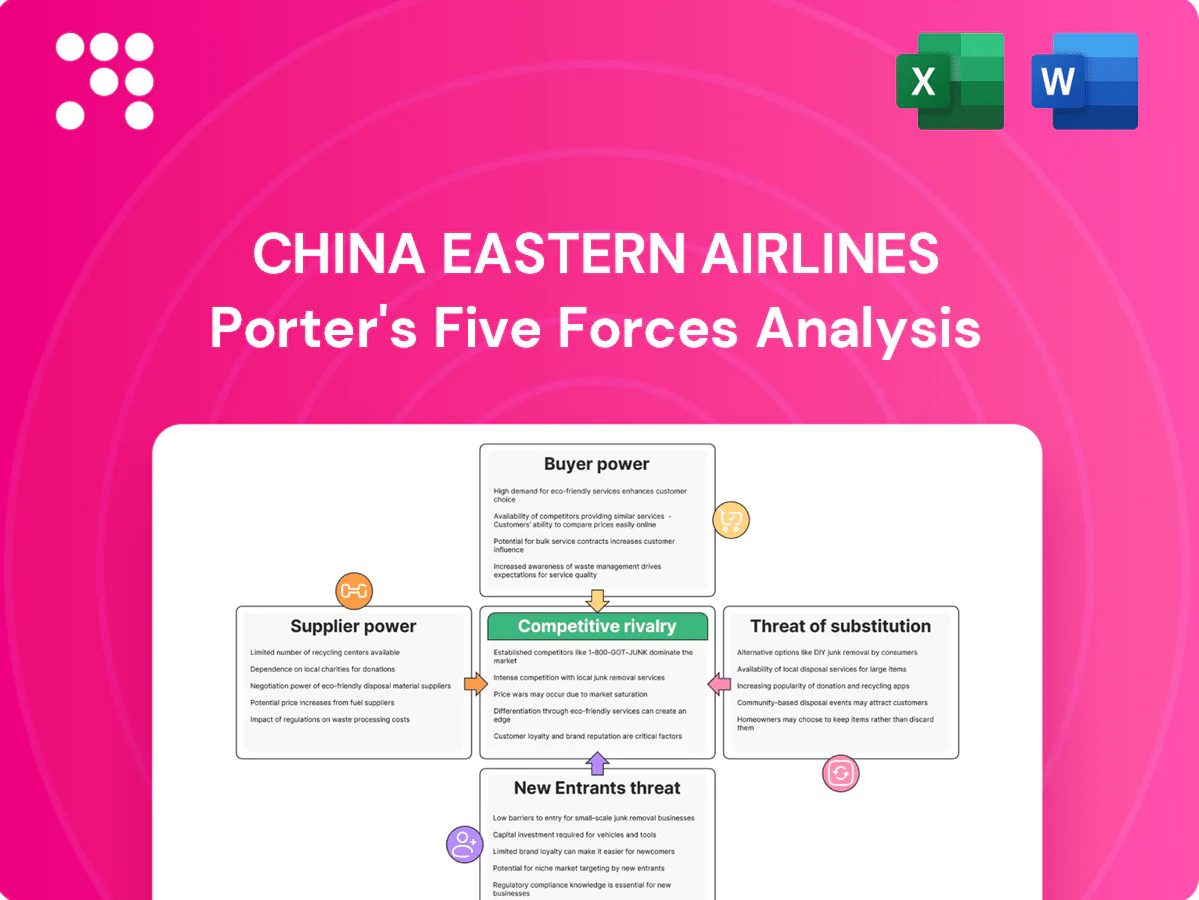

China Eastern faces intense industry rivalry, high capital and regulatory barriers, moderate supplier influence, rising buyer expectations, and limited close substitutes—factors that shape its margin and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Aircraft/engine duopoly

China Eastern relies on an Airbus/Boeing duopoly (together supplying roughly 85–90% of large commercial jets) plus a few engine makers, concentrating bargaining power with suppliers. Long type-certification and limited alternative models (typically 3–5 years) constrain switching; volume discounts lower unit cost but cannot offset supplier leverage on pricing, delivery slots and after-sales terms. The COMAC C919, in service since 2022 with limited production scale, marginally diversifies options but remains small relative to the duopoly.

Jet fuel volatility

Jet fuel is sourced from a few large, state-linked suppliers (CNPC, Sinopec, CNOOC) that together control roughly 70% of China’s refining capacity, giving them clear pricing influence. Price swings (IATA average jet fuel ~ $123/barrel in 2024) pass through quickly and China Eastern’s hedging scope has been limited, constraining protection. Scale secures delivery but not price relief; regulated, demand-sensitive fuel surcharges only partially offset costs.

Airport/slot dependence

Access to gateway airports and peak slots is tightly controlled, giving airports and regulators quasi-supplier power over China Eastern. Scarce slots at PVG, SHA, PEK and CAN raise operating costs and limit scheduling flexibility. Negotiation leverage is constrained by CAAC public-interest allocation rules. Alliance ties and state relationships improve access but do not remove slot scarcity.

MRO and parts control

OEM-controlled maintenance and proprietary parts keep lifecycle costs high for China Eastern, which operated roughly 700 aircraft in 2024, and power-by-the-hour and warranty contracts further lock the carrier into OEM ecosystems. In-house MRO facilities and joint ventures reduce some dependence, but life‑limited rotables and OEM-only LRUs remain captive; AOG delays can cascade across the network.

- High OEM leverage on parts and MRO

- Power-by-the-hour ties fleet to suppliers

- In-house MRO/JVs mitigate but do not eliminate risk

- AOG delays cause network-wide disruption

Pilot/crew labor

Pilots and skilled technicians are scarce in China, giving them significant bargaining clout over China Eastern; training pipelines last 18–24 months and require costly simulators and type ratings, limiting rapid capacity adjustments. Wage inflation and rostering constraints raise unit crew costs, while state coordination tempers disputes but does not remove structural scarcity.

- Pilot/technician scarcity → higher bargaining power

- Training 18–24 months → limited supply flexibility

- Wage inflation & rostering ↑ unit costs; state mediation reduces but does not solve scarcity

Duopoly 85-90% + fuel $123/bbl squeeze carriers

China Eastern faces concentrated supplier leverage: Airbus/Boeing supply ~85–90% of large jets, OEMs control parts/MRO for its ~700-aircraft fleet (2024), and COMAC C919 offers limited relief. Jet fuel sourced from CNPC/Sinopec/CNOOC (~70% domestic refining) — IATA jet fuel ≈ $123/barrel (2024) — passes costs quickly. Airport slots, pilot/technician shortages (18–24 month training) and OEM warranty/PPH contracts preserve supplier power.

| Metric | 2024 value |

|---|---|

| Airframe duopoly share | 85–90% |

| Fleet size | ≈700 |

| Domestic refining share (major suppliers) | ≈70% |

| IATA jet fuel avg | $123/barrel |

| Pilot/tech training | 18–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for China Eastern Airlines highlighting competitive rivalry, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/operational barriers that shape pricing, profitability, and strategic positioning within the Chinese and international aviation market.

A one-sheet Porter's Five Forces analysis for China Eastern Airlines—clear radar chart and editable pressure levels to quickly assess competitive intensity, regulatory risk, fleet/supplier power and route barriers; copy-ready layout for decks, duplicate scenarios and seamless Excel/Word integration for fast boardroom decisions.

Customers Bargaining Power

Price-sensitive leisure

Mass-market leisure travelers in China are highly price elastic, driving intense fare competition and pressuring China Eastern to match discounting; domestic leisure yield volatility rose in 2024 with promotional load-driven revenue swings. OTAs and metasearch platforms (dominant distribution channels) enable instant price comparisons, raising customer bargaining power. Ancillary upselling (baggage, seat, F&B) recovered part of margin but remained discretionary, contributing a mid-single-digit share of non-ticket revenue. Load factors hinge on dynamic pricing and targeted promotions to fill seats during off-peak periods.

Corporate/government accounts

Large corporate and public-sector buyers secure volume contracts and SLAs that in 2024 commonly delivered negotiated discounts of roughly 10–25%, stabilizing demand but compressing yields on trunk routes. China Eastern leverages schedule breadth and loyalty programmes to retain accounts, yet operational disruptions risk contract penalties and rapid share loss to competitors.

Channel intermediaries

OTAs, GDS and super-apps aggregate demand and exert fee pressure—Trip.com Group held roughly 60% of China’s OTA bookings in 2023—while algorithmic sorting can demote higher-fare options, squeezing yields for China Eastern. Direct channels and early NDC adoption (still under ~20% among carriers by 2024) reclaim some control, yet persistent distribution fragmentation keeps intermediary power relevant.

Loyalty switching costs

SkyTeam membership and frequent‑flyer benefits create tangible switching frictions for China Eastern’s high‑value flyers, leveraging alliance access to over 1,000 destinations in 170 countries and co‑branded card tie‑ups with major Chinese banks such as ICBC to reduce marginal buyer power. Elite perks and lounge access strengthen retention, but status‑match programs and overlapping alliance routes (Delta, Air France‑KLM) limit full lock‑in; service reliability remains decisive for premium segments.

- SkyTeam reach: 1,000+ destinations, 170+ countries

- Co‑brand cards: partnerships with ICBC (reduces churn)

- Alliance overlap: Delta, Air France‑KLM (enables switches)

- Key driver: service reliability for high‑value travelers

Service quality expectations

Buyers demand punctuality, clean cabins and flexible refund/reticket rules; China Eastern's service quality directly affects perceived value and repeat purchase, with on-time performance cited at 79.4% in 2024 and NPS pressures rising post-pandemic. Social media amplifies complaints—viral incidents magnify reputational risk—while inconsistency between domestic and international legs depresses retention.

- Punctuality: 79.4% (2024)

- Cleanliness & policies: drive perceived value

- Social media: raises reputational leverage

- Consistency: key to retention

Price-elastic leisure demand fuels fare competition; OTAs dominate, ancillaries recover

Leisure demand is highly price‑elastic, driving fare competition and yield volatility; ancillary sales recovered to a mid‑single‑digit share of non‑ticket revenue in 2024. Large buyers secured negotiated discounts of ~10–25% in 2024, stabilizing volumes but compressing trunk yields. OTAs (Trip.com ~60% of OTA bookings 2023) and low NDC adoption (<20% in 2024) sustain intermediary bargaining power; on‑time performance 79.4% (2024).

| Metric | Value | Year |

|---|---|---|

| Trip.com OTA share | ~60% | 2023 |

| On‑time performance | 79.4% | 2024 |

| Corporate discounts | 10–25% | 2024 |

| NDC adoption | <20% | 2024 |

| Ancillary revenue share | Mid single‑digit % | 2024 |

Preview Before You Purchase

China Eastern Airlines Porter's Five Forces Analysis

This preview shows the exact China Eastern Airlines Porter's Five Forces analysis you'll receive after purchase—no placeholders. The document covers supplier and buyer power, competitive rivalry, and threats of entry and substitutes, with data-driven insights and strategic implications. It's fully formatted and ready for immediate download.

From Overview to Strategy Blueprint

China Eastern faces intense industry rivalry, high capital and regulatory barriers, moderate supplier influence, rising buyer expectations, and limited close substitutes—factors that shape its margin and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Aircraft/engine duopoly

China Eastern relies on an Airbus/Boeing duopoly (together supplying roughly 85–90% of large commercial jets) plus a few engine makers, concentrating bargaining power with suppliers. Long type-certification and limited alternative models (typically 3–5 years) constrain switching; volume discounts lower unit cost but cannot offset supplier leverage on pricing, delivery slots and after-sales terms. The COMAC C919, in service since 2022 with limited production scale, marginally diversifies options but remains small relative to the duopoly.

Jet fuel volatility

Jet fuel is sourced from a few large, state-linked suppliers (CNPC, Sinopec, CNOOC) that together control roughly 70% of China’s refining capacity, giving them clear pricing influence. Price swings (IATA average jet fuel ~ $123/barrel in 2024) pass through quickly and China Eastern’s hedging scope has been limited, constraining protection. Scale secures delivery but not price relief; regulated, demand-sensitive fuel surcharges only partially offset costs.

Airport/slot dependence

Access to gateway airports and peak slots is tightly controlled, giving airports and regulators quasi-supplier power over China Eastern. Scarce slots at PVG, SHA, PEK and CAN raise operating costs and limit scheduling flexibility. Negotiation leverage is constrained by CAAC public-interest allocation rules. Alliance ties and state relationships improve access but do not remove slot scarcity.

MRO and parts control

OEM-controlled maintenance and proprietary parts keep lifecycle costs high for China Eastern, which operated roughly 700 aircraft in 2024, and power-by-the-hour and warranty contracts further lock the carrier into OEM ecosystems. In-house MRO facilities and joint ventures reduce some dependence, but life‑limited rotables and OEM-only LRUs remain captive; AOG delays can cascade across the network.

- High OEM leverage on parts and MRO

- Power-by-the-hour ties fleet to suppliers

- In-house MRO/JVs mitigate but do not eliminate risk

- AOG delays cause network-wide disruption

Pilot/crew labor

Pilots and skilled technicians are scarce in China, giving them significant bargaining clout over China Eastern; training pipelines last 18–24 months and require costly simulators and type ratings, limiting rapid capacity adjustments. Wage inflation and rostering constraints raise unit crew costs, while state coordination tempers disputes but does not remove structural scarcity.

- Pilot/technician scarcity → higher bargaining power

- Training 18–24 months → limited supply flexibility

- Wage inflation & rostering ↑ unit costs; state mediation reduces but does not solve scarcity

Duopoly 85-90% + fuel $123/bbl squeeze carriers

China Eastern faces concentrated supplier leverage: Airbus/Boeing supply ~85–90% of large jets, OEMs control parts/MRO for its ~700-aircraft fleet (2024), and COMAC C919 offers limited relief. Jet fuel sourced from CNPC/Sinopec/CNOOC (~70% domestic refining) — IATA jet fuel ≈ $123/barrel (2024) — passes costs quickly. Airport slots, pilot/technician shortages (18–24 month training) and OEM warranty/PPH contracts preserve supplier power.

| Metric | 2024 value |

|---|---|

| Airframe duopoly share | 85–90% |

| Fleet size | ≈700 |

| Domestic refining share (major suppliers) | ≈70% |

| IATA jet fuel avg | $123/barrel |

| Pilot/tech training | 18–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for China Eastern Airlines highlighting competitive rivalry, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/operational barriers that shape pricing, profitability, and strategic positioning within the Chinese and international aviation market.

A one-sheet Porter's Five Forces analysis for China Eastern Airlines—clear radar chart and editable pressure levels to quickly assess competitive intensity, regulatory risk, fleet/supplier power and route barriers; copy-ready layout for decks, duplicate scenarios and seamless Excel/Word integration for fast boardroom decisions.

Customers Bargaining Power

Price-sensitive leisure

Mass-market leisure travelers in China are highly price elastic, driving intense fare competition and pressuring China Eastern to match discounting; domestic leisure yield volatility rose in 2024 with promotional load-driven revenue swings. OTAs and metasearch platforms (dominant distribution channels) enable instant price comparisons, raising customer bargaining power. Ancillary upselling (baggage, seat, F&B) recovered part of margin but remained discretionary, contributing a mid-single-digit share of non-ticket revenue. Load factors hinge on dynamic pricing and targeted promotions to fill seats during off-peak periods.

Corporate/government accounts

Large corporate and public-sector buyers secure volume contracts and SLAs that in 2024 commonly delivered negotiated discounts of roughly 10–25%, stabilizing demand but compressing yields on trunk routes. China Eastern leverages schedule breadth and loyalty programmes to retain accounts, yet operational disruptions risk contract penalties and rapid share loss to competitors.

Channel intermediaries

OTAs, GDS and super-apps aggregate demand and exert fee pressure—Trip.com Group held roughly 60% of China’s OTA bookings in 2023—while algorithmic sorting can demote higher-fare options, squeezing yields for China Eastern. Direct channels and early NDC adoption (still under ~20% among carriers by 2024) reclaim some control, yet persistent distribution fragmentation keeps intermediary power relevant.

Loyalty switching costs

SkyTeam membership and frequent‑flyer benefits create tangible switching frictions for China Eastern’s high‑value flyers, leveraging alliance access to over 1,000 destinations in 170 countries and co‑branded card tie‑ups with major Chinese banks such as ICBC to reduce marginal buyer power. Elite perks and lounge access strengthen retention, but status‑match programs and overlapping alliance routes (Delta, Air France‑KLM) limit full lock‑in; service reliability remains decisive for premium segments.

- SkyTeam reach: 1,000+ destinations, 170+ countries

- Co‑brand cards: partnerships with ICBC (reduces churn)

- Alliance overlap: Delta, Air France‑KLM (enables switches)

- Key driver: service reliability for high‑value travelers

Service quality expectations

Buyers demand punctuality, clean cabins and flexible refund/reticket rules; China Eastern's service quality directly affects perceived value and repeat purchase, with on-time performance cited at 79.4% in 2024 and NPS pressures rising post-pandemic. Social media amplifies complaints—viral incidents magnify reputational risk—while inconsistency between domestic and international legs depresses retention.

- Punctuality: 79.4% (2024)

- Cleanliness & policies: drive perceived value

- Social media: raises reputational leverage

- Consistency: key to retention

Price-elastic leisure demand fuels fare competition; OTAs dominate, ancillaries recover

Leisure demand is highly price‑elastic, driving fare competition and yield volatility; ancillary sales recovered to a mid‑single‑digit share of non‑ticket revenue in 2024. Large buyers secured negotiated discounts of ~10–25% in 2024, stabilizing volumes but compressing trunk yields. OTAs (Trip.com ~60% of OTA bookings 2023) and low NDC adoption (<20% in 2024) sustain intermediary bargaining power; on‑time performance 79.4% (2024).

| Metric | Value | Year |

|---|---|---|

| Trip.com OTA share | ~60% | 2023 |

| On‑time performance | 79.4% | 2024 |

| Corporate discounts | 10–25% | 2024 |

| NDC adoption | <20% | 2024 |

| Ancillary revenue share | Mid single‑digit % | 2024 |

Preview Before You Purchase

China Eastern Airlines Porter's Five Forces Analysis

This preview shows the exact China Eastern Airlines Porter's Five Forces analysis you'll receive after purchase—no placeholders. The document covers supplier and buyer power, competitive rivalry, and threats of entry and substitutes, with data-driven insights and strategic implications. It's fully formatted and ready for immediate download.

Description

From Overview to Strategy Blueprint

China Eastern faces intense industry rivalry, high capital and regulatory barriers, moderate supplier influence, rising buyer expectations, and limited close substitutes—factors that shape its margin and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Aircraft/engine duopoly

China Eastern relies on an Airbus/Boeing duopoly (together supplying roughly 85–90% of large commercial jets) plus a few engine makers, concentrating bargaining power with suppliers. Long type-certification and limited alternative models (typically 3–5 years) constrain switching; volume discounts lower unit cost but cannot offset supplier leverage on pricing, delivery slots and after-sales terms. The COMAC C919, in service since 2022 with limited production scale, marginally diversifies options but remains small relative to the duopoly.

Jet fuel volatility

Jet fuel is sourced from a few large, state-linked suppliers (CNPC, Sinopec, CNOOC) that together control roughly 70% of China’s refining capacity, giving them clear pricing influence. Price swings (IATA average jet fuel ~ $123/barrel in 2024) pass through quickly and China Eastern’s hedging scope has been limited, constraining protection. Scale secures delivery but not price relief; regulated, demand-sensitive fuel surcharges only partially offset costs.

Airport/slot dependence

Access to gateway airports and peak slots is tightly controlled, giving airports and regulators quasi-supplier power over China Eastern. Scarce slots at PVG, SHA, PEK and CAN raise operating costs and limit scheduling flexibility. Negotiation leverage is constrained by CAAC public-interest allocation rules. Alliance ties and state relationships improve access but do not remove slot scarcity.

MRO and parts control

OEM-controlled maintenance and proprietary parts keep lifecycle costs high for China Eastern, which operated roughly 700 aircraft in 2024, and power-by-the-hour and warranty contracts further lock the carrier into OEM ecosystems. In-house MRO facilities and joint ventures reduce some dependence, but life‑limited rotables and OEM-only LRUs remain captive; AOG delays can cascade across the network.

- High OEM leverage on parts and MRO

- Power-by-the-hour ties fleet to suppliers

- In-house MRO/JVs mitigate but do not eliminate risk

- AOG delays cause network-wide disruption

Pilot/crew labor

Pilots and skilled technicians are scarce in China, giving them significant bargaining clout over China Eastern; training pipelines last 18–24 months and require costly simulators and type ratings, limiting rapid capacity adjustments. Wage inflation and rostering constraints raise unit crew costs, while state coordination tempers disputes but does not remove structural scarcity.

- Pilot/technician scarcity → higher bargaining power

- Training 18–24 months → limited supply flexibility

- Wage inflation & rostering ↑ unit costs; state mediation reduces but does not solve scarcity

Duopoly 85-90% + fuel $123/bbl squeeze carriers

China Eastern faces concentrated supplier leverage: Airbus/Boeing supply ~85–90% of large jets, OEMs control parts/MRO for its ~700-aircraft fleet (2024), and COMAC C919 offers limited relief. Jet fuel sourced from CNPC/Sinopec/CNOOC (~70% domestic refining) — IATA jet fuel ≈ $123/barrel (2024) — passes costs quickly. Airport slots, pilot/technician shortages (18–24 month training) and OEM warranty/PPH contracts preserve supplier power.

| Metric | 2024 value |

|---|---|

| Airframe duopoly share | 85–90% |

| Fleet size | ≈700 |

| Domestic refining share (major suppliers) | ≈70% |

| IATA jet fuel avg | $123/barrel |

| Pilot/tech training | 18–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for China Eastern Airlines highlighting competitive rivalry, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/operational barriers that shape pricing, profitability, and strategic positioning within the Chinese and international aviation market.

A one-sheet Porter's Five Forces analysis for China Eastern Airlines—clear radar chart and editable pressure levels to quickly assess competitive intensity, regulatory risk, fleet/supplier power and route barriers; copy-ready layout for decks, duplicate scenarios and seamless Excel/Word integration for fast boardroom decisions.

Customers Bargaining Power

Price-sensitive leisure

Mass-market leisure travelers in China are highly price elastic, driving intense fare competition and pressuring China Eastern to match discounting; domestic leisure yield volatility rose in 2024 with promotional load-driven revenue swings. OTAs and metasearch platforms (dominant distribution channels) enable instant price comparisons, raising customer bargaining power. Ancillary upselling (baggage, seat, F&B) recovered part of margin but remained discretionary, contributing a mid-single-digit share of non-ticket revenue. Load factors hinge on dynamic pricing and targeted promotions to fill seats during off-peak periods.

Corporate/government accounts

Large corporate and public-sector buyers secure volume contracts and SLAs that in 2024 commonly delivered negotiated discounts of roughly 10–25%, stabilizing demand but compressing yields on trunk routes. China Eastern leverages schedule breadth and loyalty programmes to retain accounts, yet operational disruptions risk contract penalties and rapid share loss to competitors.

Channel intermediaries

OTAs, GDS and super-apps aggregate demand and exert fee pressure—Trip.com Group held roughly 60% of China’s OTA bookings in 2023—while algorithmic sorting can demote higher-fare options, squeezing yields for China Eastern. Direct channels and early NDC adoption (still under ~20% among carriers by 2024) reclaim some control, yet persistent distribution fragmentation keeps intermediary power relevant.

Loyalty switching costs

SkyTeam membership and frequent‑flyer benefits create tangible switching frictions for China Eastern’s high‑value flyers, leveraging alliance access to over 1,000 destinations in 170 countries and co‑branded card tie‑ups with major Chinese banks such as ICBC to reduce marginal buyer power. Elite perks and lounge access strengthen retention, but status‑match programs and overlapping alliance routes (Delta, Air France‑KLM) limit full lock‑in; service reliability remains decisive for premium segments.

- SkyTeam reach: 1,000+ destinations, 170+ countries

- Co‑brand cards: partnerships with ICBC (reduces churn)

- Alliance overlap: Delta, Air France‑KLM (enables switches)

- Key driver: service reliability for high‑value travelers

Service quality expectations

Buyers demand punctuality, clean cabins and flexible refund/reticket rules; China Eastern's service quality directly affects perceived value and repeat purchase, with on-time performance cited at 79.4% in 2024 and NPS pressures rising post-pandemic. Social media amplifies complaints—viral incidents magnify reputational risk—while inconsistency between domestic and international legs depresses retention.

- Punctuality: 79.4% (2024)

- Cleanliness & policies: drive perceived value

- Social media: raises reputational leverage

- Consistency: key to retention

Price-elastic leisure demand fuels fare competition; OTAs dominate, ancillaries recover

Leisure demand is highly price‑elastic, driving fare competition and yield volatility; ancillary sales recovered to a mid‑single‑digit share of non‑ticket revenue in 2024. Large buyers secured negotiated discounts of ~10–25% in 2024, stabilizing volumes but compressing trunk yields. OTAs (Trip.com ~60% of OTA bookings 2023) and low NDC adoption (<20% in 2024) sustain intermediary bargaining power; on‑time performance 79.4% (2024).

| Metric | Value | Year |

|---|---|---|

| Trip.com OTA share | ~60% | 2023 |

| On‑time performance | 79.4% | 2024 |

| Corporate discounts | 10–25% | 2024 |

| NDC adoption | <20% | 2024 |

| Ancillary revenue share | Mid single‑digit % | 2024 |

Preview Before You Purchase

China Eastern Airlines Porter's Five Forces Analysis

This preview shows the exact China Eastern Airlines Porter's Five Forces analysis you'll receive after purchase—no placeholders. The document covers supplier and buyer power, competitive rivalry, and threats of entry and substitutes, with data-driven insights and strategic implications. It's fully formatted and ready for immediate download.