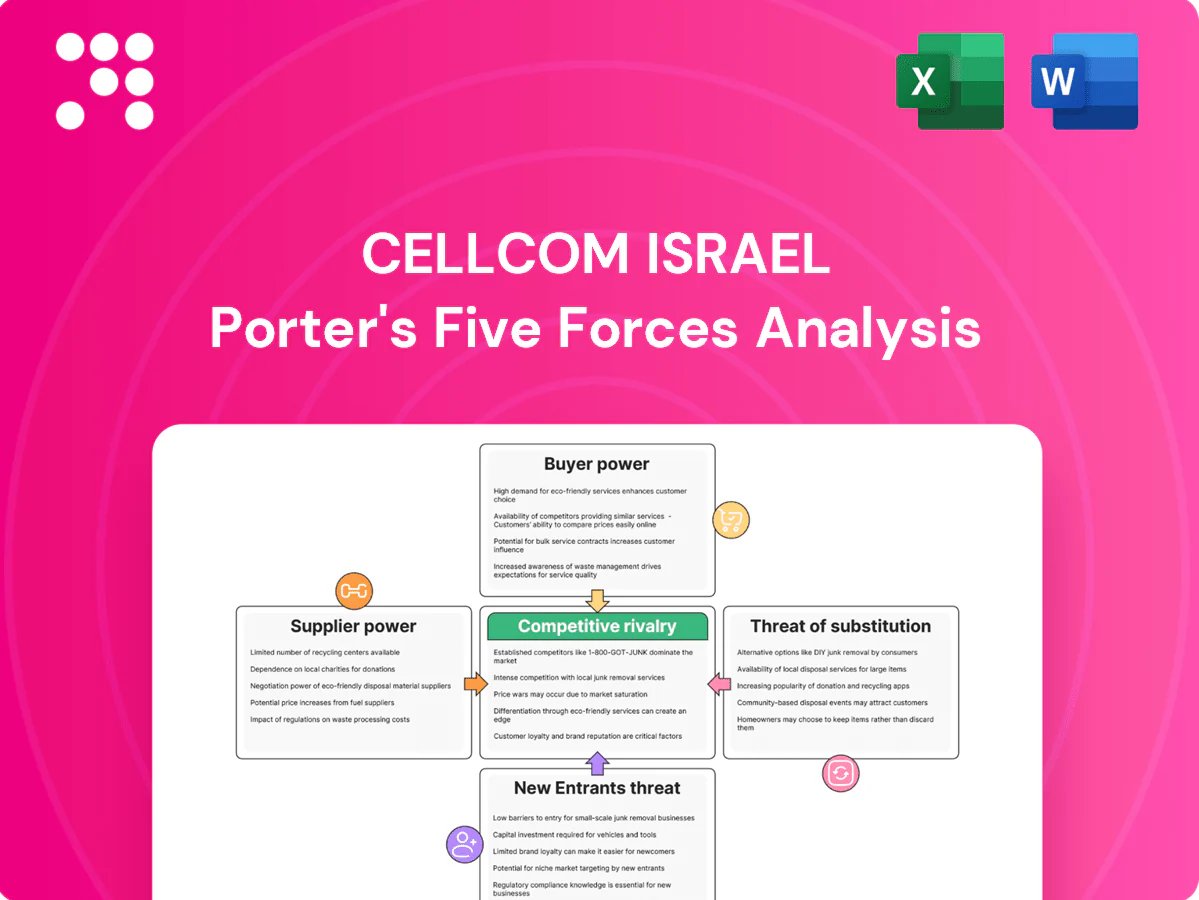

Cellcom Israel Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Cellcom Israel faces intense rivalry, high regulatory scrutiny, and growing substitute threats from OTT services, while customer price sensitivity and heavy network CAPEX shape bargaining dynamics. Supplier dependence on vendors and spectrum costs adds strategic pressure. This snapshot highlights core force interactions and implications. Unlock the full Porter's Five Forces Analysis to explore Cellcom’s competitive dynamics and actionable strategy recommendations.

Suppliers Bargaining Power

Network equipment concentration

Cellcom depends on a handful of global OEMs for RAN and core equipment, limiting switching options as the top vendors account for roughly 70–80% of the global RAN market. Proprietary interfaces, 5–10 year software/support roadmaps and certification needs create effective lock‑ins, while vendor consolidation raises supplier leverage. Imported kit priced in USD/EUR makes costs sensitive to shekel moves; a 10% shekel depreciation roughly raises procurement costs by 10%.

Spectrum and regulatory dependence

Access to licensed spectrum in Israel remains state-controlled, so the Ministry of Communications functions as a de facto supplier, setting auction rules and renewal conditions that directly affect Cellcom’s costs and flexibility. Auction terms and usage obligations — reinforced by 2024 regulatory clarifications on rollout and coverage deadlines — increase compliance costs and limit bargaining space. Strict licensing and renewal conditions compress negotiating leverage and mean policy shifts can rapidly alter network economics.

Tower, backhaul, and fiber wholesalers

Leasing towers, rooftops and fiber backhaul from a limited pool concentrates supplier power in Israel, where three national MNOs (Cellcom, Partner, Pelephone/Bezeq) compete for dense urban sites. Urban site scarcity and strict zoning in cities with ~9.3 million residents drive higher rents and switching costs. Long-term leases and SLAs commonly exceed five years and often embed escalation clauses; outage penalties and redundancy requirements further lock in operators.

Content and platform rights for TV

Premium channels, sports, and major streaming rights in Israel are concentrated among a few licensors, giving suppliers strong leverage; exclusive windows and minimum guarantees further entrench that power. Content cost inflation is difficult to pass to consumers in a price-sensitive Israeli market, squeezing margins. Integration needs for set-top boxes, apps and CDNs create additional supplier dependency and switching costs.

- Concentrated licensors

- Exclusive windows & minimum guarantees

- Price-sensitive market limits pass-through

- Platform/CDN integration dependency

IT, billing, and cloud vendors

Mission-critical BSS/OSS and multi-cloud contracts create strong vendor stickiness for Cellcom, raising switching costs and locking in long-term commitments.

Deep custom integrations and legacy adapters make migrations costly and risky, often requiring months and multimillion-shekel projects to replatform.

Cybersecurity, data-residency rules and SLA limitations mean vendor choice is constrained; in 2024 AWS, Microsoft and Google held roughly 32%, 23% and 11% of global cloud market share respectively.

- High stickiness

- Migration costliness

- Regulatory constraints

- Service credits insufficient

High supplier power: RAN 70-80% lock-in, spectrum rules, site scarcity, cloud 32%/23%/11%

Cellcom faces high supplier power: top RAN vendors hold ~70–80% market share, creating vendor lock‑in and 5–10 year support horizons. Spectrum is state‑controlled with 2024 rollout obligations tightening costs; tower/site scarcity in Israel (pop ~9.3m) pushes long leases >5 years. Cloud concentration (AWS ~32%, Microsoft ~23%, Google ~11% in 2024) and premium content exclusivity further compress bargaining leverage.

| Category | Metric (2024) | Impact |

|---|---|---|

| RAN vendors | 70–80% global share | High lock‑in |

| Spectrum | State‑controlled, new rollout rules | Regulatory risk |

| Towers/sites | Pop ~9.3m, long leases & scarce sites | Higher rents |

| Cloud | AWS 32% MSFT 23% GCP 11% | Vendor stickiness |

| Content | Concentrated licensors, exclusives | Margin pressure |

What is included in the product

Tailored Porter’s Five Forces analysis for Cellcom Israel uncovering competitive intensity, buyer and supplier leverage, threat of entrants and substitutes, and disruptive risks to market share and profitability—ready for integration into strategy decks.

Compact Porter's Five Forces summary for Cellcom Israel that instantly highlights competitive pressures and regulatory risks, with customizable scores and a ready-made spider chart to drop into pitches or boardroom slides.

Customers Bargaining Power

High price sensitivity and commoditization

High price sensitivity in Israel (mobile penetration ~125% in 2024) and easy online comparison across mobile, broadband and TV drives deal-seeking; unlimited bundles and frequent promotions establish reference prices. Consumers pivot for small savings, keeping Cellcom ARPU under persistent downward pressure as features converge.

Number portability and low switching costs

Fast number portability reduces friction to churn; Israel introduced number portability in 2006, making same-number switching routine and accelerating customer movement. eSIM and self-onboarding, supported by major Israeli operators since around 2019, further lower barriers and shorten activation time. High mobile penetration (over 100%) and common multi-SIM households fragment loyalty, while frequent retention incentives train buyers to negotiate better terms.

Enterprise and public sector bargaining

Enterprise and public sector clients buy at scale and demand bespoke SLAs, pushing Cellcom into negotiated contract terms and tighter margins in 2024. RFP-driven procurement increases price competition and compresses EBITDA on large deals. Dual-sourcing strategies by customers lower switching costs and bargaining dependence on any single operator. Value-added services frequently face competitive discounting, reducing upsell margins.

Converged bundle expectations

Customers now expect discounts that span mobile, fiber and TV; industry data in 2024 show converged bundles lift ARPU by about 15% and cut churn roughly 25% versus single-product accounts.

Unbundling increases churn risk and erodes perceived value, while cross-product service failures often trigger full-account switching; bundle depth and added discounts therefore become core negotiation levers for Cellcom.

- expectations: discounts across mobile+fiber+TV

- value: bundles ≈ +15% ARPU (2024)

- risk: unbundling → higher churn (~25%)

- leverage: bundle depth used in negotiations

Digital channels amplify transparency

Digital channels amplify transparency for Cellcom: comparison sites and social media surface real-time offers, negative reviews accelerate churn and always-on campaigns keep buyers in shopping mode, while price-matching dynamics erode pricing power; Israel internet penetration reached about 92% in 2024, intensifying customer visibility and switching.

- Real-time offers visibility

- Negative reviews → faster churn

- Continuous campaigns boost shopping frequency

- Price-matching reduces margin control

Bundling lifts ARPU 15% and lowers churn 25% amid 125% mobile penetration

Customers have strong bargaining power: high price sensitivity (mobile penetration ~125% in 2024) and easy online comparison depress ARPU as features converge. Low switching costs (number portability, eSIM) raise churn; converged bundles lift ARPU ~15% and cut churn ~25% vs single-product accounts (2024).

| Metric | 2024 | Impact |

|---|---|---|

| Mobile penetration | ~125% | High price sensitivity |

| Internet penetration | ~92% | Offer transparency |

| Bundle ARPU lift | +15% | Retention |

| Churn delta | -25% | Value of bundling |

Preview the Actual Deliverable

Cellcom Israel Porter's Five Forces Analysis

This preview shows the exact Cellcom Israel Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The document is the full, professionally formatted analysis ready for immediate download upon purchase. Use it as-is for strategy, valuation, or competitive insight.

Don't Miss the Bigger Picture

Cellcom Israel faces intense rivalry, high regulatory scrutiny, and growing substitute threats from OTT services, while customer price sensitivity and heavy network CAPEX shape bargaining dynamics. Supplier dependence on vendors and spectrum costs adds strategic pressure. This snapshot highlights core force interactions and implications. Unlock the full Porter's Five Forces Analysis to explore Cellcom’s competitive dynamics and actionable strategy recommendations.

Suppliers Bargaining Power

Network equipment concentration

Cellcom depends on a handful of global OEMs for RAN and core equipment, limiting switching options as the top vendors account for roughly 70–80% of the global RAN market. Proprietary interfaces, 5–10 year software/support roadmaps and certification needs create effective lock‑ins, while vendor consolidation raises supplier leverage. Imported kit priced in USD/EUR makes costs sensitive to shekel moves; a 10% shekel depreciation roughly raises procurement costs by 10%.

Spectrum and regulatory dependence

Access to licensed spectrum in Israel remains state-controlled, so the Ministry of Communications functions as a de facto supplier, setting auction rules and renewal conditions that directly affect Cellcom’s costs and flexibility. Auction terms and usage obligations — reinforced by 2024 regulatory clarifications on rollout and coverage deadlines — increase compliance costs and limit bargaining space. Strict licensing and renewal conditions compress negotiating leverage and mean policy shifts can rapidly alter network economics.

Tower, backhaul, and fiber wholesalers

Leasing towers, rooftops and fiber backhaul from a limited pool concentrates supplier power in Israel, where three national MNOs (Cellcom, Partner, Pelephone/Bezeq) compete for dense urban sites. Urban site scarcity and strict zoning in cities with ~9.3 million residents drive higher rents and switching costs. Long-term leases and SLAs commonly exceed five years and often embed escalation clauses; outage penalties and redundancy requirements further lock in operators.

Content and platform rights for TV

Premium channels, sports, and major streaming rights in Israel are concentrated among a few licensors, giving suppliers strong leverage; exclusive windows and minimum guarantees further entrench that power. Content cost inflation is difficult to pass to consumers in a price-sensitive Israeli market, squeezing margins. Integration needs for set-top boxes, apps and CDNs create additional supplier dependency and switching costs.

- Concentrated licensors

- Exclusive windows & minimum guarantees

- Price-sensitive market limits pass-through

- Platform/CDN integration dependency

IT, billing, and cloud vendors

Mission-critical BSS/OSS and multi-cloud contracts create strong vendor stickiness for Cellcom, raising switching costs and locking in long-term commitments.

Deep custom integrations and legacy adapters make migrations costly and risky, often requiring months and multimillion-shekel projects to replatform.

Cybersecurity, data-residency rules and SLA limitations mean vendor choice is constrained; in 2024 AWS, Microsoft and Google held roughly 32%, 23% and 11% of global cloud market share respectively.

- High stickiness

- Migration costliness

- Regulatory constraints

- Service credits insufficient

High supplier power: RAN 70-80% lock-in, spectrum rules, site scarcity, cloud 32%/23%/11%

Cellcom faces high supplier power: top RAN vendors hold ~70–80% market share, creating vendor lock‑in and 5–10 year support horizons. Spectrum is state‑controlled with 2024 rollout obligations tightening costs; tower/site scarcity in Israel (pop ~9.3m) pushes long leases >5 years. Cloud concentration (AWS ~32%, Microsoft ~23%, Google ~11% in 2024) and premium content exclusivity further compress bargaining leverage.

| Category | Metric (2024) | Impact |

|---|---|---|

| RAN vendors | 70–80% global share | High lock‑in |

| Spectrum | State‑controlled, new rollout rules | Regulatory risk |

| Towers/sites | Pop ~9.3m, long leases & scarce sites | Higher rents |

| Cloud | AWS 32% MSFT 23% GCP 11% | Vendor stickiness |

| Content | Concentrated licensors, exclusives | Margin pressure |

What is included in the product

Tailored Porter’s Five Forces analysis for Cellcom Israel uncovering competitive intensity, buyer and supplier leverage, threat of entrants and substitutes, and disruptive risks to market share and profitability—ready for integration into strategy decks.

Compact Porter's Five Forces summary for Cellcom Israel that instantly highlights competitive pressures and regulatory risks, with customizable scores and a ready-made spider chart to drop into pitches or boardroom slides.

Customers Bargaining Power

High price sensitivity and commoditization

High price sensitivity in Israel (mobile penetration ~125% in 2024) and easy online comparison across mobile, broadband and TV drives deal-seeking; unlimited bundles and frequent promotions establish reference prices. Consumers pivot for small savings, keeping Cellcom ARPU under persistent downward pressure as features converge.

Number portability and low switching costs

Fast number portability reduces friction to churn; Israel introduced number portability in 2006, making same-number switching routine and accelerating customer movement. eSIM and self-onboarding, supported by major Israeli operators since around 2019, further lower barriers and shorten activation time. High mobile penetration (over 100%) and common multi-SIM households fragment loyalty, while frequent retention incentives train buyers to negotiate better terms.

Enterprise and public sector bargaining

Enterprise and public sector clients buy at scale and demand bespoke SLAs, pushing Cellcom into negotiated contract terms and tighter margins in 2024. RFP-driven procurement increases price competition and compresses EBITDA on large deals. Dual-sourcing strategies by customers lower switching costs and bargaining dependence on any single operator. Value-added services frequently face competitive discounting, reducing upsell margins.

Converged bundle expectations

Customers now expect discounts that span mobile, fiber and TV; industry data in 2024 show converged bundles lift ARPU by about 15% and cut churn roughly 25% versus single-product accounts.

Unbundling increases churn risk and erodes perceived value, while cross-product service failures often trigger full-account switching; bundle depth and added discounts therefore become core negotiation levers for Cellcom.

- expectations: discounts across mobile+fiber+TV

- value: bundles ≈ +15% ARPU (2024)

- risk: unbundling → higher churn (~25%)

- leverage: bundle depth used in negotiations

Digital channels amplify transparency

Digital channels amplify transparency for Cellcom: comparison sites and social media surface real-time offers, negative reviews accelerate churn and always-on campaigns keep buyers in shopping mode, while price-matching dynamics erode pricing power; Israel internet penetration reached about 92% in 2024, intensifying customer visibility and switching.

- Real-time offers visibility

- Negative reviews → faster churn

- Continuous campaigns boost shopping frequency

- Price-matching reduces margin control

Bundling lifts ARPU 15% and lowers churn 25% amid 125% mobile penetration

Customers have strong bargaining power: high price sensitivity (mobile penetration ~125% in 2024) and easy online comparison depress ARPU as features converge. Low switching costs (number portability, eSIM) raise churn; converged bundles lift ARPU ~15% and cut churn ~25% vs single-product accounts (2024).

| Metric | 2024 | Impact |

|---|---|---|

| Mobile penetration | ~125% | High price sensitivity |

| Internet penetration | ~92% | Offer transparency |

| Bundle ARPU lift | +15% | Retention |

| Churn delta | -25% | Value of bundling |

Preview the Actual Deliverable

Cellcom Israel Porter's Five Forces Analysis

This preview shows the exact Cellcom Israel Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The document is the full, professionally formatted analysis ready for immediate download upon purchase. Use it as-is for strategy, valuation, or competitive insight.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Cellcom Israel faces intense rivalry, high regulatory scrutiny, and growing substitute threats from OTT services, while customer price sensitivity and heavy network CAPEX shape bargaining dynamics. Supplier dependence on vendors and spectrum costs adds strategic pressure. This snapshot highlights core force interactions and implications. Unlock the full Porter's Five Forces Analysis to explore Cellcom’s competitive dynamics and actionable strategy recommendations.

Suppliers Bargaining Power

Network equipment concentration

Cellcom depends on a handful of global OEMs for RAN and core equipment, limiting switching options as the top vendors account for roughly 70–80% of the global RAN market. Proprietary interfaces, 5–10 year software/support roadmaps and certification needs create effective lock‑ins, while vendor consolidation raises supplier leverage. Imported kit priced in USD/EUR makes costs sensitive to shekel moves; a 10% shekel depreciation roughly raises procurement costs by 10%.

Spectrum and regulatory dependence

Access to licensed spectrum in Israel remains state-controlled, so the Ministry of Communications functions as a de facto supplier, setting auction rules and renewal conditions that directly affect Cellcom’s costs and flexibility. Auction terms and usage obligations — reinforced by 2024 regulatory clarifications on rollout and coverage deadlines — increase compliance costs and limit bargaining space. Strict licensing and renewal conditions compress negotiating leverage and mean policy shifts can rapidly alter network economics.

Tower, backhaul, and fiber wholesalers

Leasing towers, rooftops and fiber backhaul from a limited pool concentrates supplier power in Israel, where three national MNOs (Cellcom, Partner, Pelephone/Bezeq) compete for dense urban sites. Urban site scarcity and strict zoning in cities with ~9.3 million residents drive higher rents and switching costs. Long-term leases and SLAs commonly exceed five years and often embed escalation clauses; outage penalties and redundancy requirements further lock in operators.

Content and platform rights for TV

Premium channels, sports, and major streaming rights in Israel are concentrated among a few licensors, giving suppliers strong leverage; exclusive windows and minimum guarantees further entrench that power. Content cost inflation is difficult to pass to consumers in a price-sensitive Israeli market, squeezing margins. Integration needs for set-top boxes, apps and CDNs create additional supplier dependency and switching costs.

- Concentrated licensors

- Exclusive windows & minimum guarantees

- Price-sensitive market limits pass-through

- Platform/CDN integration dependency

IT, billing, and cloud vendors

Mission-critical BSS/OSS and multi-cloud contracts create strong vendor stickiness for Cellcom, raising switching costs and locking in long-term commitments.

Deep custom integrations and legacy adapters make migrations costly and risky, often requiring months and multimillion-shekel projects to replatform.

Cybersecurity, data-residency rules and SLA limitations mean vendor choice is constrained; in 2024 AWS, Microsoft and Google held roughly 32%, 23% and 11% of global cloud market share respectively.

- High stickiness

- Migration costliness

- Regulatory constraints

- Service credits insufficient

High supplier power: RAN 70-80% lock-in, spectrum rules, site scarcity, cloud 32%/23%/11%

Cellcom faces high supplier power: top RAN vendors hold ~70–80% market share, creating vendor lock‑in and 5–10 year support horizons. Spectrum is state‑controlled with 2024 rollout obligations tightening costs; tower/site scarcity in Israel (pop ~9.3m) pushes long leases >5 years. Cloud concentration (AWS ~32%, Microsoft ~23%, Google ~11% in 2024) and premium content exclusivity further compress bargaining leverage.

| Category | Metric (2024) | Impact |

|---|---|---|

| RAN vendors | 70–80% global share | High lock‑in |

| Spectrum | State‑controlled, new rollout rules | Regulatory risk |

| Towers/sites | Pop ~9.3m, long leases & scarce sites | Higher rents |

| Cloud | AWS 32% MSFT 23% GCP 11% | Vendor stickiness |

| Content | Concentrated licensors, exclusives | Margin pressure |

What is included in the product

Tailored Porter’s Five Forces analysis for Cellcom Israel uncovering competitive intensity, buyer and supplier leverage, threat of entrants and substitutes, and disruptive risks to market share and profitability—ready for integration into strategy decks.

Compact Porter's Five Forces summary for Cellcom Israel that instantly highlights competitive pressures and regulatory risks, with customizable scores and a ready-made spider chart to drop into pitches or boardroom slides.

Customers Bargaining Power

High price sensitivity and commoditization

High price sensitivity in Israel (mobile penetration ~125% in 2024) and easy online comparison across mobile, broadband and TV drives deal-seeking; unlimited bundles and frequent promotions establish reference prices. Consumers pivot for small savings, keeping Cellcom ARPU under persistent downward pressure as features converge.

Number portability and low switching costs

Fast number portability reduces friction to churn; Israel introduced number portability in 2006, making same-number switching routine and accelerating customer movement. eSIM and self-onboarding, supported by major Israeli operators since around 2019, further lower barriers and shorten activation time. High mobile penetration (over 100%) and common multi-SIM households fragment loyalty, while frequent retention incentives train buyers to negotiate better terms.

Enterprise and public sector bargaining

Enterprise and public sector clients buy at scale and demand bespoke SLAs, pushing Cellcom into negotiated contract terms and tighter margins in 2024. RFP-driven procurement increases price competition and compresses EBITDA on large deals. Dual-sourcing strategies by customers lower switching costs and bargaining dependence on any single operator. Value-added services frequently face competitive discounting, reducing upsell margins.

Converged bundle expectations

Customers now expect discounts that span mobile, fiber and TV; industry data in 2024 show converged bundles lift ARPU by about 15% and cut churn roughly 25% versus single-product accounts.

Unbundling increases churn risk and erodes perceived value, while cross-product service failures often trigger full-account switching; bundle depth and added discounts therefore become core negotiation levers for Cellcom.

- expectations: discounts across mobile+fiber+TV

- value: bundles ≈ +15% ARPU (2024)

- risk: unbundling → higher churn (~25%)

- leverage: bundle depth used in negotiations

Digital channels amplify transparency

Digital channels amplify transparency for Cellcom: comparison sites and social media surface real-time offers, negative reviews accelerate churn and always-on campaigns keep buyers in shopping mode, while price-matching dynamics erode pricing power; Israel internet penetration reached about 92% in 2024, intensifying customer visibility and switching.

- Real-time offers visibility

- Negative reviews → faster churn

- Continuous campaigns boost shopping frequency

- Price-matching reduces margin control

Bundling lifts ARPU 15% and lowers churn 25% amid 125% mobile penetration

Customers have strong bargaining power: high price sensitivity (mobile penetration ~125% in 2024) and easy online comparison depress ARPU as features converge. Low switching costs (number portability, eSIM) raise churn; converged bundles lift ARPU ~15% and cut churn ~25% vs single-product accounts (2024).

| Metric | 2024 | Impact |

|---|---|---|

| Mobile penetration | ~125% | High price sensitivity |

| Internet penetration | ~92% | Offer transparency |

| Bundle ARPU lift | +15% | Retention |

| Churn delta | -25% | Value of bundling |

Preview the Actual Deliverable

Cellcom Israel Porter's Five Forces Analysis

This preview shows the exact Cellcom Israel Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The document is the full, professionally formatted analysis ready for immediate download upon purchase. Use it as-is for strategy, valuation, or competitive insight.