Cembra Money Bank Boston Consulting Group Matrix

See the Bigger Picture

Curious where Cembra Money Bank’s products sit — Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at competitive strengths and cash flow dynamics, but the full BCG Matrix gives quadrant-by-quadrant clarity, actionable recommendations, and ready-to-use Word and Excel files. Purchase the complete report now to cut through the noise and make confident strategic moves.

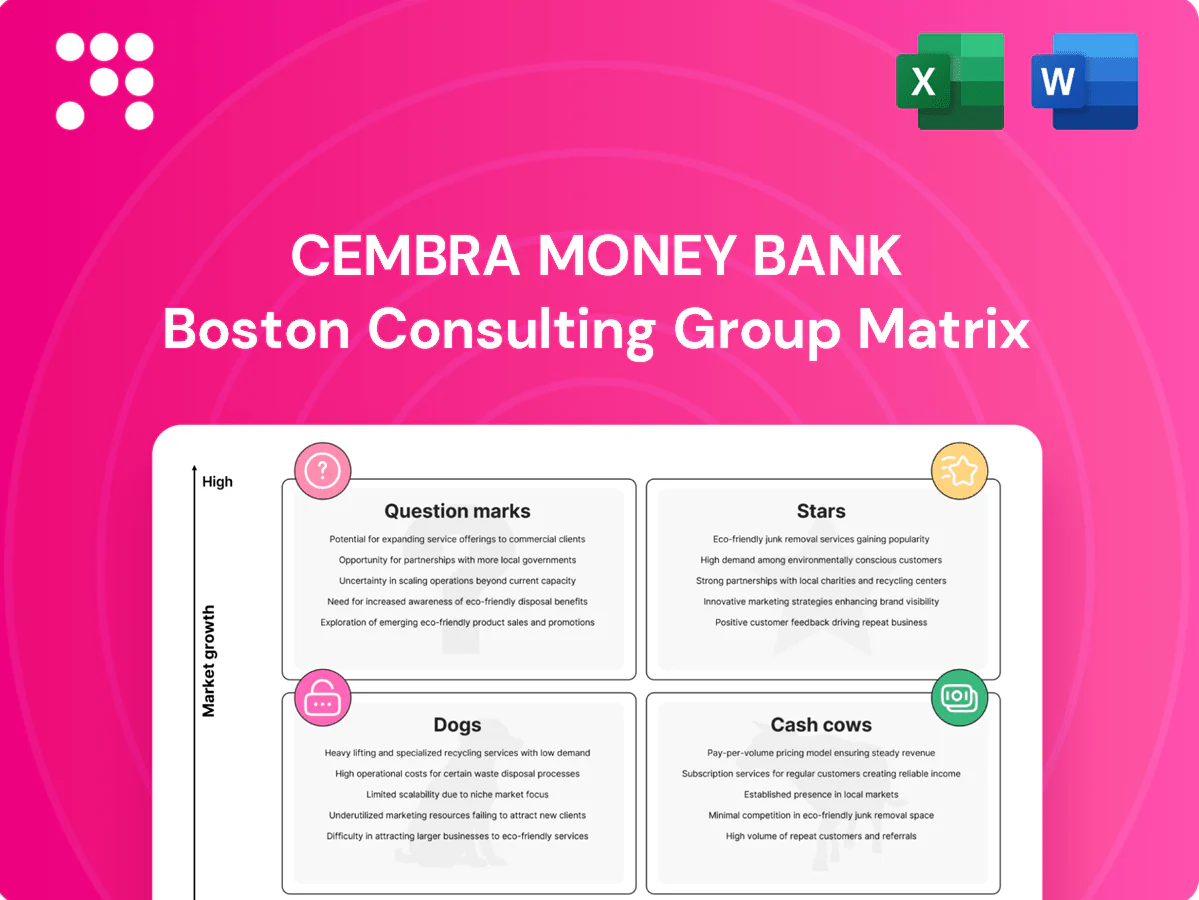

Stars

Auto leasing engine

Cembra’s auto leasing engine commands a leading position in Swiss auto finance, backing an auto portfolio of roughly CHF 4.2bn and capitalizing on a 2024 new-car EV share near 30% as demand shifts to flexible leases. Market growth is driven by EV adoption and dealer digitization; defending the lead requires sustained dealer incentives and slick onboarding. Keep fueling it — this can mint tomorrow’s cash.

Credit cards portfolio

Cembra’s credit card portfolio is a Star: high spend and recurring fees drive strong unit economics with card transaction volumes up c.8% YoY in 2024 as contactless and e‑commerce adoption keep expanding; Switzerland’s cashless share remains among the highest in Europe. Promotions and co‑brand refresh costs compress margins upfront but typically pay back within 12–18 months given elevated spend per active card. To hold share the bank must outpace fintech UX while leveraging brand recognition to sustain double‑digit volume growth.

POS installment financing

POS installment financing is a Star for Cembra: retailers demand instant lending at checkout and Cembra already has placement there, with merchant-driven adoption rising through 2024 as chains push conversion. It requires heavy cash for tech, risk buffers, and partner incentives, compressing near-term margins. Securing more integrations with large merchants will compound volume and ROE over time.

Digital invoice financing (SME)

SMEs in Switzerland represent about 99.7% of companies (SFSO) and urgently need working-capital speed, making digital invoice financing a high-priority service; digital factoring volumes in Europe rose materially through 2023 as banks and fintechs scaled operations. Cembra’s strong risk DNA and underwriting track record help attract quality SME clients, but onboarding and analytics investment is currently heavy; once the pipeline scales, unit economics improve rapidly.

Embedded lending partnerships

Placing credit inside partner ecosystems is hot and expanding, and Cembra leverages its underwriting expertise plus partner reach to scale loan volume.

Integration and compliance burn cash early, increasing upfront costs and extending payback timelines for platform builds.

With the right anchors and scale, embedded lending can transition into a meaningful top-line driver for Cembra.

- Market trend: rising demand for embedded finance

- Strength: proven underwriting + partner distribution

- Risk: high early integration and compliance spend

- Opportunity: anchors enable rapid revenue scaling

Auto leasing CHF4.2bn (EV ~30%) and cards +8% - scale, UX & dealer incentives lift ROE

Cembra’s Stars: auto leasing (CHF4.2bn portfolio; 2024 new‑car EV share ~30%) and credit cards (card volumes +8% YoY 2024) plus POS installments and embedded SME finance show high growth and ROI potential but need sustained dealer/merchant incentives, UX investment and upfront integration cost to scale. Scale reduces unit costs and lifts ROE.

| Product | 2024 metric | Key KPI |

|---|---|---|

| Auto leasing | CHF4.2bn; EV ~30% | Dealer share, yield |

| Credit cards | Volumes +8% YoY | Spend per card, fees |

| POS/SME | SMEs 99.7% (SFSO) | Merchant integrations, CAC |

What is included in the product

Comprehensive BCG Matrix for Cembra Money Bank, highlighting Stars, Cash Cows, Question Marks and Dogs with strategic actions.

One-page Cembra BCG Matrix placing units in quadrants for quick strategic clarity and ready-to-present slides.

Cash Cows

Personal loans book

Personal loans book is a mature, high-margin portfolio for Cembra with predictable repayments and historically lower volatility than unsecured segments.

Growth is low but demand remains stable across cycles, supporting steady interest cash flows and enabling predictable capital planning.

Marketing spend is limited to performance channels while management focuses on milking cash and tightening cost of risk through selective underwriting and portfolio monitoring.

Lease servicing & renewals

Lease servicing and renewals generated steady fee and interest income in 2024 from an established lease base, with operations optimized and churn/renewal dynamics well understood. Growth remained modest in 2024 but cash conversion rates stayed high, supporting internal funding. Targeted automation initiatives in 2024 raised yield per contract without material capital expenditure.

Deposit & savings base

Sticky retail funding at attractive spreads underpins Cembra’s Deposit & savings base, with retail deposits of CHF 5.6bn in 2024 providing low-cost funding and net interest margin resilience; acquisition costs drop materially once scale is reached. Growth is slow but funding stability supports lending and operations, keeping funding volatility low. Optimize pricing and minimize churn to preserve spread and liquidity — small adjustments translate to outsized P&L impact, reliably paying the bills.

Card revolving & fees

Card revolving and fees at Cembra generate durable cash via interest, interchange and annual fees; portfolio behavior in Switzerland is historically stable with low churn, requiring little incremental marketing—maintain strict risk discipline and let the product print.

- Interest income: recurring

- Interchange: steady merchant flows

- Annual fees: predictable

- Action: preserve underwriting standards

Credit insurance add‑ons

Credit insurance add‑ons attached to Cembra loans and cards generate steady recurring premiums and supported the 2024 product run‑rate, reflecting high customer awareness in the mature Swiss market. Margins remain solid when paired with disciplined claims management and tight fraud controls, though continued compliance oversight is essential to preserve profitability. Maintain penetration and run‑rate focus to sustain cash‑cow status.

- Recurring premiums: reliable revenue stream

- Mature market: high customer awareness

- Margins: solid with careful claims management

- Risks: regulatory/compliance must be tightly managed

Personal loans: high-margin, stable cash flows; deposits CHF 5.6bn

Personal loans: mature, high‑margin with stable repayments. Growth low; cash flows support capital planning. Deposits provide low‑cost funding (retail deposits CHF 5.6bn in 2024) and high cash conversion; cards, fees and credit insurance deliver recurring income.

| Product | 2024 |

|---|---|

| Deposits | CHF 5.6bn |

| Loans/Leases | High cash conversion |

| Cards & Fees | Durable recurring |

What You’re Viewing Is Included

Cembra Money Bank BCG Matrix

The file you’re previewing is the exact Cembra Money Bank BCG Matrix you’ll receive after purchase—no watermarks, no placeholders. It’s the final, fully formatted report built for strategic clarity and quick decision-making. Buy once and download immediately; it’s editable, printable, and presentation-ready. No surprises—just a market‑tested asset you can use right away.

See the Bigger Picture

Curious where Cembra Money Bank’s products sit — Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at competitive strengths and cash flow dynamics, but the full BCG Matrix gives quadrant-by-quadrant clarity, actionable recommendations, and ready-to-use Word and Excel files. Purchase the complete report now to cut through the noise and make confident strategic moves.

Stars

Auto leasing engine

Cembra’s auto leasing engine commands a leading position in Swiss auto finance, backing an auto portfolio of roughly CHF 4.2bn and capitalizing on a 2024 new-car EV share near 30% as demand shifts to flexible leases. Market growth is driven by EV adoption and dealer digitization; defending the lead requires sustained dealer incentives and slick onboarding. Keep fueling it — this can mint tomorrow’s cash.

Credit cards portfolio

Cembra’s credit card portfolio is a Star: high spend and recurring fees drive strong unit economics with card transaction volumes up c.8% YoY in 2024 as contactless and e‑commerce adoption keep expanding; Switzerland’s cashless share remains among the highest in Europe. Promotions and co‑brand refresh costs compress margins upfront but typically pay back within 12–18 months given elevated spend per active card. To hold share the bank must outpace fintech UX while leveraging brand recognition to sustain double‑digit volume growth.

POS installment financing

POS installment financing is a Star for Cembra: retailers demand instant lending at checkout and Cembra already has placement there, with merchant-driven adoption rising through 2024 as chains push conversion. It requires heavy cash for tech, risk buffers, and partner incentives, compressing near-term margins. Securing more integrations with large merchants will compound volume and ROE over time.

Digital invoice financing (SME)

SMEs in Switzerland represent about 99.7% of companies (SFSO) and urgently need working-capital speed, making digital invoice financing a high-priority service; digital factoring volumes in Europe rose materially through 2023 as banks and fintechs scaled operations. Cembra’s strong risk DNA and underwriting track record help attract quality SME clients, but onboarding and analytics investment is currently heavy; once the pipeline scales, unit economics improve rapidly.

Embedded lending partnerships

Placing credit inside partner ecosystems is hot and expanding, and Cembra leverages its underwriting expertise plus partner reach to scale loan volume.

Integration and compliance burn cash early, increasing upfront costs and extending payback timelines for platform builds.

With the right anchors and scale, embedded lending can transition into a meaningful top-line driver for Cembra.

- Market trend: rising demand for embedded finance

- Strength: proven underwriting + partner distribution

- Risk: high early integration and compliance spend

- Opportunity: anchors enable rapid revenue scaling

Auto leasing CHF4.2bn (EV ~30%) and cards +8% - scale, UX & dealer incentives lift ROE

Cembra’s Stars: auto leasing (CHF4.2bn portfolio; 2024 new‑car EV share ~30%) and credit cards (card volumes +8% YoY 2024) plus POS installments and embedded SME finance show high growth and ROI potential but need sustained dealer/merchant incentives, UX investment and upfront integration cost to scale. Scale reduces unit costs and lifts ROE.

| Product | 2024 metric | Key KPI |

|---|---|---|

| Auto leasing | CHF4.2bn; EV ~30% | Dealer share, yield |

| Credit cards | Volumes +8% YoY | Spend per card, fees |

| POS/SME | SMEs 99.7% (SFSO) | Merchant integrations, CAC |

What is included in the product

Comprehensive BCG Matrix for Cembra Money Bank, highlighting Stars, Cash Cows, Question Marks and Dogs with strategic actions.

One-page Cembra BCG Matrix placing units in quadrants for quick strategic clarity and ready-to-present slides.

Cash Cows

Personal loans book

Personal loans book is a mature, high-margin portfolio for Cembra with predictable repayments and historically lower volatility than unsecured segments.

Growth is low but demand remains stable across cycles, supporting steady interest cash flows and enabling predictable capital planning.

Marketing spend is limited to performance channels while management focuses on milking cash and tightening cost of risk through selective underwriting and portfolio monitoring.

Lease servicing & renewals

Lease servicing and renewals generated steady fee and interest income in 2024 from an established lease base, with operations optimized and churn/renewal dynamics well understood. Growth remained modest in 2024 but cash conversion rates stayed high, supporting internal funding. Targeted automation initiatives in 2024 raised yield per contract without material capital expenditure.

Deposit & savings base

Sticky retail funding at attractive spreads underpins Cembra’s Deposit & savings base, with retail deposits of CHF 5.6bn in 2024 providing low-cost funding and net interest margin resilience; acquisition costs drop materially once scale is reached. Growth is slow but funding stability supports lending and operations, keeping funding volatility low. Optimize pricing and minimize churn to preserve spread and liquidity — small adjustments translate to outsized P&L impact, reliably paying the bills.

Card revolving & fees

Card revolving and fees at Cembra generate durable cash via interest, interchange and annual fees; portfolio behavior in Switzerland is historically stable with low churn, requiring little incremental marketing—maintain strict risk discipline and let the product print.

- Interest income: recurring

- Interchange: steady merchant flows

- Annual fees: predictable

- Action: preserve underwriting standards

Credit insurance add‑ons

Credit insurance add‑ons attached to Cembra loans and cards generate steady recurring premiums and supported the 2024 product run‑rate, reflecting high customer awareness in the mature Swiss market. Margins remain solid when paired with disciplined claims management and tight fraud controls, though continued compliance oversight is essential to preserve profitability. Maintain penetration and run‑rate focus to sustain cash‑cow status.

- Recurring premiums: reliable revenue stream

- Mature market: high customer awareness

- Margins: solid with careful claims management

- Risks: regulatory/compliance must be tightly managed

Personal loans: high-margin, stable cash flows; deposits CHF 5.6bn

Personal loans: mature, high‑margin with stable repayments. Growth low; cash flows support capital planning. Deposits provide low‑cost funding (retail deposits CHF 5.6bn in 2024) and high cash conversion; cards, fees and credit insurance deliver recurring income.

| Product | 2024 |

|---|---|

| Deposits | CHF 5.6bn |

| Loans/Leases | High cash conversion |

| Cards & Fees | Durable recurring |

What You’re Viewing Is Included

Cembra Money Bank BCG Matrix

The file you’re previewing is the exact Cembra Money Bank BCG Matrix you’ll receive after purchase—no watermarks, no placeholders. It’s the final, fully formatted report built for strategic clarity and quick decision-making. Buy once and download immediately; it’s editable, printable, and presentation-ready. No surprises—just a market‑tested asset you can use right away.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Curious where Cembra Money Bank’s products sit — Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at competitive strengths and cash flow dynamics, but the full BCG Matrix gives quadrant-by-quadrant clarity, actionable recommendations, and ready-to-use Word and Excel files. Purchase the complete report now to cut through the noise and make confident strategic moves.

Stars

Auto leasing engine

Cembra’s auto leasing engine commands a leading position in Swiss auto finance, backing an auto portfolio of roughly CHF 4.2bn and capitalizing on a 2024 new-car EV share near 30% as demand shifts to flexible leases. Market growth is driven by EV adoption and dealer digitization; defending the lead requires sustained dealer incentives and slick onboarding. Keep fueling it — this can mint tomorrow’s cash.

Credit cards portfolio

Cembra’s credit card portfolio is a Star: high spend and recurring fees drive strong unit economics with card transaction volumes up c.8% YoY in 2024 as contactless and e‑commerce adoption keep expanding; Switzerland’s cashless share remains among the highest in Europe. Promotions and co‑brand refresh costs compress margins upfront but typically pay back within 12–18 months given elevated spend per active card. To hold share the bank must outpace fintech UX while leveraging brand recognition to sustain double‑digit volume growth.

POS installment financing

POS installment financing is a Star for Cembra: retailers demand instant lending at checkout and Cembra already has placement there, with merchant-driven adoption rising through 2024 as chains push conversion. It requires heavy cash for tech, risk buffers, and partner incentives, compressing near-term margins. Securing more integrations with large merchants will compound volume and ROE over time.

Digital invoice financing (SME)

SMEs in Switzerland represent about 99.7% of companies (SFSO) and urgently need working-capital speed, making digital invoice financing a high-priority service; digital factoring volumes in Europe rose materially through 2023 as banks and fintechs scaled operations. Cembra’s strong risk DNA and underwriting track record help attract quality SME clients, but onboarding and analytics investment is currently heavy; once the pipeline scales, unit economics improve rapidly.

Embedded lending partnerships

Placing credit inside partner ecosystems is hot and expanding, and Cembra leverages its underwriting expertise plus partner reach to scale loan volume.

Integration and compliance burn cash early, increasing upfront costs and extending payback timelines for platform builds.

With the right anchors and scale, embedded lending can transition into a meaningful top-line driver for Cembra.

- Market trend: rising demand for embedded finance

- Strength: proven underwriting + partner distribution

- Risk: high early integration and compliance spend

- Opportunity: anchors enable rapid revenue scaling

Auto leasing CHF4.2bn (EV ~30%) and cards +8% - scale, UX & dealer incentives lift ROE

Cembra’s Stars: auto leasing (CHF4.2bn portfolio; 2024 new‑car EV share ~30%) and credit cards (card volumes +8% YoY 2024) plus POS installments and embedded SME finance show high growth and ROI potential but need sustained dealer/merchant incentives, UX investment and upfront integration cost to scale. Scale reduces unit costs and lifts ROE.

| Product | 2024 metric | Key KPI |

|---|---|---|

| Auto leasing | CHF4.2bn; EV ~30% | Dealer share, yield |

| Credit cards | Volumes +8% YoY | Spend per card, fees |

| POS/SME | SMEs 99.7% (SFSO) | Merchant integrations, CAC |

What is included in the product

Comprehensive BCG Matrix for Cembra Money Bank, highlighting Stars, Cash Cows, Question Marks and Dogs with strategic actions.

One-page Cembra BCG Matrix placing units in quadrants for quick strategic clarity and ready-to-present slides.

Cash Cows

Personal loans book

Personal loans book is a mature, high-margin portfolio for Cembra with predictable repayments and historically lower volatility than unsecured segments.

Growth is low but demand remains stable across cycles, supporting steady interest cash flows and enabling predictable capital planning.

Marketing spend is limited to performance channels while management focuses on milking cash and tightening cost of risk through selective underwriting and portfolio monitoring.

Lease servicing & renewals

Lease servicing and renewals generated steady fee and interest income in 2024 from an established lease base, with operations optimized and churn/renewal dynamics well understood. Growth remained modest in 2024 but cash conversion rates stayed high, supporting internal funding. Targeted automation initiatives in 2024 raised yield per contract without material capital expenditure.

Deposit & savings base

Sticky retail funding at attractive spreads underpins Cembra’s Deposit & savings base, with retail deposits of CHF 5.6bn in 2024 providing low-cost funding and net interest margin resilience; acquisition costs drop materially once scale is reached. Growth is slow but funding stability supports lending and operations, keeping funding volatility low. Optimize pricing and minimize churn to preserve spread and liquidity — small adjustments translate to outsized P&L impact, reliably paying the bills.

Card revolving & fees

Card revolving and fees at Cembra generate durable cash via interest, interchange and annual fees; portfolio behavior in Switzerland is historically stable with low churn, requiring little incremental marketing—maintain strict risk discipline and let the product print.

- Interest income: recurring

- Interchange: steady merchant flows

- Annual fees: predictable

- Action: preserve underwriting standards

Credit insurance add‑ons

Credit insurance add‑ons attached to Cembra loans and cards generate steady recurring premiums and supported the 2024 product run‑rate, reflecting high customer awareness in the mature Swiss market. Margins remain solid when paired with disciplined claims management and tight fraud controls, though continued compliance oversight is essential to preserve profitability. Maintain penetration and run‑rate focus to sustain cash‑cow status.

- Recurring premiums: reliable revenue stream

- Mature market: high customer awareness

- Margins: solid with careful claims management

- Risks: regulatory/compliance must be tightly managed

Personal loans: high-margin, stable cash flows; deposits CHF 5.6bn

Personal loans: mature, high‑margin with stable repayments. Growth low; cash flows support capital planning. Deposits provide low‑cost funding (retail deposits CHF 5.6bn in 2024) and high cash conversion; cards, fees and credit insurance deliver recurring income.

| Product | 2024 |

|---|---|

| Deposits | CHF 5.6bn |

| Loans/Leases | High cash conversion |

| Cards & Fees | Durable recurring |

What You’re Viewing Is Included

Cembra Money Bank BCG Matrix

The file you’re previewing is the exact Cembra Money Bank BCG Matrix you’ll receive after purchase—no watermarks, no placeholders. It’s the final, fully formatted report built for strategic clarity and quick decision-making. Buy once and download immediately; it’s editable, printable, and presentation-ready. No surprises—just a market‑tested asset you can use right away.