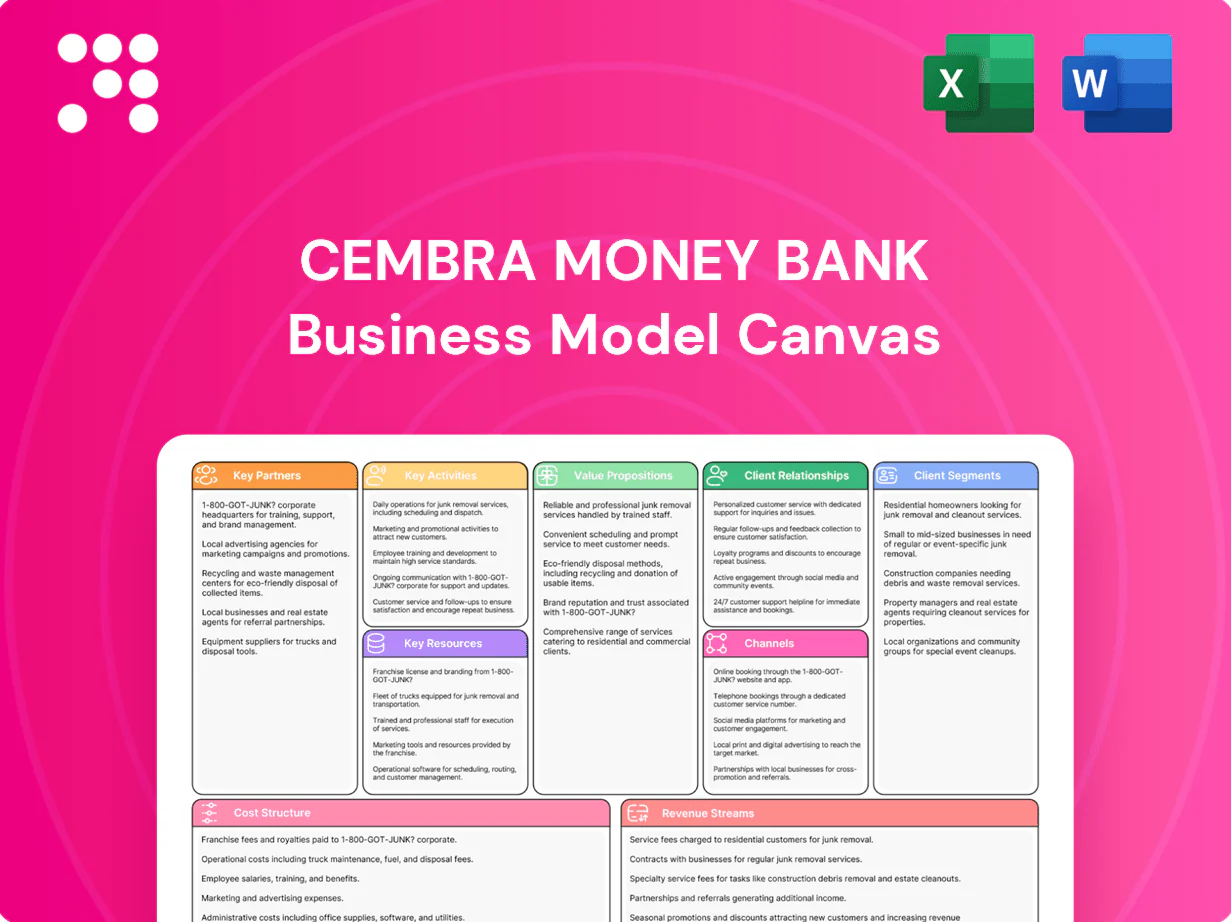

Cembra Money Bank Business Model Canvas

Business Model Canvas: Strategic Snapshot for a Consumer Finance Bank

Unlock the strategic blueprint of Cembra Money Bank with a concise Business Model Canvas that maps its value propositions, customer segments, key activities and revenue streams. This actionable snapshot highlights growth levers and risks—ideal for investors and strategists. Purchase the full Word/Excel canvas to access detailed, section-by-section insights and ready-to-use templates.

Partnerships

Auto dealer and OEM networks

Partnerships with Swiss car dealerships and OEMs drive point-of-sale origination for Cembra’s auto leases and loans, delivering fast approvals and competitive rates that help close sales.

Dealers gain quicker conversions; Cembra secures high-quality, recurring deal flow and showroom brand presence, supported by joint marketing and integrated financing tools.

Retailers and co-brand card partners

Alliances with national retailers enable co-branded credit cards and point-of-sale instalment solutions that boost basket size and loyalty. Retail partners drive higher spend; Cembra reached over 1 million card and loan customers by 2024, accessing large bases at lower acquisition cost. Data sharing, within Swiss regulation, supports targeted promotions and improved risk control. These partnerships expand reach and deepen customer engagement.

Payment networks and processors

Ties with Visa and Mastercard, accepted in 200+ countries and territories, ensure broad acceptance, security and rewards for Cembra cardholders. Network partnerships drive interchange economics and co-funded product innovation while supporting EMV, PCI DSS and scheme certifications for stable operations. Co-development with schemes accelerates digital wallet rollout and tokenization via Visa Token Service and Mastercard Digital Enablement Service.

Insurance carriers and brokers

Underwriting partners provide payment protection, credit life and asset-related insurance, expanding customer value and diversifying fee income. Joint product design aligns coverage precisely with Cembra loan and lease terms and pricing. Claims handling and compliance are standardized to Swiss regulation under FINMA and the Swiss Code of Obligations; as of 2024 partnerships involve multiple FINMA-regulated carriers.

- Insurance products: payment protection, credit life, asset-related

- Revenue: diversifies fee income streams

- Product alignment: loans/leases ↔ coverage

- Regulatory: FINMA + Swiss Code of Obligations (claims/compliance)

Funding, data, and regtech providers

Relationships with institutional funders, deposit brokers, credit bureaus, and regtech firms strengthen Cembra’s platform by diversifying liquidity beyond retail deposits and reducing funding concentration risk. Data and analytics vendors enhance underwriting accuracy and fraud detection, while regtech tools streamline KYC/AML and regulatory reporting, improving compliance efficiency and speed.

- Institutional funding: diversifies liquidity

- Credit bureaus: better credit scoring

- Data vendors: improved fraud detection

- Regtech: automated KYC/AML/reporting

Swiss POS deals drive 1M+ cards, global card-network reach and insurer-backed fees

Partnerships with Swiss dealers/OEMs drive point-of-sale auto origination and recurring deal flow. Retail alliances enable co-branded cards/instalments, supporting over 1 million cards and loans by 2024. Visa/Mastercard tie-ups deliver 200+ country acceptance and digital tokenization. Insurers and FINMA-regulated carriers expand protection products and fee income.

| Partner | Role | 2024 metric |

|---|---|---|

| Dealers/OEMs | POS origination | — |

| Retailers | Co-branded cards/instalments | >1m customers |

| Visa/Mastercard | Acceptance/tokenization | 200+ countries |

| Insurers | Payment/asset cover | FINMA-regulated |

What is included in the product

A comprehensive Business Model Canvas for Cembra Money Bank detailing customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks; includes competitive advantages, SWOT-linked insights and practical use for presentations, investor discussions and strategic decision-making.

Condenses Cembra Money Bank’s consumer finance strategy into a digestible one-page snapshot, saving hours of analysis and formatting while highlighting core lending, risk and customer channels for quick decision-making and team collaboration.

Activities

Credit underwriting and pricing

Assessing borrower risk across personal loans, auto leases, cards and invoice finance is core to underwriting, with models driving risk-based pricing and exposure limits. Verification, scorecards and affordability checks enforce regulatory and internal compliance. Continuous calibration of models and thresholds keeps approval rates aligned with target loss provisions and portfolio risk appetite.

Risk management and collections

Portfolio monitoring, early-warning systems and conservative provisioning protect asset quality at Cembra, with collections blending digital nudges and bespoke repayment plans to recover performing and non-performing receivables. Robust fraud prevention and real-time transaction monitoring reduce losses across card and consumer-lending flows. Regular stress testing and ICAAP scenarios steer capital allocation and liquidity planning.

Product development and card issuing

Designing consumer credit, co-branded cards and installment solutions drives growth by aligning product features and rewards with partner ecosystems; benefits are tuned to merchants and loyalty programs to boost acceptance and cross-sell. Lifecycle management covers activation, usage monitoring, retention campaigns and renewals, while billing, statements and dispute handling underpin customer trust and compliance.

Funding, treasury, and ALM

Funding, treasury and ALM manage deposits, securitisations and wholesale lines to secure stable liquidity while maintaining regulatory liquidity buffers and stress scenarios. Interest rate risk and duration are balanced through active ALM and internal hedging, and pricing transfers reflect actual cost of funds plus credit and liquidity premiums. Governance enforces policy limits and scenario testing.

- Deposits, securitisations, wholesale lines

- ALM hedging and duration management

- Pricing = cost of funds + risk premium

- Regulatory buffers + stress tests

Compliance and digital onboarding

Compliance with FINMA supervision and strict KYC/AML requirements is embedded in Cembra Money Bank’s processes, ensuring regulatory adherence across lending and payments.

eKYC and electronic signatures enable rapid, fully digital onboarding while privacy and data protection are enforced by design through encryption and access controls.

Continuous audits, real‑time monitoring and recurring staff training sustain control effectiveness and regulatory readiness.

- FINMA supervision

- KYC/AML embedded

- eKYC & electronic signatures

- Privacy by design

- Continuous audits & training

FINMA-aligned credit platform: underwriting, portfolio protection, liquidity and growth

Underwriting across loans, cards and leases uses scorecards, eKYC and affordability checks to enforce FINMA-aligned credit policy and dynamic pricing. Portfolio monitoring, collections and fraud detection preserve asset quality, supported by ALM, securitisations and deposit funding to secure liquidity. Product design, partner cards and lifecycle marketing drive origination and retention while continuous audit and training sustain controls.

| Metric (2024) | Value |

|---|---|

| Loan portfolio | N/A (2024) |

| Return on equity | N/A (2024) |

Delivered as Displayed

Business Model Canvas

The Business Model Canvas you’re previewing is the actual deliverable—not a mockup. When you purchase, you’ll receive this same comprehensive Cembra Money Bank canvas in full, ready-to-edit Word and Excel files. No surprises, just the exact document shown here.

Business Model Canvas: Strategic Snapshot for a Consumer Finance Bank

Unlock the strategic blueprint of Cembra Money Bank with a concise Business Model Canvas that maps its value propositions, customer segments, key activities and revenue streams. This actionable snapshot highlights growth levers and risks—ideal for investors and strategists. Purchase the full Word/Excel canvas to access detailed, section-by-section insights and ready-to-use templates.

Partnerships

Auto dealer and OEM networks

Partnerships with Swiss car dealerships and OEMs drive point-of-sale origination for Cembra’s auto leases and loans, delivering fast approvals and competitive rates that help close sales.

Dealers gain quicker conversions; Cembra secures high-quality, recurring deal flow and showroom brand presence, supported by joint marketing and integrated financing tools.

Retailers and co-brand card partners

Alliances with national retailers enable co-branded credit cards and point-of-sale instalment solutions that boost basket size and loyalty. Retail partners drive higher spend; Cembra reached over 1 million card and loan customers by 2024, accessing large bases at lower acquisition cost. Data sharing, within Swiss regulation, supports targeted promotions and improved risk control. These partnerships expand reach and deepen customer engagement.

Payment networks and processors

Ties with Visa and Mastercard, accepted in 200+ countries and territories, ensure broad acceptance, security and rewards for Cembra cardholders. Network partnerships drive interchange economics and co-funded product innovation while supporting EMV, PCI DSS and scheme certifications for stable operations. Co-development with schemes accelerates digital wallet rollout and tokenization via Visa Token Service and Mastercard Digital Enablement Service.

Insurance carriers and brokers

Underwriting partners provide payment protection, credit life and asset-related insurance, expanding customer value and diversifying fee income. Joint product design aligns coverage precisely with Cembra loan and lease terms and pricing. Claims handling and compliance are standardized to Swiss regulation under FINMA and the Swiss Code of Obligations; as of 2024 partnerships involve multiple FINMA-regulated carriers.

- Insurance products: payment protection, credit life, asset-related

- Revenue: diversifies fee income streams

- Product alignment: loans/leases ↔ coverage

- Regulatory: FINMA + Swiss Code of Obligations (claims/compliance)

Funding, data, and regtech providers

Relationships with institutional funders, deposit brokers, credit bureaus, and regtech firms strengthen Cembra’s platform by diversifying liquidity beyond retail deposits and reducing funding concentration risk. Data and analytics vendors enhance underwriting accuracy and fraud detection, while regtech tools streamline KYC/AML and regulatory reporting, improving compliance efficiency and speed.

- Institutional funding: diversifies liquidity

- Credit bureaus: better credit scoring

- Data vendors: improved fraud detection

- Regtech: automated KYC/AML/reporting

Swiss POS deals drive 1M+ cards, global card-network reach and insurer-backed fees

Partnerships with Swiss dealers/OEMs drive point-of-sale auto origination and recurring deal flow. Retail alliances enable co-branded cards/instalments, supporting over 1 million cards and loans by 2024. Visa/Mastercard tie-ups deliver 200+ country acceptance and digital tokenization. Insurers and FINMA-regulated carriers expand protection products and fee income.

| Partner | Role | 2024 metric |

|---|---|---|

| Dealers/OEMs | POS origination | — |

| Retailers | Co-branded cards/instalments | >1m customers |

| Visa/Mastercard | Acceptance/tokenization | 200+ countries |

| Insurers | Payment/asset cover | FINMA-regulated |

What is included in the product

A comprehensive Business Model Canvas for Cembra Money Bank detailing customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks; includes competitive advantages, SWOT-linked insights and practical use for presentations, investor discussions and strategic decision-making.

Condenses Cembra Money Bank’s consumer finance strategy into a digestible one-page snapshot, saving hours of analysis and formatting while highlighting core lending, risk and customer channels for quick decision-making and team collaboration.

Activities

Credit underwriting and pricing

Assessing borrower risk across personal loans, auto leases, cards and invoice finance is core to underwriting, with models driving risk-based pricing and exposure limits. Verification, scorecards and affordability checks enforce regulatory and internal compliance. Continuous calibration of models and thresholds keeps approval rates aligned with target loss provisions and portfolio risk appetite.

Risk management and collections

Portfolio monitoring, early-warning systems and conservative provisioning protect asset quality at Cembra, with collections blending digital nudges and bespoke repayment plans to recover performing and non-performing receivables. Robust fraud prevention and real-time transaction monitoring reduce losses across card and consumer-lending flows. Regular stress testing and ICAAP scenarios steer capital allocation and liquidity planning.

Product development and card issuing

Designing consumer credit, co-branded cards and installment solutions drives growth by aligning product features and rewards with partner ecosystems; benefits are tuned to merchants and loyalty programs to boost acceptance and cross-sell. Lifecycle management covers activation, usage monitoring, retention campaigns and renewals, while billing, statements and dispute handling underpin customer trust and compliance.

Funding, treasury, and ALM

Funding, treasury and ALM manage deposits, securitisations and wholesale lines to secure stable liquidity while maintaining regulatory liquidity buffers and stress scenarios. Interest rate risk and duration are balanced through active ALM and internal hedging, and pricing transfers reflect actual cost of funds plus credit and liquidity premiums. Governance enforces policy limits and scenario testing.

- Deposits, securitisations, wholesale lines

- ALM hedging and duration management

- Pricing = cost of funds + risk premium

- Regulatory buffers + stress tests

Compliance and digital onboarding

Compliance with FINMA supervision and strict KYC/AML requirements is embedded in Cembra Money Bank’s processes, ensuring regulatory adherence across lending and payments.

eKYC and electronic signatures enable rapid, fully digital onboarding while privacy and data protection are enforced by design through encryption and access controls.

Continuous audits, real‑time monitoring and recurring staff training sustain control effectiveness and regulatory readiness.

- FINMA supervision

- KYC/AML embedded

- eKYC & electronic signatures

- Privacy by design

- Continuous audits & training

FINMA-aligned credit platform: underwriting, portfolio protection, liquidity and growth

Underwriting across loans, cards and leases uses scorecards, eKYC and affordability checks to enforce FINMA-aligned credit policy and dynamic pricing. Portfolio monitoring, collections and fraud detection preserve asset quality, supported by ALM, securitisations and deposit funding to secure liquidity. Product design, partner cards and lifecycle marketing drive origination and retention while continuous audit and training sustain controls.

| Metric (2024) | Value |

|---|---|

| Loan portfolio | N/A (2024) |

| Return on equity | N/A (2024) |

Delivered as Displayed

Business Model Canvas

The Business Model Canvas you’re previewing is the actual deliverable—not a mockup. When you purchase, you’ll receive this same comprehensive Cembra Money Bank canvas in full, ready-to-edit Word and Excel files. No surprises, just the exact document shown here.

Description

Business Model Canvas: Strategic Snapshot for a Consumer Finance Bank

Unlock the strategic blueprint of Cembra Money Bank with a concise Business Model Canvas that maps its value propositions, customer segments, key activities and revenue streams. This actionable snapshot highlights growth levers and risks—ideal for investors and strategists. Purchase the full Word/Excel canvas to access detailed, section-by-section insights and ready-to-use templates.

Partnerships

Auto dealer and OEM networks

Partnerships with Swiss car dealerships and OEMs drive point-of-sale origination for Cembra’s auto leases and loans, delivering fast approvals and competitive rates that help close sales.

Dealers gain quicker conversions; Cembra secures high-quality, recurring deal flow and showroom brand presence, supported by joint marketing and integrated financing tools.

Retailers and co-brand card partners

Alliances with national retailers enable co-branded credit cards and point-of-sale instalment solutions that boost basket size and loyalty. Retail partners drive higher spend; Cembra reached over 1 million card and loan customers by 2024, accessing large bases at lower acquisition cost. Data sharing, within Swiss regulation, supports targeted promotions and improved risk control. These partnerships expand reach and deepen customer engagement.

Payment networks and processors

Ties with Visa and Mastercard, accepted in 200+ countries and territories, ensure broad acceptance, security and rewards for Cembra cardholders. Network partnerships drive interchange economics and co-funded product innovation while supporting EMV, PCI DSS and scheme certifications for stable operations. Co-development with schemes accelerates digital wallet rollout and tokenization via Visa Token Service and Mastercard Digital Enablement Service.

Insurance carriers and brokers

Underwriting partners provide payment protection, credit life and asset-related insurance, expanding customer value and diversifying fee income. Joint product design aligns coverage precisely with Cembra loan and lease terms and pricing. Claims handling and compliance are standardized to Swiss regulation under FINMA and the Swiss Code of Obligations; as of 2024 partnerships involve multiple FINMA-regulated carriers.

- Insurance products: payment protection, credit life, asset-related

- Revenue: diversifies fee income streams

- Product alignment: loans/leases ↔ coverage

- Regulatory: FINMA + Swiss Code of Obligations (claims/compliance)

Funding, data, and regtech providers

Relationships with institutional funders, deposit brokers, credit bureaus, and regtech firms strengthen Cembra’s platform by diversifying liquidity beyond retail deposits and reducing funding concentration risk. Data and analytics vendors enhance underwriting accuracy and fraud detection, while regtech tools streamline KYC/AML and regulatory reporting, improving compliance efficiency and speed.

- Institutional funding: diversifies liquidity

- Credit bureaus: better credit scoring

- Data vendors: improved fraud detection

- Regtech: automated KYC/AML/reporting

Swiss POS deals drive 1M+ cards, global card-network reach and insurer-backed fees

Partnerships with Swiss dealers/OEMs drive point-of-sale auto origination and recurring deal flow. Retail alliances enable co-branded cards/instalments, supporting over 1 million cards and loans by 2024. Visa/Mastercard tie-ups deliver 200+ country acceptance and digital tokenization. Insurers and FINMA-regulated carriers expand protection products and fee income.

| Partner | Role | 2024 metric |

|---|---|---|

| Dealers/OEMs | POS origination | — |

| Retailers | Co-branded cards/instalments | >1m customers |

| Visa/Mastercard | Acceptance/tokenization | 200+ countries |

| Insurers | Payment/asset cover | FINMA-regulated |

What is included in the product

A comprehensive Business Model Canvas for Cembra Money Bank detailing customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks; includes competitive advantages, SWOT-linked insights and practical use for presentations, investor discussions and strategic decision-making.

Condenses Cembra Money Bank’s consumer finance strategy into a digestible one-page snapshot, saving hours of analysis and formatting while highlighting core lending, risk and customer channels for quick decision-making and team collaboration.

Activities

Credit underwriting and pricing

Assessing borrower risk across personal loans, auto leases, cards and invoice finance is core to underwriting, with models driving risk-based pricing and exposure limits. Verification, scorecards and affordability checks enforce regulatory and internal compliance. Continuous calibration of models and thresholds keeps approval rates aligned with target loss provisions and portfolio risk appetite.

Risk management and collections

Portfolio monitoring, early-warning systems and conservative provisioning protect asset quality at Cembra, with collections blending digital nudges and bespoke repayment plans to recover performing and non-performing receivables. Robust fraud prevention and real-time transaction monitoring reduce losses across card and consumer-lending flows. Regular stress testing and ICAAP scenarios steer capital allocation and liquidity planning.

Product development and card issuing

Designing consumer credit, co-branded cards and installment solutions drives growth by aligning product features and rewards with partner ecosystems; benefits are tuned to merchants and loyalty programs to boost acceptance and cross-sell. Lifecycle management covers activation, usage monitoring, retention campaigns and renewals, while billing, statements and dispute handling underpin customer trust and compliance.

Funding, treasury, and ALM

Funding, treasury and ALM manage deposits, securitisations and wholesale lines to secure stable liquidity while maintaining regulatory liquidity buffers and stress scenarios. Interest rate risk and duration are balanced through active ALM and internal hedging, and pricing transfers reflect actual cost of funds plus credit and liquidity premiums. Governance enforces policy limits and scenario testing.

- Deposits, securitisations, wholesale lines

- ALM hedging and duration management

- Pricing = cost of funds + risk premium

- Regulatory buffers + stress tests

Compliance and digital onboarding

Compliance with FINMA supervision and strict KYC/AML requirements is embedded in Cembra Money Bank’s processes, ensuring regulatory adherence across lending and payments.

eKYC and electronic signatures enable rapid, fully digital onboarding while privacy and data protection are enforced by design through encryption and access controls.

Continuous audits, real‑time monitoring and recurring staff training sustain control effectiveness and regulatory readiness.

- FINMA supervision

- KYC/AML embedded

- eKYC & electronic signatures

- Privacy by design

- Continuous audits & training

FINMA-aligned credit platform: underwriting, portfolio protection, liquidity and growth

Underwriting across loans, cards and leases uses scorecards, eKYC and affordability checks to enforce FINMA-aligned credit policy and dynamic pricing. Portfolio monitoring, collections and fraud detection preserve asset quality, supported by ALM, securitisations and deposit funding to secure liquidity. Product design, partner cards and lifecycle marketing drive origination and retention while continuous audit and training sustain controls.

| Metric (2024) | Value |

|---|---|

| Loan portfolio | N/A (2024) |

| Return on equity | N/A (2024) |

Delivered as Displayed

Business Model Canvas

The Business Model Canvas you’re previewing is the actual deliverable—not a mockup. When you purchase, you’ll receive this same comprehensive Cembra Money Bank canvas in full, ready-to-edit Word and Excel files. No surprises, just the exact document shown here.