Cemex Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

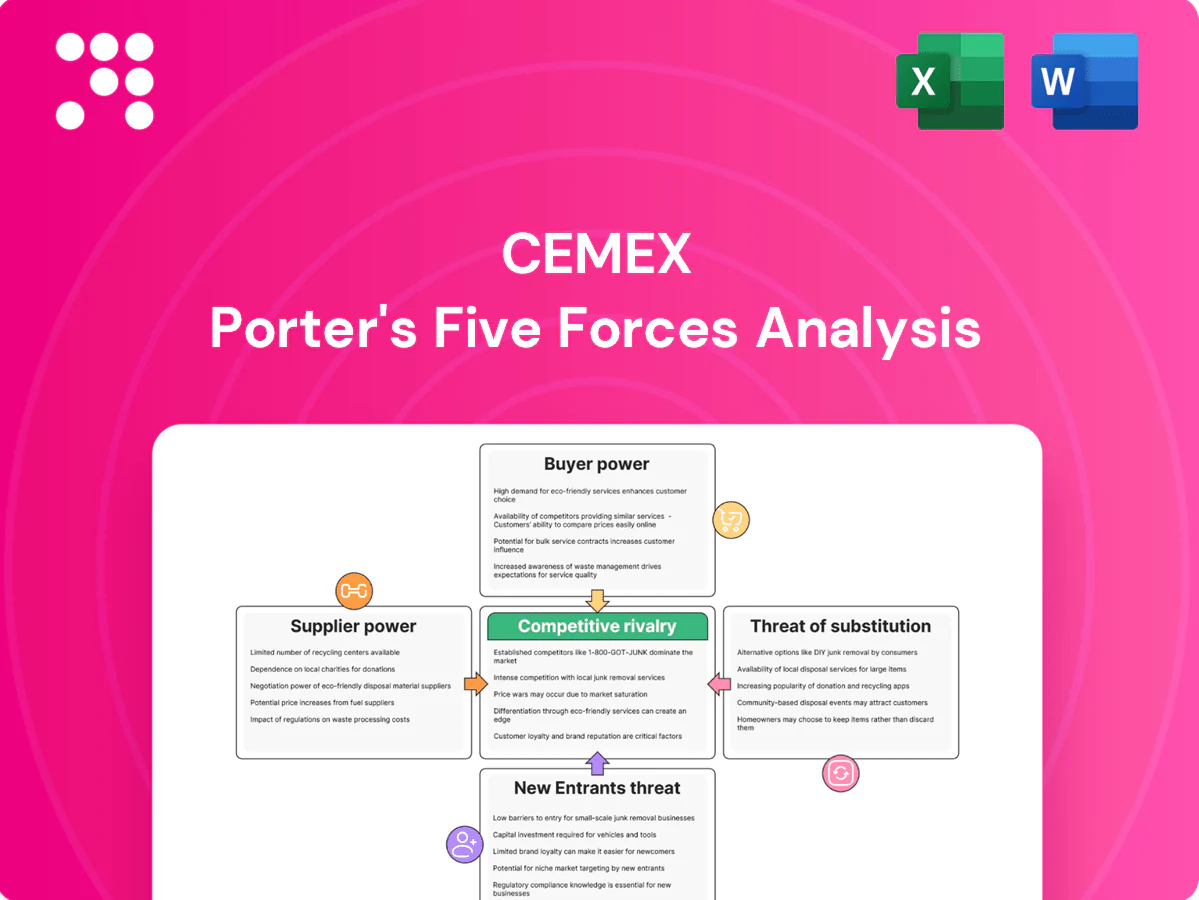

Cemex operates in a highly competitive cement market with intense rivalry, significant supplier influence on input costs, moderate buyer power, low immediate threat from substitutes, and substantial barriers deterring new entrants. This snapshot highlights pressures on margins, pricing leverage, and strategic expansion constraints. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cemex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs like limestone are largely captive at Cemex, which limits third-party supplier leverage, while additives such as gypsum, pozzolans and specialty chemicals come from a much narrower vendor base. This supplier concentration can increase switching costs and lead times, especially for specialty chemicals critical to performance. Cemex mitigates these risks through multi-sourcing strategies and maintaining internal quarries to secure feedstock and shorten supply chains.

Energy and fuel exposure

Coal, petcoke, natural gas and electricity are major, volatile cost drivers for Cemex, commonly representing roughly 10–15% of cement production costs in the industry as of 2024; utility and fuel suppliers can exert pricing power during shortages or price spikes. Long-term supply contracts and hedging programs partially offset exposure, reducing short-term margin volatility. Cemex’s alternative fuels initiatives, which industry peers report substitution rates near 25–35% by 2024, progressively cut dependency and supplier leverage.

Equipment and maintenance parts

Kilns and grinding mills depend on OEMs for critical spares and services, concentrating purchasing power with a small set of suppliers. Limited qualified vendors for refractory linings and control systems (often under 10 global providers) elevate supplier bargaining power. Preventive maintenance and inventory buffers (typically 30–60 days of critical spares) plus vendor-managed programs help stabilize costs and uptime.

Supplementary cementitious materials

Fly ash and steel slag supply for supplementary cementitious materials hinges on coal power and steel output; decarbonization in those sectors is shifting volumes and logistics, tightening available SCMs and raising supplier leverage and freight costs. Cemex is actively qualifying alternative SCMs and diversifying sources to mitigate supply risk and cost volatility.

- Dependence: SCMs tied to power/steel sectors

- Decarbonization: alters supply profiles and transport

- Market tightness: increases supplier influence and freight costs

- Cemex action: SCM qualification and diversified sourcing

Environmental services and permits

Waste co-processing partners and permit-linked services create bottlenecks for Cemex, as 2024 alternative fuel sourcing remained constrained with roughly 11.5% AFR thermal substitution, narrowing supplier choices and raising niche providers’ leverage. Stringent local permit conditions and compliance specificity further reduce replaceability, increasing supplier negotiation power. Long-standing supplier relationships and proven ESG credentials help Cemex secure better terms and continuity.

- Waste co-processing scarcity raises supplier leverage

- Compliance specificity narrows viable suppliers

- Niche providers can command premium pricing

- Long-term ESG-trusted partners improve contract terms

Quarries limit supplier power; energy ~12%, AFR 11.5%

Cemex captures limestone via internal quarries reducing supplier power, but specialty chemicals and OEM spares concentrate with few vendors. Energy costs (fuel+power ~12% of production in 2024) and limited AFR supply (11.5% substitution in 2024) raise supplier leverage. Diversification, multi-sourcing and 30–60 day spares buffers mitigate risks.

| Item | 2024 metric |

|---|---|

| Energy share | ~12% |

| AFR substitution | 11.5% |

| Spare buffer | 30–60 days |

What is included in the product

Tailored Porter's Five Forces analysis for Cemex that uncovers competitive intensity, supplier and buyer power, threat of substitutes, and barriers to entry, highlighting disruptive trends and strategic levers affecting pricing, margins, and market share.

A concise Cemex Porter's Five Forces one-sheet that clarifies competitive pressure and strategic levers at a glance. Customize force levels, swap data or labels, and export clean charts for decks—no macros required.

Customers Bargaining Power

Large buyers and tenders

Governments, megaprojects and top contractors purchase cement at scale, with many megaprojects exceeding USD 1 billion, driving large-volume tenders; competitive bidding intensifies price pressure and service requirements, compressing margins. Framework agreements lower unit margins but secure volumes and cash flow. Cemex leverages integrated offerings—materials, logistics and digital services—to strengthen tender wins and lock in long-term projects.

Product standardization

Ordinary cement grades and commodity aggregates remain highly standardized, so buyers in 2024 can readily switch suppliers based on price pressure; quality certifications such as ISO 9001 are widespread but not differentiating. Low product differentiation gives customers bargaining leverage, especially on spot and bulk purchases. Cemex and peers mitigate this through tailored value-added mixes and integrated logistics services that shift negotiation toward service and reliability rather than pure price.

Switching and logistics

In ready-mix cement, proximity and narrow delivery windows create practical stickiness for customers, and Cemex’s ~1,300 ready-mix plants worldwide in 2024 reinforce that local presence; overlapping plant networks still permit regional switching, especially for large contractors. Increasing digital ordering and tracking in 2024 raised transparency and expectations, while service reliability typically outweighs minor price differences.

Price sensitivity and cycles

Construction demand is cyclical, amplifying buyer bargaining in downturns. Distributors and retailers negotiate aggressively in slow markets. Indexation clauses and surcharges (fuel/energy) provide partial margin protection while sustainability premiums demand clear ROI; global cement production ~4.1 billion tonnes (2023–24).

- Higher buyer leverage in downturns

- Indexation/surcharges mitigate input volatility

- Sustainability premiums need measurable ROI

Specification influence

Engineers and owners set tight performance specs that determine approved supplier lists, and winning those spec positions can lock demand at the project level; Cemex leverages this by aligning product performance with client specs. Buyers increasingly require low-carbon alternatives and rigorously test equivalence; Cemex’s EPDs and independently verified CO2 footprints and its ~US$17bn 2024 revenue position help acceptance in major projects.

- Specification control drives project wins

- Low-carbon demand rising — rigorous equivalence testing

- Cemex EPDs and verified footprints support acceptance

Buyers squeeze margins despite US$17bn scale

Large-volume buyers and megaproject tenders drive intense price/service pressure, compressing margins despite Cemex’s US$17bn 2024 scale and integrated offerings. Low product differentiation and widespread certifications give buyers switching power; local ready-mix proximity (≈1,300 plants) and reliable logistics partly offset this. Cyclicality raises buyer leverage in downturns; surcharges/indexation and EPD-backed low‑carbon products preserve margins.

| Metric | Value (2023–24) |

|---|---|

| Revenue | US$17bn |

| Ready-mix plants | ≈1,300 |

| Global cement prod. | ≈4.1bn t |

| Buyer leverage | High in downturns |

Full Version Awaits

Cemex Porter's Five Forces Analysis

This preview shows the exact Cemex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, comprehensive and ready for download, containing actionable insights on competitive rivalry, buyer and supplier power, threats of entry and substitution. You'll get this same final file instantly upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Cemex operates in a highly competitive cement market with intense rivalry, significant supplier influence on input costs, moderate buyer power, low immediate threat from substitutes, and substantial barriers deterring new entrants. This snapshot highlights pressures on margins, pricing leverage, and strategic expansion constraints. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cemex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs like limestone are largely captive at Cemex, which limits third-party supplier leverage, while additives such as gypsum, pozzolans and specialty chemicals come from a much narrower vendor base. This supplier concentration can increase switching costs and lead times, especially for specialty chemicals critical to performance. Cemex mitigates these risks through multi-sourcing strategies and maintaining internal quarries to secure feedstock and shorten supply chains.

Energy and fuel exposure

Coal, petcoke, natural gas and electricity are major, volatile cost drivers for Cemex, commonly representing roughly 10–15% of cement production costs in the industry as of 2024; utility and fuel suppliers can exert pricing power during shortages or price spikes. Long-term supply contracts and hedging programs partially offset exposure, reducing short-term margin volatility. Cemex’s alternative fuels initiatives, which industry peers report substitution rates near 25–35% by 2024, progressively cut dependency and supplier leverage.

Equipment and maintenance parts

Kilns and grinding mills depend on OEMs for critical spares and services, concentrating purchasing power with a small set of suppliers. Limited qualified vendors for refractory linings and control systems (often under 10 global providers) elevate supplier bargaining power. Preventive maintenance and inventory buffers (typically 30–60 days of critical spares) plus vendor-managed programs help stabilize costs and uptime.

Supplementary cementitious materials

Fly ash and steel slag supply for supplementary cementitious materials hinges on coal power and steel output; decarbonization in those sectors is shifting volumes and logistics, tightening available SCMs and raising supplier leverage and freight costs. Cemex is actively qualifying alternative SCMs and diversifying sources to mitigate supply risk and cost volatility.

- Dependence: SCMs tied to power/steel sectors

- Decarbonization: alters supply profiles and transport

- Market tightness: increases supplier influence and freight costs

- Cemex action: SCM qualification and diversified sourcing

Environmental services and permits

Waste co-processing partners and permit-linked services create bottlenecks for Cemex, as 2024 alternative fuel sourcing remained constrained with roughly 11.5% AFR thermal substitution, narrowing supplier choices and raising niche providers’ leverage. Stringent local permit conditions and compliance specificity further reduce replaceability, increasing supplier negotiation power. Long-standing supplier relationships and proven ESG credentials help Cemex secure better terms and continuity.

- Waste co-processing scarcity raises supplier leverage

- Compliance specificity narrows viable suppliers

- Niche providers can command premium pricing

- Long-term ESG-trusted partners improve contract terms

Quarries limit supplier power; energy ~12%, AFR 11.5%

Cemex captures limestone via internal quarries reducing supplier power, but specialty chemicals and OEM spares concentrate with few vendors. Energy costs (fuel+power ~12% of production in 2024) and limited AFR supply (11.5% substitution in 2024) raise supplier leverage. Diversification, multi-sourcing and 30–60 day spares buffers mitigate risks.

| Item | 2024 metric |

|---|---|

| Energy share | ~12% |

| AFR substitution | 11.5% |

| Spare buffer | 30–60 days |

What is included in the product

Tailored Porter's Five Forces analysis for Cemex that uncovers competitive intensity, supplier and buyer power, threat of substitutes, and barriers to entry, highlighting disruptive trends and strategic levers affecting pricing, margins, and market share.

A concise Cemex Porter's Five Forces one-sheet that clarifies competitive pressure and strategic levers at a glance. Customize force levels, swap data or labels, and export clean charts for decks—no macros required.

Customers Bargaining Power

Large buyers and tenders

Governments, megaprojects and top contractors purchase cement at scale, with many megaprojects exceeding USD 1 billion, driving large-volume tenders; competitive bidding intensifies price pressure and service requirements, compressing margins. Framework agreements lower unit margins but secure volumes and cash flow. Cemex leverages integrated offerings—materials, logistics and digital services—to strengthen tender wins and lock in long-term projects.

Product standardization

Ordinary cement grades and commodity aggregates remain highly standardized, so buyers in 2024 can readily switch suppliers based on price pressure; quality certifications such as ISO 9001 are widespread but not differentiating. Low product differentiation gives customers bargaining leverage, especially on spot and bulk purchases. Cemex and peers mitigate this through tailored value-added mixes and integrated logistics services that shift negotiation toward service and reliability rather than pure price.

Switching and logistics

In ready-mix cement, proximity and narrow delivery windows create practical stickiness for customers, and Cemex’s ~1,300 ready-mix plants worldwide in 2024 reinforce that local presence; overlapping plant networks still permit regional switching, especially for large contractors. Increasing digital ordering and tracking in 2024 raised transparency and expectations, while service reliability typically outweighs minor price differences.

Price sensitivity and cycles

Construction demand is cyclical, amplifying buyer bargaining in downturns. Distributors and retailers negotiate aggressively in slow markets. Indexation clauses and surcharges (fuel/energy) provide partial margin protection while sustainability premiums demand clear ROI; global cement production ~4.1 billion tonnes (2023–24).

- Higher buyer leverage in downturns

- Indexation/surcharges mitigate input volatility

- Sustainability premiums need measurable ROI

Specification influence

Engineers and owners set tight performance specs that determine approved supplier lists, and winning those spec positions can lock demand at the project level; Cemex leverages this by aligning product performance with client specs. Buyers increasingly require low-carbon alternatives and rigorously test equivalence; Cemex’s EPDs and independently verified CO2 footprints and its ~US$17bn 2024 revenue position help acceptance in major projects.

- Specification control drives project wins

- Low-carbon demand rising — rigorous equivalence testing

- Cemex EPDs and verified footprints support acceptance

Buyers squeeze margins despite US$17bn scale

Large-volume buyers and megaproject tenders drive intense price/service pressure, compressing margins despite Cemex’s US$17bn 2024 scale and integrated offerings. Low product differentiation and widespread certifications give buyers switching power; local ready-mix proximity (≈1,300 plants) and reliable logistics partly offset this. Cyclicality raises buyer leverage in downturns; surcharges/indexation and EPD-backed low‑carbon products preserve margins.

| Metric | Value (2023–24) |

|---|---|

| Revenue | US$17bn |

| Ready-mix plants | ≈1,300 |

| Global cement prod. | ≈4.1bn t |

| Buyer leverage | High in downturns |

Full Version Awaits

Cemex Porter's Five Forces Analysis

This preview shows the exact Cemex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, comprehensive and ready for download, containing actionable insights on competitive rivalry, buyer and supplier power, threats of entry and substitution. You'll get this same final file instantly upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Cemex operates in a highly competitive cement market with intense rivalry, significant supplier influence on input costs, moderate buyer power, low immediate threat from substitutes, and substantial barriers deterring new entrants. This snapshot highlights pressures on margins, pricing leverage, and strategic expansion constraints. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cemex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs like limestone are largely captive at Cemex, which limits third-party supplier leverage, while additives such as gypsum, pozzolans and specialty chemicals come from a much narrower vendor base. This supplier concentration can increase switching costs and lead times, especially for specialty chemicals critical to performance. Cemex mitigates these risks through multi-sourcing strategies and maintaining internal quarries to secure feedstock and shorten supply chains.

Energy and fuel exposure

Coal, petcoke, natural gas and electricity are major, volatile cost drivers for Cemex, commonly representing roughly 10–15% of cement production costs in the industry as of 2024; utility and fuel suppliers can exert pricing power during shortages or price spikes. Long-term supply contracts and hedging programs partially offset exposure, reducing short-term margin volatility. Cemex’s alternative fuels initiatives, which industry peers report substitution rates near 25–35% by 2024, progressively cut dependency and supplier leverage.

Equipment and maintenance parts

Kilns and grinding mills depend on OEMs for critical spares and services, concentrating purchasing power with a small set of suppliers. Limited qualified vendors for refractory linings and control systems (often under 10 global providers) elevate supplier bargaining power. Preventive maintenance and inventory buffers (typically 30–60 days of critical spares) plus vendor-managed programs help stabilize costs and uptime.

Supplementary cementitious materials

Fly ash and steel slag supply for supplementary cementitious materials hinges on coal power and steel output; decarbonization in those sectors is shifting volumes and logistics, tightening available SCMs and raising supplier leverage and freight costs. Cemex is actively qualifying alternative SCMs and diversifying sources to mitigate supply risk and cost volatility.

- Dependence: SCMs tied to power/steel sectors

- Decarbonization: alters supply profiles and transport

- Market tightness: increases supplier influence and freight costs

- Cemex action: SCM qualification and diversified sourcing

Environmental services and permits

Waste co-processing partners and permit-linked services create bottlenecks for Cemex, as 2024 alternative fuel sourcing remained constrained with roughly 11.5% AFR thermal substitution, narrowing supplier choices and raising niche providers’ leverage. Stringent local permit conditions and compliance specificity further reduce replaceability, increasing supplier negotiation power. Long-standing supplier relationships and proven ESG credentials help Cemex secure better terms and continuity.

- Waste co-processing scarcity raises supplier leverage

- Compliance specificity narrows viable suppliers

- Niche providers can command premium pricing

- Long-term ESG-trusted partners improve contract terms

Quarries limit supplier power; energy ~12%, AFR 11.5%

Cemex captures limestone via internal quarries reducing supplier power, but specialty chemicals and OEM spares concentrate with few vendors. Energy costs (fuel+power ~12% of production in 2024) and limited AFR supply (11.5% substitution in 2024) raise supplier leverage. Diversification, multi-sourcing and 30–60 day spares buffers mitigate risks.

| Item | 2024 metric |

|---|---|

| Energy share | ~12% |

| AFR substitution | 11.5% |

| Spare buffer | 30–60 days |

What is included in the product

Tailored Porter's Five Forces analysis for Cemex that uncovers competitive intensity, supplier and buyer power, threat of substitutes, and barriers to entry, highlighting disruptive trends and strategic levers affecting pricing, margins, and market share.

A concise Cemex Porter's Five Forces one-sheet that clarifies competitive pressure and strategic levers at a glance. Customize force levels, swap data or labels, and export clean charts for decks—no macros required.

Customers Bargaining Power

Large buyers and tenders

Governments, megaprojects and top contractors purchase cement at scale, with many megaprojects exceeding USD 1 billion, driving large-volume tenders; competitive bidding intensifies price pressure and service requirements, compressing margins. Framework agreements lower unit margins but secure volumes and cash flow. Cemex leverages integrated offerings—materials, logistics and digital services—to strengthen tender wins and lock in long-term projects.

Product standardization

Ordinary cement grades and commodity aggregates remain highly standardized, so buyers in 2024 can readily switch suppliers based on price pressure; quality certifications such as ISO 9001 are widespread but not differentiating. Low product differentiation gives customers bargaining leverage, especially on spot and bulk purchases. Cemex and peers mitigate this through tailored value-added mixes and integrated logistics services that shift negotiation toward service and reliability rather than pure price.

Switching and logistics

In ready-mix cement, proximity and narrow delivery windows create practical stickiness for customers, and Cemex’s ~1,300 ready-mix plants worldwide in 2024 reinforce that local presence; overlapping plant networks still permit regional switching, especially for large contractors. Increasing digital ordering and tracking in 2024 raised transparency and expectations, while service reliability typically outweighs minor price differences.

Price sensitivity and cycles

Construction demand is cyclical, amplifying buyer bargaining in downturns. Distributors and retailers negotiate aggressively in slow markets. Indexation clauses and surcharges (fuel/energy) provide partial margin protection while sustainability premiums demand clear ROI; global cement production ~4.1 billion tonnes (2023–24).

- Higher buyer leverage in downturns

- Indexation/surcharges mitigate input volatility

- Sustainability premiums need measurable ROI

Specification influence

Engineers and owners set tight performance specs that determine approved supplier lists, and winning those spec positions can lock demand at the project level; Cemex leverages this by aligning product performance with client specs. Buyers increasingly require low-carbon alternatives and rigorously test equivalence; Cemex’s EPDs and independently verified CO2 footprints and its ~US$17bn 2024 revenue position help acceptance in major projects.

- Specification control drives project wins

- Low-carbon demand rising — rigorous equivalence testing

- Cemex EPDs and verified footprints support acceptance

Buyers squeeze margins despite US$17bn scale

Large-volume buyers and megaproject tenders drive intense price/service pressure, compressing margins despite Cemex’s US$17bn 2024 scale and integrated offerings. Low product differentiation and widespread certifications give buyers switching power; local ready-mix proximity (≈1,300 plants) and reliable logistics partly offset this. Cyclicality raises buyer leverage in downturns; surcharges/indexation and EPD-backed low‑carbon products preserve margins.

| Metric | Value (2023–24) |

|---|---|

| Revenue | US$17bn |

| Ready-mix plants | ≈1,300 |

| Global cement prod. | ≈4.1bn t |

| Buyer leverage | High in downturns |

Full Version Awaits

Cemex Porter's Five Forces Analysis

This preview shows the exact Cemex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, comprehensive and ready for download, containing actionable insights on competitive rivalry, buyer and supplier power, threats of entry and substitution. You'll get this same final file instantly upon payment.