Central Bank of India Business Model Canvas

Unlock the strategic blueprint of a leading Indian bank's Business Model Canvas

Unlock the full strategic blueprint behind Central Bank of India's Business Model Canvas—three to five sentence preview here shows how customer segments, revenue streams, and partnerships drive growth. Purchase the complete, editable Canvas to get section-by-section insights, actionable recommendations, and formats ready for presentations and planning.

Partnerships

Regulators and Government Bodies

Partnerships with RBI, Ministry of Finance and other regulators ensure compliance, access to liquidity windows and policy alignment; RBI's repo rate stood at 6.50% in June 2024, shaping lending costs. These ties enable Central Bank of India to participate in government schemes and meet 40% priority-sector lending norms. Coordination supports stable interest rate transmission and financial inclusion, strengthening credibility and public trust.

Payment Networks and Switches

Alliances with NPCI, UPI, RuPay, Visa and Mastercard enable seamless payments and omnichannel acceptance, leveraging RuPay’s >1 billion cards and UPI’s >100 billion transactions in FY2023-24 to expand card issuance and digital volumes. Co-development on switches enhances security, scalability and UX, while participation in networks drives material fee income and increases customer stickiness.

Fintechs and Technology Providers

Collaborations with fintechs, core-banking vendors, cloud and cybersecurity firms accelerate digital innovation for Central Bank of India, cutting time-to-market for new products by 30–50% and lowering operating costs by around 20–25% (industry benchmarks, 2024).

Correspondent Banking and BC Agents

Tie-ups with correspondent banks and a large BC agent network extend Central Bank of India's reach into underserved areas, facilitating remittances, cash-in/cash-out and limited cross-border services to support financial inclusion and deposit growth; by FY2023-24 the bank leveraged its BCs and correspondents to scale last-mile delivery at lower unit cost.

- BC reach: expanded branchless outlets to deepen rural deposits

- Services: remittances, CICO, cross-border payouts

- Benefit: lower last-mile cost, higher CASA and deposit mobilization

Insurers and Capital Market Intermediaries

Insurers, mutual funds and broking partners enable Central Bank of India to distribute third-party insurance, investment and pension solutions under one roof, improving customer stickiness; Indian mutual fund AUM crossed ₹50 trillion in 2024, enlarging product inventory for bancassurance tie-ups.

- Third-party distribution via bancassurance

- One-stop insurance, investment, pension

- Shared revenue boosts non-interest income

- Joint training and co-marketing raise sales productivity

Partnerships boost liquidity, compliance & digital reach — RBI 6.50%

Key partnerships (RBI, MoF, NPCI, fintechs, BCs, insurers) secure liquidity, compliance, digital reach and fee income; RBI repo 6.50% (Jun 2024), UPI >100bn txns FY2023-24, RuPay >1bn cards, mutual fund AUM ₹50tn (2024); BCs raised rural CASA and cut last-mile cost.

| Partner | Metric | 2024 |

|---|---|---|

| RBI | Repo | 6.50% |

| NPCI | UPI txns | >100bn |

| RuPay | Cards | >1bn |

What is included in the product

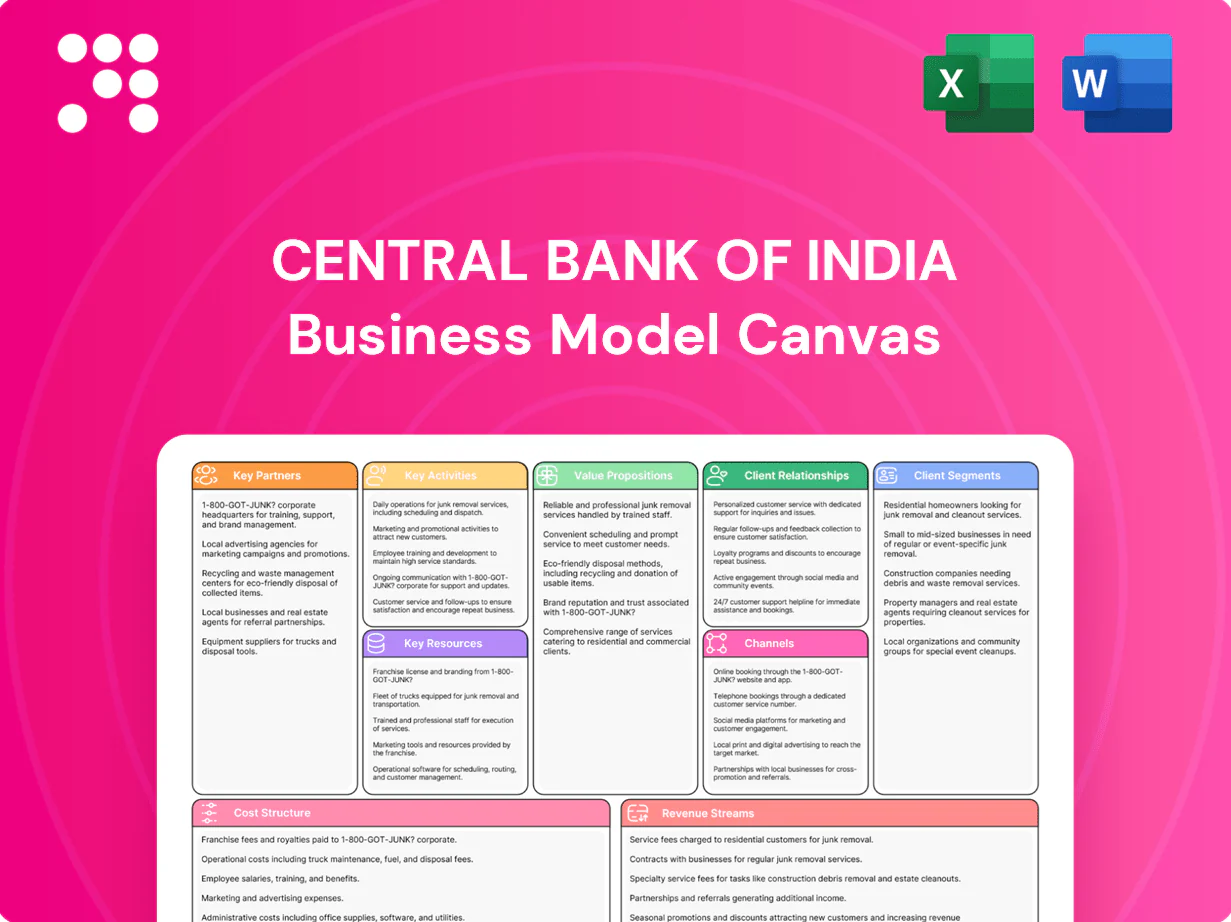

A comprehensive Business Model Canvas for Central Bank of India detailing customer segments, channels, value propositions, key activities and partners, revenue/cost structure and risk profile, with SWOT-linked insights to support strategic decisions and investor presentations.

High-level, editable Business Model Canvas for Central Bank of India that condenses strategy into a one-page snapshot to quickly identify strengths, risks, and growth levers. Shareable and ready for boardrooms or teams, it saves hours of structuring while enabling fast comparison, collaboration, and strategic decision-making.

Activities

Deposit Mobilization and CASA Growth

Designing attractive savings, current and term deposit schemes drives Central Bank of India’s deposit mix, targeting CASA-led cost efficiency; PSBs’ average CASA was ~39% in FY2024 (RBI). Marketing, rural branch outreach and digital onboarding push low-cost CASA balances. Active liquidity management aligns deposit tenor with lending needs, while continuous rate benchmarking sustains competitiveness.

Credit Underwriting and Portfolio Management

End-to-end lending across retail, MSME, corporate and agri is central to Central Bank of India’s credit model, with robust underwriting, ongoing monitoring and collections to control NPA risk. Sectoral exposure limits and RBI-style stress testing guide portfolio actions; system GNPA was about 5.3% in Mar 2024. Active recovery and targeted restructuring optimize portfolio health and improve coverage over time.

Digital Banking Operations

Operating internet, mobile, UPI, and card platforms provides Central Bank of India 24x7 services, leveraging India's UPI network which processed about 86.5 billion transactions in FY 2023‑24 (NPCI). Continuous enhancements target improved UX, security, and uptime with industry SLAs above 99.9%. Data analytics personalize offers and detect fraud in real time, while API integrations enable partnerships across fintech ecosystems.

Treasury and ALM

Treasury manages SLR investments to meet the RBI 18% requirement, steers liquidity and mitigates interest-rate risk amid a 2024 repo rate of 6.50%, while ALM balances asset-liability tenors to protect margins. Trading and hedging optimize returns within board-set risk limits and approved VaR/exposure caps. Regulatory reporting delivers timely disclosures to RBI and stakeholders.

- SLR requirement: 18%

- Repo rate (2024): 6.50%

- ALM: tenor & margin optimization

- Trading/hedging: returns within VaR/exposure limits

- Regulatory reporting: RBI disclosures

Compliance and Financial Inclusion

Strict KYC/AML, regular audits and RBI compliance reviews safeguard Central Bank of India operations; risk and control frameworks and stress-testing maintain resilience across retail and MSME portfolios in FY 2023-24.

- Regulatory adherence: RBI compliance reviews FY 2023-24

- Inclusion: active participation in PMJDY and DBT disbursals FY 2023-24

- Customer trust: education programs and grievance redressal mechanisms

- Controls: audit, KYC/AML and risk frameworks

CASA ~39%, digital onboarding, ALM vs 6.50% repo

Designing CASA-led deposit products (PSB CASA ~39% FY2024) and digital onboarding drive low-cost funding; treasury manages SLR 18% and ALM against a 6.50% repo (2024). End-to-end lending across retail, MSME, corporate and agri with underwriting, monitoring and recovery keeps GNPA ~5.3% (Mar 2024). Digital platforms (UPI ~86.5bn txns FY2023-24) plus KYC/AML, audits and RBI compliance sustain operations.

| Metric | Value |

|---|---|

| CASA (PSB avg) | ~39% FY2024 |

| GNPA | ~5.3% Mar 2024 |

| UPI volumes | 86.5 bn FY2023-24 |

| SLR | 18% |

| Repo rate | 6.50% 2024 |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Central Bank of India Business Model Canvas you'll receive after purchase; it's not a mockup. On completion, you'll download the full, editable file formatted identically for immediate use in analysis, presentation, or modification—no hidden pages, no surprises.

Unlock the strategic blueprint of a leading Indian bank's Business Model Canvas

Unlock the full strategic blueprint behind Central Bank of India's Business Model Canvas—three to five sentence preview here shows how customer segments, revenue streams, and partnerships drive growth. Purchase the complete, editable Canvas to get section-by-section insights, actionable recommendations, and formats ready for presentations and planning.

Partnerships

Regulators and Government Bodies

Partnerships with RBI, Ministry of Finance and other regulators ensure compliance, access to liquidity windows and policy alignment; RBI's repo rate stood at 6.50% in June 2024, shaping lending costs. These ties enable Central Bank of India to participate in government schemes and meet 40% priority-sector lending norms. Coordination supports stable interest rate transmission and financial inclusion, strengthening credibility and public trust.

Payment Networks and Switches

Alliances with NPCI, UPI, RuPay, Visa and Mastercard enable seamless payments and omnichannel acceptance, leveraging RuPay’s >1 billion cards and UPI’s >100 billion transactions in FY2023-24 to expand card issuance and digital volumes. Co-development on switches enhances security, scalability and UX, while participation in networks drives material fee income and increases customer stickiness.

Fintechs and Technology Providers

Collaborations with fintechs, core-banking vendors, cloud and cybersecurity firms accelerate digital innovation for Central Bank of India, cutting time-to-market for new products by 30–50% and lowering operating costs by around 20–25% (industry benchmarks, 2024).

Correspondent Banking and BC Agents

Tie-ups with correspondent banks and a large BC agent network extend Central Bank of India's reach into underserved areas, facilitating remittances, cash-in/cash-out and limited cross-border services to support financial inclusion and deposit growth; by FY2023-24 the bank leveraged its BCs and correspondents to scale last-mile delivery at lower unit cost.

- BC reach: expanded branchless outlets to deepen rural deposits

- Services: remittances, CICO, cross-border payouts

- Benefit: lower last-mile cost, higher CASA and deposit mobilization

Insurers and Capital Market Intermediaries

Insurers, mutual funds and broking partners enable Central Bank of India to distribute third-party insurance, investment and pension solutions under one roof, improving customer stickiness; Indian mutual fund AUM crossed ₹50 trillion in 2024, enlarging product inventory for bancassurance tie-ups.

- Third-party distribution via bancassurance

- One-stop insurance, investment, pension

- Shared revenue boosts non-interest income

- Joint training and co-marketing raise sales productivity

Partnerships boost liquidity, compliance & digital reach — RBI 6.50%

Key partnerships (RBI, MoF, NPCI, fintechs, BCs, insurers) secure liquidity, compliance, digital reach and fee income; RBI repo 6.50% (Jun 2024), UPI >100bn txns FY2023-24, RuPay >1bn cards, mutual fund AUM ₹50tn (2024); BCs raised rural CASA and cut last-mile cost.

| Partner | Metric | 2024 |

|---|---|---|

| RBI | Repo | 6.50% |

| NPCI | UPI txns | >100bn |

| RuPay | Cards | >1bn |

What is included in the product

A comprehensive Business Model Canvas for Central Bank of India detailing customer segments, channels, value propositions, key activities and partners, revenue/cost structure and risk profile, with SWOT-linked insights to support strategic decisions and investor presentations.

High-level, editable Business Model Canvas for Central Bank of India that condenses strategy into a one-page snapshot to quickly identify strengths, risks, and growth levers. Shareable and ready for boardrooms or teams, it saves hours of structuring while enabling fast comparison, collaboration, and strategic decision-making.

Activities

Deposit Mobilization and CASA Growth

Designing attractive savings, current and term deposit schemes drives Central Bank of India’s deposit mix, targeting CASA-led cost efficiency; PSBs’ average CASA was ~39% in FY2024 (RBI). Marketing, rural branch outreach and digital onboarding push low-cost CASA balances. Active liquidity management aligns deposit tenor with lending needs, while continuous rate benchmarking sustains competitiveness.

Credit Underwriting and Portfolio Management

End-to-end lending across retail, MSME, corporate and agri is central to Central Bank of India’s credit model, with robust underwriting, ongoing monitoring and collections to control NPA risk. Sectoral exposure limits and RBI-style stress testing guide portfolio actions; system GNPA was about 5.3% in Mar 2024. Active recovery and targeted restructuring optimize portfolio health and improve coverage over time.

Digital Banking Operations

Operating internet, mobile, UPI, and card platforms provides Central Bank of India 24x7 services, leveraging India's UPI network which processed about 86.5 billion transactions in FY 2023‑24 (NPCI). Continuous enhancements target improved UX, security, and uptime with industry SLAs above 99.9%. Data analytics personalize offers and detect fraud in real time, while API integrations enable partnerships across fintech ecosystems.

Treasury and ALM

Treasury manages SLR investments to meet the RBI 18% requirement, steers liquidity and mitigates interest-rate risk amid a 2024 repo rate of 6.50%, while ALM balances asset-liability tenors to protect margins. Trading and hedging optimize returns within board-set risk limits and approved VaR/exposure caps. Regulatory reporting delivers timely disclosures to RBI and stakeholders.

- SLR requirement: 18%

- Repo rate (2024): 6.50%

- ALM: tenor & margin optimization

- Trading/hedging: returns within VaR/exposure limits

- Regulatory reporting: RBI disclosures

Compliance and Financial Inclusion

Strict KYC/AML, regular audits and RBI compliance reviews safeguard Central Bank of India operations; risk and control frameworks and stress-testing maintain resilience across retail and MSME portfolios in FY 2023-24.

- Regulatory adherence: RBI compliance reviews FY 2023-24

- Inclusion: active participation in PMJDY and DBT disbursals FY 2023-24

- Customer trust: education programs and grievance redressal mechanisms

- Controls: audit, KYC/AML and risk frameworks

CASA ~39%, digital onboarding, ALM vs 6.50% repo

Designing CASA-led deposit products (PSB CASA ~39% FY2024) and digital onboarding drive low-cost funding; treasury manages SLR 18% and ALM against a 6.50% repo (2024). End-to-end lending across retail, MSME, corporate and agri with underwriting, monitoring and recovery keeps GNPA ~5.3% (Mar 2024). Digital platforms (UPI ~86.5bn txns FY2023-24) plus KYC/AML, audits and RBI compliance sustain operations.

| Metric | Value |

|---|---|

| CASA (PSB avg) | ~39% FY2024 |

| GNPA | ~5.3% Mar 2024 |

| UPI volumes | 86.5 bn FY2023-24 |

| SLR | 18% |

| Repo rate | 6.50% 2024 |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Central Bank of India Business Model Canvas you'll receive after purchase; it's not a mockup. On completion, you'll download the full, editable file formatted identically for immediate use in analysis, presentation, or modification—no hidden pages, no surprises.

Description

Unlock the strategic blueprint of a leading Indian bank's Business Model Canvas

Unlock the full strategic blueprint behind Central Bank of India's Business Model Canvas—three to five sentence preview here shows how customer segments, revenue streams, and partnerships drive growth. Purchase the complete, editable Canvas to get section-by-section insights, actionable recommendations, and formats ready for presentations and planning.

Partnerships

Regulators and Government Bodies

Partnerships with RBI, Ministry of Finance and other regulators ensure compliance, access to liquidity windows and policy alignment; RBI's repo rate stood at 6.50% in June 2024, shaping lending costs. These ties enable Central Bank of India to participate in government schemes and meet 40% priority-sector lending norms. Coordination supports stable interest rate transmission and financial inclusion, strengthening credibility and public trust.

Payment Networks and Switches

Alliances with NPCI, UPI, RuPay, Visa and Mastercard enable seamless payments and omnichannel acceptance, leveraging RuPay’s >1 billion cards and UPI’s >100 billion transactions in FY2023-24 to expand card issuance and digital volumes. Co-development on switches enhances security, scalability and UX, while participation in networks drives material fee income and increases customer stickiness.

Fintechs and Technology Providers

Collaborations with fintechs, core-banking vendors, cloud and cybersecurity firms accelerate digital innovation for Central Bank of India, cutting time-to-market for new products by 30–50% and lowering operating costs by around 20–25% (industry benchmarks, 2024).

Correspondent Banking and BC Agents

Tie-ups with correspondent banks and a large BC agent network extend Central Bank of India's reach into underserved areas, facilitating remittances, cash-in/cash-out and limited cross-border services to support financial inclusion and deposit growth; by FY2023-24 the bank leveraged its BCs and correspondents to scale last-mile delivery at lower unit cost.

- BC reach: expanded branchless outlets to deepen rural deposits

- Services: remittances, CICO, cross-border payouts

- Benefit: lower last-mile cost, higher CASA and deposit mobilization

Insurers and Capital Market Intermediaries

Insurers, mutual funds and broking partners enable Central Bank of India to distribute third-party insurance, investment and pension solutions under one roof, improving customer stickiness; Indian mutual fund AUM crossed ₹50 trillion in 2024, enlarging product inventory for bancassurance tie-ups.

- Third-party distribution via bancassurance

- One-stop insurance, investment, pension

- Shared revenue boosts non-interest income

- Joint training and co-marketing raise sales productivity

Partnerships boost liquidity, compliance & digital reach — RBI 6.50%

Key partnerships (RBI, MoF, NPCI, fintechs, BCs, insurers) secure liquidity, compliance, digital reach and fee income; RBI repo 6.50% (Jun 2024), UPI >100bn txns FY2023-24, RuPay >1bn cards, mutual fund AUM ₹50tn (2024); BCs raised rural CASA and cut last-mile cost.

| Partner | Metric | 2024 |

|---|---|---|

| RBI | Repo | 6.50% |

| NPCI | UPI txns | >100bn |

| RuPay | Cards | >1bn |

What is included in the product

A comprehensive Business Model Canvas for Central Bank of India detailing customer segments, channels, value propositions, key activities and partners, revenue/cost structure and risk profile, with SWOT-linked insights to support strategic decisions and investor presentations.

High-level, editable Business Model Canvas for Central Bank of India that condenses strategy into a one-page snapshot to quickly identify strengths, risks, and growth levers. Shareable and ready for boardrooms or teams, it saves hours of structuring while enabling fast comparison, collaboration, and strategic decision-making.

Activities

Deposit Mobilization and CASA Growth

Designing attractive savings, current and term deposit schemes drives Central Bank of India’s deposit mix, targeting CASA-led cost efficiency; PSBs’ average CASA was ~39% in FY2024 (RBI). Marketing, rural branch outreach and digital onboarding push low-cost CASA balances. Active liquidity management aligns deposit tenor with lending needs, while continuous rate benchmarking sustains competitiveness.

Credit Underwriting and Portfolio Management

End-to-end lending across retail, MSME, corporate and agri is central to Central Bank of India’s credit model, with robust underwriting, ongoing monitoring and collections to control NPA risk. Sectoral exposure limits and RBI-style stress testing guide portfolio actions; system GNPA was about 5.3% in Mar 2024. Active recovery and targeted restructuring optimize portfolio health and improve coverage over time.

Digital Banking Operations

Operating internet, mobile, UPI, and card platforms provides Central Bank of India 24x7 services, leveraging India's UPI network which processed about 86.5 billion transactions in FY 2023‑24 (NPCI). Continuous enhancements target improved UX, security, and uptime with industry SLAs above 99.9%. Data analytics personalize offers and detect fraud in real time, while API integrations enable partnerships across fintech ecosystems.

Treasury and ALM

Treasury manages SLR investments to meet the RBI 18% requirement, steers liquidity and mitigates interest-rate risk amid a 2024 repo rate of 6.50%, while ALM balances asset-liability tenors to protect margins. Trading and hedging optimize returns within board-set risk limits and approved VaR/exposure caps. Regulatory reporting delivers timely disclosures to RBI and stakeholders.

- SLR requirement: 18%

- Repo rate (2024): 6.50%

- ALM: tenor & margin optimization

- Trading/hedging: returns within VaR/exposure limits

- Regulatory reporting: RBI disclosures

Compliance and Financial Inclusion

Strict KYC/AML, regular audits and RBI compliance reviews safeguard Central Bank of India operations; risk and control frameworks and stress-testing maintain resilience across retail and MSME portfolios in FY 2023-24.

- Regulatory adherence: RBI compliance reviews FY 2023-24

- Inclusion: active participation in PMJDY and DBT disbursals FY 2023-24

- Customer trust: education programs and grievance redressal mechanisms

- Controls: audit, KYC/AML and risk frameworks

CASA ~39%, digital onboarding, ALM vs 6.50% repo

Designing CASA-led deposit products (PSB CASA ~39% FY2024) and digital onboarding drive low-cost funding; treasury manages SLR 18% and ALM against a 6.50% repo (2024). End-to-end lending across retail, MSME, corporate and agri with underwriting, monitoring and recovery keeps GNPA ~5.3% (Mar 2024). Digital platforms (UPI ~86.5bn txns FY2023-24) plus KYC/AML, audits and RBI compliance sustain operations.

| Metric | Value |

|---|---|

| CASA (PSB avg) | ~39% FY2024 |

| GNPA | ~5.3% Mar 2024 |

| UPI volumes | 86.5 bn FY2023-24 |

| SLR | 18% |

| Repo rate | 6.50% 2024 |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Central Bank of India Business Model Canvas you'll receive after purchase; it's not a mockup. On completion, you'll download the full, editable file formatted identically for immediate use in analysis, presentation, or modification—no hidden pages, no surprises.