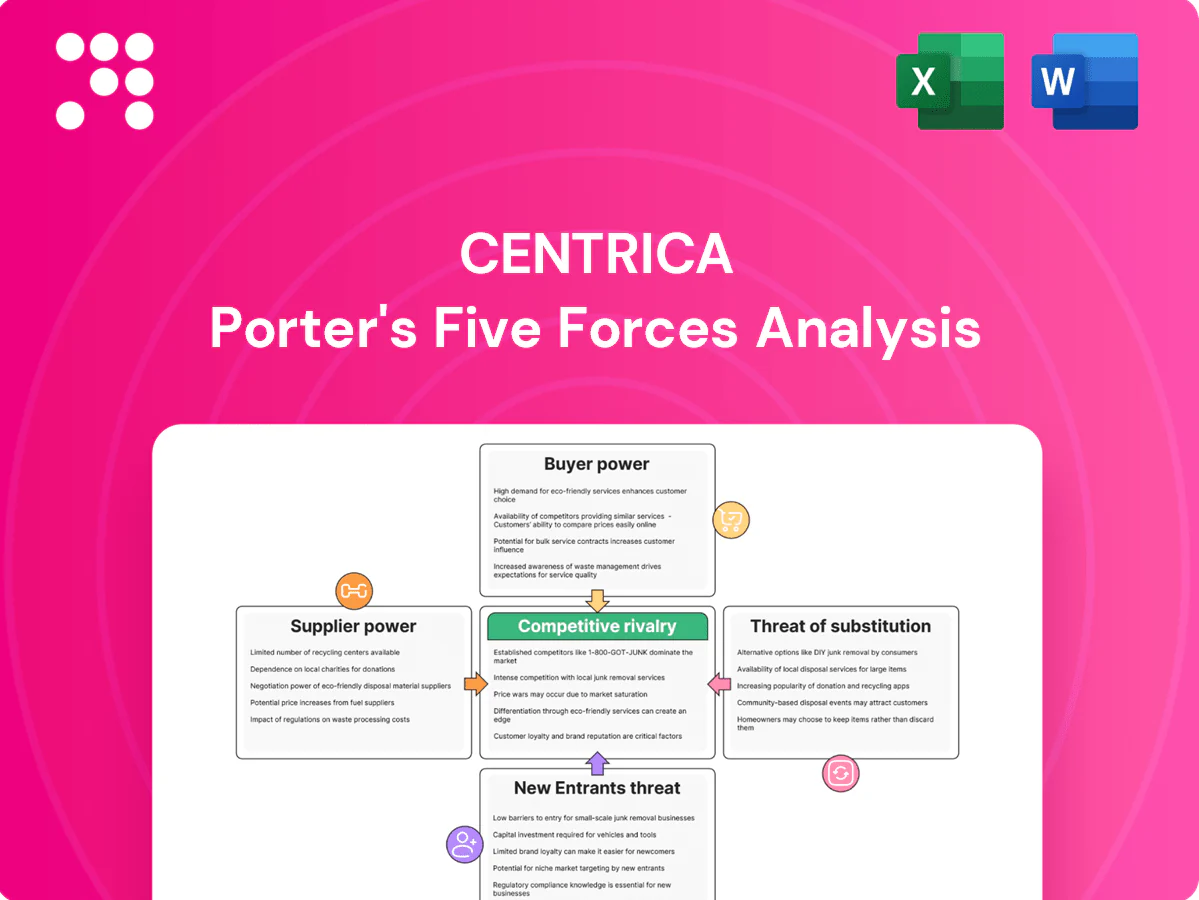

Centrica Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Centrica operates in a tightly contested UK energy market where supplier bargaining, regulatory shifts, and rising clean-tech substitutes shape profitability; buyer power and margin pressure are central concerns. This brief highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated upstream fuel sources

Wholesale gas producers, LNG suppliers and large generators remain relatively concentrated—top exporters such as Qatar, Australia and the US account for around 60% of global LNG export capacity, giving them leverage on price and contract terms. Global commodity volatility in 2023–24, with NBP and Henry Hub swings, amplified supplier bargaining power. Centrica mitigates exposure via diversified sourcing and hedging programs and by maintaining storage and long-term contracts, which partially offset but do not eliminate spike risk.

Regulated networks as essential inputs

Transmission and distribution operators are regulated monopolies, creating unavoidable dependency for Centrica. While tariffs are regulated, access rules and service quality can affect costs and reliability; network charges were about 25–30% of UK retail electricity bills in 2024. Centrica has limited negotiation leverage, so operational planning and active advocacy with Ofgem and regional DNOs are key mitigants.

OEMs and tech vendors

OEMs and tech vendors (boilers, heat pumps, smart meters, platforms) are concentrated among a handful of major suppliers, with the top 5 firms capturing roughly 60–70% of UK device volumes in 2024, so standardization lowers switching costs and tempers supplier power. Scarce skilled installers and constrained supply of heat-pump compressors pushed prices up in 2024, with installations around 120,000 units. Centrica uses strategic partnerships and volume commitments to secure availability and mitigate volatility.

Labor and skilled contractors

Field engineers and specialist contractors are critical to Centrica’s service delivery, and tight UK labor markets in 2024 pushed contractor day-rates and technician wages higher, increasing operating costs and supplier bargaining power.

Investing in training pipelines and expanding in-house capabilities can lower dependency on external contractors; union negotiations and stringent safety standards further strengthen supplier leverage.

- c.22,000 employees (2024)

- Rising contractor rates elevate OPEX

- Training reduces supplier reliance

- Union and safety rules amplify bargaining power

Environmental and compliance costs

- Carbon price 2024: EU ETS ≈ €80–95/t

- Costs largely pass-through, limited negotiation

- PPAs vs conventional generation reduce net exposure

- Policy shifts can quickly swing supplier leverage

LNG exporters ~60%; UK networks add 25-30% to retail

Supplier power is elevated: global LNG exporters (Qatar, Australia, US) hold ~60% of export capacity and 2023–24 price volatility raised leverage. Regulated networks drive unavoidable transmission costs (~25–30% of UK retail 2024). OEM concentration and installer shortages (≈120,000 heat pumps installed 2024) push input prices; EU ETS ≈ €80–95/t in 2024.

| Metric | 2024 |

|---|---|

| LNG export share (top exporters) | ~60% |

| Network charges of UK retail | 25–30% |

| Heat pump installs (UK) | ≈120,000 |

| EU ETS price | €80–95/t |

What is included in the product

Tailored Porter's Five Forces analysis for Centrica that uncovers key competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect market share—fully editable for investor, strategy, or academic use.

A concise one-sheet Porter's Five Forces for Centrica that visualizes competitive pressure with a radar chart and customizable ratings—perfect for quick decisions, board decks, or scenario tabs without macros.

Customers Bargaining Power

High switching ease for households

Comparison sites and one-click online onboarding mean UK households can switch suppliers in minutes, driving Ofgem-recorded 2024 switch volumes of about 2.8 million and boosting price sensitivity that compresses retail margins. Service reliability and Centrica’s brand trust help retain customers despite easy churn. Bundled products like smart tariffs and energy+services reduce pure price-led switching by increasing perceived switching costs.

SME procurement sophistication

Many SMEs use brokers and fixed-term contracts, with 2024 market surveys showing over 40% of UK SMEs engaging brokers or aggregators, strengthening their negotiating stance. Aggregated buying power forces suppliers to concede margin pressure, especially at renewal windows. Delivering energy management insights and analytics creates differentiation beyond price, while flexible contract structures (e.g., mix of fixed, index-linked and advisory fees) help balance retention and profitability.

Regulatory price cap influence

The UK energy price cap, set at about £1,928/year for Oct 2023–Sep 2024 and protecting some 27 million households, anchors customer expectations on fair pricing and limits full cost pass-through during volatility, effectively increasing buyer power. Regulator-mandated transparency reduces information asymmetry. Centrica must therefore compete on service quality and add-ons within tighter capped margins.

Demand for green and smart solutions

Customers increasingly prioritize low-carbon tariffs, heat pumps, EV tariffs and smart-home integration, shifting bargaining power to buyers seeking tailored solutions; UK smart meter penetration reached about 55% in 2024 and the UK target of 600,000 heat pumps/year by 2028 underlines demand growth. Centrica can capture value via premium green bundles, financing and clear decarbonization roadmaps that raise willingness to pay.

- Demand: rising preference for low-carbon tariffs, heat pumps, EV tariffs

- Power shift: buyers seek tailored, financed solutions

- Opportunity: premium bundles + clear decarbonization roadmap

Service quality and trust as levers

Outage response, billing accuracy and call-centre performance drive retention for Centrica: British Gas serves about 8 million UK homes and Bord Gáis Energy roughly 1.2 million in Ireland, so poor experiences materially raise churn and customer bargaining power. Proactive maintenance and digital self-serve tools—which Centrica reported expanding in 2024—cut friction and complaints, improving retention and lowering acquisition costs. Reputation effects compound across both brands, amplifying the impact of service lapses.

- Outage response: fast restoration lowers churn

- Billing & call-centre accuracy: direct retention levers

- Digital self-serve & maintenance: reduce complaints, improve NPS

UK switching (~2.8m) and 55% smart meters squeeze energy retail margins

UK household switching (~2.8m in 2024) and price sensitivity compress Centrica retail margins despite brand trust and bundles that raise switching costs. SMEs (40%+ use brokers) exert negotiation pressure at renewals; analytics and flexible contracts help defend margins. Regulatory price cap (~£1,928 for Oct23–Sep24) and 55% smart meter penetration shift power toward informed buyers.

| Metric | 2024 value |

|---|---|

| Household switches | ~2.8m |

| Price cap (yr) | £1,928 |

| Smart meter penetration | ~55% |

| British Gas customers | ~8m homes |

| SMEs using brokers | >40% |

Preview the Actual Deliverable

Centrica Porter's Five Forces Analysis

This preview shows the exact Centrica Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full, professionally formatted document is ready for immediate download after purchase. Use it as-is for decision-making or presentation purposes.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Centrica operates in a tightly contested UK energy market where supplier bargaining, regulatory shifts, and rising clean-tech substitutes shape profitability; buyer power and margin pressure are central concerns. This brief highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated upstream fuel sources

Wholesale gas producers, LNG suppliers and large generators remain relatively concentrated—top exporters such as Qatar, Australia and the US account for around 60% of global LNG export capacity, giving them leverage on price and contract terms. Global commodity volatility in 2023–24, with NBP and Henry Hub swings, amplified supplier bargaining power. Centrica mitigates exposure via diversified sourcing and hedging programs and by maintaining storage and long-term contracts, which partially offset but do not eliminate spike risk.

Regulated networks as essential inputs

Transmission and distribution operators are regulated monopolies, creating unavoidable dependency for Centrica. While tariffs are regulated, access rules and service quality can affect costs and reliability; network charges were about 25–30% of UK retail electricity bills in 2024. Centrica has limited negotiation leverage, so operational planning and active advocacy with Ofgem and regional DNOs are key mitigants.

OEMs and tech vendors

OEMs and tech vendors (boilers, heat pumps, smart meters, platforms) are concentrated among a handful of major suppliers, with the top 5 firms capturing roughly 60–70% of UK device volumes in 2024, so standardization lowers switching costs and tempers supplier power. Scarce skilled installers and constrained supply of heat-pump compressors pushed prices up in 2024, with installations around 120,000 units. Centrica uses strategic partnerships and volume commitments to secure availability and mitigate volatility.

Labor and skilled contractors

Field engineers and specialist contractors are critical to Centrica’s service delivery, and tight UK labor markets in 2024 pushed contractor day-rates and technician wages higher, increasing operating costs and supplier bargaining power.

Investing in training pipelines and expanding in-house capabilities can lower dependency on external contractors; union negotiations and stringent safety standards further strengthen supplier leverage.

- c.22,000 employees (2024)

- Rising contractor rates elevate OPEX

- Training reduces supplier reliance

- Union and safety rules amplify bargaining power

Environmental and compliance costs

- Carbon price 2024: EU ETS ≈ €80–95/t

- Costs largely pass-through, limited negotiation

- PPAs vs conventional generation reduce net exposure

- Policy shifts can quickly swing supplier leverage

LNG exporters ~60%; UK networks add 25-30% to retail

Supplier power is elevated: global LNG exporters (Qatar, Australia, US) hold ~60% of export capacity and 2023–24 price volatility raised leverage. Regulated networks drive unavoidable transmission costs (~25–30% of UK retail 2024). OEM concentration and installer shortages (≈120,000 heat pumps installed 2024) push input prices; EU ETS ≈ €80–95/t in 2024.

| Metric | 2024 |

|---|---|

| LNG export share (top exporters) | ~60% |

| Network charges of UK retail | 25–30% |

| Heat pump installs (UK) | ≈120,000 |

| EU ETS price | €80–95/t |

What is included in the product

Tailored Porter's Five Forces analysis for Centrica that uncovers key competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect market share—fully editable for investor, strategy, or academic use.

A concise one-sheet Porter's Five Forces for Centrica that visualizes competitive pressure with a radar chart and customizable ratings—perfect for quick decisions, board decks, or scenario tabs without macros.

Customers Bargaining Power

High switching ease for households

Comparison sites and one-click online onboarding mean UK households can switch suppliers in minutes, driving Ofgem-recorded 2024 switch volumes of about 2.8 million and boosting price sensitivity that compresses retail margins. Service reliability and Centrica’s brand trust help retain customers despite easy churn. Bundled products like smart tariffs and energy+services reduce pure price-led switching by increasing perceived switching costs.

SME procurement sophistication

Many SMEs use brokers and fixed-term contracts, with 2024 market surveys showing over 40% of UK SMEs engaging brokers or aggregators, strengthening their negotiating stance. Aggregated buying power forces suppliers to concede margin pressure, especially at renewal windows. Delivering energy management insights and analytics creates differentiation beyond price, while flexible contract structures (e.g., mix of fixed, index-linked and advisory fees) help balance retention and profitability.

Regulatory price cap influence

The UK energy price cap, set at about £1,928/year for Oct 2023–Sep 2024 and protecting some 27 million households, anchors customer expectations on fair pricing and limits full cost pass-through during volatility, effectively increasing buyer power. Regulator-mandated transparency reduces information asymmetry. Centrica must therefore compete on service quality and add-ons within tighter capped margins.

Demand for green and smart solutions

Customers increasingly prioritize low-carbon tariffs, heat pumps, EV tariffs and smart-home integration, shifting bargaining power to buyers seeking tailored solutions; UK smart meter penetration reached about 55% in 2024 and the UK target of 600,000 heat pumps/year by 2028 underlines demand growth. Centrica can capture value via premium green bundles, financing and clear decarbonization roadmaps that raise willingness to pay.

- Demand: rising preference for low-carbon tariffs, heat pumps, EV tariffs

- Power shift: buyers seek tailored, financed solutions

- Opportunity: premium bundles + clear decarbonization roadmap

Service quality and trust as levers

Outage response, billing accuracy and call-centre performance drive retention for Centrica: British Gas serves about 8 million UK homes and Bord Gáis Energy roughly 1.2 million in Ireland, so poor experiences materially raise churn and customer bargaining power. Proactive maintenance and digital self-serve tools—which Centrica reported expanding in 2024—cut friction and complaints, improving retention and lowering acquisition costs. Reputation effects compound across both brands, amplifying the impact of service lapses.

- Outage response: fast restoration lowers churn

- Billing & call-centre accuracy: direct retention levers

- Digital self-serve & maintenance: reduce complaints, improve NPS

UK switching (~2.8m) and 55% smart meters squeeze energy retail margins

UK household switching (~2.8m in 2024) and price sensitivity compress Centrica retail margins despite brand trust and bundles that raise switching costs. SMEs (40%+ use brokers) exert negotiation pressure at renewals; analytics and flexible contracts help defend margins. Regulatory price cap (~£1,928 for Oct23–Sep24) and 55% smart meter penetration shift power toward informed buyers.

| Metric | 2024 value |

|---|---|

| Household switches | ~2.8m |

| Price cap (yr) | £1,928 |

| Smart meter penetration | ~55% |

| British Gas customers | ~8m homes |

| SMEs using brokers | >40% |

Preview the Actual Deliverable

Centrica Porter's Five Forces Analysis

This preview shows the exact Centrica Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full, professionally formatted document is ready for immediate download after purchase. Use it as-is for decision-making or presentation purposes.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Centrica operates in a tightly contested UK energy market where supplier bargaining, regulatory shifts, and rising clean-tech substitutes shape profitability; buyer power and margin pressure are central concerns. This brief highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated upstream fuel sources

Wholesale gas producers, LNG suppliers and large generators remain relatively concentrated—top exporters such as Qatar, Australia and the US account for around 60% of global LNG export capacity, giving them leverage on price and contract terms. Global commodity volatility in 2023–24, with NBP and Henry Hub swings, amplified supplier bargaining power. Centrica mitigates exposure via diversified sourcing and hedging programs and by maintaining storage and long-term contracts, which partially offset but do not eliminate spike risk.

Regulated networks as essential inputs

Transmission and distribution operators are regulated monopolies, creating unavoidable dependency for Centrica. While tariffs are regulated, access rules and service quality can affect costs and reliability; network charges were about 25–30% of UK retail electricity bills in 2024. Centrica has limited negotiation leverage, so operational planning and active advocacy with Ofgem and regional DNOs are key mitigants.

OEMs and tech vendors

OEMs and tech vendors (boilers, heat pumps, smart meters, platforms) are concentrated among a handful of major suppliers, with the top 5 firms capturing roughly 60–70% of UK device volumes in 2024, so standardization lowers switching costs and tempers supplier power. Scarce skilled installers and constrained supply of heat-pump compressors pushed prices up in 2024, with installations around 120,000 units. Centrica uses strategic partnerships and volume commitments to secure availability and mitigate volatility.

Labor and skilled contractors

Field engineers and specialist contractors are critical to Centrica’s service delivery, and tight UK labor markets in 2024 pushed contractor day-rates and technician wages higher, increasing operating costs and supplier bargaining power.

Investing in training pipelines and expanding in-house capabilities can lower dependency on external contractors; union negotiations and stringent safety standards further strengthen supplier leverage.

- c.22,000 employees (2024)

- Rising contractor rates elevate OPEX

- Training reduces supplier reliance

- Union and safety rules amplify bargaining power

Environmental and compliance costs

- Carbon price 2024: EU ETS ≈ €80–95/t

- Costs largely pass-through, limited negotiation

- PPAs vs conventional generation reduce net exposure

- Policy shifts can quickly swing supplier leverage

LNG exporters ~60%; UK networks add 25-30% to retail

Supplier power is elevated: global LNG exporters (Qatar, Australia, US) hold ~60% of export capacity and 2023–24 price volatility raised leverage. Regulated networks drive unavoidable transmission costs (~25–30% of UK retail 2024). OEM concentration and installer shortages (≈120,000 heat pumps installed 2024) push input prices; EU ETS ≈ €80–95/t in 2024.

| Metric | 2024 |

|---|---|

| LNG export share (top exporters) | ~60% |

| Network charges of UK retail | 25–30% |

| Heat pump installs (UK) | ≈120,000 |

| EU ETS price | €80–95/t |

What is included in the product

Tailored Porter's Five Forces analysis for Centrica that uncovers key competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect market share—fully editable for investor, strategy, or academic use.

A concise one-sheet Porter's Five Forces for Centrica that visualizes competitive pressure with a radar chart and customizable ratings—perfect for quick decisions, board decks, or scenario tabs without macros.

Customers Bargaining Power

High switching ease for households

Comparison sites and one-click online onboarding mean UK households can switch suppliers in minutes, driving Ofgem-recorded 2024 switch volumes of about 2.8 million and boosting price sensitivity that compresses retail margins. Service reliability and Centrica’s brand trust help retain customers despite easy churn. Bundled products like smart tariffs and energy+services reduce pure price-led switching by increasing perceived switching costs.

SME procurement sophistication

Many SMEs use brokers and fixed-term contracts, with 2024 market surveys showing over 40% of UK SMEs engaging brokers or aggregators, strengthening their negotiating stance. Aggregated buying power forces suppliers to concede margin pressure, especially at renewal windows. Delivering energy management insights and analytics creates differentiation beyond price, while flexible contract structures (e.g., mix of fixed, index-linked and advisory fees) help balance retention and profitability.

Regulatory price cap influence

The UK energy price cap, set at about £1,928/year for Oct 2023–Sep 2024 and protecting some 27 million households, anchors customer expectations on fair pricing and limits full cost pass-through during volatility, effectively increasing buyer power. Regulator-mandated transparency reduces information asymmetry. Centrica must therefore compete on service quality and add-ons within tighter capped margins.

Demand for green and smart solutions

Customers increasingly prioritize low-carbon tariffs, heat pumps, EV tariffs and smart-home integration, shifting bargaining power to buyers seeking tailored solutions; UK smart meter penetration reached about 55% in 2024 and the UK target of 600,000 heat pumps/year by 2028 underlines demand growth. Centrica can capture value via premium green bundles, financing and clear decarbonization roadmaps that raise willingness to pay.

- Demand: rising preference for low-carbon tariffs, heat pumps, EV tariffs

- Power shift: buyers seek tailored, financed solutions

- Opportunity: premium bundles + clear decarbonization roadmap

Service quality and trust as levers

Outage response, billing accuracy and call-centre performance drive retention for Centrica: British Gas serves about 8 million UK homes and Bord Gáis Energy roughly 1.2 million in Ireland, so poor experiences materially raise churn and customer bargaining power. Proactive maintenance and digital self-serve tools—which Centrica reported expanding in 2024—cut friction and complaints, improving retention and lowering acquisition costs. Reputation effects compound across both brands, amplifying the impact of service lapses.

- Outage response: fast restoration lowers churn

- Billing & call-centre accuracy: direct retention levers

- Digital self-serve & maintenance: reduce complaints, improve NPS

UK switching (~2.8m) and 55% smart meters squeeze energy retail margins

UK household switching (~2.8m in 2024) and price sensitivity compress Centrica retail margins despite brand trust and bundles that raise switching costs. SMEs (40%+ use brokers) exert negotiation pressure at renewals; analytics and flexible contracts help defend margins. Regulatory price cap (~£1,928 for Oct23–Sep24) and 55% smart meter penetration shift power toward informed buyers.

| Metric | 2024 value |

|---|---|

| Household switches | ~2.8m |

| Price cap (yr) | £1,928 |

| Smart meter penetration | ~55% |

| British Gas customers | ~8m homes |

| SMEs using brokers | >40% |

Preview the Actual Deliverable

Centrica Porter's Five Forces Analysis

This preview shows the exact Centrica Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full, professionally formatted document is ready for immediate download after purchase. Use it as-is for decision-making or presentation purposes.