Ceres Global Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

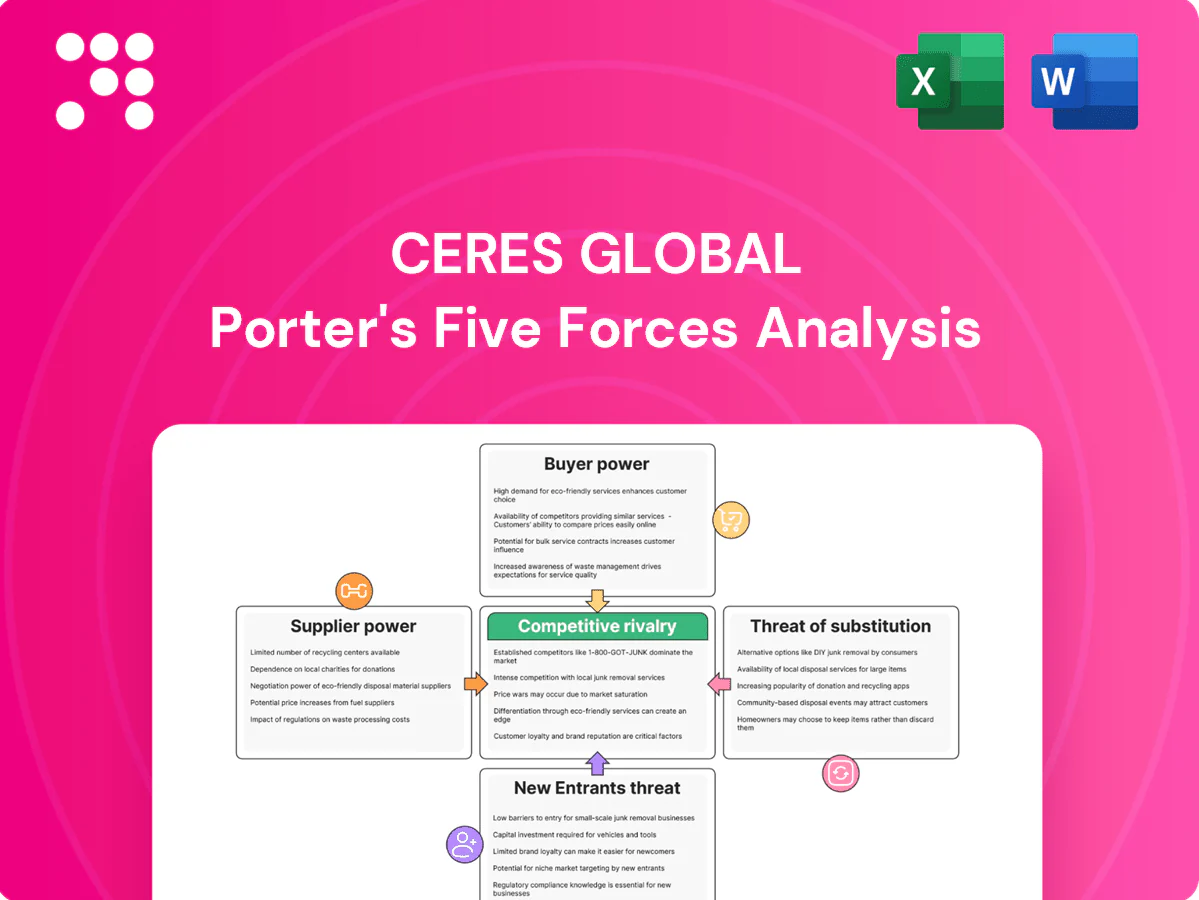

Ceres Global's Porter's Five Forces Analysis examines competitive intensity across suppliers, buyers, new entrants, substitutes and industry rivalry to reveal where margins and risks concentrate. The snapshot highlights supplier leverage from concentrated inputs and moderate buyer power amid commodity cycles. It flags barriers to entry and substitute risks that could reshape growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ceres Global’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Farmer base fragmentation

Most grain supply stems from numerous small and mid-size farmers, limiting any single grower’s leverage over price and contract terms. Aggregators and cooperatives consolidate volumes, securing stronger negotiating positions and better access to finance and logistics. Seasonal cash needs at harvest often force sellers to accept weaker terms, though tight-crop years can temporarily boost farmgate bargaining power.

Rail and barge dependence

Ceres Global terminals are highly dependent on concentrated access to seven Class I railroads and limited barge lanes, giving carriers and terminal owners pricing influence. Take-or-pay contracts and constrained railcar availability raise fixed costs and operational risk. Service reliability issues and demurrage exposure amplify that dependence. Long-term contracts mitigate some risk but switching options for shippers remain limited.

Fertilizer and seed OEMs

Global fertilizer producers and seed firms such as Nutrien, Yara and Bayer retain strong brand and channel power, allowing margin-setting on inputs Ceres distributes. 2024 export controls and lingering post-2022 energy-driven supply tightness continue to restrict volumes and elevate OEM leverage. Seasonal allocation during planting peaks further strengthens OEM pricing power. Diversified multi-sourcing and private-label programs materially reduce Ceres exposure.

Storage and handling equipment

Silo, dryer, conveyor and specialized maintenance suppliers remain concentrated as of 2024, raising switching costs; long lead times and limited spare-parts availability directly affect terminal uptime. Preventive maintenance contracts lower failure risk but create supplier dependency; equipment standardization improves negotiating leverage across vendors.

- Concentration: fewer specialized vendors

- Lead times: affect uptime/spares

- Contracts: reduce risk, raise dependency

- Standardization: increases bargaining power

Quality and grade variability

Protein, moisture and toxin levels shifted markedly in 2024 harvests across key regions (notably US Midwest and Brazil), narrowing immediately usable supply and enabling upstream holders to extract quality premiums during tight windows.

Blending reduces pressure but needs inventory flexibility; risk management lowers exposure but does not eliminate supplier power.

- 2024: localized toxin upticks raised sorting/blending costs

- Premiums: quality differentials widened during constrained weeks

- Blending requires extra working capital and storage flexibility

Moderate supplier power: rail fees 6-9% of ops; sorting/blending costs +12-18% (2024)

Supplier power is moderate: fragmented farmers limit price leverage, but 7 Class I railroads and concentrated equipment/OEM vendors amplify input and logistics pricing pressure. 2024 toxin/quality shifts raised sorting/blending costs ~12–18% in peak weeks, while take-or-pay rail fees represent ~6–9% of terminal operating costs. Long-term contracts soften volatility but keep switching costs high.

| Supplier | Concentration | 2024 impact |

|---|---|---|

| Farmers | Low | Price power minimal |

| Rail/Barge | High (7 carriers) | 6–9% op cost |

| OEMs | High | Input premium ↑12–18% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Ceres Global, highlighting competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to assess pricing pressure and strategic positioning.

Clear one-sheet summary of Ceres Global's Five Forces—customize pressure levels, view instant spider charts, and drop the clean layout straight into pitch decks or reports to simplify strategic decisions.

Customers Bargaining Power

Large industrial buyers

Large multinationals, ethanol plants, crushers and feed mills buy grain at scale and demand tight specs that compress merchant margins. They routinely dual-source across merchants, using performance, timing and freight terms as heavy negotiation levers. Long-standing supply relationships help lock volumes but do not eliminate buyer leverage, especially during spot-price swings and tight logistics windows.

Exporters and traders

Exporters and global traders arbitrage origins and destinations, driving terminal competition down to service and logistics cost rather than commodity margins. Ready access to alternative terminals reduces dependence on any single Ceres facility and elevates switching power. Transparent futures curves and deep exchange liquidity compress physical spreads and shorten holding windows. Ceres must bundle value-added logistics to retain share.

Price transparency

Real-time futures, basis data and live bids give buyers millisecond-level price comparisons, compressing decision windows and exposing even small basis movements. Digital marketplaces and e-trading portals have materially increased switching ease, driving higher churn and faster repricing. With widespread use of hedging tools, buyers now prioritize execution quality and total landed cost over nominal price. Differentiation must come from service reliability, logistics certainty and counterparty trust.

Quality and service penalties

Strict grade, timing and documentation penalties shift performance and financial risk to the merchant, tightening customer leverage; liquidated damages clauses reduce buyers need to renegotiate by making recovery automatic. Service-level agreements reward consistent providers but compress margins, making pricing competitive. Contract compliance is essential to preserve long-term customer relationships.

- Penalties shift merchant risk

- Liquidated damages cut buyer bargaining

- SLAs favor consistency, tighten pricing

- Contract compliance preserves relationships

Input distribution alternatives

Farmers can source seed and fertilizer directly from OEMs or co-ops, reducing intermediary margins; the global fertilizer market was roughly 150 billion USD in 2024, intensifying supplier-customer negotiations. Prepay and bundle programs (seed+fertilizer+advice) create lock-in and shift volume away from intermediaries. Agronomy services and on-farm financing notably reduce buyer price sensitivity, while proximity and logistics costs remain decisive.

- Direct OEM/co-op sourcing: lowers intermediary dependence

- Prepay/bundle: increases lock-in

- Agronomy+financing: lowers buyer power

- Logistics/proximity: key cost driver

Buyers, e-trading and the 150 billion USD fertilizer market squeeze intermediaries

Large buyers and global traders exert high leverage through scale, dual-sourcing and hedging, forcing margins to service and logistics. Transparent futures and e-trading shorten holding windows; buyers prioritize total landed cost. Fertilizer market ~150 billion USD in 2024 increases direct sourcing pressure on intermediaries.

| Buyer | Leverage | 2024 metric |

|---|---|---|

| Farmers/Co-ops | Medium | Fertilizer market 150B USD |

What You See Is What You Get

Ceres Global Porter's Five Forces Analysis

This preview shows the exact Ceres Global Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. It is the complete, professionally formatted document, ready for immediate download and use. The analysis covers competitive rivalry, buyer and supplier power, threats of entry and substitution. Purchase grants instant access to this same file.

A Must-Have Tool for Decision-Makers

Ceres Global's Porter's Five Forces Analysis examines competitive intensity across suppliers, buyers, new entrants, substitutes and industry rivalry to reveal where margins and risks concentrate. The snapshot highlights supplier leverage from concentrated inputs and moderate buyer power amid commodity cycles. It flags barriers to entry and substitute risks that could reshape growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ceres Global’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Farmer base fragmentation

Most grain supply stems from numerous small and mid-size farmers, limiting any single grower’s leverage over price and contract terms. Aggregators and cooperatives consolidate volumes, securing stronger negotiating positions and better access to finance and logistics. Seasonal cash needs at harvest often force sellers to accept weaker terms, though tight-crop years can temporarily boost farmgate bargaining power.

Rail and barge dependence

Ceres Global terminals are highly dependent on concentrated access to seven Class I railroads and limited barge lanes, giving carriers and terminal owners pricing influence. Take-or-pay contracts and constrained railcar availability raise fixed costs and operational risk. Service reliability issues and demurrage exposure amplify that dependence. Long-term contracts mitigate some risk but switching options for shippers remain limited.

Fertilizer and seed OEMs

Global fertilizer producers and seed firms such as Nutrien, Yara and Bayer retain strong brand and channel power, allowing margin-setting on inputs Ceres distributes. 2024 export controls and lingering post-2022 energy-driven supply tightness continue to restrict volumes and elevate OEM leverage. Seasonal allocation during planting peaks further strengthens OEM pricing power. Diversified multi-sourcing and private-label programs materially reduce Ceres exposure.

Storage and handling equipment

Silo, dryer, conveyor and specialized maintenance suppliers remain concentrated as of 2024, raising switching costs; long lead times and limited spare-parts availability directly affect terminal uptime. Preventive maintenance contracts lower failure risk but create supplier dependency; equipment standardization improves negotiating leverage across vendors.

- Concentration: fewer specialized vendors

- Lead times: affect uptime/spares

- Contracts: reduce risk, raise dependency

- Standardization: increases bargaining power

Quality and grade variability

Protein, moisture and toxin levels shifted markedly in 2024 harvests across key regions (notably US Midwest and Brazil), narrowing immediately usable supply and enabling upstream holders to extract quality premiums during tight windows.

Blending reduces pressure but needs inventory flexibility; risk management lowers exposure but does not eliminate supplier power.

- 2024: localized toxin upticks raised sorting/blending costs

- Premiums: quality differentials widened during constrained weeks

- Blending requires extra working capital and storage flexibility

Moderate supplier power: rail fees 6-9% of ops; sorting/blending costs +12-18% (2024)

Supplier power is moderate: fragmented farmers limit price leverage, but 7 Class I railroads and concentrated equipment/OEM vendors amplify input and logistics pricing pressure. 2024 toxin/quality shifts raised sorting/blending costs ~12–18% in peak weeks, while take-or-pay rail fees represent ~6–9% of terminal operating costs. Long-term contracts soften volatility but keep switching costs high.

| Supplier | Concentration | 2024 impact |

|---|---|---|

| Farmers | Low | Price power minimal |

| Rail/Barge | High (7 carriers) | 6–9% op cost |

| OEMs | High | Input premium ↑12–18% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Ceres Global, highlighting competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to assess pricing pressure and strategic positioning.

Clear one-sheet summary of Ceres Global's Five Forces—customize pressure levels, view instant spider charts, and drop the clean layout straight into pitch decks or reports to simplify strategic decisions.

Customers Bargaining Power

Large industrial buyers

Large multinationals, ethanol plants, crushers and feed mills buy grain at scale and demand tight specs that compress merchant margins. They routinely dual-source across merchants, using performance, timing and freight terms as heavy negotiation levers. Long-standing supply relationships help lock volumes but do not eliminate buyer leverage, especially during spot-price swings and tight logistics windows.

Exporters and traders

Exporters and global traders arbitrage origins and destinations, driving terminal competition down to service and logistics cost rather than commodity margins. Ready access to alternative terminals reduces dependence on any single Ceres facility and elevates switching power. Transparent futures curves and deep exchange liquidity compress physical spreads and shorten holding windows. Ceres must bundle value-added logistics to retain share.

Price transparency

Real-time futures, basis data and live bids give buyers millisecond-level price comparisons, compressing decision windows and exposing even small basis movements. Digital marketplaces and e-trading portals have materially increased switching ease, driving higher churn and faster repricing. With widespread use of hedging tools, buyers now prioritize execution quality and total landed cost over nominal price. Differentiation must come from service reliability, logistics certainty and counterparty trust.

Quality and service penalties

Strict grade, timing and documentation penalties shift performance and financial risk to the merchant, tightening customer leverage; liquidated damages clauses reduce buyers need to renegotiate by making recovery automatic. Service-level agreements reward consistent providers but compress margins, making pricing competitive. Contract compliance is essential to preserve long-term customer relationships.

- Penalties shift merchant risk

- Liquidated damages cut buyer bargaining

- SLAs favor consistency, tighten pricing

- Contract compliance preserves relationships

Input distribution alternatives

Farmers can source seed and fertilizer directly from OEMs or co-ops, reducing intermediary margins; the global fertilizer market was roughly 150 billion USD in 2024, intensifying supplier-customer negotiations. Prepay and bundle programs (seed+fertilizer+advice) create lock-in and shift volume away from intermediaries. Agronomy services and on-farm financing notably reduce buyer price sensitivity, while proximity and logistics costs remain decisive.

- Direct OEM/co-op sourcing: lowers intermediary dependence

- Prepay/bundle: increases lock-in

- Agronomy+financing: lowers buyer power

- Logistics/proximity: key cost driver

Buyers, e-trading and the 150 billion USD fertilizer market squeeze intermediaries

Large buyers and global traders exert high leverage through scale, dual-sourcing and hedging, forcing margins to service and logistics. Transparent futures and e-trading shorten holding windows; buyers prioritize total landed cost. Fertilizer market ~150 billion USD in 2024 increases direct sourcing pressure on intermediaries.

| Buyer | Leverage | 2024 metric |

|---|---|---|

| Farmers/Co-ops | Medium | Fertilizer market 150B USD |

What You See Is What You Get

Ceres Global Porter's Five Forces Analysis

This preview shows the exact Ceres Global Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. It is the complete, professionally formatted document, ready for immediate download and use. The analysis covers competitive rivalry, buyer and supplier power, threats of entry and substitution. Purchase grants instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Ceres Global's Porter's Five Forces Analysis examines competitive intensity across suppliers, buyers, new entrants, substitutes and industry rivalry to reveal where margins and risks concentrate. The snapshot highlights supplier leverage from concentrated inputs and moderate buyer power amid commodity cycles. It flags barriers to entry and substitute risks that could reshape growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ceres Global’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Farmer base fragmentation

Most grain supply stems from numerous small and mid-size farmers, limiting any single grower’s leverage over price and contract terms. Aggregators and cooperatives consolidate volumes, securing stronger negotiating positions and better access to finance and logistics. Seasonal cash needs at harvest often force sellers to accept weaker terms, though tight-crop years can temporarily boost farmgate bargaining power.

Rail and barge dependence

Ceres Global terminals are highly dependent on concentrated access to seven Class I railroads and limited barge lanes, giving carriers and terminal owners pricing influence. Take-or-pay contracts and constrained railcar availability raise fixed costs and operational risk. Service reliability issues and demurrage exposure amplify that dependence. Long-term contracts mitigate some risk but switching options for shippers remain limited.

Fertilizer and seed OEMs

Global fertilizer producers and seed firms such as Nutrien, Yara and Bayer retain strong brand and channel power, allowing margin-setting on inputs Ceres distributes. 2024 export controls and lingering post-2022 energy-driven supply tightness continue to restrict volumes and elevate OEM leverage. Seasonal allocation during planting peaks further strengthens OEM pricing power. Diversified multi-sourcing and private-label programs materially reduce Ceres exposure.

Storage and handling equipment

Silo, dryer, conveyor and specialized maintenance suppliers remain concentrated as of 2024, raising switching costs; long lead times and limited spare-parts availability directly affect terminal uptime. Preventive maintenance contracts lower failure risk but create supplier dependency; equipment standardization improves negotiating leverage across vendors.

- Concentration: fewer specialized vendors

- Lead times: affect uptime/spares

- Contracts: reduce risk, raise dependency

- Standardization: increases bargaining power

Quality and grade variability

Protein, moisture and toxin levels shifted markedly in 2024 harvests across key regions (notably US Midwest and Brazil), narrowing immediately usable supply and enabling upstream holders to extract quality premiums during tight windows.

Blending reduces pressure but needs inventory flexibility; risk management lowers exposure but does not eliminate supplier power.

- 2024: localized toxin upticks raised sorting/blending costs

- Premiums: quality differentials widened during constrained weeks

- Blending requires extra working capital and storage flexibility

Moderate supplier power: rail fees 6-9% of ops; sorting/blending costs +12-18% (2024)

Supplier power is moderate: fragmented farmers limit price leverage, but 7 Class I railroads and concentrated equipment/OEM vendors amplify input and logistics pricing pressure. 2024 toxin/quality shifts raised sorting/blending costs ~12–18% in peak weeks, while take-or-pay rail fees represent ~6–9% of terminal operating costs. Long-term contracts soften volatility but keep switching costs high.

| Supplier | Concentration | 2024 impact |

|---|---|---|

| Farmers | Low | Price power minimal |

| Rail/Barge | High (7 carriers) | 6–9% op cost |

| OEMs | High | Input premium ↑12–18% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Ceres Global, highlighting competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to assess pricing pressure and strategic positioning.

Clear one-sheet summary of Ceres Global's Five Forces—customize pressure levels, view instant spider charts, and drop the clean layout straight into pitch decks or reports to simplify strategic decisions.

Customers Bargaining Power

Large industrial buyers

Large multinationals, ethanol plants, crushers and feed mills buy grain at scale and demand tight specs that compress merchant margins. They routinely dual-source across merchants, using performance, timing and freight terms as heavy negotiation levers. Long-standing supply relationships help lock volumes but do not eliminate buyer leverage, especially during spot-price swings and tight logistics windows.

Exporters and traders

Exporters and global traders arbitrage origins and destinations, driving terminal competition down to service and logistics cost rather than commodity margins. Ready access to alternative terminals reduces dependence on any single Ceres facility and elevates switching power. Transparent futures curves and deep exchange liquidity compress physical spreads and shorten holding windows. Ceres must bundle value-added logistics to retain share.

Price transparency

Real-time futures, basis data and live bids give buyers millisecond-level price comparisons, compressing decision windows and exposing even small basis movements. Digital marketplaces and e-trading portals have materially increased switching ease, driving higher churn and faster repricing. With widespread use of hedging tools, buyers now prioritize execution quality and total landed cost over nominal price. Differentiation must come from service reliability, logistics certainty and counterparty trust.

Quality and service penalties

Strict grade, timing and documentation penalties shift performance and financial risk to the merchant, tightening customer leverage; liquidated damages clauses reduce buyers need to renegotiate by making recovery automatic. Service-level agreements reward consistent providers but compress margins, making pricing competitive. Contract compliance is essential to preserve long-term customer relationships.

- Penalties shift merchant risk

- Liquidated damages cut buyer bargaining

- SLAs favor consistency, tighten pricing

- Contract compliance preserves relationships

Input distribution alternatives

Farmers can source seed and fertilizer directly from OEMs or co-ops, reducing intermediary margins; the global fertilizer market was roughly 150 billion USD in 2024, intensifying supplier-customer negotiations. Prepay and bundle programs (seed+fertilizer+advice) create lock-in and shift volume away from intermediaries. Agronomy services and on-farm financing notably reduce buyer price sensitivity, while proximity and logistics costs remain decisive.

- Direct OEM/co-op sourcing: lowers intermediary dependence

- Prepay/bundle: increases lock-in

- Agronomy+financing: lowers buyer power

- Logistics/proximity: key cost driver

Buyers, e-trading and the 150 billion USD fertilizer market squeeze intermediaries

Large buyers and global traders exert high leverage through scale, dual-sourcing and hedging, forcing margins to service and logistics. Transparent futures and e-trading shorten holding windows; buyers prioritize total landed cost. Fertilizer market ~150 billion USD in 2024 increases direct sourcing pressure on intermediaries.

| Buyer | Leverage | 2024 metric |

|---|---|---|

| Farmers/Co-ops | Medium | Fertilizer market 150B USD |

What You See Is What You Get

Ceres Global Porter's Five Forces Analysis

This preview shows the exact Ceres Global Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. It is the complete, professionally formatted document, ready for immediate download and use. The analysis covers competitive rivalry, buyer and supplier power, threats of entry and substitution. Purchase grants instant access to this same file.