CF Industries Holdings Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

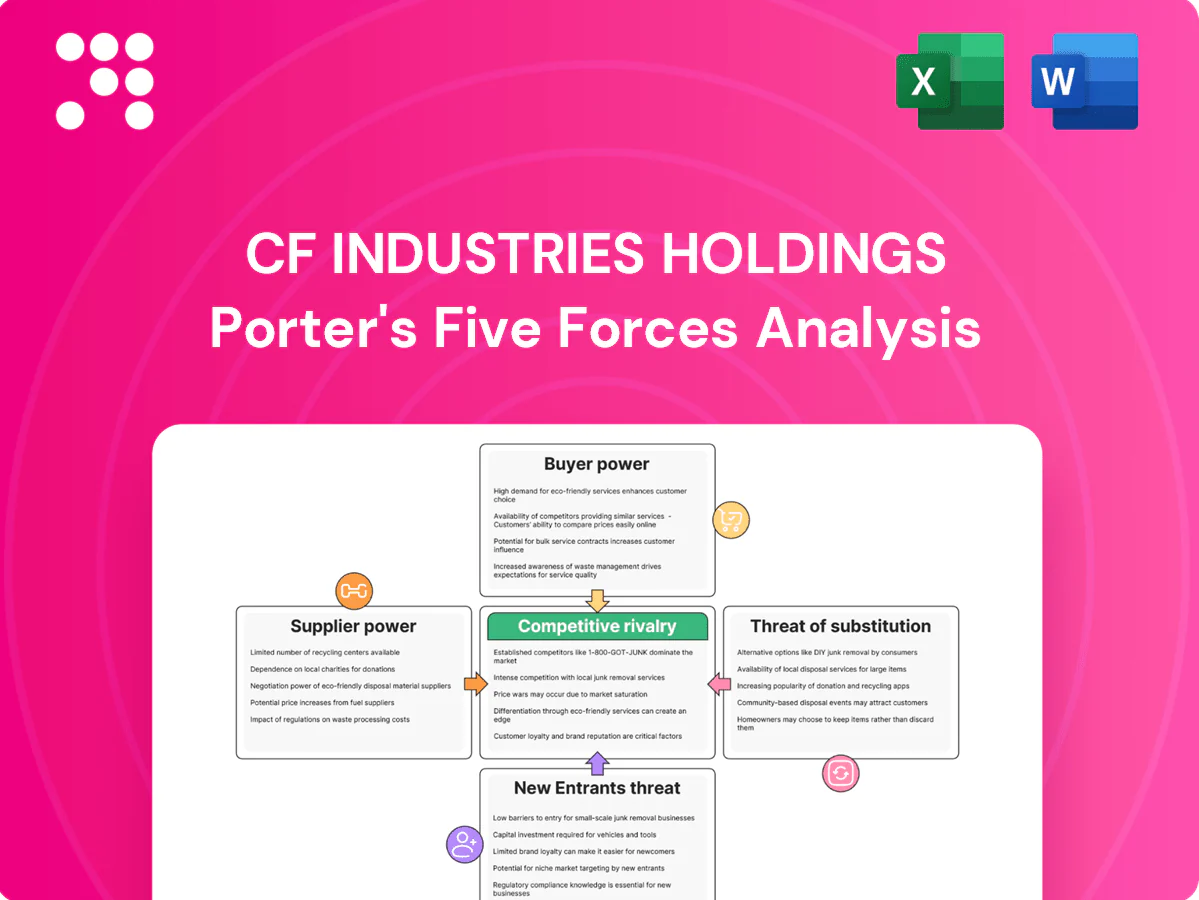

CF Industries Holdings faces balanced pressures from concentrated suppliers and variable buyer power amid shifting fertilizer demand; competitive rivalry and regulatory risks heighten strategic complexity. This snapshot teases key dynamics and tradeoffs. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Natural gas dependency

Feedstock gas is the dominant cost driver, accounting for roughly 70% of ammonia production cash cost and tying CF Industries margins to regional gas hubs. Suppliers gain leverage during price spikes or pipeline constraints—as seen in 2022–23 volatility—and hedging and multi‑sourcing mitigate but cannot eliminate exposure. 2024 Henry Hub averaged about 2.84/MMBtu, keeping feedstock risk material.

Specialized catalysts/equipment

In 2024 CF Industries faces a concentrated OEM base for catalysts, compressors and reformer parts, which limits sourcing alternatives. High switching costs and lengthy qualification tied to safety and process integrity increase supplier leverage, particularly during planned turnarounds that create short, urgent windows. Long-term contracts and vendor partnerships temper pricing power and provide procurement stability despite OEM concentration.

Logistics and storage services

Railcars, barges, terminals and ammonia tanks are scarce and highly regulated, and with a North American freight-railcar fleet of roughly 1.6 million units, tight availability can raise logistics costs and constrain shipments in peak seasons. Suppliers of leased assets therefore wield pricing and service bargaining power, pushing up spot and lease rates and creating volatility. CF Industries' partial ownership of terminals and storage helps offset this exposure by reducing reliance on third-party capacity.

Utilities and CO2 handling

Water, power and CO2 offtake/sequestration partners directly affect CF Industries continuity and decarbonization options; US industry consumes around 30% of national energy, so local utility monopolies can push input prices and terms. Limited CCS providers and pipeline access create potential bottlenecks for announced decarbonization projects, while multi-utility contracts and on-site generation/CCS reduce disruption risk.

- Water and power: local utility dominance raises input pricing risk

- CO2 handling: CCS provider and pipeline capacity may constrain timelines

- Mitigants: multi-utility arrangements and on-site projects lower supplier leverage

Geographic concentration

Plants concentrated in North America and the UK tie CF Industries to local supplier dynamics; natural gas typically represents about 70% of ammonia production cost, so regional gas disruptions, weather, maintenance or labor outages can significantly boost supplier leverage. Cross-basin gas sourcing is limited, while a diversified plant network provides some balancing capacity.

- Regional concentration: North America/UK exposure

- Input cost weight: gas ≈70% of ammonia cost

- Risk amplifiers: weather, outages, labor

- Mitigation: diversified plant footprint

Feedstock gas ~70% of cost gives suppliers pricing leverage

Feedstock gas (~70% of ammonia cash cost) and 2024 Henry Hub ~2.84/MMBtu give suppliers material leverage during price spikes; hedging/multi‑sourcing reduce but do not remove exposure. Concentrated OEMs for critical equipment and scarce leased rail/storage increase switching costs and spot rate risk. On-site assets, long‑term contracts and partial terminal ownership are key mitigants.

| Metric | 2024 |

|---|---|

| Gas share of cost | ~70% |

| Henry Hub avg | $2.84/MMBtu |

| NA railcars | ~1.6M units |

What is included in the product

Tailored Porter's Five Forces analysis of CF Industries Holdings revealing how supplier concentration, buyer power, substitutes, regulatory barriers, and industry rivalry shape pricing, margins, and strategic resilience, highlighting emerging threats, entry deterrents, and competitive levers to inform investor and management decisions.

A clear, one-sheet summary of CF Industries' five competitive forces—perfect for quick decision-making on fertilizer market positioning, regulatory impacts, and pricing power.

Customers Bargaining Power

Concentrated ag retailers/co-ops

Large distributors and co-ops such as Nutrien and CHS aggregate farmer demand and use purchasing scale to negotiate fertilizer prices with CF Industries; their national logistics and on-farm storage provide timing advantages to buy or defer supply. They can switch among producers and imports, pressuring margins. Deep buyer relationships and reliable service help them defend share despite market shifts.

Price-sensitive commodity buyers

Ammonia, urea and UAN trade on transparent spot and contract markets and remained highly volatile—urea prices fell over 60% from 2022 peaks by 2024, enabling buyers to arbitrage across products and delivery windows. Limited product differentiation constrains CF Industries' ability to capture premiums, while logistics and agronomy services (bulk shipping and application support) provide incremental value that softens price pressure.

Industrial customers’ specs

Industrial buyers in AdBlue/DEF, chemicals and power demand tight quality and reliability, making contracted volumes and penalty clauses a major source of buyer leverage. Qualification processes lower supplier churn but concentrate customer exposure on a few certified vendors. Long-term contracts and uptime SLAs elevate service levels into key bargaining chips. Penalties and volume commitments shift negotiating power toward large industrial customers.

Seasonality and timing power

Seasonal spring and fall application windows create concentrated demand spikes that in 2024 continued to shape buyers’ negotiating leverage, as agronomic timing forces purchases into narrow periods. Buyers able to pre-buy or delay shipments use that timing to extract price or payment concessions, while CF Industries’ inventory positioning and timing of ammonia and urea allocations can rebalance power. Unexpected weather disruptions in 2024 — late freezes or heavy rains — rapidly flipped leverage to holders of product able to deliver.

- Seasonal spikes: spring/fall concentrate demand

- Buyer tactics: pre-buy/delay increase leverage

- CF response: inventory timing can rebalance

- Weather risk: 2024 events quickly shifted power

Global import alternatives

In 2024 traders shifted toward low-cost regions when freight arbitrage opened, increasing coastal buyer options via expanded port access, while tariffs and duties limited some flow; CF Industries’ inland footprint and favorable rail/truck freight economics continue to protect core Midwestern markets.

- 2024: increased seaborne sourcing when freight fell

- Port access expands buyer choice

- Tariffs/duties blunt arbitrage

- Inland plants + freight economics protect core markets

Buyers dominate as urea drops >60%; inland stocks temper power

Large distributors/co-ops and industrial buyers hold strong price and contract leverage; urea prices fell >60% from 2022 peaks by 2024, enabling buyer arbitrage. Seasonal application windows and 2024 weather shocks amplified timing power, while CF’s inland footprint and inventory timing partly rebalance negotiating strength.

| Metric | 2024 |

|---|---|

| Urea price change | - >60% vs 2022 peak |

Preview the Actual Deliverable

CF Industries Holdings Porter's Five Forces Analysis

This preview shows the exact CF Industries Holdings Porter’s Five Forces Analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted analysis ready for download and use the moment you buy, covering supplier power, buyer power, rivalry, threat of substitutes, and barriers to entry. You’ll get instant access to this same file with no further setup required.

Go Beyond the Preview—Access the Full Strategic Report

CF Industries Holdings faces balanced pressures from concentrated suppliers and variable buyer power amid shifting fertilizer demand; competitive rivalry and regulatory risks heighten strategic complexity. This snapshot teases key dynamics and tradeoffs. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Natural gas dependency

Feedstock gas is the dominant cost driver, accounting for roughly 70% of ammonia production cash cost and tying CF Industries margins to regional gas hubs. Suppliers gain leverage during price spikes or pipeline constraints—as seen in 2022–23 volatility—and hedging and multi‑sourcing mitigate but cannot eliminate exposure. 2024 Henry Hub averaged about 2.84/MMBtu, keeping feedstock risk material.

Specialized catalysts/equipment

In 2024 CF Industries faces a concentrated OEM base for catalysts, compressors and reformer parts, which limits sourcing alternatives. High switching costs and lengthy qualification tied to safety and process integrity increase supplier leverage, particularly during planned turnarounds that create short, urgent windows. Long-term contracts and vendor partnerships temper pricing power and provide procurement stability despite OEM concentration.

Logistics and storage services

Railcars, barges, terminals and ammonia tanks are scarce and highly regulated, and with a North American freight-railcar fleet of roughly 1.6 million units, tight availability can raise logistics costs and constrain shipments in peak seasons. Suppliers of leased assets therefore wield pricing and service bargaining power, pushing up spot and lease rates and creating volatility. CF Industries' partial ownership of terminals and storage helps offset this exposure by reducing reliance on third-party capacity.

Utilities and CO2 handling

Water, power and CO2 offtake/sequestration partners directly affect CF Industries continuity and decarbonization options; US industry consumes around 30% of national energy, so local utility monopolies can push input prices and terms. Limited CCS providers and pipeline access create potential bottlenecks for announced decarbonization projects, while multi-utility contracts and on-site generation/CCS reduce disruption risk.

- Water and power: local utility dominance raises input pricing risk

- CO2 handling: CCS provider and pipeline capacity may constrain timelines

- Mitigants: multi-utility arrangements and on-site projects lower supplier leverage

Geographic concentration

Plants concentrated in North America and the UK tie CF Industries to local supplier dynamics; natural gas typically represents about 70% of ammonia production cost, so regional gas disruptions, weather, maintenance or labor outages can significantly boost supplier leverage. Cross-basin gas sourcing is limited, while a diversified plant network provides some balancing capacity.

- Regional concentration: North America/UK exposure

- Input cost weight: gas ≈70% of ammonia cost

- Risk amplifiers: weather, outages, labor

- Mitigation: diversified plant footprint

Feedstock gas ~70% of cost gives suppliers pricing leverage

Feedstock gas (~70% of ammonia cash cost) and 2024 Henry Hub ~2.84/MMBtu give suppliers material leverage during price spikes; hedging/multi‑sourcing reduce but do not remove exposure. Concentrated OEMs for critical equipment and scarce leased rail/storage increase switching costs and spot rate risk. On-site assets, long‑term contracts and partial terminal ownership are key mitigants.

| Metric | 2024 |

|---|---|

| Gas share of cost | ~70% |

| Henry Hub avg | $2.84/MMBtu |

| NA railcars | ~1.6M units |

What is included in the product

Tailored Porter's Five Forces analysis of CF Industries Holdings revealing how supplier concentration, buyer power, substitutes, regulatory barriers, and industry rivalry shape pricing, margins, and strategic resilience, highlighting emerging threats, entry deterrents, and competitive levers to inform investor and management decisions.

A clear, one-sheet summary of CF Industries' five competitive forces—perfect for quick decision-making on fertilizer market positioning, regulatory impacts, and pricing power.

Customers Bargaining Power

Concentrated ag retailers/co-ops

Large distributors and co-ops such as Nutrien and CHS aggregate farmer demand and use purchasing scale to negotiate fertilizer prices with CF Industries; their national logistics and on-farm storage provide timing advantages to buy or defer supply. They can switch among producers and imports, pressuring margins. Deep buyer relationships and reliable service help them defend share despite market shifts.

Price-sensitive commodity buyers

Ammonia, urea and UAN trade on transparent spot and contract markets and remained highly volatile—urea prices fell over 60% from 2022 peaks by 2024, enabling buyers to arbitrage across products and delivery windows. Limited product differentiation constrains CF Industries' ability to capture premiums, while logistics and agronomy services (bulk shipping and application support) provide incremental value that softens price pressure.

Industrial customers’ specs

Industrial buyers in AdBlue/DEF, chemicals and power demand tight quality and reliability, making contracted volumes and penalty clauses a major source of buyer leverage. Qualification processes lower supplier churn but concentrate customer exposure on a few certified vendors. Long-term contracts and uptime SLAs elevate service levels into key bargaining chips. Penalties and volume commitments shift negotiating power toward large industrial customers.

Seasonality and timing power

Seasonal spring and fall application windows create concentrated demand spikes that in 2024 continued to shape buyers’ negotiating leverage, as agronomic timing forces purchases into narrow periods. Buyers able to pre-buy or delay shipments use that timing to extract price or payment concessions, while CF Industries’ inventory positioning and timing of ammonia and urea allocations can rebalance power. Unexpected weather disruptions in 2024 — late freezes or heavy rains — rapidly flipped leverage to holders of product able to deliver.

- Seasonal spikes: spring/fall concentrate demand

- Buyer tactics: pre-buy/delay increase leverage

- CF response: inventory timing can rebalance

- Weather risk: 2024 events quickly shifted power

Global import alternatives

In 2024 traders shifted toward low-cost regions when freight arbitrage opened, increasing coastal buyer options via expanded port access, while tariffs and duties limited some flow; CF Industries’ inland footprint and favorable rail/truck freight economics continue to protect core Midwestern markets.

- 2024: increased seaborne sourcing when freight fell

- Port access expands buyer choice

- Tariffs/duties blunt arbitrage

- Inland plants + freight economics protect core markets

Buyers dominate as urea drops >60%; inland stocks temper power

Large distributors/co-ops and industrial buyers hold strong price and contract leverage; urea prices fell >60% from 2022 peaks by 2024, enabling buyer arbitrage. Seasonal application windows and 2024 weather shocks amplified timing power, while CF’s inland footprint and inventory timing partly rebalance negotiating strength.

| Metric | 2024 |

|---|---|

| Urea price change | - >60% vs 2022 peak |

Preview the Actual Deliverable

CF Industries Holdings Porter's Five Forces Analysis

This preview shows the exact CF Industries Holdings Porter’s Five Forces Analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted analysis ready for download and use the moment you buy, covering supplier power, buyer power, rivalry, threat of substitutes, and barriers to entry. You’ll get instant access to this same file with no further setup required.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

CF Industries Holdings faces balanced pressures from concentrated suppliers and variable buyer power amid shifting fertilizer demand; competitive rivalry and regulatory risks heighten strategic complexity. This snapshot teases key dynamics and tradeoffs. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Natural gas dependency

Feedstock gas is the dominant cost driver, accounting for roughly 70% of ammonia production cash cost and tying CF Industries margins to regional gas hubs. Suppliers gain leverage during price spikes or pipeline constraints—as seen in 2022–23 volatility—and hedging and multi‑sourcing mitigate but cannot eliminate exposure. 2024 Henry Hub averaged about 2.84/MMBtu, keeping feedstock risk material.

Specialized catalysts/equipment

In 2024 CF Industries faces a concentrated OEM base for catalysts, compressors and reformer parts, which limits sourcing alternatives. High switching costs and lengthy qualification tied to safety and process integrity increase supplier leverage, particularly during planned turnarounds that create short, urgent windows. Long-term contracts and vendor partnerships temper pricing power and provide procurement stability despite OEM concentration.

Logistics and storage services

Railcars, barges, terminals and ammonia tanks are scarce and highly regulated, and with a North American freight-railcar fleet of roughly 1.6 million units, tight availability can raise logistics costs and constrain shipments in peak seasons. Suppliers of leased assets therefore wield pricing and service bargaining power, pushing up spot and lease rates and creating volatility. CF Industries' partial ownership of terminals and storage helps offset this exposure by reducing reliance on third-party capacity.

Utilities and CO2 handling

Water, power and CO2 offtake/sequestration partners directly affect CF Industries continuity and decarbonization options; US industry consumes around 30% of national energy, so local utility monopolies can push input prices and terms. Limited CCS providers and pipeline access create potential bottlenecks for announced decarbonization projects, while multi-utility contracts and on-site generation/CCS reduce disruption risk.

- Water and power: local utility dominance raises input pricing risk

- CO2 handling: CCS provider and pipeline capacity may constrain timelines

- Mitigants: multi-utility arrangements and on-site projects lower supplier leverage

Geographic concentration

Plants concentrated in North America and the UK tie CF Industries to local supplier dynamics; natural gas typically represents about 70% of ammonia production cost, so regional gas disruptions, weather, maintenance or labor outages can significantly boost supplier leverage. Cross-basin gas sourcing is limited, while a diversified plant network provides some balancing capacity.

- Regional concentration: North America/UK exposure

- Input cost weight: gas ≈70% of ammonia cost

- Risk amplifiers: weather, outages, labor

- Mitigation: diversified plant footprint

Feedstock gas ~70% of cost gives suppliers pricing leverage

Feedstock gas (~70% of ammonia cash cost) and 2024 Henry Hub ~2.84/MMBtu give suppliers material leverage during price spikes; hedging/multi‑sourcing reduce but do not remove exposure. Concentrated OEMs for critical equipment and scarce leased rail/storage increase switching costs and spot rate risk. On-site assets, long‑term contracts and partial terminal ownership are key mitigants.

| Metric | 2024 |

|---|---|

| Gas share of cost | ~70% |

| Henry Hub avg | $2.84/MMBtu |

| NA railcars | ~1.6M units |

What is included in the product

Tailored Porter's Five Forces analysis of CF Industries Holdings revealing how supplier concentration, buyer power, substitutes, regulatory barriers, and industry rivalry shape pricing, margins, and strategic resilience, highlighting emerging threats, entry deterrents, and competitive levers to inform investor and management decisions.

A clear, one-sheet summary of CF Industries' five competitive forces—perfect for quick decision-making on fertilizer market positioning, regulatory impacts, and pricing power.

Customers Bargaining Power

Concentrated ag retailers/co-ops

Large distributors and co-ops such as Nutrien and CHS aggregate farmer demand and use purchasing scale to negotiate fertilizer prices with CF Industries; their national logistics and on-farm storage provide timing advantages to buy or defer supply. They can switch among producers and imports, pressuring margins. Deep buyer relationships and reliable service help them defend share despite market shifts.

Price-sensitive commodity buyers

Ammonia, urea and UAN trade on transparent spot and contract markets and remained highly volatile—urea prices fell over 60% from 2022 peaks by 2024, enabling buyers to arbitrage across products and delivery windows. Limited product differentiation constrains CF Industries' ability to capture premiums, while logistics and agronomy services (bulk shipping and application support) provide incremental value that softens price pressure.

Industrial customers’ specs

Industrial buyers in AdBlue/DEF, chemicals and power demand tight quality and reliability, making contracted volumes and penalty clauses a major source of buyer leverage. Qualification processes lower supplier churn but concentrate customer exposure on a few certified vendors. Long-term contracts and uptime SLAs elevate service levels into key bargaining chips. Penalties and volume commitments shift negotiating power toward large industrial customers.

Seasonality and timing power

Seasonal spring and fall application windows create concentrated demand spikes that in 2024 continued to shape buyers’ negotiating leverage, as agronomic timing forces purchases into narrow periods. Buyers able to pre-buy or delay shipments use that timing to extract price or payment concessions, while CF Industries’ inventory positioning and timing of ammonia and urea allocations can rebalance power. Unexpected weather disruptions in 2024 — late freezes or heavy rains — rapidly flipped leverage to holders of product able to deliver.

- Seasonal spikes: spring/fall concentrate demand

- Buyer tactics: pre-buy/delay increase leverage

- CF response: inventory timing can rebalance

- Weather risk: 2024 events quickly shifted power

Global import alternatives

In 2024 traders shifted toward low-cost regions when freight arbitrage opened, increasing coastal buyer options via expanded port access, while tariffs and duties limited some flow; CF Industries’ inland footprint and favorable rail/truck freight economics continue to protect core Midwestern markets.

- 2024: increased seaborne sourcing when freight fell

- Port access expands buyer choice

- Tariffs/duties blunt arbitrage

- Inland plants + freight economics protect core markets

Buyers dominate as urea drops >60%; inland stocks temper power

Large distributors/co-ops and industrial buyers hold strong price and contract leverage; urea prices fell >60% from 2022 peaks by 2024, enabling buyer arbitrage. Seasonal application windows and 2024 weather shocks amplified timing power, while CF’s inland footprint and inventory timing partly rebalance negotiating strength.

| Metric | 2024 |

|---|---|

| Urea price change | - >60% vs 2022 peak |

Preview the Actual Deliverable

CF Industries Holdings Porter's Five Forces Analysis

This preview shows the exact CF Industries Holdings Porter’s Five Forces Analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted analysis ready for download and use the moment you buy, covering supplier power, buyer power, rivalry, threat of substitutes, and barriers to entry. You’ll get instant access to this same file with no further setup required.