Chandra Asri Petrochemical Boston Consulting Group Matrix

Unlock Strategic Clarity

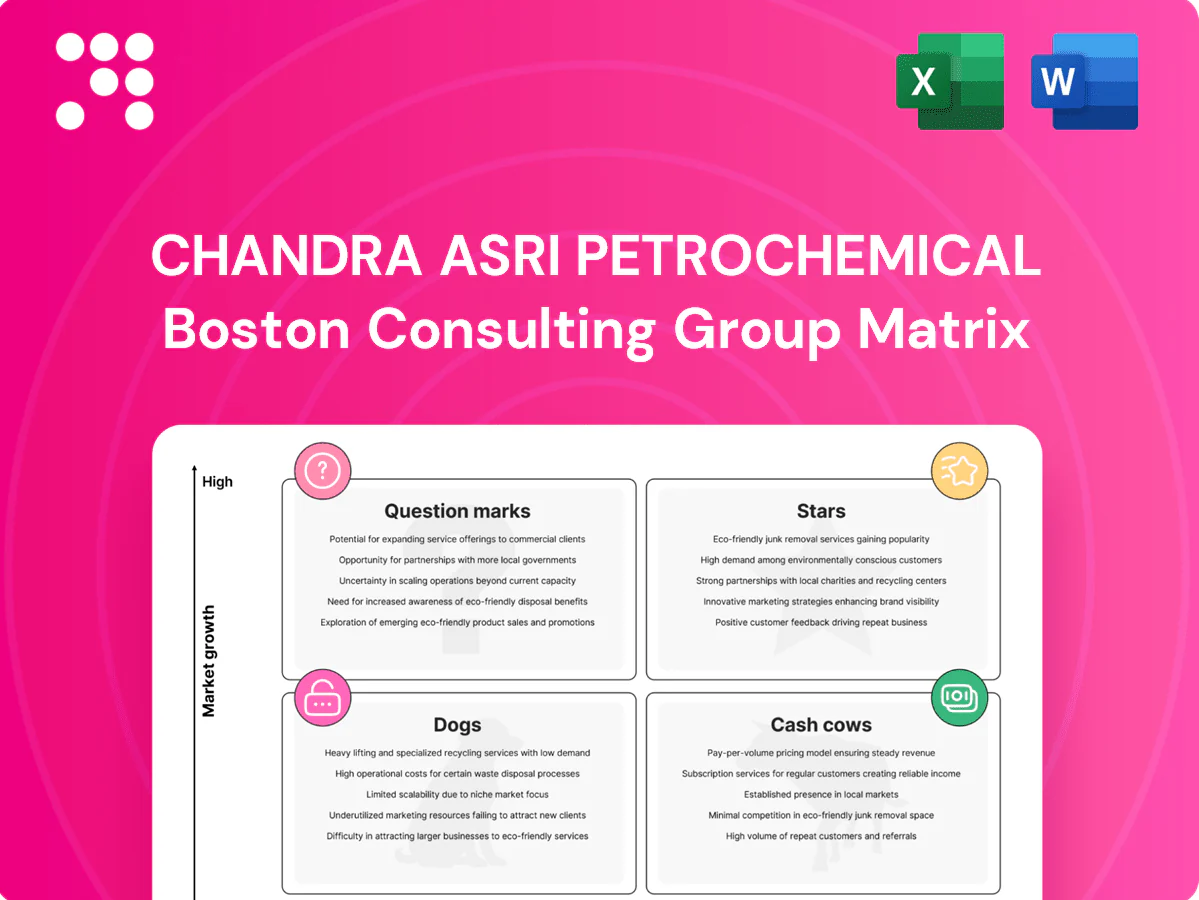

Curious how Chandra Asri’s product lines stack up in growth and market share? This snapshot teases the Stars, Cash Cows, Dogs and Question Marks—grab the full BCG Matrix to see exact quadrant placements, data-driven recommendations, and where to deploy capital next. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary that saves you hours and supports smarter, faster strategic decisions.

Stars

Olefins cracker leadership

High share in Indonesia’s rising demand for ethylene and propylene positions Chandra Asri’s olefins crackers as a Star, leading the domestic value chain. The asset requires continued heavy spending on debottlenecking, reliability and product placement, so cash-in is matched by cash-out as growth absorbs investment. Maintain share now; when domestic demand growth cools it will transition into a Cash Cow.

Polypropylene growth engine

Polypropylene growth engine: Packaging, FMCG and automotive kept PP volumes climbing in 2024, supporting Chandra Asri’s roughly 800 ktpa PP capacity and securing a strong local share. Promotions with converters and faster grade availability remain decisive to lock contracts. The unit generates significant cash while reinvestment stays high to meet demand. Sustained leadership can mature the unit into a Cash Cow.

Polyethylene momentum

HDPE/LLDPE demand for films and pipes in Indonesia reached about 4.0 Mt in 2024 with CAGR ~5% since 2020; Chandra Asri holds an estimated ~35% domestic PE market share, but placement and logistics investments remain critical to displace imports. Margin volatility persisted (EBITDA margin swinging near mid-teens in 2024), yet strong volume growth justifies targeted funding. Tight capacity management will transition the segment toward Cash Cow status as utilization climbs.

Domestic substitution push

As Indonesia's largest integrated petrochemical producer, Chandra Asri leads domestic PE/PVC supply in 2024, plugging fast-growing import substitution where CAP already dominates. Winning specs and delivery windows requires sustained commercial spend and logistics investment. The flywheel needs cash today to secure lower unit costs and long-term margin advantage; defending share hard compounds payoffs over time.

- market-position: CAP dominant in domestic PE/PVC (2024)

- investment-need: ongoing commercial & logistics spend

- strategy: short-term cash to build long-term margin flywheel

- outcome: defended share compounds payoff

Butadiene tie-ins

Butadiene tie-ins at Chandra Asri are Stars: 2024 industry trends show steady upswing in tyre and elastomer demand with CAP positioned as a key local node, capturing growth pocket leadership; customer development and QA investments raise costs while cash burn funds capacity ramp; held market share should convert to a Cow as growth normalizes.

- Tag: growth

- Tag: CAP node

- Tag: investment-intensive

- Tag: future Cow

Olefins crackers tighten supply as ethylene/propylene demand rises ~5% CAGR

Chandra Asri’s olefins crackers are Stars: domestic ethylene/propylene demand up ~5% CAGR to 2024, driving high utilization but requiring heavy debottlenecking capex.

PP (≈800 ktpa) is a Star with 2024 volume growth from packaging/FMCG; convertor promotions and grade rollout need sustained spend.

PE (HDPE/LLDPE) demand ~4.0 Mt in 2024; CAP ~35% share; EBITDA margins swung near mid-teens in 2024.

| Metric | 2024 |

|---|---|

| PP capacity | ≈800 ktpa |

| PE demand | ≈4.0 Mt |

| CAP PE share | ≈35% |

| EBITDA margin | mid-teens |

What is included in the product

BCG Matrix review of Chandra Asri’s products: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page BCG Matrix placing Chandra Asri units in quadrants for instant portfolio clarity and faster strategic decisions

Cash Cows

Styrene monomer base

Styrene monomer base benefits from mature ABS/PS demand that keeps offtake and pricing within predictable corridors in 2024, supporting steady margin realization for Chandra Asri. High domestic penetration and efficient plant runs convert this stream into consistent surplus cash with minimal promotional spend. Focus remains on uptime and cost control, allowing generated cash to fund risk-on investments elsewhere in the portfolio.

Commodity PE grades

Commodity PE grades (film and blow-molding) are cash cows for Chandra Asri, supplying steady volumes in a mature 2024 market with predictable margins. Scale and plant learning curves keep unit costs low versus smaller regional players. Growth is minimal and placement spend is low. Continued focus on energy efficiency and logistics optimization can incrementally boost yield and EBITDA.

Raffinate/MTBE by-product stream

Raffinate/MTBE by-product streams sell into established fuel and chemical pools with predictable demand, generating steady margins while requiring light incremental capex; cash outlays are largely routine maintenance. These quiet earners provide reliable free cash flow that can underwrite expansion capex and support balance-sheet stability. Operational consistency reduces volatility versus core olefins.

Long-term domestic contracts

Long-term domestic contracts secure locked-in volumes with local converters, smoothing utilization and protecting margins for Chandra Asri in 2024; growth is limited but capex and selling costs remain low. Risk exposure is reduced by stable offtake agreements, and cash conversion stays strong when plants run steady, so focus on reliability and let it print.

- Locked volumes: stable utilization

- Low growth, low selling cost

- Reduced market risk

- Strong cash conversion when plants steady

Utilities and site integration

Utilities and site integration at Chandra Asri (Indonesia’s largest petrochemical, ticker TPIA) centralize feed, power and logistics, materially lowering opex and lifting EBITDA margins; the unglamorous utility unit functions as a cash cow funding efficiency upgrades rather than growth.

- Integrated feed/power reduces variable cost per ton

- Spending prioritizes reliability and efficiency upgrades

- Stable cash generation supports dividends and deleveraging

Styrene, PE, raffinate and utilities: steady cash funds expansion and deleveraging

Styrene, commodity PE, raffinate/MTBE and utilities acted as cash cows for Chandra Asri in 2024, delivering predictable volumes, low selling costs and strong cash conversion while funding expansion and deleveraging. Long-term domestic contracts and site integration kept utilization high and unit opex low, preserving EBITDA generation for reinvestment and payouts.

| Stream | 2024 Utilization | Role |

|---|---|---|

| Styrene | ~88% | Stable margins |

| PE commodity | ~90% | High cash flow |

| Raffinate/MTBE | ~85% | By-product cash |

| Utilities | Consolidated | Opex cut |

Delivered as Shown

Chandra Asri Petrochemical BCG Matrix

The Chandra Asri Petrochemical BCG Matrix you're previewing is the exact same file you'll receive after purchase — no watermarks, no placeholders. It's a fully formatted, analysis-ready report tailored to the company’s market positioning and product portfolio. Buy once and download immediately; it’s editable, printable, and presentation-ready. What you see is what you get—clear, strategic, and ready to use.

Unlock Strategic Clarity

Curious how Chandra Asri’s product lines stack up in growth and market share? This snapshot teases the Stars, Cash Cows, Dogs and Question Marks—grab the full BCG Matrix to see exact quadrant placements, data-driven recommendations, and where to deploy capital next. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary that saves you hours and supports smarter, faster strategic decisions.

Stars

Olefins cracker leadership

High share in Indonesia’s rising demand for ethylene and propylene positions Chandra Asri’s olefins crackers as a Star, leading the domestic value chain. The asset requires continued heavy spending on debottlenecking, reliability and product placement, so cash-in is matched by cash-out as growth absorbs investment. Maintain share now; when domestic demand growth cools it will transition into a Cash Cow.

Polypropylene growth engine

Polypropylene growth engine: Packaging, FMCG and automotive kept PP volumes climbing in 2024, supporting Chandra Asri’s roughly 800 ktpa PP capacity and securing a strong local share. Promotions with converters and faster grade availability remain decisive to lock contracts. The unit generates significant cash while reinvestment stays high to meet demand. Sustained leadership can mature the unit into a Cash Cow.

Polyethylene momentum

HDPE/LLDPE demand for films and pipes in Indonesia reached about 4.0 Mt in 2024 with CAGR ~5% since 2020; Chandra Asri holds an estimated ~35% domestic PE market share, but placement and logistics investments remain critical to displace imports. Margin volatility persisted (EBITDA margin swinging near mid-teens in 2024), yet strong volume growth justifies targeted funding. Tight capacity management will transition the segment toward Cash Cow status as utilization climbs.

Domestic substitution push

As Indonesia's largest integrated petrochemical producer, Chandra Asri leads domestic PE/PVC supply in 2024, plugging fast-growing import substitution where CAP already dominates. Winning specs and delivery windows requires sustained commercial spend and logistics investment. The flywheel needs cash today to secure lower unit costs and long-term margin advantage; defending share hard compounds payoffs over time.

- market-position: CAP dominant in domestic PE/PVC (2024)

- investment-need: ongoing commercial & logistics spend

- strategy: short-term cash to build long-term margin flywheel

- outcome: defended share compounds payoff

Butadiene tie-ins

Butadiene tie-ins at Chandra Asri are Stars: 2024 industry trends show steady upswing in tyre and elastomer demand with CAP positioned as a key local node, capturing growth pocket leadership; customer development and QA investments raise costs while cash burn funds capacity ramp; held market share should convert to a Cow as growth normalizes.

- Tag: growth

- Tag: CAP node

- Tag: investment-intensive

- Tag: future Cow

Olefins crackers tighten supply as ethylene/propylene demand rises ~5% CAGR

Chandra Asri’s olefins crackers are Stars: domestic ethylene/propylene demand up ~5% CAGR to 2024, driving high utilization but requiring heavy debottlenecking capex.

PP (≈800 ktpa) is a Star with 2024 volume growth from packaging/FMCG; convertor promotions and grade rollout need sustained spend.

PE (HDPE/LLDPE) demand ~4.0 Mt in 2024; CAP ~35% share; EBITDA margins swung near mid-teens in 2024.

| Metric | 2024 |

|---|---|

| PP capacity | ≈800 ktpa |

| PE demand | ≈4.0 Mt |

| CAP PE share | ≈35% |

| EBITDA margin | mid-teens |

What is included in the product

BCG Matrix review of Chandra Asri’s products: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page BCG Matrix placing Chandra Asri units in quadrants for instant portfolio clarity and faster strategic decisions

Cash Cows

Styrene monomer base

Styrene monomer base benefits from mature ABS/PS demand that keeps offtake and pricing within predictable corridors in 2024, supporting steady margin realization for Chandra Asri. High domestic penetration and efficient plant runs convert this stream into consistent surplus cash with minimal promotional spend. Focus remains on uptime and cost control, allowing generated cash to fund risk-on investments elsewhere in the portfolio.

Commodity PE grades

Commodity PE grades (film and blow-molding) are cash cows for Chandra Asri, supplying steady volumes in a mature 2024 market with predictable margins. Scale and plant learning curves keep unit costs low versus smaller regional players. Growth is minimal and placement spend is low. Continued focus on energy efficiency and logistics optimization can incrementally boost yield and EBITDA.

Raffinate/MTBE by-product stream

Raffinate/MTBE by-product streams sell into established fuel and chemical pools with predictable demand, generating steady margins while requiring light incremental capex; cash outlays are largely routine maintenance. These quiet earners provide reliable free cash flow that can underwrite expansion capex and support balance-sheet stability. Operational consistency reduces volatility versus core olefins.

Long-term domestic contracts

Long-term domestic contracts secure locked-in volumes with local converters, smoothing utilization and protecting margins for Chandra Asri in 2024; growth is limited but capex and selling costs remain low. Risk exposure is reduced by stable offtake agreements, and cash conversion stays strong when plants run steady, so focus on reliability and let it print.

- Locked volumes: stable utilization

- Low growth, low selling cost

- Reduced market risk

- Strong cash conversion when plants steady

Utilities and site integration

Utilities and site integration at Chandra Asri (Indonesia’s largest petrochemical, ticker TPIA) centralize feed, power and logistics, materially lowering opex and lifting EBITDA margins; the unglamorous utility unit functions as a cash cow funding efficiency upgrades rather than growth.

- Integrated feed/power reduces variable cost per ton

- Spending prioritizes reliability and efficiency upgrades

- Stable cash generation supports dividends and deleveraging

Styrene, PE, raffinate and utilities: steady cash funds expansion and deleveraging

Styrene, commodity PE, raffinate/MTBE and utilities acted as cash cows for Chandra Asri in 2024, delivering predictable volumes, low selling costs and strong cash conversion while funding expansion and deleveraging. Long-term domestic contracts and site integration kept utilization high and unit opex low, preserving EBITDA generation for reinvestment and payouts.

| Stream | 2024 Utilization | Role |

|---|---|---|

| Styrene | ~88% | Stable margins |

| PE commodity | ~90% | High cash flow |

| Raffinate/MTBE | ~85% | By-product cash |

| Utilities | Consolidated | Opex cut |

Delivered as Shown

Chandra Asri Petrochemical BCG Matrix

The Chandra Asri Petrochemical BCG Matrix you're previewing is the exact same file you'll receive after purchase — no watermarks, no placeholders. It's a fully formatted, analysis-ready report tailored to the company’s market positioning and product portfolio. Buy once and download immediately; it’s editable, printable, and presentation-ready. What you see is what you get—clear, strategic, and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Unlock Strategic Clarity

Curious how Chandra Asri’s product lines stack up in growth and market share? This snapshot teases the Stars, Cash Cows, Dogs and Question Marks—grab the full BCG Matrix to see exact quadrant placements, data-driven recommendations, and where to deploy capital next. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary that saves you hours and supports smarter, faster strategic decisions.

Stars

Olefins cracker leadership

High share in Indonesia’s rising demand for ethylene and propylene positions Chandra Asri’s olefins crackers as a Star, leading the domestic value chain. The asset requires continued heavy spending on debottlenecking, reliability and product placement, so cash-in is matched by cash-out as growth absorbs investment. Maintain share now; when domestic demand growth cools it will transition into a Cash Cow.

Polypropylene growth engine

Polypropylene growth engine: Packaging, FMCG and automotive kept PP volumes climbing in 2024, supporting Chandra Asri’s roughly 800 ktpa PP capacity and securing a strong local share. Promotions with converters and faster grade availability remain decisive to lock contracts. The unit generates significant cash while reinvestment stays high to meet demand. Sustained leadership can mature the unit into a Cash Cow.

Polyethylene momentum

HDPE/LLDPE demand for films and pipes in Indonesia reached about 4.0 Mt in 2024 with CAGR ~5% since 2020; Chandra Asri holds an estimated ~35% domestic PE market share, but placement and logistics investments remain critical to displace imports. Margin volatility persisted (EBITDA margin swinging near mid-teens in 2024), yet strong volume growth justifies targeted funding. Tight capacity management will transition the segment toward Cash Cow status as utilization climbs.

Domestic substitution push

As Indonesia's largest integrated petrochemical producer, Chandra Asri leads domestic PE/PVC supply in 2024, plugging fast-growing import substitution where CAP already dominates. Winning specs and delivery windows requires sustained commercial spend and logistics investment. The flywheel needs cash today to secure lower unit costs and long-term margin advantage; defending share hard compounds payoffs over time.

- market-position: CAP dominant in domestic PE/PVC (2024)

- investment-need: ongoing commercial & logistics spend

- strategy: short-term cash to build long-term margin flywheel

- outcome: defended share compounds payoff

Butadiene tie-ins

Butadiene tie-ins at Chandra Asri are Stars: 2024 industry trends show steady upswing in tyre and elastomer demand with CAP positioned as a key local node, capturing growth pocket leadership; customer development and QA investments raise costs while cash burn funds capacity ramp; held market share should convert to a Cow as growth normalizes.

- Tag: growth

- Tag: CAP node

- Tag: investment-intensive

- Tag: future Cow

Olefins crackers tighten supply as ethylene/propylene demand rises ~5% CAGR

Chandra Asri’s olefins crackers are Stars: domestic ethylene/propylene demand up ~5% CAGR to 2024, driving high utilization but requiring heavy debottlenecking capex.

PP (≈800 ktpa) is a Star with 2024 volume growth from packaging/FMCG; convertor promotions and grade rollout need sustained spend.

PE (HDPE/LLDPE) demand ~4.0 Mt in 2024; CAP ~35% share; EBITDA margins swung near mid-teens in 2024.

| Metric | 2024 |

|---|---|

| PP capacity | ≈800 ktpa |

| PE demand | ≈4.0 Mt |

| CAP PE share | ≈35% |

| EBITDA margin | mid-teens |

What is included in the product

BCG Matrix review of Chandra Asri’s products: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page BCG Matrix placing Chandra Asri units in quadrants for instant portfolio clarity and faster strategic decisions

Cash Cows

Styrene monomer base

Styrene monomer base benefits from mature ABS/PS demand that keeps offtake and pricing within predictable corridors in 2024, supporting steady margin realization for Chandra Asri. High domestic penetration and efficient plant runs convert this stream into consistent surplus cash with minimal promotional spend. Focus remains on uptime and cost control, allowing generated cash to fund risk-on investments elsewhere in the portfolio.

Commodity PE grades

Commodity PE grades (film and blow-molding) are cash cows for Chandra Asri, supplying steady volumes in a mature 2024 market with predictable margins. Scale and plant learning curves keep unit costs low versus smaller regional players. Growth is minimal and placement spend is low. Continued focus on energy efficiency and logistics optimization can incrementally boost yield and EBITDA.

Raffinate/MTBE by-product stream

Raffinate/MTBE by-product streams sell into established fuel and chemical pools with predictable demand, generating steady margins while requiring light incremental capex; cash outlays are largely routine maintenance. These quiet earners provide reliable free cash flow that can underwrite expansion capex and support balance-sheet stability. Operational consistency reduces volatility versus core olefins.

Long-term domestic contracts

Long-term domestic contracts secure locked-in volumes with local converters, smoothing utilization and protecting margins for Chandra Asri in 2024; growth is limited but capex and selling costs remain low. Risk exposure is reduced by stable offtake agreements, and cash conversion stays strong when plants run steady, so focus on reliability and let it print.

- Locked volumes: stable utilization

- Low growth, low selling cost

- Reduced market risk

- Strong cash conversion when plants steady

Utilities and site integration

Utilities and site integration at Chandra Asri (Indonesia’s largest petrochemical, ticker TPIA) centralize feed, power and logistics, materially lowering opex and lifting EBITDA margins; the unglamorous utility unit functions as a cash cow funding efficiency upgrades rather than growth.

- Integrated feed/power reduces variable cost per ton

- Spending prioritizes reliability and efficiency upgrades

- Stable cash generation supports dividends and deleveraging

Styrene, PE, raffinate and utilities: steady cash funds expansion and deleveraging

Styrene, commodity PE, raffinate/MTBE and utilities acted as cash cows for Chandra Asri in 2024, delivering predictable volumes, low selling costs and strong cash conversion while funding expansion and deleveraging. Long-term domestic contracts and site integration kept utilization high and unit opex low, preserving EBITDA generation for reinvestment and payouts.

| Stream | 2024 Utilization | Role |

|---|---|---|

| Styrene | ~88% | Stable margins |

| PE commodity | ~90% | High cash flow |

| Raffinate/MTBE | ~85% | By-product cash |

| Utilities | Consolidated | Opex cut |

Delivered as Shown

Chandra Asri Petrochemical BCG Matrix

The Chandra Asri Petrochemical BCG Matrix you're previewing is the exact same file you'll receive after purchase — no watermarks, no placeholders. It's a fully formatted, analysis-ready report tailored to the company’s market positioning and product portfolio. Buy once and download immediately; it’s editable, printable, and presentation-ready. What you see is what you get—clear, strategic, and ready to use.