Chevalier Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

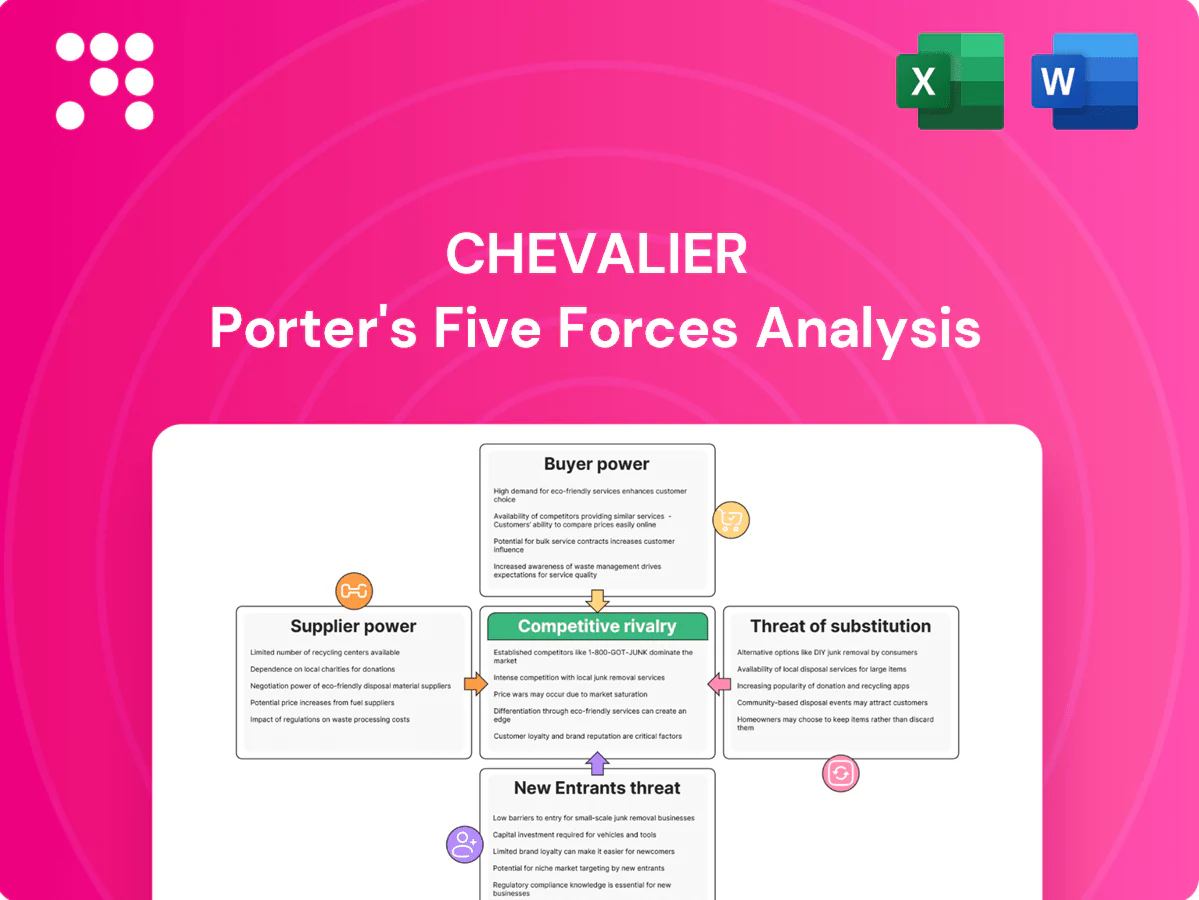

Chevalier’s Five Forces snapshot outlines competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory pressures shaping profitability. This brief preview highlights key pressure points and strategic implications. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Chevalier.

Suppliers Bargaining Power

Diverse input base tempers leverage

As of 2024 Chevalier sources materials, tech and services across construction, property, IT, healthcare and distribution, diluting any single supplier’s power and enabling cross-portfolio procurement synergies. Specialized inputs such as HVAC systems, medical devices and niche IT stacks still elevate vendor influence and can create single points of failure. Long-term framework contracts and dual-sourcing mitigate these risks and preserve negotiating leverage.

Commodity volatility in construction

Steel, cement, copper and fuel price swings—up to ~30% in 2024—can shift bargaining power to upstream producers, especially as Mainland China (≈55% of global steel output) or Southeast Asia supply disruptions tighten markets. Large contractors hedge and aggregate demand to secure discounts and volume terms, while index-linked contracts and pass-through clauses partially pass costs to clients; Brent averaged about $86/bbl in 2024.

Regulated healthcare and IT vendor lock-in

Healthcare equipment and certified software entail high switching and compliance costs, especially given regulations covering roughly 6,100 US hospitals (AHA 2024). OEM parts, proprietary service agreements and non‑interoperable data standards drive strong vendor lock‑in and pricing power for select suppliers. Chevalier can blunt this by prioritizing open‑architecture preferences and lifecycle total‑cost bidding in procurement.

Land and subcontractor concentration

Access to land banks via government tenders and a small set of major holders concentrates supplier power in Hong Kong and Tier‑1 Chinese cities; scarcity of specialized trades pushes subcontractor leverage during construction peaks, though relationship capital and prequalified panels lower exposure and enable smoothing of cycle timing and workloads.

- Concentrated land access

- Specialized trade scarcity at peaks

- Prequalified panels mitigate risk

- Workload smoothing reduces volatility

FX and logistics dependence

Regional operations rely heavily on cross-border logistics and imported components, and 2024 freight-rate volatility (spot swings reported up to 20% on some Asia–Europe lanes) and FX moves can quickly shift bargaining power toward carriers and forwarders. Strategic forwarding partnerships and 30–90 day inventory buffers materially reduce this vulnerability. Investing in digital supply-chain visibility platforms improved negotiating leverage in 2024 by shortening transit-cost blind spots.

- High dependence on imports increases supplier leverage

- FX and freight spikes (up to ~20% in 2024) boost logistics power

- Forwarding partnerships + inventory buffers = lowered exposure

- Real-time visibility = stronger negotiation position

Moderate supplier power; steel, freight & FX swings increase risk - contracts limit exposure

Supplier power is moderate: diversified sourcing across construction, property, IT and healthcare reduces single-vendor risk, but specialized equipment, land concentration and inputs (steel/cement swings ~30% in 2024; China ≈55% steel output) create localized leverage; freight/FX volatility (spot swings up to ~20% in 2024) and proprietary healthcare software raise switching costs. Long-term contracts, dual‑sourcing and digital visibility cut exposure.

| Metric | 2024 Figure |

|---|---|

| Brent oil | $86/bbl |

| Freight spot swings | ~20% |

| Steel output (China) | ≈55% |

What is included in the product

Tailored Five Forces assessment for Chevalier that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform pricing, positioning and defense.

A concise Chevalier Porter's Five Forces one-sheet that translates complex competitive dynamics into actionable insights for faster decisions. Customize force levels, swap data or labels, and drop the clean chart straight into decks or dashboards.

Customers Bargaining Power

Institutional and government clients

Institutional and government clients—public agencies and large developers—hold strong negotiating clout; World Bank estimates public procurement equals about 15% of GDP in many countries (2024), concentrating buying power. Tendering and benchmark-driven pricing push contractor margins into single digits, while performance bonds, SLAs and penalties further raise buyer leverage. Differentiation via safety, ESG and on-time delivery reduces pressure.

Property tenants and investors

Commercial tenants compare landlords on rent, amenities and location, and in 2024 many major office markets recorded vacancy rates above 10%, increasing tenant bargaining power. In cyclical downturns landlords offer concessions and fit-out incentives, boosting leverage for tenants and often compressing effective rents. Institutional investors in 2024 focused on yield and occupancy, pressuring asset managers; value-add upgrades and flexible leases remain primary defenses to preserve pricing.

IT and healthcare end-users

Enterprise IT buyers run competitive RFPs focused on interoperability and total cost, with over 60% of large firms using formal procurement cycles in 2024; hospitals and clinics demand regulatory compliance, 24/7 uptime and rapid service SLA responses, citing uptime as a top buying criterion. Switching barriers differ by stack, reducing price pressure where deep integration exists, while outcome-based contracts—now used by a growing share of health systems—can realign incentives toward performance.

Distribution channel customers

Retailers and B2B distributors (top 5 typically control ~60% of channel sales) push terms via shelf space and volume commitments; private labels represent ~20% of global FMCG sales and reach ~40% in some EU markets, increasing buyer leverage. Chevalier can deploy exclusive SKUs, demand-generation support and sustain 98%+ fill rates; data-sharing can cut stockouts ~30% and returns 10–15% to improve joint planning.

- Shelf/volume leverage: top-5 ~60%

- Private labels: ~20% global, up to ~40% EU

- Defense: exclusive SKUs, marketing support, 98%+ fill rates

- Data-sharing impact: −30% stockouts, −10–15% returns

Cross-portfolio bundling potential

Diversification enables cross-portfolio bundles (e.g., build-operate-manage) that shrink visible buyer alternatives and simplify price comparisons; 2024 surveys report 47% of enterprise buyers prefer integrated service bundles. Bundle-led stickiness reduces buyer power over time as switching costs rise. Procurement silos can block these benefits, but case-based ROI proof points (often >15% cost reduction) accelerate adoption.

- Bundling reduces alternatives

- 47% enterprise preference in 2024

- Stickiness raises switching costs

- Procurement silos block gains

- ROI cases (>15% savings) drive adoption

Buyers wield leverage: procurement ~15% GDP, top retailers 60% — bundles & ESG restore margin

Buyers wield high leverage: public procurement ~15% of GDP (2024) and top-5 retailers ~60% channel share, pushing margins and demanding SLAs, penalties and concessions. Differentiation (ESG, safety, uptime) and bundle offerings (47% enterprise prefer bundles in 2024) raise switching costs and blunt price pressure. Data-sharing and exclusive SKUs reduce stockouts (~30%) and returns (10–15%), restoring margin.

| Buyer type | Metric | 2024 stat |

|---|---|---|

| Public procurement | Share of GDP | ~15% |

| Top retailers | Channel share | ~60% |

| Enterprise buyers | Prefer bundles | 47% |

Same Document Delivered

Chevalier Porter's Five Forces Analysis

This preview is the Chevalier Porter's Five Forces Analysis and contains the exact, fully formatted document you’ll receive immediately after purchase. It includes comprehensive assessment of industry rivalry, supplier and buyer power, threats of entry and substitutes. No placeholders or samples—what you see is ready to download and use.

Go Beyond the Preview—Access the Full Strategic Report

Chevalier’s Five Forces snapshot outlines competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory pressures shaping profitability. This brief preview highlights key pressure points and strategic implications. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Chevalier.

Suppliers Bargaining Power

Diverse input base tempers leverage

As of 2024 Chevalier sources materials, tech and services across construction, property, IT, healthcare and distribution, diluting any single supplier’s power and enabling cross-portfolio procurement synergies. Specialized inputs such as HVAC systems, medical devices and niche IT stacks still elevate vendor influence and can create single points of failure. Long-term framework contracts and dual-sourcing mitigate these risks and preserve negotiating leverage.

Commodity volatility in construction

Steel, cement, copper and fuel price swings—up to ~30% in 2024—can shift bargaining power to upstream producers, especially as Mainland China (≈55% of global steel output) or Southeast Asia supply disruptions tighten markets. Large contractors hedge and aggregate demand to secure discounts and volume terms, while index-linked contracts and pass-through clauses partially pass costs to clients; Brent averaged about $86/bbl in 2024.

Regulated healthcare and IT vendor lock-in

Healthcare equipment and certified software entail high switching and compliance costs, especially given regulations covering roughly 6,100 US hospitals (AHA 2024). OEM parts, proprietary service agreements and non‑interoperable data standards drive strong vendor lock‑in and pricing power for select suppliers. Chevalier can blunt this by prioritizing open‑architecture preferences and lifecycle total‑cost bidding in procurement.

Land and subcontractor concentration

Access to land banks via government tenders and a small set of major holders concentrates supplier power in Hong Kong and Tier‑1 Chinese cities; scarcity of specialized trades pushes subcontractor leverage during construction peaks, though relationship capital and prequalified panels lower exposure and enable smoothing of cycle timing and workloads.

- Concentrated land access

- Specialized trade scarcity at peaks

- Prequalified panels mitigate risk

- Workload smoothing reduces volatility

FX and logistics dependence

Regional operations rely heavily on cross-border logistics and imported components, and 2024 freight-rate volatility (spot swings reported up to 20% on some Asia–Europe lanes) and FX moves can quickly shift bargaining power toward carriers and forwarders. Strategic forwarding partnerships and 30–90 day inventory buffers materially reduce this vulnerability. Investing in digital supply-chain visibility platforms improved negotiating leverage in 2024 by shortening transit-cost blind spots.

- High dependence on imports increases supplier leverage

- FX and freight spikes (up to ~20% in 2024) boost logistics power

- Forwarding partnerships + inventory buffers = lowered exposure

- Real-time visibility = stronger negotiation position

Moderate supplier power; steel, freight & FX swings increase risk - contracts limit exposure

Supplier power is moderate: diversified sourcing across construction, property, IT and healthcare reduces single-vendor risk, but specialized equipment, land concentration and inputs (steel/cement swings ~30% in 2024; China ≈55% steel output) create localized leverage; freight/FX volatility (spot swings up to ~20% in 2024) and proprietary healthcare software raise switching costs. Long-term contracts, dual‑sourcing and digital visibility cut exposure.

| Metric | 2024 Figure |

|---|---|

| Brent oil | $86/bbl |

| Freight spot swings | ~20% |

| Steel output (China) | ≈55% |

What is included in the product

Tailored Five Forces assessment for Chevalier that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform pricing, positioning and defense.

A concise Chevalier Porter's Five Forces one-sheet that translates complex competitive dynamics into actionable insights for faster decisions. Customize force levels, swap data or labels, and drop the clean chart straight into decks or dashboards.

Customers Bargaining Power

Institutional and government clients

Institutional and government clients—public agencies and large developers—hold strong negotiating clout; World Bank estimates public procurement equals about 15% of GDP in many countries (2024), concentrating buying power. Tendering and benchmark-driven pricing push contractor margins into single digits, while performance bonds, SLAs and penalties further raise buyer leverage. Differentiation via safety, ESG and on-time delivery reduces pressure.

Property tenants and investors

Commercial tenants compare landlords on rent, amenities and location, and in 2024 many major office markets recorded vacancy rates above 10%, increasing tenant bargaining power. In cyclical downturns landlords offer concessions and fit-out incentives, boosting leverage for tenants and often compressing effective rents. Institutional investors in 2024 focused on yield and occupancy, pressuring asset managers; value-add upgrades and flexible leases remain primary defenses to preserve pricing.

IT and healthcare end-users

Enterprise IT buyers run competitive RFPs focused on interoperability and total cost, with over 60% of large firms using formal procurement cycles in 2024; hospitals and clinics demand regulatory compliance, 24/7 uptime and rapid service SLA responses, citing uptime as a top buying criterion. Switching barriers differ by stack, reducing price pressure where deep integration exists, while outcome-based contracts—now used by a growing share of health systems—can realign incentives toward performance.

Distribution channel customers

Retailers and B2B distributors (top 5 typically control ~60% of channel sales) push terms via shelf space and volume commitments; private labels represent ~20% of global FMCG sales and reach ~40% in some EU markets, increasing buyer leverage. Chevalier can deploy exclusive SKUs, demand-generation support and sustain 98%+ fill rates; data-sharing can cut stockouts ~30% and returns 10–15% to improve joint planning.

- Shelf/volume leverage: top-5 ~60%

- Private labels: ~20% global, up to ~40% EU

- Defense: exclusive SKUs, marketing support, 98%+ fill rates

- Data-sharing impact: −30% stockouts, −10–15% returns

Cross-portfolio bundling potential

Diversification enables cross-portfolio bundles (e.g., build-operate-manage) that shrink visible buyer alternatives and simplify price comparisons; 2024 surveys report 47% of enterprise buyers prefer integrated service bundles. Bundle-led stickiness reduces buyer power over time as switching costs rise. Procurement silos can block these benefits, but case-based ROI proof points (often >15% cost reduction) accelerate adoption.

- Bundling reduces alternatives

- 47% enterprise preference in 2024

- Stickiness raises switching costs

- Procurement silos block gains

- ROI cases (>15% savings) drive adoption

Buyers wield leverage: procurement ~15% GDP, top retailers 60% — bundles & ESG restore margin

Buyers wield high leverage: public procurement ~15% of GDP (2024) and top-5 retailers ~60% channel share, pushing margins and demanding SLAs, penalties and concessions. Differentiation (ESG, safety, uptime) and bundle offerings (47% enterprise prefer bundles in 2024) raise switching costs and blunt price pressure. Data-sharing and exclusive SKUs reduce stockouts (~30%) and returns (10–15%), restoring margin.

| Buyer type | Metric | 2024 stat |

|---|---|---|

| Public procurement | Share of GDP | ~15% |

| Top retailers | Channel share | ~60% |

| Enterprise buyers | Prefer bundles | 47% |

Same Document Delivered

Chevalier Porter's Five Forces Analysis

This preview is the Chevalier Porter's Five Forces Analysis and contains the exact, fully formatted document you’ll receive immediately after purchase. It includes comprehensive assessment of industry rivalry, supplier and buyer power, threats of entry and substitutes. No placeholders or samples—what you see is ready to download and use.

Description

Go Beyond the Preview—Access the Full Strategic Report

Chevalier’s Five Forces snapshot outlines competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory pressures shaping profitability. This brief preview highlights key pressure points and strategic implications. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Chevalier.

Suppliers Bargaining Power

Diverse input base tempers leverage

As of 2024 Chevalier sources materials, tech and services across construction, property, IT, healthcare and distribution, diluting any single supplier’s power and enabling cross-portfolio procurement synergies. Specialized inputs such as HVAC systems, medical devices and niche IT stacks still elevate vendor influence and can create single points of failure. Long-term framework contracts and dual-sourcing mitigate these risks and preserve negotiating leverage.

Commodity volatility in construction

Steel, cement, copper and fuel price swings—up to ~30% in 2024—can shift bargaining power to upstream producers, especially as Mainland China (≈55% of global steel output) or Southeast Asia supply disruptions tighten markets. Large contractors hedge and aggregate demand to secure discounts and volume terms, while index-linked contracts and pass-through clauses partially pass costs to clients; Brent averaged about $86/bbl in 2024.

Regulated healthcare and IT vendor lock-in

Healthcare equipment and certified software entail high switching and compliance costs, especially given regulations covering roughly 6,100 US hospitals (AHA 2024). OEM parts, proprietary service agreements and non‑interoperable data standards drive strong vendor lock‑in and pricing power for select suppliers. Chevalier can blunt this by prioritizing open‑architecture preferences and lifecycle total‑cost bidding in procurement.

Land and subcontractor concentration

Access to land banks via government tenders and a small set of major holders concentrates supplier power in Hong Kong and Tier‑1 Chinese cities; scarcity of specialized trades pushes subcontractor leverage during construction peaks, though relationship capital and prequalified panels lower exposure and enable smoothing of cycle timing and workloads.

- Concentrated land access

- Specialized trade scarcity at peaks

- Prequalified panels mitigate risk

- Workload smoothing reduces volatility

FX and logistics dependence

Regional operations rely heavily on cross-border logistics and imported components, and 2024 freight-rate volatility (spot swings reported up to 20% on some Asia–Europe lanes) and FX moves can quickly shift bargaining power toward carriers and forwarders. Strategic forwarding partnerships and 30–90 day inventory buffers materially reduce this vulnerability. Investing in digital supply-chain visibility platforms improved negotiating leverage in 2024 by shortening transit-cost blind spots.

- High dependence on imports increases supplier leverage

- FX and freight spikes (up to ~20% in 2024) boost logistics power

- Forwarding partnerships + inventory buffers = lowered exposure

- Real-time visibility = stronger negotiation position

Moderate supplier power; steel, freight & FX swings increase risk - contracts limit exposure

Supplier power is moderate: diversified sourcing across construction, property, IT and healthcare reduces single-vendor risk, but specialized equipment, land concentration and inputs (steel/cement swings ~30% in 2024; China ≈55% steel output) create localized leverage; freight/FX volatility (spot swings up to ~20% in 2024) and proprietary healthcare software raise switching costs. Long-term contracts, dual‑sourcing and digital visibility cut exposure.

| Metric | 2024 Figure |

|---|---|

| Brent oil | $86/bbl |

| Freight spot swings | ~20% |

| Steel output (China) | ≈55% |

What is included in the product

Tailored Five Forces assessment for Chevalier that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform pricing, positioning and defense.

A concise Chevalier Porter's Five Forces one-sheet that translates complex competitive dynamics into actionable insights for faster decisions. Customize force levels, swap data or labels, and drop the clean chart straight into decks or dashboards.

Customers Bargaining Power

Institutional and government clients

Institutional and government clients—public agencies and large developers—hold strong negotiating clout; World Bank estimates public procurement equals about 15% of GDP in many countries (2024), concentrating buying power. Tendering and benchmark-driven pricing push contractor margins into single digits, while performance bonds, SLAs and penalties further raise buyer leverage. Differentiation via safety, ESG and on-time delivery reduces pressure.

Property tenants and investors

Commercial tenants compare landlords on rent, amenities and location, and in 2024 many major office markets recorded vacancy rates above 10%, increasing tenant bargaining power. In cyclical downturns landlords offer concessions and fit-out incentives, boosting leverage for tenants and often compressing effective rents. Institutional investors in 2024 focused on yield and occupancy, pressuring asset managers; value-add upgrades and flexible leases remain primary defenses to preserve pricing.

IT and healthcare end-users

Enterprise IT buyers run competitive RFPs focused on interoperability and total cost, with over 60% of large firms using formal procurement cycles in 2024; hospitals and clinics demand regulatory compliance, 24/7 uptime and rapid service SLA responses, citing uptime as a top buying criterion. Switching barriers differ by stack, reducing price pressure where deep integration exists, while outcome-based contracts—now used by a growing share of health systems—can realign incentives toward performance.

Distribution channel customers

Retailers and B2B distributors (top 5 typically control ~60% of channel sales) push terms via shelf space and volume commitments; private labels represent ~20% of global FMCG sales and reach ~40% in some EU markets, increasing buyer leverage. Chevalier can deploy exclusive SKUs, demand-generation support and sustain 98%+ fill rates; data-sharing can cut stockouts ~30% and returns 10–15% to improve joint planning.

- Shelf/volume leverage: top-5 ~60%

- Private labels: ~20% global, up to ~40% EU

- Defense: exclusive SKUs, marketing support, 98%+ fill rates

- Data-sharing impact: −30% stockouts, −10–15% returns

Cross-portfolio bundling potential

Diversification enables cross-portfolio bundles (e.g., build-operate-manage) that shrink visible buyer alternatives and simplify price comparisons; 2024 surveys report 47% of enterprise buyers prefer integrated service bundles. Bundle-led stickiness reduces buyer power over time as switching costs rise. Procurement silos can block these benefits, but case-based ROI proof points (often >15% cost reduction) accelerate adoption.

- Bundling reduces alternatives

- 47% enterprise preference in 2024

- Stickiness raises switching costs

- Procurement silos block gains

- ROI cases (>15% savings) drive adoption

Buyers wield leverage: procurement ~15% GDP, top retailers 60% — bundles & ESG restore margin

Buyers wield high leverage: public procurement ~15% of GDP (2024) and top-5 retailers ~60% channel share, pushing margins and demanding SLAs, penalties and concessions. Differentiation (ESG, safety, uptime) and bundle offerings (47% enterprise prefer bundles in 2024) raise switching costs and blunt price pressure. Data-sharing and exclusive SKUs reduce stockouts (~30%) and returns (10–15%), restoring margin.

| Buyer type | Metric | 2024 stat |

|---|---|---|

| Public procurement | Share of GDP | ~15% |

| Top retailers | Channel share | ~60% |

| Enterprise buyers | Prefer bundles | 47% |

Same Document Delivered

Chevalier Porter's Five Forces Analysis

This preview is the Chevalier Porter's Five Forces Analysis and contains the exact, fully formatted document you’ll receive immediately after purchase. It includes comprehensive assessment of industry rivalry, supplier and buyer power, threats of entry and substitutes. No placeholders or samples—what you see is ready to download and use.