Datang International Power Porter's Five Forces Analysis

Don't Miss the Bigger Picture

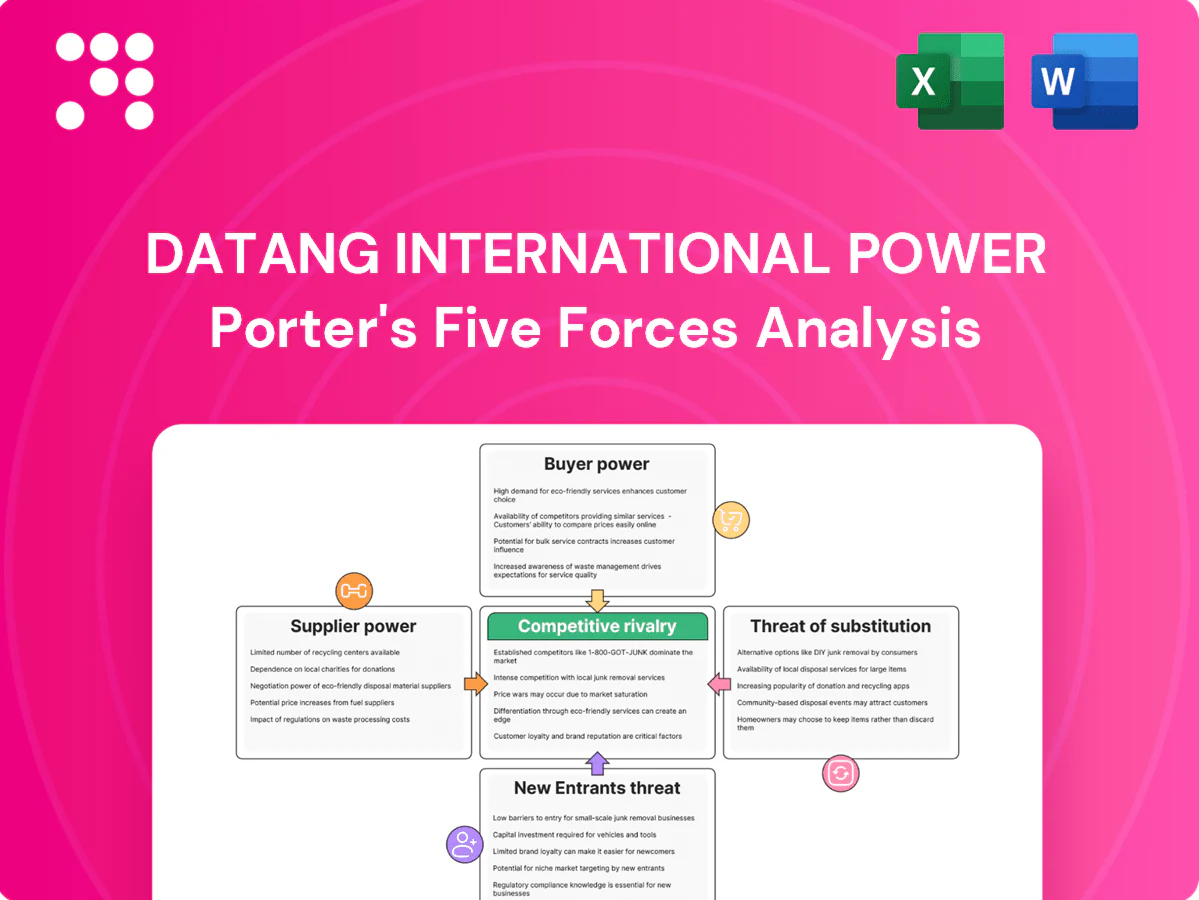

Datang International Power’s Porter’s Five Forces snapshot highlights supplier and buyer leverage, rivalry intensity, threats from entrants and substitutes within China’s power sector. Regulatory shifts, fuel mix and capacity overhang shape competitive pressure and margins. This brief only scratches the surface. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Vertical integration tempers coal leverage

Datang’s ownership stakes in coal mines give it a stronger bargaining position on price and volumes, and in 2024 those upstream assets helped cushion the group against recent coal-price volatility and supply shocks. Partial vertical integration lowers exposure to spot-market spikes, yet Datang still purchases substantial external tonnage. Persistent rail-logistics bottlenecks and port capacity limits in 2024 can reintroduce leverage for transport providers, constraining procurement flexibility.

Equipment and O&M concentration

Major turbine, boiler and balance-of-plant supply in China is concentrated among Harbin Electric, Dongfang Electric and Shanghai Electric, giving suppliers measurable pricing and delivery leverage for Datang International Power. China's thermal fleet exceeds 1,000 GW, with typical asset lives of 25–40 years and proprietary spare parts creating switching costs and long-term O&M dependence. Localization and multi-vendor frameworks have raised in-country sourcing and spare-part availability, but advanced retrofit projects and digital control upgrades in 2024 keep supplier power elevated for specialized scopes.

Renewables OEM pricing tailwinds

PV module and onshore wind-turbine pricing softened in 2024, with module spot prices down roughly 15–20% year-on-year to about $0.18–0.20/W and turbine OEM prices easing ~5–10%, reducing supplier leverage.

Global module capacity overhang of ~15–25% improved buyer terms and lead times, but high-efficiency cells (TOPCon/IBC) and large offshore turbines command 10–30% premiums, while grid-connection gear and battery cells still face periodic cyclic tightness.

Fuel logistics and quality constraints

Railway allocations, port slots and coal quality specs give logistics providers leverage over Datang; port slot utilization often exceeds 85% in peak months and winter freight surcharges rose ~20% in 2024, tightening negotiating power. Seasonal demand and weather disruptions can cut throughput sharply; long-term contracts and coordinated planning reduce this exposure. Hydro inflow variability in 2024 shifted fuel mixes, changing supplier dynamics.

- High slot utilization: >85% peak (2024)

- Freight surcharges: ~+20% (2024 winter)

- Long-term contracts mitigate shortages

- Hydro variability altered coal demand in 2024

Capital and financing providers

Large-scale generation for Datang depends heavily on state-owned banks and capital markets; in 2024 Chinese state-owned banks held roughly two-thirds of domestic banking assets, allowing lenders to influence terms via interest rates and covenants. Policy-aligned financing in 2024 remained tilted toward renewables and retrofits, improving access and pricing, while tighter green taxonomies have constrained coal lending and raised its effective cost. Balance sheet strength therefore materially shapes bargaining outcomes.

Integration cuts coal risk; ports at 85%+ strain, bank tilt lifts funding

Datang's partial vertical integration and coal-mine ownership reduced exposure to 2024 spot coal volatility, but external purchases remain material and logistics (port slots >85% peak) and OEMs (Harbin/Dongfang/Shanghai) retain pricing power for specialized equipment. State banks (~66% assets) and green finance tilt raise coal funding costs.

| Metric | 2024 |

|---|---|

| Port utilization (peak) | >85% |

| Winter freight surcharge | +~20% |

| Module spot price | $0.18–0.20/W |

| State banks share | ~66% |

What is included in the product

Tailored Porter’s Five Forces analysis for Datang International Power, assessing competitive rivalry, supplier and buyer power, substitutes, and entry barriers to identify strategic risks, pricing pressures, and opportunities for defensive positioning.

A concise one-sheet Porter's Five Forces for Datang International Power—translates complex sector pressures into a clear, editable radar chart and summary so teams can quickly spot threats and opportunities and drop it into decks or dashboards without macros.

Customers Bargaining Power

Grid companies as dominant buyers

State Grid (serving roughly 1.1 billion people) and China Southern Grid (serving about 240 million) are Datang’s primary off-takers, creating a highly concentrated buyer base; their scale gives strong leverage over dispatch, settlement and grid connection timelines. Regulatory tariff frameworks and provincial mandates in 2024 limit pure price bargaining, while plant compliance and reliability metrics directly affect acceptance and curtailment risk.

Market trading and direct supply growth

Expanding spot markets and direct supply in 2024 increased price sensitivity, as spot trades in pilot regions rose materially, pushing large industrial buyers to secure bilateral contracts and exploit peak/off-peak arbitrage. Major industrial users gained bargaining leverage through long-term and flexible bilateral deals. Datang must offer competitive tariffs and modular products. A diversified generation and trading portfolio enables tailored offers and effective hedging.

Tariff and policy mediation

Regulated tariffs and capacity payments set price bands that cap buyer power against Datang International, with China’s market reforms and capacity mechanisms stabilizing merchant exposure; solar and wind capacity in China surpassed roughly 800 GW by 2024, shifting system price dynamics. Policy incentives and priority dispatch for renewables increase demand for green attributes, while guarantee hours for contracted assets reduce buyer leverage over baseload contracts. Verification processes and renewable energy certificates (RECs) add negotiation layers and create separate value streams that buyers must factor into procurement and pricing discussions.

Quality, reliability, and ancillary services

Buyers value grid stability, fast ramping, and ancillary services which distinguish suppliers beyond price; in China in 2024 thermal plants still supplied over 50% of electricity, so coal/hydro flexibility can command premiums in capacity-constrained regions.

Demonstrated reliability cuts imbalance penalties and raises contract-renewal odds, while underperformance shifts leverage to buyers and spot-market exposure.

- Ancillary services: differentiation beyond price

- Coal/hydro flexibility: premium in constrained markets

- Reliability: fewer penalties, higher renewal probability

- Underperformance: increases buyer bargaining power

Curtailment and interconnection terms

In regions with grid congestion curtailment gives buyers effective volume control, and in 2024 China-wide renewable curtailment eased to mid-single digits, reducing but not eliminating buyer leverage; connection queue priority and metering rules directly affect realized revenues and settlement timing for Datang International Power, while proactive grid coordination and dispatch agreements cut exposure and delays.

- Curtailment risk: mid-single-digit rate (2024)

- Queue/metering: affects settlement timing and revenue

- Mitigation: grid coordination lowers leverage

- Diversification: lowers localized curtailment exposure

Buyer concentration caps dispatch; renewables>800 GW drive flexible demand

Concentrated buyers (State Grid ~1.1bn, China Southern ~240m) exert strong non-price leverage over dispatch and connection; regulated tariffs and capacity payments in 2024 cap pure price pressure. Renewables >800 GW and thermal still >50% of supply shift price dynamics; curtailment eased to mid-single-digit rates in 2024, reducing but not removing buyer volume control. Spot market growth and large industrial bilateral deals raise price sensitivity and demand for flexible products.

| Metric | 2024 |

|---|---|

| State Grid customers | ~1.1 bn |

| China Southern customers | ~240 m |

| Renewable capacity | >800 GW |

| Renewable curtailment | mid-single-digit % |

| Thermal share | >50% |

Same Document Delivered

Datang International Power Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Datang International Power you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable; instant access is granted upon payment.

Don't Miss the Bigger Picture

Datang International Power’s Porter’s Five Forces snapshot highlights supplier and buyer leverage, rivalry intensity, threats from entrants and substitutes within China’s power sector. Regulatory shifts, fuel mix and capacity overhang shape competitive pressure and margins. This brief only scratches the surface. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Vertical integration tempers coal leverage

Datang’s ownership stakes in coal mines give it a stronger bargaining position on price and volumes, and in 2024 those upstream assets helped cushion the group against recent coal-price volatility and supply shocks. Partial vertical integration lowers exposure to spot-market spikes, yet Datang still purchases substantial external tonnage. Persistent rail-logistics bottlenecks and port capacity limits in 2024 can reintroduce leverage for transport providers, constraining procurement flexibility.

Equipment and O&M concentration

Major turbine, boiler and balance-of-plant supply in China is concentrated among Harbin Electric, Dongfang Electric and Shanghai Electric, giving suppliers measurable pricing and delivery leverage for Datang International Power. China's thermal fleet exceeds 1,000 GW, with typical asset lives of 25–40 years and proprietary spare parts creating switching costs and long-term O&M dependence. Localization and multi-vendor frameworks have raised in-country sourcing and spare-part availability, but advanced retrofit projects and digital control upgrades in 2024 keep supplier power elevated for specialized scopes.

Renewables OEM pricing tailwinds

PV module and onshore wind-turbine pricing softened in 2024, with module spot prices down roughly 15–20% year-on-year to about $0.18–0.20/W and turbine OEM prices easing ~5–10%, reducing supplier leverage.

Global module capacity overhang of ~15–25% improved buyer terms and lead times, but high-efficiency cells (TOPCon/IBC) and large offshore turbines command 10–30% premiums, while grid-connection gear and battery cells still face periodic cyclic tightness.

Fuel logistics and quality constraints

Railway allocations, port slots and coal quality specs give logistics providers leverage over Datang; port slot utilization often exceeds 85% in peak months and winter freight surcharges rose ~20% in 2024, tightening negotiating power. Seasonal demand and weather disruptions can cut throughput sharply; long-term contracts and coordinated planning reduce this exposure. Hydro inflow variability in 2024 shifted fuel mixes, changing supplier dynamics.

- High slot utilization: >85% peak (2024)

- Freight surcharges: ~+20% (2024 winter)

- Long-term contracts mitigate shortages

- Hydro variability altered coal demand in 2024

Capital and financing providers

Large-scale generation for Datang depends heavily on state-owned banks and capital markets; in 2024 Chinese state-owned banks held roughly two-thirds of domestic banking assets, allowing lenders to influence terms via interest rates and covenants. Policy-aligned financing in 2024 remained tilted toward renewables and retrofits, improving access and pricing, while tighter green taxonomies have constrained coal lending and raised its effective cost. Balance sheet strength therefore materially shapes bargaining outcomes.

Integration cuts coal risk; ports at 85%+ strain, bank tilt lifts funding

Datang's partial vertical integration and coal-mine ownership reduced exposure to 2024 spot coal volatility, but external purchases remain material and logistics (port slots >85% peak) and OEMs (Harbin/Dongfang/Shanghai) retain pricing power for specialized equipment. State banks (~66% assets) and green finance tilt raise coal funding costs.

| Metric | 2024 |

|---|---|

| Port utilization (peak) | >85% |

| Winter freight surcharge | +~20% |

| Module spot price | $0.18–0.20/W |

| State banks share | ~66% |

What is included in the product

Tailored Porter’s Five Forces analysis for Datang International Power, assessing competitive rivalry, supplier and buyer power, substitutes, and entry barriers to identify strategic risks, pricing pressures, and opportunities for defensive positioning.

A concise one-sheet Porter's Five Forces for Datang International Power—translates complex sector pressures into a clear, editable radar chart and summary so teams can quickly spot threats and opportunities and drop it into decks or dashboards without macros.

Customers Bargaining Power

Grid companies as dominant buyers

State Grid (serving roughly 1.1 billion people) and China Southern Grid (serving about 240 million) are Datang’s primary off-takers, creating a highly concentrated buyer base; their scale gives strong leverage over dispatch, settlement and grid connection timelines. Regulatory tariff frameworks and provincial mandates in 2024 limit pure price bargaining, while plant compliance and reliability metrics directly affect acceptance and curtailment risk.

Market trading and direct supply growth

Expanding spot markets and direct supply in 2024 increased price sensitivity, as spot trades in pilot regions rose materially, pushing large industrial buyers to secure bilateral contracts and exploit peak/off-peak arbitrage. Major industrial users gained bargaining leverage through long-term and flexible bilateral deals. Datang must offer competitive tariffs and modular products. A diversified generation and trading portfolio enables tailored offers and effective hedging.

Tariff and policy mediation

Regulated tariffs and capacity payments set price bands that cap buyer power against Datang International, with China’s market reforms and capacity mechanisms stabilizing merchant exposure; solar and wind capacity in China surpassed roughly 800 GW by 2024, shifting system price dynamics. Policy incentives and priority dispatch for renewables increase demand for green attributes, while guarantee hours for contracted assets reduce buyer leverage over baseload contracts. Verification processes and renewable energy certificates (RECs) add negotiation layers and create separate value streams that buyers must factor into procurement and pricing discussions.

Quality, reliability, and ancillary services

Buyers value grid stability, fast ramping, and ancillary services which distinguish suppliers beyond price; in China in 2024 thermal plants still supplied over 50% of electricity, so coal/hydro flexibility can command premiums in capacity-constrained regions.

Demonstrated reliability cuts imbalance penalties and raises contract-renewal odds, while underperformance shifts leverage to buyers and spot-market exposure.

- Ancillary services: differentiation beyond price

- Coal/hydro flexibility: premium in constrained markets

- Reliability: fewer penalties, higher renewal probability

- Underperformance: increases buyer bargaining power

Curtailment and interconnection terms

In regions with grid congestion curtailment gives buyers effective volume control, and in 2024 China-wide renewable curtailment eased to mid-single digits, reducing but not eliminating buyer leverage; connection queue priority and metering rules directly affect realized revenues and settlement timing for Datang International Power, while proactive grid coordination and dispatch agreements cut exposure and delays.

- Curtailment risk: mid-single-digit rate (2024)

- Queue/metering: affects settlement timing and revenue

- Mitigation: grid coordination lowers leverage

- Diversification: lowers localized curtailment exposure

Buyer concentration caps dispatch; renewables>800 GW drive flexible demand

Concentrated buyers (State Grid ~1.1bn, China Southern ~240m) exert strong non-price leverage over dispatch and connection; regulated tariffs and capacity payments in 2024 cap pure price pressure. Renewables >800 GW and thermal still >50% of supply shift price dynamics; curtailment eased to mid-single-digit rates in 2024, reducing but not removing buyer volume control. Spot market growth and large industrial bilateral deals raise price sensitivity and demand for flexible products.

| Metric | 2024 |

|---|---|

| State Grid customers | ~1.1 bn |

| China Southern customers | ~240 m |

| Renewable capacity | >800 GW |

| Renewable curtailment | mid-single-digit % |

| Thermal share | >50% |

Same Document Delivered

Datang International Power Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Datang International Power you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable; instant access is granted upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Datang International Power’s Porter’s Five Forces snapshot highlights supplier and buyer leverage, rivalry intensity, threats from entrants and substitutes within China’s power sector. Regulatory shifts, fuel mix and capacity overhang shape competitive pressure and margins. This brief only scratches the surface. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Vertical integration tempers coal leverage

Datang’s ownership stakes in coal mines give it a stronger bargaining position on price and volumes, and in 2024 those upstream assets helped cushion the group against recent coal-price volatility and supply shocks. Partial vertical integration lowers exposure to spot-market spikes, yet Datang still purchases substantial external tonnage. Persistent rail-logistics bottlenecks and port capacity limits in 2024 can reintroduce leverage for transport providers, constraining procurement flexibility.

Equipment and O&M concentration

Major turbine, boiler and balance-of-plant supply in China is concentrated among Harbin Electric, Dongfang Electric and Shanghai Electric, giving suppliers measurable pricing and delivery leverage for Datang International Power. China's thermal fleet exceeds 1,000 GW, with typical asset lives of 25–40 years and proprietary spare parts creating switching costs and long-term O&M dependence. Localization and multi-vendor frameworks have raised in-country sourcing and spare-part availability, but advanced retrofit projects and digital control upgrades in 2024 keep supplier power elevated for specialized scopes.

Renewables OEM pricing tailwinds

PV module and onshore wind-turbine pricing softened in 2024, with module spot prices down roughly 15–20% year-on-year to about $0.18–0.20/W and turbine OEM prices easing ~5–10%, reducing supplier leverage.

Global module capacity overhang of ~15–25% improved buyer terms and lead times, but high-efficiency cells (TOPCon/IBC) and large offshore turbines command 10–30% premiums, while grid-connection gear and battery cells still face periodic cyclic tightness.

Fuel logistics and quality constraints

Railway allocations, port slots and coal quality specs give logistics providers leverage over Datang; port slot utilization often exceeds 85% in peak months and winter freight surcharges rose ~20% in 2024, tightening negotiating power. Seasonal demand and weather disruptions can cut throughput sharply; long-term contracts and coordinated planning reduce this exposure. Hydro inflow variability in 2024 shifted fuel mixes, changing supplier dynamics.

- High slot utilization: >85% peak (2024)

- Freight surcharges: ~+20% (2024 winter)

- Long-term contracts mitigate shortages

- Hydro variability altered coal demand in 2024

Capital and financing providers

Large-scale generation for Datang depends heavily on state-owned banks and capital markets; in 2024 Chinese state-owned banks held roughly two-thirds of domestic banking assets, allowing lenders to influence terms via interest rates and covenants. Policy-aligned financing in 2024 remained tilted toward renewables and retrofits, improving access and pricing, while tighter green taxonomies have constrained coal lending and raised its effective cost. Balance sheet strength therefore materially shapes bargaining outcomes.

Integration cuts coal risk; ports at 85%+ strain, bank tilt lifts funding

Datang's partial vertical integration and coal-mine ownership reduced exposure to 2024 spot coal volatility, but external purchases remain material and logistics (port slots >85% peak) and OEMs (Harbin/Dongfang/Shanghai) retain pricing power for specialized equipment. State banks (~66% assets) and green finance tilt raise coal funding costs.

| Metric | 2024 |

|---|---|

| Port utilization (peak) | >85% |

| Winter freight surcharge | +~20% |

| Module spot price | $0.18–0.20/W |

| State banks share | ~66% |

What is included in the product

Tailored Porter’s Five Forces analysis for Datang International Power, assessing competitive rivalry, supplier and buyer power, substitutes, and entry barriers to identify strategic risks, pricing pressures, and opportunities for defensive positioning.

A concise one-sheet Porter's Five Forces for Datang International Power—translates complex sector pressures into a clear, editable radar chart and summary so teams can quickly spot threats and opportunities and drop it into decks or dashboards without macros.

Customers Bargaining Power

Grid companies as dominant buyers

State Grid (serving roughly 1.1 billion people) and China Southern Grid (serving about 240 million) are Datang’s primary off-takers, creating a highly concentrated buyer base; their scale gives strong leverage over dispatch, settlement and grid connection timelines. Regulatory tariff frameworks and provincial mandates in 2024 limit pure price bargaining, while plant compliance and reliability metrics directly affect acceptance and curtailment risk.

Market trading and direct supply growth

Expanding spot markets and direct supply in 2024 increased price sensitivity, as spot trades in pilot regions rose materially, pushing large industrial buyers to secure bilateral contracts and exploit peak/off-peak arbitrage. Major industrial users gained bargaining leverage through long-term and flexible bilateral deals. Datang must offer competitive tariffs and modular products. A diversified generation and trading portfolio enables tailored offers and effective hedging.

Tariff and policy mediation

Regulated tariffs and capacity payments set price bands that cap buyer power against Datang International, with China’s market reforms and capacity mechanisms stabilizing merchant exposure; solar and wind capacity in China surpassed roughly 800 GW by 2024, shifting system price dynamics. Policy incentives and priority dispatch for renewables increase demand for green attributes, while guarantee hours for contracted assets reduce buyer leverage over baseload contracts. Verification processes and renewable energy certificates (RECs) add negotiation layers and create separate value streams that buyers must factor into procurement and pricing discussions.

Quality, reliability, and ancillary services

Buyers value grid stability, fast ramping, and ancillary services which distinguish suppliers beyond price; in China in 2024 thermal plants still supplied over 50% of electricity, so coal/hydro flexibility can command premiums in capacity-constrained regions.

Demonstrated reliability cuts imbalance penalties and raises contract-renewal odds, while underperformance shifts leverage to buyers and spot-market exposure.

- Ancillary services: differentiation beyond price

- Coal/hydro flexibility: premium in constrained markets

- Reliability: fewer penalties, higher renewal probability

- Underperformance: increases buyer bargaining power

Curtailment and interconnection terms

In regions with grid congestion curtailment gives buyers effective volume control, and in 2024 China-wide renewable curtailment eased to mid-single digits, reducing but not eliminating buyer leverage; connection queue priority and metering rules directly affect realized revenues and settlement timing for Datang International Power, while proactive grid coordination and dispatch agreements cut exposure and delays.

- Curtailment risk: mid-single-digit rate (2024)

- Queue/metering: affects settlement timing and revenue

- Mitigation: grid coordination lowers leverage

- Diversification: lowers localized curtailment exposure

Buyer concentration caps dispatch; renewables>800 GW drive flexible demand

Concentrated buyers (State Grid ~1.1bn, China Southern ~240m) exert strong non-price leverage over dispatch and connection; regulated tariffs and capacity payments in 2024 cap pure price pressure. Renewables >800 GW and thermal still >50% of supply shift price dynamics; curtailment eased to mid-single-digit rates in 2024, reducing but not removing buyer volume control. Spot market growth and large industrial bilateral deals raise price sensitivity and demand for flexible products.

| Metric | 2024 |

|---|---|

| State Grid customers | ~1.1 bn |

| China Southern customers | ~240 m |

| Renewable capacity | >800 GW |

| Renewable curtailment | mid-single-digit % |

| Thermal share | >50% |

Same Document Delivered

Datang International Power Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Datang International Power you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable; instant access is granted upon payment.