China Gas Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

China Gas Holdings faces moderate supplier leverage, intense regional competition, and regulatory sensitivity that together shape margins and expansion prospects; buyer power and substitutes (renewables) are rising but currently manageable. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to see force ratings, visuals, and actionable recommendations.

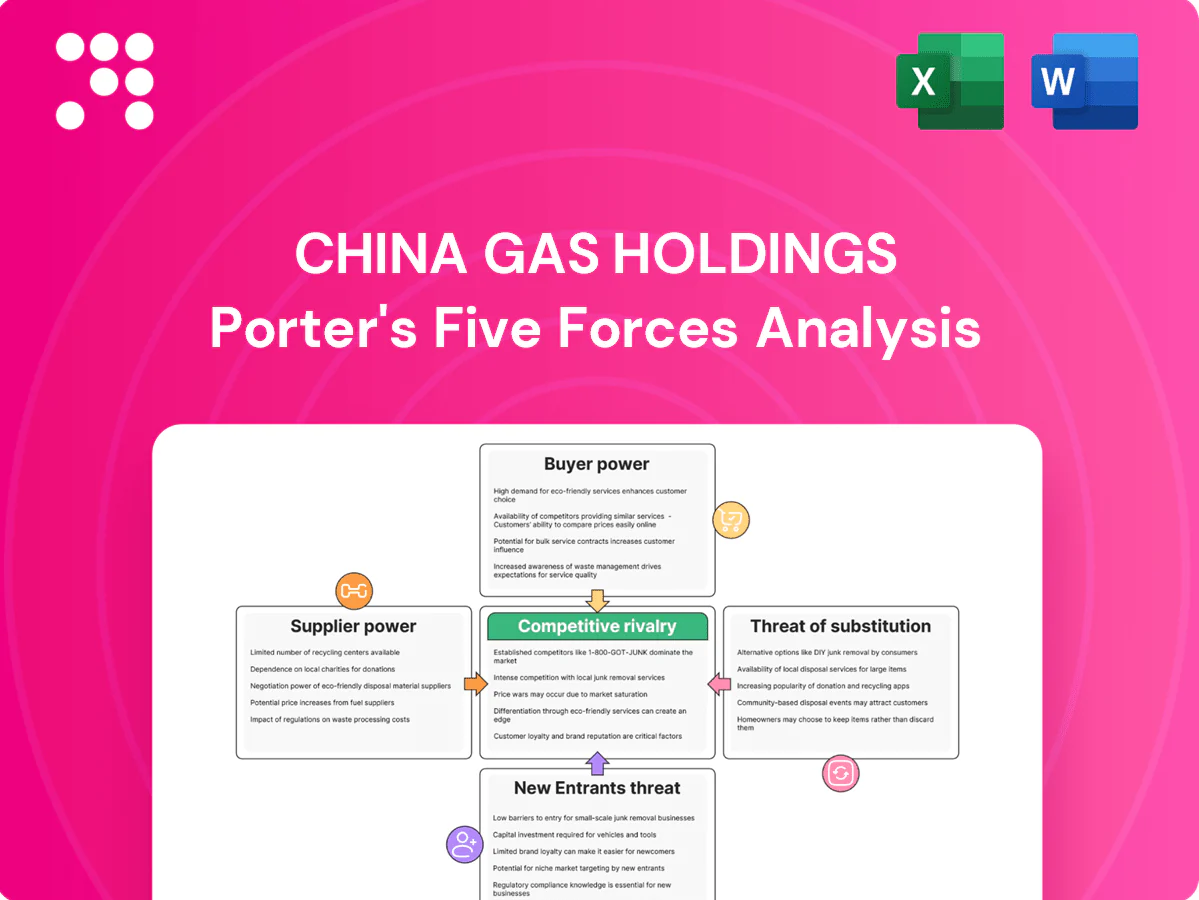

Suppliers Bargaining Power

Concentrated upstream

CNPC, Sinopec and CNOOC together supply roughly 80% of China’s upstream gas production (2024), giving suppliers material leverage over volumes and terms. PipeChina’s trunk-pipeline consolidation improved physical access but not upstream bargaining parity. China Gas remains exposed to take-or-pay clauses and contract rigidity, elevating dependency risk during tight market periods.

LNG price volatility

Imported LNG diversifies China Gas but exposes it to spot swings: JKM averaged about $12/MMBtu in 2024, yet cargo premiums spiked up to 30% during demand surges or geopolitical disruptions, compressing margins. Hedging and portfolio sourcing can cut exposure but cannot fully neutralize sudden spikes. Suppliers typically pass through cost rises faster than city-gas tariffs are adjusted, widening a timing mismatch.

Pipeline access gatekeeping

Third-party access rules exist, but allocation, capacity and balancing remain largely controlled by state midstream operators and regulators, constraining city distributors' flexibility; China’s gas consumption reached about 360 billion cubic meters in 2023 (National Bureau of Statistics), amplifying demand pressure on gate stations. Operational constraints at gate stations create bottleneck power for midstream operators, so China Gas must coordinate tightly with pipeline owners and regulators to secure stable flows.

Specification and quality control

Suppliers set gas quality, calorific value and delivery pressure standards that China Gas must meet; variability forces blending and system adjustments, raising operating costs and OPEX volatility. Dependence on supplier certification and testing amplifies supplier leverage, since noncompliance can trigger penalties or volume curtailments that directly disrupt end-customer supply. Contractual deviations have led to service interruptions in the sector, increasing risk exposure.

- Supplier control: quality, calorific value, pressure

- Operational impact: blending and system adjustments raise OPEX

- Compliance risk: penalties or curtailments affect end-customer supply

Limited alternative feedstock

Domestic unconventional gas and coal-to-gas output rose in 2024 (combined ~40 bcm) but still cover under 25% of China’s gas demand, leaving China Gas Holdings reliant on major upstream suppliers; biogas/RNG pilots expanded from a very low base (~1–2 bcm capacity in 2024) so supplier optionality remains constrained near-term, keeping bargaining power tilted toward upstream providers.

- Domestic unconventional + coal-to-gas ~40 bcm (2024)

- Share of national gas demand <25% (2024)

- Biogas/RNG pilot capacity ~1–2 bcm (2024)

- Supplier optionality limited → upstream bargaining advantage

Major upstream control (~80%) and rising LNG costs drive margin volatility for China gas retailers

Major upstream players (CNPC/Sinopec/CNOOC) supply ~80% of upstream gas (2024), giving suppliers strong leverage; China Gas faces take-or-pay and contract rigidity. Imported LNG (JKM ~$12/MMBtu in 2024) and spot premiums up to +30% raise margin volatility. Domestic unconventional + coal-to-gas ~40 bcm (<25% demand) and biogas ~1–2 bcm limit short-term supplier alternatives.

| Metric | 2024 value | Implication |

|---|---|---|

| Upstream share | CNPC/Sinopec/CNOOC ~80% | High supplier leverage |

| JKM price | $12/MMBtu avg | Imported cost exposure |

| Domestic supply | ~40 bcm (<25%) | Limited diversification |

What is included in the product

Provides a tailored Porter’s Five Forces assessment of China Gas Holdings, highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory/technology disruptions; evaluates how these forces affect pricing, margins and strategic positioning for investors and management.

Clear one-sheet Porter's Five Forces for China Gas Holdings—quickly visualize competitive pressure with an editable spider chart and customizable force levels to inform boardroom decisions.

Customers Bargaining Power

Regulated residential tariffs

Residential gas tariffs in China are regulated by the NDRC and local authorities, limiting end-user bargaining power and keeping buyer leverage low in 2024. Pass-through of wholesale cost changes to retail can be delayed by several months, temporarily squeezing distributor margins. Network dependence and high switching costs make consumer substitution difficult, reinforcing weak residential buyer power.

Industrial/commercial negotiability

Larger industrial and commercial users negotiate volumes, discounts and seasonal terms, leveraging concentrated purchases to extract concessions. They can credibly threaten fuel switching or dual-fuel setups to secure lower tariffs, making contract tenors and indexation key bargaining levers. Aggregated demand from these accounts gives China Gas moderate-to-high buyer power, forcing flexible pricing and tailored contract structures.

Multi-sourcing and dual-fuel

Many industrial and commercial customers maintain LPG, diesel or electricity back-ups to increase leverage, enabling tactical switching during price spikes; in 2024 China saw non-fossil generation near 32% of power supply, raising substitution options for buyers. China Gas counters with bundled gas-plus-services and uptime guarantees, protecting margins and retention. Buyer power rises where alternatives are abundant and switching costs low.

Service quality sensitivity

Reliability, pressure stability and fast emergency response materially drive customer satisfaction for China Gas (HKEX: 384) in 2024, as outages can trigger service penalties and contract renegotiation pressure.

Stronger SLAs and rollout of digital metering in 2024 help defend pricing by reducing billed losses and tightening performance-linked fees; service differentiation therefore tempers buyer power.

- Reliability impact

- Outage penalties

- SLAs + digital metering

- Service differentiation

Appliance and value-add bundling

Appliance and value-add bundling—combining bundled appliance sales, financing and maintenance—creates switching costs that lock customers into China Gas’s ecosystem, with typical lifecycle service contracts in 2024 spanning 3–5 years and rising uptake of pay-as-you-go financing.

Lifecycle services shift perceived value from commodity gas to integrated solutions, reducing pure price-based negotiations and lowering buyer leverage as long-term bundles deepen retention.

- Bundled appliance sales

- Financing + maintenance

- 3–5 year contract horizons (2024)

- Lower pure price bargaining

Regulated tariffs weaken residential buyers; industrial leverage grows as non-fossil hits 32%

Residential buyer power is low due to NDRC-regulated tariffs and high switching costs; distributor margins face short-term squeeze from delayed cost pass-through. Industrial buyers hold moderate-high leverage via volume contracts and fuel-switch options; non-fossil power ~32% (2024). Bundled 3–5yr service contracts and digital metering reduce pure price bargaining.

| Metric | 2024 |

|---|---|

| Non-fossil power share | 32% |

| Service contract length | 3–5 yrs |

| Residential buyer power | Low |

| Industrial buyer power | Moderate-High |

Same Document Delivered

China Gas Holdings Porter's Five Forces Analysis

This China Gas Holdings Porter’s Five Forces analysis is the exact, fully formatted document you’re previewing and will receive immediately after purchase. It contains a comprehensive assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. No placeholders or samples—this file is ready for download and use.

Don't Miss the Bigger Picture

China Gas Holdings faces moderate supplier leverage, intense regional competition, and regulatory sensitivity that together shape margins and expansion prospects; buyer power and substitutes (renewables) are rising but currently manageable. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to see force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated upstream

CNPC, Sinopec and CNOOC together supply roughly 80% of China’s upstream gas production (2024), giving suppliers material leverage over volumes and terms. PipeChina’s trunk-pipeline consolidation improved physical access but not upstream bargaining parity. China Gas remains exposed to take-or-pay clauses and contract rigidity, elevating dependency risk during tight market periods.

LNG price volatility

Imported LNG diversifies China Gas but exposes it to spot swings: JKM averaged about $12/MMBtu in 2024, yet cargo premiums spiked up to 30% during demand surges or geopolitical disruptions, compressing margins. Hedging and portfolio sourcing can cut exposure but cannot fully neutralize sudden spikes. Suppliers typically pass through cost rises faster than city-gas tariffs are adjusted, widening a timing mismatch.

Pipeline access gatekeeping

Third-party access rules exist, but allocation, capacity and balancing remain largely controlled by state midstream operators and regulators, constraining city distributors' flexibility; China’s gas consumption reached about 360 billion cubic meters in 2023 (National Bureau of Statistics), amplifying demand pressure on gate stations. Operational constraints at gate stations create bottleneck power for midstream operators, so China Gas must coordinate tightly with pipeline owners and regulators to secure stable flows.

Specification and quality control

Suppliers set gas quality, calorific value and delivery pressure standards that China Gas must meet; variability forces blending and system adjustments, raising operating costs and OPEX volatility. Dependence on supplier certification and testing amplifies supplier leverage, since noncompliance can trigger penalties or volume curtailments that directly disrupt end-customer supply. Contractual deviations have led to service interruptions in the sector, increasing risk exposure.

- Supplier control: quality, calorific value, pressure

- Operational impact: blending and system adjustments raise OPEX

- Compliance risk: penalties or curtailments affect end-customer supply

Limited alternative feedstock

Domestic unconventional gas and coal-to-gas output rose in 2024 (combined ~40 bcm) but still cover under 25% of China’s gas demand, leaving China Gas Holdings reliant on major upstream suppliers; biogas/RNG pilots expanded from a very low base (~1–2 bcm capacity in 2024) so supplier optionality remains constrained near-term, keeping bargaining power tilted toward upstream providers.

- Domestic unconventional + coal-to-gas ~40 bcm (2024)

- Share of national gas demand <25% (2024)

- Biogas/RNG pilot capacity ~1–2 bcm (2024)

- Supplier optionality limited → upstream bargaining advantage

Major upstream control (~80%) and rising LNG costs drive margin volatility for China gas retailers

Major upstream players (CNPC/Sinopec/CNOOC) supply ~80% of upstream gas (2024), giving suppliers strong leverage; China Gas faces take-or-pay and contract rigidity. Imported LNG (JKM ~$12/MMBtu in 2024) and spot premiums up to +30% raise margin volatility. Domestic unconventional + coal-to-gas ~40 bcm (<25% demand) and biogas ~1–2 bcm limit short-term supplier alternatives.

| Metric | 2024 value | Implication |

|---|---|---|

| Upstream share | CNPC/Sinopec/CNOOC ~80% | High supplier leverage |

| JKM price | $12/MMBtu avg | Imported cost exposure |

| Domestic supply | ~40 bcm (<25%) | Limited diversification |

What is included in the product

Provides a tailored Porter’s Five Forces assessment of China Gas Holdings, highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory/technology disruptions; evaluates how these forces affect pricing, margins and strategic positioning for investors and management.

Clear one-sheet Porter's Five Forces for China Gas Holdings—quickly visualize competitive pressure with an editable spider chart and customizable force levels to inform boardroom decisions.

Customers Bargaining Power

Regulated residential tariffs

Residential gas tariffs in China are regulated by the NDRC and local authorities, limiting end-user bargaining power and keeping buyer leverage low in 2024. Pass-through of wholesale cost changes to retail can be delayed by several months, temporarily squeezing distributor margins. Network dependence and high switching costs make consumer substitution difficult, reinforcing weak residential buyer power.

Industrial/commercial negotiability

Larger industrial and commercial users negotiate volumes, discounts and seasonal terms, leveraging concentrated purchases to extract concessions. They can credibly threaten fuel switching or dual-fuel setups to secure lower tariffs, making contract tenors and indexation key bargaining levers. Aggregated demand from these accounts gives China Gas moderate-to-high buyer power, forcing flexible pricing and tailored contract structures.

Multi-sourcing and dual-fuel

Many industrial and commercial customers maintain LPG, diesel or electricity back-ups to increase leverage, enabling tactical switching during price spikes; in 2024 China saw non-fossil generation near 32% of power supply, raising substitution options for buyers. China Gas counters with bundled gas-plus-services and uptime guarantees, protecting margins and retention. Buyer power rises where alternatives are abundant and switching costs low.

Service quality sensitivity

Reliability, pressure stability and fast emergency response materially drive customer satisfaction for China Gas (HKEX: 384) in 2024, as outages can trigger service penalties and contract renegotiation pressure.

Stronger SLAs and rollout of digital metering in 2024 help defend pricing by reducing billed losses and tightening performance-linked fees; service differentiation therefore tempers buyer power.

- Reliability impact

- Outage penalties

- SLAs + digital metering

- Service differentiation

Appliance and value-add bundling

Appliance and value-add bundling—combining bundled appliance sales, financing and maintenance—creates switching costs that lock customers into China Gas’s ecosystem, with typical lifecycle service contracts in 2024 spanning 3–5 years and rising uptake of pay-as-you-go financing.

Lifecycle services shift perceived value from commodity gas to integrated solutions, reducing pure price-based negotiations and lowering buyer leverage as long-term bundles deepen retention.

- Bundled appliance sales

- Financing + maintenance

- 3–5 year contract horizons (2024)

- Lower pure price bargaining

Regulated tariffs weaken residential buyers; industrial leverage grows as non-fossil hits 32%

Residential buyer power is low due to NDRC-regulated tariffs and high switching costs; distributor margins face short-term squeeze from delayed cost pass-through. Industrial buyers hold moderate-high leverage via volume contracts and fuel-switch options; non-fossil power ~32% (2024). Bundled 3–5yr service contracts and digital metering reduce pure price bargaining.

| Metric | 2024 |

|---|---|

| Non-fossil power share | 32% |

| Service contract length | 3–5 yrs |

| Residential buyer power | Low |

| Industrial buyer power | Moderate-High |

Same Document Delivered

China Gas Holdings Porter's Five Forces Analysis

This China Gas Holdings Porter’s Five Forces analysis is the exact, fully formatted document you’re previewing and will receive immediately after purchase. It contains a comprehensive assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. No placeholders or samples—this file is ready for download and use.

Description

Don't Miss the Bigger Picture

China Gas Holdings faces moderate supplier leverage, intense regional competition, and regulatory sensitivity that together shape margins and expansion prospects; buyer power and substitutes (renewables) are rising but currently manageable. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to see force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated upstream

CNPC, Sinopec and CNOOC together supply roughly 80% of China’s upstream gas production (2024), giving suppliers material leverage over volumes and terms. PipeChina’s trunk-pipeline consolidation improved physical access but not upstream bargaining parity. China Gas remains exposed to take-or-pay clauses and contract rigidity, elevating dependency risk during tight market periods.

LNG price volatility

Imported LNG diversifies China Gas but exposes it to spot swings: JKM averaged about $12/MMBtu in 2024, yet cargo premiums spiked up to 30% during demand surges or geopolitical disruptions, compressing margins. Hedging and portfolio sourcing can cut exposure but cannot fully neutralize sudden spikes. Suppliers typically pass through cost rises faster than city-gas tariffs are adjusted, widening a timing mismatch.

Pipeline access gatekeeping

Third-party access rules exist, but allocation, capacity and balancing remain largely controlled by state midstream operators and regulators, constraining city distributors' flexibility; China’s gas consumption reached about 360 billion cubic meters in 2023 (National Bureau of Statistics), amplifying demand pressure on gate stations. Operational constraints at gate stations create bottleneck power for midstream operators, so China Gas must coordinate tightly with pipeline owners and regulators to secure stable flows.

Specification and quality control

Suppliers set gas quality, calorific value and delivery pressure standards that China Gas must meet; variability forces blending and system adjustments, raising operating costs and OPEX volatility. Dependence on supplier certification and testing amplifies supplier leverage, since noncompliance can trigger penalties or volume curtailments that directly disrupt end-customer supply. Contractual deviations have led to service interruptions in the sector, increasing risk exposure.

- Supplier control: quality, calorific value, pressure

- Operational impact: blending and system adjustments raise OPEX

- Compliance risk: penalties or curtailments affect end-customer supply

Limited alternative feedstock

Domestic unconventional gas and coal-to-gas output rose in 2024 (combined ~40 bcm) but still cover under 25% of China’s gas demand, leaving China Gas Holdings reliant on major upstream suppliers; biogas/RNG pilots expanded from a very low base (~1–2 bcm capacity in 2024) so supplier optionality remains constrained near-term, keeping bargaining power tilted toward upstream providers.

- Domestic unconventional + coal-to-gas ~40 bcm (2024)

- Share of national gas demand <25% (2024)

- Biogas/RNG pilot capacity ~1–2 bcm (2024)

- Supplier optionality limited → upstream bargaining advantage

Major upstream control (~80%) and rising LNG costs drive margin volatility for China gas retailers

Major upstream players (CNPC/Sinopec/CNOOC) supply ~80% of upstream gas (2024), giving suppliers strong leverage; China Gas faces take-or-pay and contract rigidity. Imported LNG (JKM ~$12/MMBtu in 2024) and spot premiums up to +30% raise margin volatility. Domestic unconventional + coal-to-gas ~40 bcm (<25% demand) and biogas ~1–2 bcm limit short-term supplier alternatives.

| Metric | 2024 value | Implication |

|---|---|---|

| Upstream share | CNPC/Sinopec/CNOOC ~80% | High supplier leverage |

| JKM price | $12/MMBtu avg | Imported cost exposure |

| Domestic supply | ~40 bcm (<25%) | Limited diversification |

What is included in the product

Provides a tailored Porter’s Five Forces assessment of China Gas Holdings, highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory/technology disruptions; evaluates how these forces affect pricing, margins and strategic positioning for investors and management.

Clear one-sheet Porter's Five Forces for China Gas Holdings—quickly visualize competitive pressure with an editable spider chart and customizable force levels to inform boardroom decisions.

Customers Bargaining Power

Regulated residential tariffs

Residential gas tariffs in China are regulated by the NDRC and local authorities, limiting end-user bargaining power and keeping buyer leverage low in 2024. Pass-through of wholesale cost changes to retail can be delayed by several months, temporarily squeezing distributor margins. Network dependence and high switching costs make consumer substitution difficult, reinforcing weak residential buyer power.

Industrial/commercial negotiability

Larger industrial and commercial users negotiate volumes, discounts and seasonal terms, leveraging concentrated purchases to extract concessions. They can credibly threaten fuel switching or dual-fuel setups to secure lower tariffs, making contract tenors and indexation key bargaining levers. Aggregated demand from these accounts gives China Gas moderate-to-high buyer power, forcing flexible pricing and tailored contract structures.

Multi-sourcing and dual-fuel

Many industrial and commercial customers maintain LPG, diesel or electricity back-ups to increase leverage, enabling tactical switching during price spikes; in 2024 China saw non-fossil generation near 32% of power supply, raising substitution options for buyers. China Gas counters with bundled gas-plus-services and uptime guarantees, protecting margins and retention. Buyer power rises where alternatives are abundant and switching costs low.

Service quality sensitivity

Reliability, pressure stability and fast emergency response materially drive customer satisfaction for China Gas (HKEX: 384) in 2024, as outages can trigger service penalties and contract renegotiation pressure.

Stronger SLAs and rollout of digital metering in 2024 help defend pricing by reducing billed losses and tightening performance-linked fees; service differentiation therefore tempers buyer power.

- Reliability impact

- Outage penalties

- SLAs + digital metering

- Service differentiation

Appliance and value-add bundling

Appliance and value-add bundling—combining bundled appliance sales, financing and maintenance—creates switching costs that lock customers into China Gas’s ecosystem, with typical lifecycle service contracts in 2024 spanning 3–5 years and rising uptake of pay-as-you-go financing.

Lifecycle services shift perceived value from commodity gas to integrated solutions, reducing pure price-based negotiations and lowering buyer leverage as long-term bundles deepen retention.

- Bundled appliance sales

- Financing + maintenance

- 3–5 year contract horizons (2024)

- Lower pure price bargaining

Regulated tariffs weaken residential buyers; industrial leverage grows as non-fossil hits 32%

Residential buyer power is low due to NDRC-regulated tariffs and high switching costs; distributor margins face short-term squeeze from delayed cost pass-through. Industrial buyers hold moderate-high leverage via volume contracts and fuel-switch options; non-fossil power ~32% (2024). Bundled 3–5yr service contracts and digital metering reduce pure price bargaining.

| Metric | 2024 |

|---|---|

| Non-fossil power share | 32% |

| Service contract length | 3–5 yrs |

| Residential buyer power | Low |

| Industrial buyer power | Moderate-High |

Same Document Delivered

China Gas Holdings Porter's Five Forces Analysis

This China Gas Holdings Porter’s Five Forces analysis is the exact, fully formatted document you’re previewing and will receive immediately after purchase. It contains a comprehensive assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. No placeholders or samples—this file is ready for download and use.