Red Star Macalline Home Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

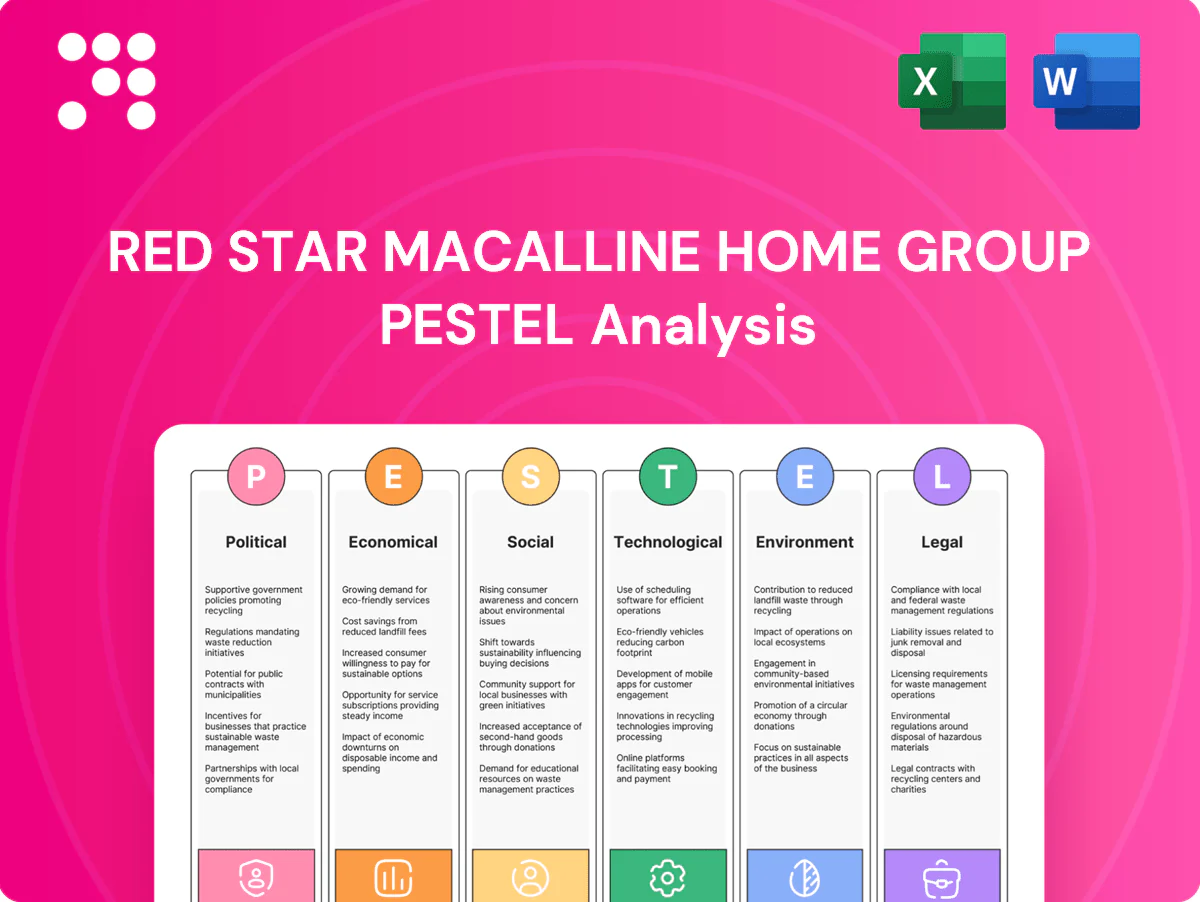

Gain strategic advantage with our PESTLE Analysis of Red Star Macalline Home Group. We map political, economic, social, technological, legal and environmental forces shaping its growth and risks. Ideal for investors and strategists—buy the full report to download actionable, editable insights now.

Political factors

Consumption-boost policies

China frequently rolls out measures to stimulate consumption — including 2024 local consumption voucher and home-improvement subsidy pilots — helping national retail sales of consumer goods rise about 6.7% year-on-year in 2024 (NBS). Such policies lift mall footfall and tenant sales, and Red Star Macalline can align promotions, trade-in programs and tailored financing to capture this demand. Execution varies by city, so local coordination across its mall network is essential.

Property sector interventions

Policy shifts in 2024—including targeted easing and a lower 5-year LPR (about 3.95%)—directly affect renovation demand, with easing unlocking transactions and fueling furnishing spend while tightening suppresses it. Furnishing typically represents roughly 30% of renovation outlays, so shifts in home sales (tier-1/2 cities account for ~60% of volumes) materially impact Red Star Macalline. The company should flex leasing terms and marketing to match cycle moves and closely monitor city-level policy pilots.

Central–local dynamics

Permitting, land use and mall approvals for Red Star Macalline hinge on local governments’ fiscal and development priorities, with approvals often tied to municipal zoning and infrastructure plans as China’s urbanization reached about 64.7% in 2023. Strong municipal relationships can accelerate openings and renovation permits, shortening lead times for new stores. Regionally negotiated incentives or rent-relief deals are common, but variability across jurisdictions raises execution risk across the network.

Trade and import regulation

Tariffs, standards and customs rules (commonly ranging 0–25% by HS code) directly affect costs and lead times for imported furniture and raw materials, altering assortment, pricing and delivery windows for Red Star Macalline tenants. Geopolitical shifts have recently disrupted supplier routes, so diversifying supplier bases and promoting domestic brands reduces exposure, while transparent compliance limits clearance delays.

- Tariffs: 0–25% by HS code

- Risk: supply/price volatility from geopolitics

- Mitigation: diversify suppliers, promote domestic brands

- Compliance: reduces customs clearance delays

Infrastructure and urban planning

Transit expansions and urban redevelopment reshape mall accessibility and catchment areas; China’s urban rail network exceeded 9,500 km by end-2023, expanding annual catchments for retail. Co-locating near transport hubs increases foot traffic and logistics efficiency, often lifting mall visitation rates materially. Active engagement in city planning helps secure advantageous sites and avoid stranded assets from misaligned developments.

- Transit growth: China urban rail >9,500 km (2023)

- Site strategy: proximity to hubs boosts footfall and logistics

- Planning engagement: reduces risk of underperforming malls

Vouchers spark retail +6.7% and mall traffic; LPR 3.95% aids renovation demand

Local consumption vouchers and 2024 home-improvement pilots lifted national retail goods +6.7% y/y (NBS), boosting mall traffic; 5y LPR ~3.95% in 2024 affects renovation demand; municipal zoning and permits hinge on urbanization ~64.7% (2023); tariffs 0–25% and geopolitics raise input cost risk; urban rail >9,500 km (2023) expands catchments.

| Factor | Stat | Impact | Mitigation |

|---|---|---|---|

| Consumption | +6.7% (2024) | Higher footfall | Promos/finance |

| Rates | LPR 3.95% (2024) | Renovation demand | Flexible leasing |

| Tariffs | 0–25% | Cost/lead time | Supply diversify |

| Urbanization | 64.7% (2023) | Site approvals | Local gov engagement |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces specifically shape Red Star Macalline Home Group’s operating landscape, using current data and trends to identify risks, growth levers and forward-looking scenarios to guide executives, investors and strategists.

A concise, visually segmented PESTLE summary of Red Star Macalline that’s editable for local context, PowerPoint-ready and easily shareable to speed risk discussions, align teams, and support planning or client reports.

Economic factors

Housing cycle sensitivity

Renovation and furnishing spend at Red Star Macalline closely tracks new home sales and completions, with mall sales highly correlated to housing activity; the group operates over 400 shopping complexes across China, concentrating exposure to residential cycles.

Prolonged property downturns compress tenant revenues and rent collection, pressuring mall cashflows and franchisee performance.

Counter-cyclical services (maintenance, replacements) and flexible, short-term leases have cushioned demand and reduced vacancy risk during weak market episodes.

Consumer income and confidence

Rising or falling disposable income shifts basket sizes and upgrade cycles; with China retail sales up about 5.6% in 2024 (NBS), higher disposable income supports premium furniture demand while dips compress baskets. Confidence shocks delay non-essential décor purchases, so Red Star Macalline can broaden affordability via value tiers and financing. Data-driven, targeted promotions during soft months improve conversion and average ticket.

Inflation and input costs

Commodity and logistics costs remain key levers for tenant pricing and margins: China’s CPI was only about 0.2% in 2024, but input-price volatility persisted as logistics normalized from pandemic highs, pressuring margins and requiring clearer value communication to avoid traffic declines. Index-linked or staggered rent escalators are increasingly used to share inflation risk between Red Star Macalline and tenants. Joint procurement and shared fulfillment have reduced procurement and last‑mile costs in industry cases by double digits, lowering total cost.

Credit conditions

Availability and cost of consumer and SME credit shape big-ticket spend and tenant liquidity; China household debt-to-GDP was about 61% in 2024, constraining discretionary buying and raising default risk for retailers and landlords.

Tighter lending increases vacancy and default risks; partnerships with banks and BNPL providers (rising adoption in 2023–24) and rigorous tenant screening with early-warning analytics are essential.

- Credit squeeze: higher funding cost → lower sales

- 61% household debt/GDP (2024)

- BNPL/lender partnerships sustain demand

- Tenant screening + early-warning reduces defaults

Regional demand divergence

Tier-1/2 cities show greater resilience in demand for home furnishings while lower-tier markets remain more cyclical; China’s retail recovery strengthened in 2024 with retail sales of consumer goods up about 5% year-on-year, concentrating spending in major city clusters. Red Star Macalline can optimize tenant mixes and pricing by city tier to lift sales productivity and margins. Rebalancing the portfolio toward higher-yield, stable locations and using localized marketing increases ROI and occupancy stability.

- Tier differentiation: prioritize Tier-1/2 for stability

- Tenant mix: tailor by city cluster

- Portfolio tilt: shift to higher-yield locations

- Marketing: local campaigns to boost conversion

Vouchers spark retail +6.7% and mall traffic; LPR 3.95% aids renovation demand

Renovation/furnishing sales track housing cycles; group operates over 400 malls, tying revenue to property recovery.

Prolonged downturns squeeze tenant cashflows and rents; flexible short leases and counter-cyclical services partially mitigate impact.

Disposable income and credit availability drive big-ticket demand—China retail sales +5.6% (2024); household debt/GDP ~61% (2024).

Input cost volatility (CPI ~0.2% 2024) and logistics affect margins; BNPL and bank partnerships support demand and lower defaults.

| Metric | Value (2024) |

|---|---|

| Malls | 400+ |

| Retail sales growth | +5.6% |

| Household debt/GDP | 61% |

| CPI | 0.2% |

Same Document Delivered

Red Star Macalline Home Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This PESTLE analysis of Red Star Macalline Home Group includes political, economic, social, technological, legal, and environmental assessments with actionable insights and key references. The layout, content, and structure visible here are exactly what you’ll download immediately after buying.

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic advantage with our PESTLE Analysis of Red Star Macalline Home Group. We map political, economic, social, technological, legal and environmental forces shaping its growth and risks. Ideal for investors and strategists—buy the full report to download actionable, editable insights now.

Political factors

Consumption-boost policies

China frequently rolls out measures to stimulate consumption — including 2024 local consumption voucher and home-improvement subsidy pilots — helping national retail sales of consumer goods rise about 6.7% year-on-year in 2024 (NBS). Such policies lift mall footfall and tenant sales, and Red Star Macalline can align promotions, trade-in programs and tailored financing to capture this demand. Execution varies by city, so local coordination across its mall network is essential.

Property sector interventions

Policy shifts in 2024—including targeted easing and a lower 5-year LPR (about 3.95%)—directly affect renovation demand, with easing unlocking transactions and fueling furnishing spend while tightening suppresses it. Furnishing typically represents roughly 30% of renovation outlays, so shifts in home sales (tier-1/2 cities account for ~60% of volumes) materially impact Red Star Macalline. The company should flex leasing terms and marketing to match cycle moves and closely monitor city-level policy pilots.

Central–local dynamics

Permitting, land use and mall approvals for Red Star Macalline hinge on local governments’ fiscal and development priorities, with approvals often tied to municipal zoning and infrastructure plans as China’s urbanization reached about 64.7% in 2023. Strong municipal relationships can accelerate openings and renovation permits, shortening lead times for new stores. Regionally negotiated incentives or rent-relief deals are common, but variability across jurisdictions raises execution risk across the network.

Trade and import regulation

Tariffs, standards and customs rules (commonly ranging 0–25% by HS code) directly affect costs and lead times for imported furniture and raw materials, altering assortment, pricing and delivery windows for Red Star Macalline tenants. Geopolitical shifts have recently disrupted supplier routes, so diversifying supplier bases and promoting domestic brands reduces exposure, while transparent compliance limits clearance delays.

- Tariffs: 0–25% by HS code

- Risk: supply/price volatility from geopolitics

- Mitigation: diversify suppliers, promote domestic brands

- Compliance: reduces customs clearance delays

Infrastructure and urban planning

Transit expansions and urban redevelopment reshape mall accessibility and catchment areas; China’s urban rail network exceeded 9,500 km by end-2023, expanding annual catchments for retail. Co-locating near transport hubs increases foot traffic and logistics efficiency, often lifting mall visitation rates materially. Active engagement in city planning helps secure advantageous sites and avoid stranded assets from misaligned developments.

- Transit growth: China urban rail >9,500 km (2023)

- Site strategy: proximity to hubs boosts footfall and logistics

- Planning engagement: reduces risk of underperforming malls

Vouchers spark retail +6.7% and mall traffic; LPR 3.95% aids renovation demand

Local consumption vouchers and 2024 home-improvement pilots lifted national retail goods +6.7% y/y (NBS), boosting mall traffic; 5y LPR ~3.95% in 2024 affects renovation demand; municipal zoning and permits hinge on urbanization ~64.7% (2023); tariffs 0–25% and geopolitics raise input cost risk; urban rail >9,500 km (2023) expands catchments.

| Factor | Stat | Impact | Mitigation |

|---|---|---|---|

| Consumption | +6.7% (2024) | Higher footfall | Promos/finance |

| Rates | LPR 3.95% (2024) | Renovation demand | Flexible leasing |

| Tariffs | 0–25% | Cost/lead time | Supply diversify |

| Urbanization | 64.7% (2023) | Site approvals | Local gov engagement |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces specifically shape Red Star Macalline Home Group’s operating landscape, using current data and trends to identify risks, growth levers and forward-looking scenarios to guide executives, investors and strategists.

A concise, visually segmented PESTLE summary of Red Star Macalline that’s editable for local context, PowerPoint-ready and easily shareable to speed risk discussions, align teams, and support planning or client reports.

Economic factors

Housing cycle sensitivity

Renovation and furnishing spend at Red Star Macalline closely tracks new home sales and completions, with mall sales highly correlated to housing activity; the group operates over 400 shopping complexes across China, concentrating exposure to residential cycles.

Prolonged property downturns compress tenant revenues and rent collection, pressuring mall cashflows and franchisee performance.

Counter-cyclical services (maintenance, replacements) and flexible, short-term leases have cushioned demand and reduced vacancy risk during weak market episodes.

Consumer income and confidence

Rising or falling disposable income shifts basket sizes and upgrade cycles; with China retail sales up about 5.6% in 2024 (NBS), higher disposable income supports premium furniture demand while dips compress baskets. Confidence shocks delay non-essential décor purchases, so Red Star Macalline can broaden affordability via value tiers and financing. Data-driven, targeted promotions during soft months improve conversion and average ticket.

Inflation and input costs

Commodity and logistics costs remain key levers for tenant pricing and margins: China’s CPI was only about 0.2% in 2024, but input-price volatility persisted as logistics normalized from pandemic highs, pressuring margins and requiring clearer value communication to avoid traffic declines. Index-linked or staggered rent escalators are increasingly used to share inflation risk between Red Star Macalline and tenants. Joint procurement and shared fulfillment have reduced procurement and last‑mile costs in industry cases by double digits, lowering total cost.

Credit conditions

Availability and cost of consumer and SME credit shape big-ticket spend and tenant liquidity; China household debt-to-GDP was about 61% in 2024, constraining discretionary buying and raising default risk for retailers and landlords.

Tighter lending increases vacancy and default risks; partnerships with banks and BNPL providers (rising adoption in 2023–24) and rigorous tenant screening with early-warning analytics are essential.

- Credit squeeze: higher funding cost → lower sales

- 61% household debt/GDP (2024)

- BNPL/lender partnerships sustain demand

- Tenant screening + early-warning reduces defaults

Regional demand divergence

Tier-1/2 cities show greater resilience in demand for home furnishings while lower-tier markets remain more cyclical; China’s retail recovery strengthened in 2024 with retail sales of consumer goods up about 5% year-on-year, concentrating spending in major city clusters. Red Star Macalline can optimize tenant mixes and pricing by city tier to lift sales productivity and margins. Rebalancing the portfolio toward higher-yield, stable locations and using localized marketing increases ROI and occupancy stability.

- Tier differentiation: prioritize Tier-1/2 for stability

- Tenant mix: tailor by city cluster

- Portfolio tilt: shift to higher-yield locations

- Marketing: local campaigns to boost conversion

Vouchers spark retail +6.7% and mall traffic; LPR 3.95% aids renovation demand

Renovation/furnishing sales track housing cycles; group operates over 400 malls, tying revenue to property recovery.

Prolonged downturns squeeze tenant cashflows and rents; flexible short leases and counter-cyclical services partially mitigate impact.

Disposable income and credit availability drive big-ticket demand—China retail sales +5.6% (2024); household debt/GDP ~61% (2024).

Input cost volatility (CPI ~0.2% 2024) and logistics affect margins; BNPL and bank partnerships support demand and lower defaults.

| Metric | Value (2024) |

|---|---|

| Malls | 400+ |

| Retail sales growth | +5.6% |

| Household debt/GDP | 61% |

| CPI | 0.2% |

Same Document Delivered

Red Star Macalline Home Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This PESTLE analysis of Red Star Macalline Home Group includes political, economic, social, technological, legal, and environmental assessments with actionable insights and key references. The layout, content, and structure visible here are exactly what you’ll download immediately after buying.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic advantage with our PESTLE Analysis of Red Star Macalline Home Group. We map political, economic, social, technological, legal and environmental forces shaping its growth and risks. Ideal for investors and strategists—buy the full report to download actionable, editable insights now.

Political factors

Consumption-boost policies

China frequently rolls out measures to stimulate consumption — including 2024 local consumption voucher and home-improvement subsidy pilots — helping national retail sales of consumer goods rise about 6.7% year-on-year in 2024 (NBS). Such policies lift mall footfall and tenant sales, and Red Star Macalline can align promotions, trade-in programs and tailored financing to capture this demand. Execution varies by city, so local coordination across its mall network is essential.

Property sector interventions

Policy shifts in 2024—including targeted easing and a lower 5-year LPR (about 3.95%)—directly affect renovation demand, with easing unlocking transactions and fueling furnishing spend while tightening suppresses it. Furnishing typically represents roughly 30% of renovation outlays, so shifts in home sales (tier-1/2 cities account for ~60% of volumes) materially impact Red Star Macalline. The company should flex leasing terms and marketing to match cycle moves and closely monitor city-level policy pilots.

Central–local dynamics

Permitting, land use and mall approvals for Red Star Macalline hinge on local governments’ fiscal and development priorities, with approvals often tied to municipal zoning and infrastructure plans as China’s urbanization reached about 64.7% in 2023. Strong municipal relationships can accelerate openings and renovation permits, shortening lead times for new stores. Regionally negotiated incentives or rent-relief deals are common, but variability across jurisdictions raises execution risk across the network.

Trade and import regulation

Tariffs, standards and customs rules (commonly ranging 0–25% by HS code) directly affect costs and lead times for imported furniture and raw materials, altering assortment, pricing and delivery windows for Red Star Macalline tenants. Geopolitical shifts have recently disrupted supplier routes, so diversifying supplier bases and promoting domestic brands reduces exposure, while transparent compliance limits clearance delays.

- Tariffs: 0–25% by HS code

- Risk: supply/price volatility from geopolitics

- Mitigation: diversify suppliers, promote domestic brands

- Compliance: reduces customs clearance delays

Infrastructure and urban planning

Transit expansions and urban redevelopment reshape mall accessibility and catchment areas; China’s urban rail network exceeded 9,500 km by end-2023, expanding annual catchments for retail. Co-locating near transport hubs increases foot traffic and logistics efficiency, often lifting mall visitation rates materially. Active engagement in city planning helps secure advantageous sites and avoid stranded assets from misaligned developments.

- Transit growth: China urban rail >9,500 km (2023)

- Site strategy: proximity to hubs boosts footfall and logistics

- Planning engagement: reduces risk of underperforming malls

Vouchers spark retail +6.7% and mall traffic; LPR 3.95% aids renovation demand

Local consumption vouchers and 2024 home-improvement pilots lifted national retail goods +6.7% y/y (NBS), boosting mall traffic; 5y LPR ~3.95% in 2024 affects renovation demand; municipal zoning and permits hinge on urbanization ~64.7% (2023); tariffs 0–25% and geopolitics raise input cost risk; urban rail >9,500 km (2023) expands catchments.

| Factor | Stat | Impact | Mitigation |

|---|---|---|---|

| Consumption | +6.7% (2024) | Higher footfall | Promos/finance |

| Rates | LPR 3.95% (2024) | Renovation demand | Flexible leasing |

| Tariffs | 0–25% | Cost/lead time | Supply diversify |

| Urbanization | 64.7% (2023) | Site approvals | Local gov engagement |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces specifically shape Red Star Macalline Home Group’s operating landscape, using current data and trends to identify risks, growth levers and forward-looking scenarios to guide executives, investors and strategists.

A concise, visually segmented PESTLE summary of Red Star Macalline that’s editable for local context, PowerPoint-ready and easily shareable to speed risk discussions, align teams, and support planning or client reports.

Economic factors

Housing cycle sensitivity

Renovation and furnishing spend at Red Star Macalline closely tracks new home sales and completions, with mall sales highly correlated to housing activity; the group operates over 400 shopping complexes across China, concentrating exposure to residential cycles.

Prolonged property downturns compress tenant revenues and rent collection, pressuring mall cashflows and franchisee performance.

Counter-cyclical services (maintenance, replacements) and flexible, short-term leases have cushioned demand and reduced vacancy risk during weak market episodes.

Consumer income and confidence

Rising or falling disposable income shifts basket sizes and upgrade cycles; with China retail sales up about 5.6% in 2024 (NBS), higher disposable income supports premium furniture demand while dips compress baskets. Confidence shocks delay non-essential décor purchases, so Red Star Macalline can broaden affordability via value tiers and financing. Data-driven, targeted promotions during soft months improve conversion and average ticket.

Inflation and input costs

Commodity and logistics costs remain key levers for tenant pricing and margins: China’s CPI was only about 0.2% in 2024, but input-price volatility persisted as logistics normalized from pandemic highs, pressuring margins and requiring clearer value communication to avoid traffic declines. Index-linked or staggered rent escalators are increasingly used to share inflation risk between Red Star Macalline and tenants. Joint procurement and shared fulfillment have reduced procurement and last‑mile costs in industry cases by double digits, lowering total cost.

Credit conditions

Availability and cost of consumer and SME credit shape big-ticket spend and tenant liquidity; China household debt-to-GDP was about 61% in 2024, constraining discretionary buying and raising default risk for retailers and landlords.

Tighter lending increases vacancy and default risks; partnerships with banks and BNPL providers (rising adoption in 2023–24) and rigorous tenant screening with early-warning analytics are essential.

- Credit squeeze: higher funding cost → lower sales

- 61% household debt/GDP (2024)

- BNPL/lender partnerships sustain demand

- Tenant screening + early-warning reduces defaults

Regional demand divergence

Tier-1/2 cities show greater resilience in demand for home furnishings while lower-tier markets remain more cyclical; China’s retail recovery strengthened in 2024 with retail sales of consumer goods up about 5% year-on-year, concentrating spending in major city clusters. Red Star Macalline can optimize tenant mixes and pricing by city tier to lift sales productivity and margins. Rebalancing the portfolio toward higher-yield, stable locations and using localized marketing increases ROI and occupancy stability.

- Tier differentiation: prioritize Tier-1/2 for stability

- Tenant mix: tailor by city cluster

- Portfolio tilt: shift to higher-yield locations

- Marketing: local campaigns to boost conversion

Vouchers spark retail +6.7% and mall traffic; LPR 3.95% aids renovation demand

Renovation/furnishing sales track housing cycles; group operates over 400 malls, tying revenue to property recovery.

Prolonged downturns squeeze tenant cashflows and rents; flexible short leases and counter-cyclical services partially mitigate impact.

Disposable income and credit availability drive big-ticket demand—China retail sales +5.6% (2024); household debt/GDP ~61% (2024).

Input cost volatility (CPI ~0.2% 2024) and logistics affect margins; BNPL and bank partnerships support demand and lower defaults.

| Metric | Value (2024) |

|---|---|

| Malls | 400+ |

| Retail sales growth | +5.6% |

| Household debt/GDP | 61% |

| CPI | 0.2% |

Same Document Delivered

Red Star Macalline Home Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This PESTLE analysis of Red Star Macalline Home Group includes political, economic, social, technological, legal, and environmental assessments with actionable insights and key references. The layout, content, and structure visible here are exactly what you’ll download immediately after buying.