Red Star Macalline Home Group SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Explore Red Star Macalline Home Group’s strategic position with a concise SWOT snapshot highlighting its retail scale, supply-chain strengths, and sector risks. Want deeper, actionable insights and financial context? Purchase the full SWOT to receive a professionally written Word report and editable Excel matrix for planning and investment.

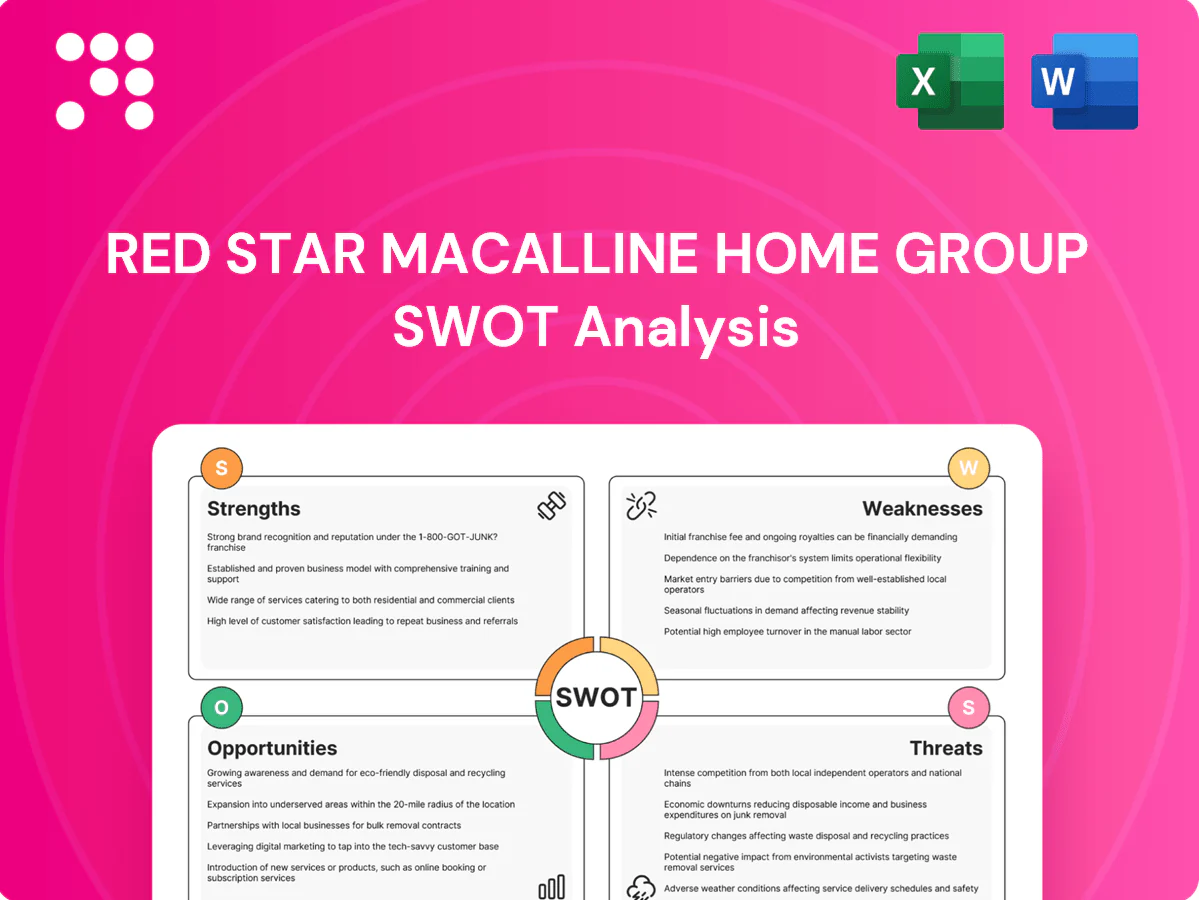

Strengths

Nationwide mall network

Red Star Macalline operates over 300 home-improvement malls across 200+ Chinese cities, giving scale advantages in centralized leasing and marketing that lower unit costs and boost bargaining power. The broad footprint attracts leading furniture and building-material brands seeking aggregated demand, while network effects enhance tenant curation and customer convenience through cross-mall promotions and standardized services.

Asset-light leasing model

Leasing space to retailers shifts inventory risk to tenants while generating recurring rental income; Red Star Macalline operates over 300 home-furnishing malls, supporting a landlord-style revenue base. This asset-light model yields more predictable cash flows versus pure retail operators, with portfolio occupancy remaining above 90% in recent periods. It frees capital for renovations, value-added services and digital tools to boost tenant productivity and footfall.

Diverse tenant mix

Diverse tenant mix across furniture, décor and building materials creates a one-stop shopping ecosystem that, as of 2024, spans 371 malls and over 30,000 brand tenants, driving cross-category traffic. Increased cross-shopping raises average dwell time and conversion for tenants, supporting higher per-visitor spend. This breadth reduces reliance on any single category’s cycle, smoothing revenue volatility for the group.

Strong brand in home furnishing

Recognition as a go-to destination for home improvement strengthens customer trust and repeat purchase behaviour, supporting Red Star Macalline's market position in 2024 and beyond. Brand equity enables premium mall locations and favourable tenant terms, and boosts participation and ROI from platform-wide promotions and events.

- Brand trust: enhances repeat purchases

- Premium sites: secures better tenant terms

- Promotions: higher conversion across platform

Value-added services ecosystem

Value-added services like design consultation and installation deepen customer engagement beyond browsing, driving reported higher conversion in mall formats versus pure e-commerce; China’s home furnishings market exceeded RMB 2 trillion in 2023, underpinning strong demand for on-site services. Service attachment raises tenant basket size and platform stickiness, differentiating malls from generic retail centers and online-only players.

- Design consultation increases conversion

- Installation ups average transaction value

- Enhances tenant retention and mall differentiation

Scale: 371 malls, 30,000+ tenants, >90% occupancy; RMB 2T home-furnishings tailwind

Scale of 371 malls and 30,000+ brand tenants (2024) drives bargaining power and cross-mall network effects. Asset-light leasing model yields recurring rental income with portfolio occupancy >90%, supporting stable cash flow. Market tailwinds: China home-furnishings market >RMB 2 trillion in 2023, enabling service upsell and higher tenant ROI.

| Metric | Value |

|---|---|

| Malls | 371 (2024) |

| Tenants | 30,000+ |

| Occupancy | >90% |

| Market size | >RMB 2 trillion (2023) |

What is included in the product

Delivers a strategic overview of Red Star Macalline Home Group’s internal strengths and weaknesses and external opportunities and threats, outlining key growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise SWOT matrix tailored to Red Star Macalline, enabling fast alignment on retail strengths and expansion risks for strategic decision-making.

Weaknesses

Exposure to China property cycle

Home-improvement demand at Red Star Macalline tracks housing transactions and renovations, so China’s property slowdown directly reduces tenant sales and leasing demand. With property-related activity historically accounting for about 25% of China’s GDP, cyclicality can materially pressure mall occupancy and rent growth. Recent market weakness has tightened cashflows for developers and retailers, amplifying downside risk to Red Star’s store-level revenues.

High dependence on offline footfall

Mall-centric traffic is exposed as global e-commerce captured 22.5% of retail sales in 2024, so shoppers increasingly start research and purchase online. Without robust O2O integration, discovery and consideration are likely to migrate to platforms, reducing in-mall conversion. Declining store sales can compress tenants’ margins and weaken renewal pricing power, risking lower rent growth and higher vacancy.

Capex needs for mall upgrades

Keeping its malls modern forces Red Star Macalline into ongoing remodeling and experience upgrades, which require significant recurring capex. Delays in refresh cycles can leave venues less competitive versus newer mixed-use and e-commerce-integrated formats. Elevated capex needs also risk compressing returns during economic downturns as investment timelines lengthen and cash flow tightens.

Tenant concentration and overlap risk

Tenant concentration at Red Star Macalline (1528.HK) raises cannibalization risk as similar-format stores within the same mall dilute sales and lower per-store productivity; overlapping assortments also amplify vulnerability to category-specific shocks. Heavy exposure to anchors like furniture and appliances magnifies sector downturns, while curating balanced assortments across price points and styles remains operationally complex and costly.

- cannibalization risk

- anchor-category overexposure

- operational complexity in assortment balance

Credit and receivables exposure

Weaker tenants may struggle to pay rent during market softness, increasing rental concessions and vacancy risk for Red Star Macalline. Rising receivables push on working-capital and heighten bad-debt exposure, squeezing cashflow and financing flexibility. Tighter credit controls can reduce arrears but may conflict with occupancy and sales targets, forcing trade-offs between liquidity and growth.

Home-furnishing malls hit by property slump and 22.5% e‑commerce rise

Red Star Macalline (1528.HK) is cyclically tied to China's property sector (~25% of GDP), so the housing slowdown cuts mall leasing and tenant sales. E-commerce penetration reached 22.5% of retail sales in 2024, pressuring in-mall conversion without strong O2O. High recurring capex for remodels and tenant concentration in furniture/appliances raise vacancy and cashflow risk.

| Weakness | Metric | Impact |

|---|---|---|

| Property cyclicality | ~25% GDP | Lower leasing |

| E‑commerce | 22.5% (2024) | Reduced footfall |

What You See Is What You Get

Red Star Macalline Home Group SWOT Analysis

This is the actual SWOT analysis of Red Star Macalline Home Group you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You're viewing a live preview of the real file—buy now to download the complete, ready-to-use analysis.

Go Beyond the Preview—Access the Full Strategic Report

Explore Red Star Macalline Home Group’s strategic position with a concise SWOT snapshot highlighting its retail scale, supply-chain strengths, and sector risks. Want deeper, actionable insights and financial context? Purchase the full SWOT to receive a professionally written Word report and editable Excel matrix for planning and investment.

Strengths

Nationwide mall network

Red Star Macalline operates over 300 home-improvement malls across 200+ Chinese cities, giving scale advantages in centralized leasing and marketing that lower unit costs and boost bargaining power. The broad footprint attracts leading furniture and building-material brands seeking aggregated demand, while network effects enhance tenant curation and customer convenience through cross-mall promotions and standardized services.

Asset-light leasing model

Leasing space to retailers shifts inventory risk to tenants while generating recurring rental income; Red Star Macalline operates over 300 home-furnishing malls, supporting a landlord-style revenue base. This asset-light model yields more predictable cash flows versus pure retail operators, with portfolio occupancy remaining above 90% in recent periods. It frees capital for renovations, value-added services and digital tools to boost tenant productivity and footfall.

Diverse tenant mix

Diverse tenant mix across furniture, décor and building materials creates a one-stop shopping ecosystem that, as of 2024, spans 371 malls and over 30,000 brand tenants, driving cross-category traffic. Increased cross-shopping raises average dwell time and conversion for tenants, supporting higher per-visitor spend. This breadth reduces reliance on any single category’s cycle, smoothing revenue volatility for the group.

Strong brand in home furnishing

Recognition as a go-to destination for home improvement strengthens customer trust and repeat purchase behaviour, supporting Red Star Macalline's market position in 2024 and beyond. Brand equity enables premium mall locations and favourable tenant terms, and boosts participation and ROI from platform-wide promotions and events.

- Brand trust: enhances repeat purchases

- Premium sites: secures better tenant terms

- Promotions: higher conversion across platform

Value-added services ecosystem

Value-added services like design consultation and installation deepen customer engagement beyond browsing, driving reported higher conversion in mall formats versus pure e-commerce; China’s home furnishings market exceeded RMB 2 trillion in 2023, underpinning strong demand for on-site services. Service attachment raises tenant basket size and platform stickiness, differentiating malls from generic retail centers and online-only players.

- Design consultation increases conversion

- Installation ups average transaction value

- Enhances tenant retention and mall differentiation

Scale: 371 malls, 30,000+ tenants, >90% occupancy; RMB 2T home-furnishings tailwind

Scale of 371 malls and 30,000+ brand tenants (2024) drives bargaining power and cross-mall network effects. Asset-light leasing model yields recurring rental income with portfolio occupancy >90%, supporting stable cash flow. Market tailwinds: China home-furnishings market >RMB 2 trillion in 2023, enabling service upsell and higher tenant ROI.

| Metric | Value |

|---|---|

| Malls | 371 (2024) |

| Tenants | 30,000+ |

| Occupancy | >90% |

| Market size | >RMB 2 trillion (2023) |

What is included in the product

Delivers a strategic overview of Red Star Macalline Home Group’s internal strengths and weaknesses and external opportunities and threats, outlining key growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise SWOT matrix tailored to Red Star Macalline, enabling fast alignment on retail strengths and expansion risks for strategic decision-making.

Weaknesses

Exposure to China property cycle

Home-improvement demand at Red Star Macalline tracks housing transactions and renovations, so China’s property slowdown directly reduces tenant sales and leasing demand. With property-related activity historically accounting for about 25% of China’s GDP, cyclicality can materially pressure mall occupancy and rent growth. Recent market weakness has tightened cashflows for developers and retailers, amplifying downside risk to Red Star’s store-level revenues.

High dependence on offline footfall

Mall-centric traffic is exposed as global e-commerce captured 22.5% of retail sales in 2024, so shoppers increasingly start research and purchase online. Without robust O2O integration, discovery and consideration are likely to migrate to platforms, reducing in-mall conversion. Declining store sales can compress tenants’ margins and weaken renewal pricing power, risking lower rent growth and higher vacancy.

Capex needs for mall upgrades

Keeping its malls modern forces Red Star Macalline into ongoing remodeling and experience upgrades, which require significant recurring capex. Delays in refresh cycles can leave venues less competitive versus newer mixed-use and e-commerce-integrated formats. Elevated capex needs also risk compressing returns during economic downturns as investment timelines lengthen and cash flow tightens.

Tenant concentration and overlap risk

Tenant concentration at Red Star Macalline (1528.HK) raises cannibalization risk as similar-format stores within the same mall dilute sales and lower per-store productivity; overlapping assortments also amplify vulnerability to category-specific shocks. Heavy exposure to anchors like furniture and appliances magnifies sector downturns, while curating balanced assortments across price points and styles remains operationally complex and costly.

- cannibalization risk

- anchor-category overexposure

- operational complexity in assortment balance

Credit and receivables exposure

Weaker tenants may struggle to pay rent during market softness, increasing rental concessions and vacancy risk for Red Star Macalline. Rising receivables push on working-capital and heighten bad-debt exposure, squeezing cashflow and financing flexibility. Tighter credit controls can reduce arrears but may conflict with occupancy and sales targets, forcing trade-offs between liquidity and growth.

Home-furnishing malls hit by property slump and 22.5% e‑commerce rise

Red Star Macalline (1528.HK) is cyclically tied to China's property sector (~25% of GDP), so the housing slowdown cuts mall leasing and tenant sales. E-commerce penetration reached 22.5% of retail sales in 2024, pressuring in-mall conversion without strong O2O. High recurring capex for remodels and tenant concentration in furniture/appliances raise vacancy and cashflow risk.

| Weakness | Metric | Impact |

|---|---|---|

| Property cyclicality | ~25% GDP | Lower leasing |

| E‑commerce | 22.5% (2024) | Reduced footfall |

What You See Is What You Get

Red Star Macalline Home Group SWOT Analysis

This is the actual SWOT analysis of Red Star Macalline Home Group you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You're viewing a live preview of the real file—buy now to download the complete, ready-to-use analysis.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Explore Red Star Macalline Home Group’s strategic position with a concise SWOT snapshot highlighting its retail scale, supply-chain strengths, and sector risks. Want deeper, actionable insights and financial context? Purchase the full SWOT to receive a professionally written Word report and editable Excel matrix for planning and investment.

Strengths

Nationwide mall network

Red Star Macalline operates over 300 home-improvement malls across 200+ Chinese cities, giving scale advantages in centralized leasing and marketing that lower unit costs and boost bargaining power. The broad footprint attracts leading furniture and building-material brands seeking aggregated demand, while network effects enhance tenant curation and customer convenience through cross-mall promotions and standardized services.

Asset-light leasing model

Leasing space to retailers shifts inventory risk to tenants while generating recurring rental income; Red Star Macalline operates over 300 home-furnishing malls, supporting a landlord-style revenue base. This asset-light model yields more predictable cash flows versus pure retail operators, with portfolio occupancy remaining above 90% in recent periods. It frees capital for renovations, value-added services and digital tools to boost tenant productivity and footfall.

Diverse tenant mix

Diverse tenant mix across furniture, décor and building materials creates a one-stop shopping ecosystem that, as of 2024, spans 371 malls and over 30,000 brand tenants, driving cross-category traffic. Increased cross-shopping raises average dwell time and conversion for tenants, supporting higher per-visitor spend. This breadth reduces reliance on any single category’s cycle, smoothing revenue volatility for the group.

Strong brand in home furnishing

Recognition as a go-to destination for home improvement strengthens customer trust and repeat purchase behaviour, supporting Red Star Macalline's market position in 2024 and beyond. Brand equity enables premium mall locations and favourable tenant terms, and boosts participation and ROI from platform-wide promotions and events.

- Brand trust: enhances repeat purchases

- Premium sites: secures better tenant terms

- Promotions: higher conversion across platform

Value-added services ecosystem

Value-added services like design consultation and installation deepen customer engagement beyond browsing, driving reported higher conversion in mall formats versus pure e-commerce; China’s home furnishings market exceeded RMB 2 trillion in 2023, underpinning strong demand for on-site services. Service attachment raises tenant basket size and platform stickiness, differentiating malls from generic retail centers and online-only players.

- Design consultation increases conversion

- Installation ups average transaction value

- Enhances tenant retention and mall differentiation

Scale: 371 malls, 30,000+ tenants, >90% occupancy; RMB 2T home-furnishings tailwind

Scale of 371 malls and 30,000+ brand tenants (2024) drives bargaining power and cross-mall network effects. Asset-light leasing model yields recurring rental income with portfolio occupancy >90%, supporting stable cash flow. Market tailwinds: China home-furnishings market >RMB 2 trillion in 2023, enabling service upsell and higher tenant ROI.

| Metric | Value |

|---|---|

| Malls | 371 (2024) |

| Tenants | 30,000+ |

| Occupancy | >90% |

| Market size | >RMB 2 trillion (2023) |

What is included in the product

Delivers a strategic overview of Red Star Macalline Home Group’s internal strengths and weaknesses and external opportunities and threats, outlining key growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise SWOT matrix tailored to Red Star Macalline, enabling fast alignment on retail strengths and expansion risks for strategic decision-making.

Weaknesses

Exposure to China property cycle

Home-improvement demand at Red Star Macalline tracks housing transactions and renovations, so China’s property slowdown directly reduces tenant sales and leasing demand. With property-related activity historically accounting for about 25% of China’s GDP, cyclicality can materially pressure mall occupancy and rent growth. Recent market weakness has tightened cashflows for developers and retailers, amplifying downside risk to Red Star’s store-level revenues.

High dependence on offline footfall

Mall-centric traffic is exposed as global e-commerce captured 22.5% of retail sales in 2024, so shoppers increasingly start research and purchase online. Without robust O2O integration, discovery and consideration are likely to migrate to platforms, reducing in-mall conversion. Declining store sales can compress tenants’ margins and weaken renewal pricing power, risking lower rent growth and higher vacancy.

Capex needs for mall upgrades

Keeping its malls modern forces Red Star Macalline into ongoing remodeling and experience upgrades, which require significant recurring capex. Delays in refresh cycles can leave venues less competitive versus newer mixed-use and e-commerce-integrated formats. Elevated capex needs also risk compressing returns during economic downturns as investment timelines lengthen and cash flow tightens.

Tenant concentration and overlap risk

Tenant concentration at Red Star Macalline (1528.HK) raises cannibalization risk as similar-format stores within the same mall dilute sales and lower per-store productivity; overlapping assortments also amplify vulnerability to category-specific shocks. Heavy exposure to anchors like furniture and appliances magnifies sector downturns, while curating balanced assortments across price points and styles remains operationally complex and costly.

- cannibalization risk

- anchor-category overexposure

- operational complexity in assortment balance

Credit and receivables exposure

Weaker tenants may struggle to pay rent during market softness, increasing rental concessions and vacancy risk for Red Star Macalline. Rising receivables push on working-capital and heighten bad-debt exposure, squeezing cashflow and financing flexibility. Tighter credit controls can reduce arrears but may conflict with occupancy and sales targets, forcing trade-offs between liquidity and growth.

Home-furnishing malls hit by property slump and 22.5% e‑commerce rise

Red Star Macalline (1528.HK) is cyclically tied to China's property sector (~25% of GDP), so the housing slowdown cuts mall leasing and tenant sales. E-commerce penetration reached 22.5% of retail sales in 2024, pressuring in-mall conversion without strong O2O. High recurring capex for remodels and tenant concentration in furniture/appliances raise vacancy and cashflow risk.

| Weakness | Metric | Impact |

|---|---|---|

| Property cyclicality | ~25% GDP | Lower leasing |

| E‑commerce | 22.5% (2024) | Reduced footfall |

What You See Is What You Get

Red Star Macalline Home Group SWOT Analysis

This is the actual SWOT analysis of Red Star Macalline Home Group you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You're viewing a live preview of the real file—buy now to download the complete, ready-to-use analysis.