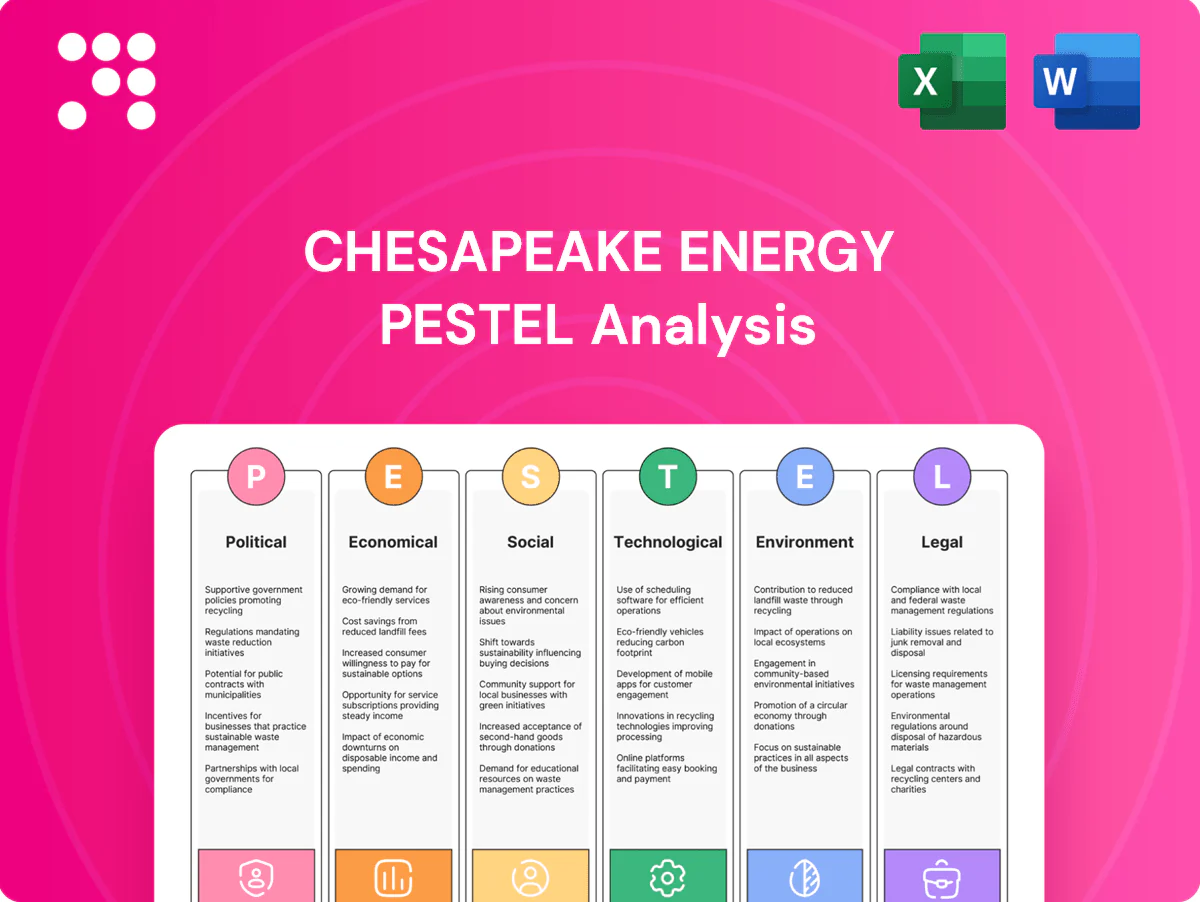

Chesapeake Energy PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, energy markets, environmental rules, and tech trends are shaping Chesapeake Energy’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full analysis to get detailed, actionable insights and ready-to-use charts for smarter decisions.

Political factors

US energy policy shifts

Shifts in US federal priorities can rapidly expand or restrict drilling and midstream access, affecting Chesapeake’s pace of development and pipeline hookups. Incentives in federal law and programs that support gas as a transition fuel underpin demand—U.S. natural gas supplied about 37% of electricity generation in 2023 (EIA). Meanwhile tighter EPA methane rules finalized in 2023–24 raise compliance costs. Chesapeake must remain agile, aligning capital plans to policy direction and regulatory timelines.

State-level permitting

Permitting timelines in states like Texas, Louisiana and Pennsylvania drive cycle times, with approvals commonly ranging from weeks to several months depending on agency workload and environmental review. County ordinances and local zoning add variability and can increase lead times for site build-out. Chesapeake’s proactive stakeholder engagement and community agreements have been shown industry-wide to reduce approval delays, often shortening timelines by as much as 20–40%.

Infrastructure and pipeline politics

Political resistance to new pipelines has tightened takeaway capacity, with Appalachian basis discounts spiking over 2.00 $/MMBtu during past constraint episodes and U.S. dry gas production near 102 Bcf/d in 2024 (EIA). Supporting modernization of existing corridors is a pragmatic path to ease basis stress and lower takeaway bottlenecks. Strategic acreage choices should prioritize locations with stable, long-term midstream routes and contracted capacity.

Royalty and severance taxes

Adjustments to state severance taxes directly compress Chesapeake Energy netbacks, increasing per-unit cost pressure and affecting capital allocation and well economics. Local royalty-owner advocacy has driven recent state debates, raising regulatory uncertainty for producers. Chesapeake must sustain targeted advocacy to preserve competitive fiscal regimes and protect margins.

Geopolitical gas dynamics

Rising US LNG export capacity (≈14 Bcf/d operational by 2025) and geopolitical tensions in Europe/Asia have shifted domestic balances, with US exports averaging roughly 11 Bcf/d in 2024, tightening supply and supporting higher upstream realizations.

- US export capacity ≈14 Bcf/d (2025)

- Avg US LNG exports ≈11 Bcf/d (2024)

- Tighter exports → stronger upstream prices

- Chesapeake materially exposed to global policy shifts

Policy, methane rules & permits delay; LNG exports 11Bcf/d tighten

Federal policy swings and EPA methane rules (2023–24) change compliance costs and project timing, affecting capital plans. State permitting variability (weeks–months) and local zoning add lead-time risks; proactive engagement can cut delays ~20–40%. Severance tax shifts compress netbacks; LNG exports (~11 Bcf/d 2024, capacity ≈14 Bcf/d 2025) tighten markets and support realizations.

| Factor | Metric | 2024/25 |

|---|---|---|

| EPA rules | Compliance timing/cost | 2023–24 finalized |

| LNG exports | Avg exports / capacity | 11 Bcf/d / ≈14 Bcf/d |

What is included in the product

Explores how macro-environmental factors affect Chesapeake Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, investors and strategists identify risks, opportunities and actionable scenario plans.

A concise, visually segmented PESTLE of Chesapeake Energy that simplifies external risk and market positioning for quick sharing in presentations, planning sessions, or client reports.

Economic factors

Gas price volatility

Henry Hub price swings remain the primary determinant of Chesapeake Energy revenue and capital allocation, with U.S. dry gas production averaging about 100 Bcf/d in 2024 (EIA) amplifying supply-driven volatility. Chesapeake uses hedging to smooth cash flows, which limits upside when spot rallies. A flexible drilling cadence lets the company scale activity to protect returns across cycles.

Service cost inflation

Pressure pumping, sand, and labor cost inflation can materially erode Chesapeake Energy margins by raising per-well service bills and shortening break-even windows. Counter-cyclical contracting and multi-year service agreements provide greater cost visibility and hedging against spot spikes. Continued focus on pad-scale operations and drilling automation delivers operational efficiency that offsets some inflationary pressure. Management cites service-contracting as a key margin defense.

Capital discipline focus

Investor demand for free cash flow and shareholder returns forces Chesapeake to prioritize distributions over aggressive capex, with management publicly citing return-of-capital as primary capital-allocation objective. The company emphasizes buybacks and dividends instead of growth-at-all-costs, reallocating cash to repurchases and payouts. New projects must meet elevated return thresholds before funding, tightening capital deployment and pushing shorter payback timelines.

Basis and transportation

Basis differentials versus Henry Hub directly lower Chesapeake’s realized gas prices; Henry Hub averaged about $2.80/MMBtu in 2024, with Gulf and Permian bases often trading at $0.30–$0.80/MMBtu discounts. Firm transport and market optionality (coverage on key routes) mitigate those discounts and stabilize receipts. Balancing production across Appalachia, Haynesville and other basins reduces exposure to localized pipeline bottlenecks.

- Basis vs HH: -$0.30–$0.80/MMBtu

- HH 2024 avg: $2.80/MMBtu

- Firm transport: majority coverage

- Portfolio: multi-basin diversification

LNG and petrochem demand

Rising global LNG capacity (about 480 mtpa in 2024) and 100+ mtpa of projects under construction to 2030, alongside petrochemical feedstock growth (ethylene demand ~3.5% CAGR), underpin medium-term US gas fundamentals. Long-dated demand visibility supports capex and inventory delineation decisions today. Chesapeake can align marketing to premium coastal markets, where export-basis and Northeast premiums averaged $1–3/MMBtu in 2024.

- 480 mtpa global LNG capacity (2024)

- 100+ mtpa projects to 2030

- ~3.5% ethylene demand CAGR

- $1–3/MMBtu coastal premiums (2024)

Policy, methane rules & permits delay; LNG exports 11Bcf/d tighten

Henry Hub price swings (HH 2024 avg $2.80/MMBtu) and basis discounts (-$0.30–$0.80/MMBtu) drive revenue and capex timing; hedging smooths cash flow but caps upside. Inflation in services and labor elevates per-well costs; pad-scale ops and multi-year contracts limit margin erosion. Global LNG (≈480 mtpa 2024; 100+ mtpa projects to 2030) and coastal premiums ($1–$3/MMBtu) support medium-term demand.

| Metric | Value/Note |

|---|---|

| Henry Hub 2024 avg | $2.80/MMBtu |

| Basis vs HH | -$0.30–$0.80/MMBtu |

| Global LNG capacity 2024 | ≈480 mtpa |

| Projects to 2030 | 100+ mtpa |

| Coastal premium 2024 | $1–$3/MMBtu |

What You See Is What You Get

Chesapeake Energy PESTLE Analysis

The Chesapeake Energy PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides a complete, professional assessment of political, economic, social, technological, legal, and environmental factors affecting Chesapeake Energy. No placeholders or teasers—this is the final file you’ll download immediately after checkout.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, energy markets, environmental rules, and tech trends are shaping Chesapeake Energy’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full analysis to get detailed, actionable insights and ready-to-use charts for smarter decisions.

Political factors

US energy policy shifts

Shifts in US federal priorities can rapidly expand or restrict drilling and midstream access, affecting Chesapeake’s pace of development and pipeline hookups. Incentives in federal law and programs that support gas as a transition fuel underpin demand—U.S. natural gas supplied about 37% of electricity generation in 2023 (EIA). Meanwhile tighter EPA methane rules finalized in 2023–24 raise compliance costs. Chesapeake must remain agile, aligning capital plans to policy direction and regulatory timelines.

State-level permitting

Permitting timelines in states like Texas, Louisiana and Pennsylvania drive cycle times, with approvals commonly ranging from weeks to several months depending on agency workload and environmental review. County ordinances and local zoning add variability and can increase lead times for site build-out. Chesapeake’s proactive stakeholder engagement and community agreements have been shown industry-wide to reduce approval delays, often shortening timelines by as much as 20–40%.

Infrastructure and pipeline politics

Political resistance to new pipelines has tightened takeaway capacity, with Appalachian basis discounts spiking over 2.00 $/MMBtu during past constraint episodes and U.S. dry gas production near 102 Bcf/d in 2024 (EIA). Supporting modernization of existing corridors is a pragmatic path to ease basis stress and lower takeaway bottlenecks. Strategic acreage choices should prioritize locations with stable, long-term midstream routes and contracted capacity.

Royalty and severance taxes

Adjustments to state severance taxes directly compress Chesapeake Energy netbacks, increasing per-unit cost pressure and affecting capital allocation and well economics. Local royalty-owner advocacy has driven recent state debates, raising regulatory uncertainty for producers. Chesapeake must sustain targeted advocacy to preserve competitive fiscal regimes and protect margins.

Geopolitical gas dynamics

Rising US LNG export capacity (≈14 Bcf/d operational by 2025) and geopolitical tensions in Europe/Asia have shifted domestic balances, with US exports averaging roughly 11 Bcf/d in 2024, tightening supply and supporting higher upstream realizations.

- US export capacity ≈14 Bcf/d (2025)

- Avg US LNG exports ≈11 Bcf/d (2024)

- Tighter exports → stronger upstream prices

- Chesapeake materially exposed to global policy shifts

Policy, methane rules & permits delay; LNG exports 11Bcf/d tighten

Federal policy swings and EPA methane rules (2023–24) change compliance costs and project timing, affecting capital plans. State permitting variability (weeks–months) and local zoning add lead-time risks; proactive engagement can cut delays ~20–40%. Severance tax shifts compress netbacks; LNG exports (~11 Bcf/d 2024, capacity ≈14 Bcf/d 2025) tighten markets and support realizations.

| Factor | Metric | 2024/25 |

|---|---|---|

| EPA rules | Compliance timing/cost | 2023–24 finalized |

| LNG exports | Avg exports / capacity | 11 Bcf/d / ≈14 Bcf/d |

What is included in the product

Explores how macro-environmental factors affect Chesapeake Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, investors and strategists identify risks, opportunities and actionable scenario plans.

A concise, visually segmented PESTLE of Chesapeake Energy that simplifies external risk and market positioning for quick sharing in presentations, planning sessions, or client reports.

Economic factors

Gas price volatility

Henry Hub price swings remain the primary determinant of Chesapeake Energy revenue and capital allocation, with U.S. dry gas production averaging about 100 Bcf/d in 2024 (EIA) amplifying supply-driven volatility. Chesapeake uses hedging to smooth cash flows, which limits upside when spot rallies. A flexible drilling cadence lets the company scale activity to protect returns across cycles.

Service cost inflation

Pressure pumping, sand, and labor cost inflation can materially erode Chesapeake Energy margins by raising per-well service bills and shortening break-even windows. Counter-cyclical contracting and multi-year service agreements provide greater cost visibility and hedging against spot spikes. Continued focus on pad-scale operations and drilling automation delivers operational efficiency that offsets some inflationary pressure. Management cites service-contracting as a key margin defense.

Capital discipline focus

Investor demand for free cash flow and shareholder returns forces Chesapeake to prioritize distributions over aggressive capex, with management publicly citing return-of-capital as primary capital-allocation objective. The company emphasizes buybacks and dividends instead of growth-at-all-costs, reallocating cash to repurchases and payouts. New projects must meet elevated return thresholds before funding, tightening capital deployment and pushing shorter payback timelines.

Basis and transportation

Basis differentials versus Henry Hub directly lower Chesapeake’s realized gas prices; Henry Hub averaged about $2.80/MMBtu in 2024, with Gulf and Permian bases often trading at $0.30–$0.80/MMBtu discounts. Firm transport and market optionality (coverage on key routes) mitigate those discounts and stabilize receipts. Balancing production across Appalachia, Haynesville and other basins reduces exposure to localized pipeline bottlenecks.

- Basis vs HH: -$0.30–$0.80/MMBtu

- HH 2024 avg: $2.80/MMBtu

- Firm transport: majority coverage

- Portfolio: multi-basin diversification

LNG and petrochem demand

Rising global LNG capacity (about 480 mtpa in 2024) and 100+ mtpa of projects under construction to 2030, alongside petrochemical feedstock growth (ethylene demand ~3.5% CAGR), underpin medium-term US gas fundamentals. Long-dated demand visibility supports capex and inventory delineation decisions today. Chesapeake can align marketing to premium coastal markets, where export-basis and Northeast premiums averaged $1–3/MMBtu in 2024.

- 480 mtpa global LNG capacity (2024)

- 100+ mtpa projects to 2030

- ~3.5% ethylene demand CAGR

- $1–3/MMBtu coastal premiums (2024)

Policy, methane rules & permits delay; LNG exports 11Bcf/d tighten

Henry Hub price swings (HH 2024 avg $2.80/MMBtu) and basis discounts (-$0.30–$0.80/MMBtu) drive revenue and capex timing; hedging smooths cash flow but caps upside. Inflation in services and labor elevates per-well costs; pad-scale ops and multi-year contracts limit margin erosion. Global LNG (≈480 mtpa 2024; 100+ mtpa projects to 2030) and coastal premiums ($1–$3/MMBtu) support medium-term demand.

| Metric | Value/Note |

|---|---|

| Henry Hub 2024 avg | $2.80/MMBtu |

| Basis vs HH | -$0.30–$0.80/MMBtu |

| Global LNG capacity 2024 | ≈480 mtpa |

| Projects to 2030 | 100+ mtpa |

| Coastal premium 2024 | $1–$3/MMBtu |

What You See Is What You Get

Chesapeake Energy PESTLE Analysis

The Chesapeake Energy PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides a complete, professional assessment of political, economic, social, technological, legal, and environmental factors affecting Chesapeake Energy. No placeholders or teasers—this is the final file you’ll download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, energy markets, environmental rules, and tech trends are shaping Chesapeake Energy’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full analysis to get detailed, actionable insights and ready-to-use charts for smarter decisions.

Political factors

US energy policy shifts

Shifts in US federal priorities can rapidly expand or restrict drilling and midstream access, affecting Chesapeake’s pace of development and pipeline hookups. Incentives in federal law and programs that support gas as a transition fuel underpin demand—U.S. natural gas supplied about 37% of electricity generation in 2023 (EIA). Meanwhile tighter EPA methane rules finalized in 2023–24 raise compliance costs. Chesapeake must remain agile, aligning capital plans to policy direction and regulatory timelines.

State-level permitting

Permitting timelines in states like Texas, Louisiana and Pennsylvania drive cycle times, with approvals commonly ranging from weeks to several months depending on agency workload and environmental review. County ordinances and local zoning add variability and can increase lead times for site build-out. Chesapeake’s proactive stakeholder engagement and community agreements have been shown industry-wide to reduce approval delays, often shortening timelines by as much as 20–40%.

Infrastructure and pipeline politics

Political resistance to new pipelines has tightened takeaway capacity, with Appalachian basis discounts spiking over 2.00 $/MMBtu during past constraint episodes and U.S. dry gas production near 102 Bcf/d in 2024 (EIA). Supporting modernization of existing corridors is a pragmatic path to ease basis stress and lower takeaway bottlenecks. Strategic acreage choices should prioritize locations with stable, long-term midstream routes and contracted capacity.

Royalty and severance taxes

Adjustments to state severance taxes directly compress Chesapeake Energy netbacks, increasing per-unit cost pressure and affecting capital allocation and well economics. Local royalty-owner advocacy has driven recent state debates, raising regulatory uncertainty for producers. Chesapeake must sustain targeted advocacy to preserve competitive fiscal regimes and protect margins.

Geopolitical gas dynamics

Rising US LNG export capacity (≈14 Bcf/d operational by 2025) and geopolitical tensions in Europe/Asia have shifted domestic balances, with US exports averaging roughly 11 Bcf/d in 2024, tightening supply and supporting higher upstream realizations.

- US export capacity ≈14 Bcf/d (2025)

- Avg US LNG exports ≈11 Bcf/d (2024)

- Tighter exports → stronger upstream prices

- Chesapeake materially exposed to global policy shifts

Policy, methane rules & permits delay; LNG exports 11Bcf/d tighten

Federal policy swings and EPA methane rules (2023–24) change compliance costs and project timing, affecting capital plans. State permitting variability (weeks–months) and local zoning add lead-time risks; proactive engagement can cut delays ~20–40%. Severance tax shifts compress netbacks; LNG exports (~11 Bcf/d 2024, capacity ≈14 Bcf/d 2025) tighten markets and support realizations.

| Factor | Metric | 2024/25 |

|---|---|---|

| EPA rules | Compliance timing/cost | 2023–24 finalized |

| LNG exports | Avg exports / capacity | 11 Bcf/d / ≈14 Bcf/d |

What is included in the product

Explores how macro-environmental factors affect Chesapeake Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, investors and strategists identify risks, opportunities and actionable scenario plans.

A concise, visually segmented PESTLE of Chesapeake Energy that simplifies external risk and market positioning for quick sharing in presentations, planning sessions, or client reports.

Economic factors

Gas price volatility

Henry Hub price swings remain the primary determinant of Chesapeake Energy revenue and capital allocation, with U.S. dry gas production averaging about 100 Bcf/d in 2024 (EIA) amplifying supply-driven volatility. Chesapeake uses hedging to smooth cash flows, which limits upside when spot rallies. A flexible drilling cadence lets the company scale activity to protect returns across cycles.

Service cost inflation

Pressure pumping, sand, and labor cost inflation can materially erode Chesapeake Energy margins by raising per-well service bills and shortening break-even windows. Counter-cyclical contracting and multi-year service agreements provide greater cost visibility and hedging against spot spikes. Continued focus on pad-scale operations and drilling automation delivers operational efficiency that offsets some inflationary pressure. Management cites service-contracting as a key margin defense.

Capital discipline focus

Investor demand for free cash flow and shareholder returns forces Chesapeake to prioritize distributions over aggressive capex, with management publicly citing return-of-capital as primary capital-allocation objective. The company emphasizes buybacks and dividends instead of growth-at-all-costs, reallocating cash to repurchases and payouts. New projects must meet elevated return thresholds before funding, tightening capital deployment and pushing shorter payback timelines.

Basis and transportation

Basis differentials versus Henry Hub directly lower Chesapeake’s realized gas prices; Henry Hub averaged about $2.80/MMBtu in 2024, with Gulf and Permian bases often trading at $0.30–$0.80/MMBtu discounts. Firm transport and market optionality (coverage on key routes) mitigate those discounts and stabilize receipts. Balancing production across Appalachia, Haynesville and other basins reduces exposure to localized pipeline bottlenecks.

- Basis vs HH: -$0.30–$0.80/MMBtu

- HH 2024 avg: $2.80/MMBtu

- Firm transport: majority coverage

- Portfolio: multi-basin diversification

LNG and petrochem demand

Rising global LNG capacity (about 480 mtpa in 2024) and 100+ mtpa of projects under construction to 2030, alongside petrochemical feedstock growth (ethylene demand ~3.5% CAGR), underpin medium-term US gas fundamentals. Long-dated demand visibility supports capex and inventory delineation decisions today. Chesapeake can align marketing to premium coastal markets, where export-basis and Northeast premiums averaged $1–3/MMBtu in 2024.

- 480 mtpa global LNG capacity (2024)

- 100+ mtpa projects to 2030

- ~3.5% ethylene demand CAGR

- $1–3/MMBtu coastal premiums (2024)

Policy, methane rules & permits delay; LNG exports 11Bcf/d tighten

Henry Hub price swings (HH 2024 avg $2.80/MMBtu) and basis discounts (-$0.30–$0.80/MMBtu) drive revenue and capex timing; hedging smooths cash flow but caps upside. Inflation in services and labor elevates per-well costs; pad-scale ops and multi-year contracts limit margin erosion. Global LNG (≈480 mtpa 2024; 100+ mtpa projects to 2030) and coastal premiums ($1–$3/MMBtu) support medium-term demand.

| Metric | Value/Note |

|---|---|

| Henry Hub 2024 avg | $2.80/MMBtu |

| Basis vs HH | -$0.30–$0.80/MMBtu |

| Global LNG capacity 2024 | ≈480 mtpa |

| Projects to 2030 | 100+ mtpa |

| Coastal premium 2024 | $1–$3/MMBtu |

What You See Is What You Get

Chesapeake Energy PESTLE Analysis

The Chesapeake Energy PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides a complete, professional assessment of political, economic, social, technological, legal, and environmental factors affecting Chesapeake Energy. No placeholders or teasers—this is the final file you’ll download immediately after checkout.