Chobani Porter's Five Forces Analysis

From Overview to Strategy Blueprint

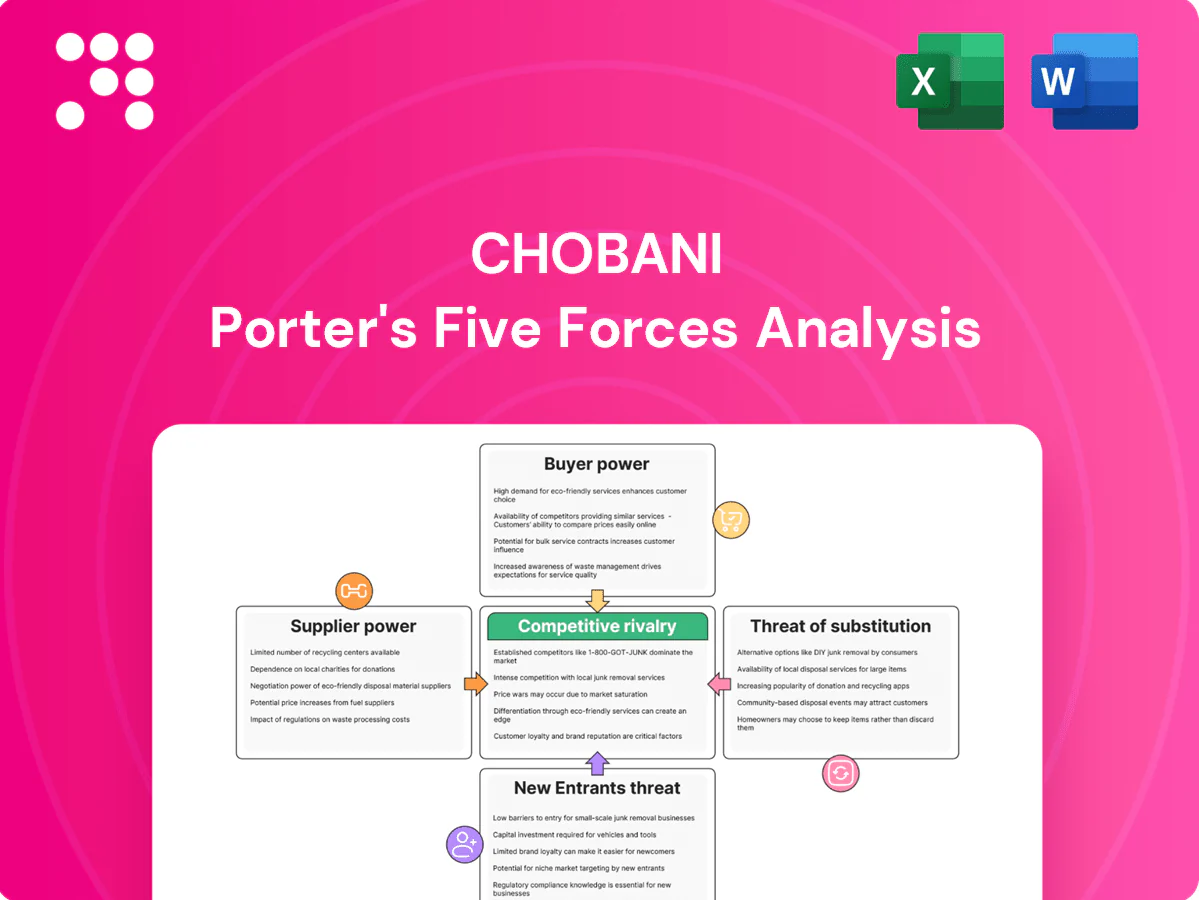

Chobani faces intense supplier negotiation for dairy inputs, significant buyer power from retail giants, and moderate threat from new entrants due to brand loyalty and scale. Private-label yogurts and alternative proteins elevate substitute pressure while rivalry among established dairy brands remains high. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Chobani’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dairy input concentration

Milk, Chobani’s core input, is sourced from regional farms and co-ops whose consolidation gives suppliers moderate leverage; USDA data show US milk production around 229 billion pounds in 2024, while feed and herd-cycle volatility drove spot price swings that tightened supply. Long-term contracts mitigate risk, but strict quality and animal-welfare standards shrink the eligible supplier pool, concentrating bargaining power.

Specialty ingredients

Specialty fruit purees, cultures and stabilizers come from a narrow set of global suppliers, and in 2024 industry reports showed growing demand for certified clean-label inputs that further concentrates qualified vendors. Limited options raise switching costs and make Chobani vulnerable to harvest variability or supplier disruption, which can push input costs higher. Chobani’s scale and multi-site production provide mitigation, but supplier leverage remains balanced rather than tilted in Chobani’s favor.

Packaging and cold chain

Cups, lids and sustainable substrates remain concentrated categories with regional capacity constraints, giving suppliers leverage; global PET and fiber converters saw 2024 spot price volatility near ±20%, transmitting costs to buyers. Resin and paper price swings amplified supplier pressure on COGS. Cold‑chain providers held pricing power during tight freight windows—reefer rates and capacity spikes in 2024 tightened margins. Multi‑sourcing lowers but does not remove supplier leverage.

Oats and alt-dairy inputs

Oat milk and creamers depend on steady oat, oil and enzyme supplies; global oat production was about 24 million tonnes in 2023 (FAO), so adverse weather or commodity cycles can tighten availability and spike input costs. A limited set of processors that meet clean‑label and non‑GMO specs raises dependence, keeping supplier power at a moderate level for Chobani.

- Inputs: oats, oil, enzymes

- Global oats ~24M t (2023, FAO)

- Fewer clean‑label processors → moderate supplier power

Co-manufacturing flexibility

Selective use of co-packers for innovation or peak demand adds capacity but creates dependence; as of 2024 qualified co-packers for cultured dairy and aseptic lines remain limited, concentrating supplier leverage. Contract terms, minimum runs and quality oversight give co-packers bargaining power, though Chobani’s growing in-house scale and capital investment reduce that dependence over time.

- dependence: concentrated co-packer base (2024)

- leverage: contract minimums & quality oversight

- offset: expanding in-house capacity

Milk tightness, oat limits and ±20% packaging volatility squeeze dairy processors

Milk sourcing concentration and strict quality standards give suppliers moderate leverage; US milk production ~229 billion lb (2024) but price volatility tightened supply. Specialty inputs and co-packers remain limited, raising switching costs; global oats ~24M t (2023). Packaging resin/paper and cold‑chain saw ~±20% spot volatility in 2024, transmitting cost pressure to Chobani.

| Input | 2023/24 |

|---|---|

| US milk | ~229B lb (2024) |

| Oats | ~24M t (2023) |

| PET/paper volatility | ~±20% (2024) |

What is included in the product

Uncovers how competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes shape Chobani's pricing, margins, and growth prospects, highlighting disruptive forces and barriers that protect or threaten its market position.

A concise Porter's Five Forces snapshot for Chobani that quickly identifies supplier, buyer and competitive pain points—ideal for pinpointing immediate strategic fixes; ready to drop into decks or iterate with your own data.

Customers Bargaining Power

Retailer concentration

Large grocers and club stores dominate shelf access—Walmart controls roughly 25% of US grocery sales and Kroger about 11%, while Costco reported $267B revenue in FY2024—giving buyers pricing power. Slotting fees (commonly $25,000–$250,000 per SKU) and category captaincy raise barriers and leverage. Rising private label share (~19% of US grocery) intensifies pressure. Chobani’s ~ $1.6B revenue brand helps, but retail buyers stay powerful.

Price sensitivity

Yogurt is a frequent promotion category with promotions driving roughly 40% of retail unit sales, creating elastic demand. Shoppers routinely trade across brands and pack sizes to chase deals, with retailers reporting up to 60% promotional switch. Economic pressure in 2024 increased value focus, and buyers pressure suppliers for EDLP and promo funding to protect volumes.

Switching ease

Low switching costs between chilled yogurt, plant-based options and creamers mean consumers can swap brands quickly; Chobani held roughly 11% of US retail yogurt sales in 2023–24, while plant-based alternatives grew double digits in 2023. Comparable taste profiles and formats accelerate churn, making loyalty present but not absolute. Retailers, where private-label penetration approaches 20%, leverage this to demand better terms.

Data and private label

Retailers leverage granular POS and category insights to drive tougher 2024 negotiations, using scan data to quantify SKU velocity, margin and space elasticity; strong private-label programs (private label ~18% of US grocery sales in 2024) create credible, lower-cost alternatives and allow buyers to reallocate shelf space if vendors resist, forcing Chobani to prove premium pricing through measurable performance.

- POS-driven leverage

- Private label ~18% (2024)

- Space shift risk

- Must justify premium with ROI

Channel diversification

Channel diversification—foodservice, convenience, and e-commerce—erodes some retailer bargaining power; U.S. online grocery penetration reached about 8% in 2024, giving alternative shelf space and promotional levers. Direct-to-consumer remains a low-single-digit share for Chobani but serves as an R&D and innovation lab. Despite gains, grocery chains remain the dominant gatekeepers of shelf access and promotions.

- Foodservice/convenience/e‑commerce reduce buyer concentration

- D2C = innovation channel, limited share (low single digits, 2024)

- Online grocery ≈ 8% (2024)

- Grocery retailers still primary gatekeepers

Retail giants' pricing power forces yogurt makers to subsidize promos despite scale gains

Large grocers (Walmart ~25%, Kroger ~11%) and Costco ($267B FY2024) exert strong pricing/placement power; private label ~18–19% (2024) and promotions (~40% of unit sales) pressure margins. Chobani (~$1.6B, ~11% yogurt share 2023–24) benefits from scale but must fund promotions and prove ROI. Channel diversification (online ~8% 2024, DTC low-single-digits) reduces but does not eliminate buyer leverage.

| Metric | 2023–24 |

|---|---|

| Walmart share | ~25% |

| Kroger | ~11% |

| Costco revenue | $267B |

| Private label | ~18–19% |

| Promotions impact | ~40% units |

| Chobani revenue | ~$1.6B |

| Chobani share | ~11% |

| Online grocery | ~8% |

Full Version Awaits

Chobani Porter's Five Forces Analysis

This preview shows the exact Chobani Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, ready for download, and covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, plus actionable strategic insights. What you see is what you get.

From Overview to Strategy Blueprint

Chobani faces intense supplier negotiation for dairy inputs, significant buyer power from retail giants, and moderate threat from new entrants due to brand loyalty and scale. Private-label yogurts and alternative proteins elevate substitute pressure while rivalry among established dairy brands remains high. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Chobani’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dairy input concentration

Milk, Chobani’s core input, is sourced from regional farms and co-ops whose consolidation gives suppliers moderate leverage; USDA data show US milk production around 229 billion pounds in 2024, while feed and herd-cycle volatility drove spot price swings that tightened supply. Long-term contracts mitigate risk, but strict quality and animal-welfare standards shrink the eligible supplier pool, concentrating bargaining power.

Specialty ingredients

Specialty fruit purees, cultures and stabilizers come from a narrow set of global suppliers, and in 2024 industry reports showed growing demand for certified clean-label inputs that further concentrates qualified vendors. Limited options raise switching costs and make Chobani vulnerable to harvest variability or supplier disruption, which can push input costs higher. Chobani’s scale and multi-site production provide mitigation, but supplier leverage remains balanced rather than tilted in Chobani’s favor.

Packaging and cold chain

Cups, lids and sustainable substrates remain concentrated categories with regional capacity constraints, giving suppliers leverage; global PET and fiber converters saw 2024 spot price volatility near ±20%, transmitting costs to buyers. Resin and paper price swings amplified supplier pressure on COGS. Cold‑chain providers held pricing power during tight freight windows—reefer rates and capacity spikes in 2024 tightened margins. Multi‑sourcing lowers but does not remove supplier leverage.

Oats and alt-dairy inputs

Oat milk and creamers depend on steady oat, oil and enzyme supplies; global oat production was about 24 million tonnes in 2023 (FAO), so adverse weather or commodity cycles can tighten availability and spike input costs. A limited set of processors that meet clean‑label and non‑GMO specs raises dependence, keeping supplier power at a moderate level for Chobani.

- Inputs: oats, oil, enzymes

- Global oats ~24M t (2023, FAO)

- Fewer clean‑label processors → moderate supplier power

Co-manufacturing flexibility

Selective use of co-packers for innovation or peak demand adds capacity but creates dependence; as of 2024 qualified co-packers for cultured dairy and aseptic lines remain limited, concentrating supplier leverage. Contract terms, minimum runs and quality oversight give co-packers bargaining power, though Chobani’s growing in-house scale and capital investment reduce that dependence over time.

- dependence: concentrated co-packer base (2024)

- leverage: contract minimums & quality oversight

- offset: expanding in-house capacity

Milk tightness, oat limits and ±20% packaging volatility squeeze dairy processors

Milk sourcing concentration and strict quality standards give suppliers moderate leverage; US milk production ~229 billion lb (2024) but price volatility tightened supply. Specialty inputs and co-packers remain limited, raising switching costs; global oats ~24M t (2023). Packaging resin/paper and cold‑chain saw ~±20% spot volatility in 2024, transmitting cost pressure to Chobani.

| Input | 2023/24 |

|---|---|

| US milk | ~229B lb (2024) |

| Oats | ~24M t (2023) |

| PET/paper volatility | ~±20% (2024) |

What is included in the product

Uncovers how competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes shape Chobani's pricing, margins, and growth prospects, highlighting disruptive forces and barriers that protect or threaten its market position.

A concise Porter's Five Forces snapshot for Chobani that quickly identifies supplier, buyer and competitive pain points—ideal for pinpointing immediate strategic fixes; ready to drop into decks or iterate with your own data.

Customers Bargaining Power

Retailer concentration

Large grocers and club stores dominate shelf access—Walmart controls roughly 25% of US grocery sales and Kroger about 11%, while Costco reported $267B revenue in FY2024—giving buyers pricing power. Slotting fees (commonly $25,000–$250,000 per SKU) and category captaincy raise barriers and leverage. Rising private label share (~19% of US grocery) intensifies pressure. Chobani’s ~ $1.6B revenue brand helps, but retail buyers stay powerful.

Price sensitivity

Yogurt is a frequent promotion category with promotions driving roughly 40% of retail unit sales, creating elastic demand. Shoppers routinely trade across brands and pack sizes to chase deals, with retailers reporting up to 60% promotional switch. Economic pressure in 2024 increased value focus, and buyers pressure suppliers for EDLP and promo funding to protect volumes.

Switching ease

Low switching costs between chilled yogurt, plant-based options and creamers mean consumers can swap brands quickly; Chobani held roughly 11% of US retail yogurt sales in 2023–24, while plant-based alternatives grew double digits in 2023. Comparable taste profiles and formats accelerate churn, making loyalty present but not absolute. Retailers, where private-label penetration approaches 20%, leverage this to demand better terms.

Data and private label

Retailers leverage granular POS and category insights to drive tougher 2024 negotiations, using scan data to quantify SKU velocity, margin and space elasticity; strong private-label programs (private label ~18% of US grocery sales in 2024) create credible, lower-cost alternatives and allow buyers to reallocate shelf space if vendors resist, forcing Chobani to prove premium pricing through measurable performance.

- POS-driven leverage

- Private label ~18% (2024)

- Space shift risk

- Must justify premium with ROI

Channel diversification

Channel diversification—foodservice, convenience, and e-commerce—erodes some retailer bargaining power; U.S. online grocery penetration reached about 8% in 2024, giving alternative shelf space and promotional levers. Direct-to-consumer remains a low-single-digit share for Chobani but serves as an R&D and innovation lab. Despite gains, grocery chains remain the dominant gatekeepers of shelf access and promotions.

- Foodservice/convenience/e‑commerce reduce buyer concentration

- D2C = innovation channel, limited share (low single digits, 2024)

- Online grocery ≈ 8% (2024)

- Grocery retailers still primary gatekeepers

Retail giants' pricing power forces yogurt makers to subsidize promos despite scale gains

Large grocers (Walmart ~25%, Kroger ~11%) and Costco ($267B FY2024) exert strong pricing/placement power; private label ~18–19% (2024) and promotions (~40% of unit sales) pressure margins. Chobani (~$1.6B, ~11% yogurt share 2023–24) benefits from scale but must fund promotions and prove ROI. Channel diversification (online ~8% 2024, DTC low-single-digits) reduces but does not eliminate buyer leverage.

| Metric | 2023–24 |

|---|---|

| Walmart share | ~25% |

| Kroger | ~11% |

| Costco revenue | $267B |

| Private label | ~18–19% |

| Promotions impact | ~40% units |

| Chobani revenue | ~$1.6B |

| Chobani share | ~11% |

| Online grocery | ~8% |

Full Version Awaits

Chobani Porter's Five Forces Analysis

This preview shows the exact Chobani Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, ready for download, and covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, plus actionable strategic insights. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Chobani faces intense supplier negotiation for dairy inputs, significant buyer power from retail giants, and moderate threat from new entrants due to brand loyalty and scale. Private-label yogurts and alternative proteins elevate substitute pressure while rivalry among established dairy brands remains high. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Chobani’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dairy input concentration

Milk, Chobani’s core input, is sourced from regional farms and co-ops whose consolidation gives suppliers moderate leverage; USDA data show US milk production around 229 billion pounds in 2024, while feed and herd-cycle volatility drove spot price swings that tightened supply. Long-term contracts mitigate risk, but strict quality and animal-welfare standards shrink the eligible supplier pool, concentrating bargaining power.

Specialty ingredients

Specialty fruit purees, cultures and stabilizers come from a narrow set of global suppliers, and in 2024 industry reports showed growing demand for certified clean-label inputs that further concentrates qualified vendors. Limited options raise switching costs and make Chobani vulnerable to harvest variability or supplier disruption, which can push input costs higher. Chobani’s scale and multi-site production provide mitigation, but supplier leverage remains balanced rather than tilted in Chobani’s favor.

Packaging and cold chain

Cups, lids and sustainable substrates remain concentrated categories with regional capacity constraints, giving suppliers leverage; global PET and fiber converters saw 2024 spot price volatility near ±20%, transmitting costs to buyers. Resin and paper price swings amplified supplier pressure on COGS. Cold‑chain providers held pricing power during tight freight windows—reefer rates and capacity spikes in 2024 tightened margins. Multi‑sourcing lowers but does not remove supplier leverage.

Oats and alt-dairy inputs

Oat milk and creamers depend on steady oat, oil and enzyme supplies; global oat production was about 24 million tonnes in 2023 (FAO), so adverse weather or commodity cycles can tighten availability and spike input costs. A limited set of processors that meet clean‑label and non‑GMO specs raises dependence, keeping supplier power at a moderate level for Chobani.

- Inputs: oats, oil, enzymes

- Global oats ~24M t (2023, FAO)

- Fewer clean‑label processors → moderate supplier power

Co-manufacturing flexibility

Selective use of co-packers for innovation or peak demand adds capacity but creates dependence; as of 2024 qualified co-packers for cultured dairy and aseptic lines remain limited, concentrating supplier leverage. Contract terms, minimum runs and quality oversight give co-packers bargaining power, though Chobani’s growing in-house scale and capital investment reduce that dependence over time.

- dependence: concentrated co-packer base (2024)

- leverage: contract minimums & quality oversight

- offset: expanding in-house capacity

Milk tightness, oat limits and ±20% packaging volatility squeeze dairy processors

Milk sourcing concentration and strict quality standards give suppliers moderate leverage; US milk production ~229 billion lb (2024) but price volatility tightened supply. Specialty inputs and co-packers remain limited, raising switching costs; global oats ~24M t (2023). Packaging resin/paper and cold‑chain saw ~±20% spot volatility in 2024, transmitting cost pressure to Chobani.

| Input | 2023/24 |

|---|---|

| US milk | ~229B lb (2024) |

| Oats | ~24M t (2023) |

| PET/paper volatility | ~±20% (2024) |

What is included in the product

Uncovers how competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes shape Chobani's pricing, margins, and growth prospects, highlighting disruptive forces and barriers that protect or threaten its market position.

A concise Porter's Five Forces snapshot for Chobani that quickly identifies supplier, buyer and competitive pain points—ideal for pinpointing immediate strategic fixes; ready to drop into decks or iterate with your own data.

Customers Bargaining Power

Retailer concentration

Large grocers and club stores dominate shelf access—Walmart controls roughly 25% of US grocery sales and Kroger about 11%, while Costco reported $267B revenue in FY2024—giving buyers pricing power. Slotting fees (commonly $25,000–$250,000 per SKU) and category captaincy raise barriers and leverage. Rising private label share (~19% of US grocery) intensifies pressure. Chobani’s ~ $1.6B revenue brand helps, but retail buyers stay powerful.

Price sensitivity

Yogurt is a frequent promotion category with promotions driving roughly 40% of retail unit sales, creating elastic demand. Shoppers routinely trade across brands and pack sizes to chase deals, with retailers reporting up to 60% promotional switch. Economic pressure in 2024 increased value focus, and buyers pressure suppliers for EDLP and promo funding to protect volumes.

Switching ease

Low switching costs between chilled yogurt, plant-based options and creamers mean consumers can swap brands quickly; Chobani held roughly 11% of US retail yogurt sales in 2023–24, while plant-based alternatives grew double digits in 2023. Comparable taste profiles and formats accelerate churn, making loyalty present but not absolute. Retailers, where private-label penetration approaches 20%, leverage this to demand better terms.

Data and private label

Retailers leverage granular POS and category insights to drive tougher 2024 negotiations, using scan data to quantify SKU velocity, margin and space elasticity; strong private-label programs (private label ~18% of US grocery sales in 2024) create credible, lower-cost alternatives and allow buyers to reallocate shelf space if vendors resist, forcing Chobani to prove premium pricing through measurable performance.

- POS-driven leverage

- Private label ~18% (2024)

- Space shift risk

- Must justify premium with ROI

Channel diversification

Channel diversification—foodservice, convenience, and e-commerce—erodes some retailer bargaining power; U.S. online grocery penetration reached about 8% in 2024, giving alternative shelf space and promotional levers. Direct-to-consumer remains a low-single-digit share for Chobani but serves as an R&D and innovation lab. Despite gains, grocery chains remain the dominant gatekeepers of shelf access and promotions.

- Foodservice/convenience/e‑commerce reduce buyer concentration

- D2C = innovation channel, limited share (low single digits, 2024)

- Online grocery ≈ 8% (2024)

- Grocery retailers still primary gatekeepers

Retail giants' pricing power forces yogurt makers to subsidize promos despite scale gains

Large grocers (Walmart ~25%, Kroger ~11%) and Costco ($267B FY2024) exert strong pricing/placement power; private label ~18–19% (2024) and promotions (~40% of unit sales) pressure margins. Chobani (~$1.6B, ~11% yogurt share 2023–24) benefits from scale but must fund promotions and prove ROI. Channel diversification (online ~8% 2024, DTC low-single-digits) reduces but does not eliminate buyer leverage.

| Metric | 2023–24 |

|---|---|

| Walmart share | ~25% |

| Kroger | ~11% |

| Costco revenue | $267B |

| Private label | ~18–19% |

| Promotions impact | ~40% units |

| Chobani revenue | ~$1.6B |

| Chobani share | ~11% |

| Online grocery | ~8% |

Full Version Awaits

Chobani Porter's Five Forces Analysis

This preview shows the exact Chobani Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, ready for download, and covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, plus actionable strategic insights. What you see is what you get.