Chord Energy Boston Consulting Group Matrix

Actionable Strategy Starts Here

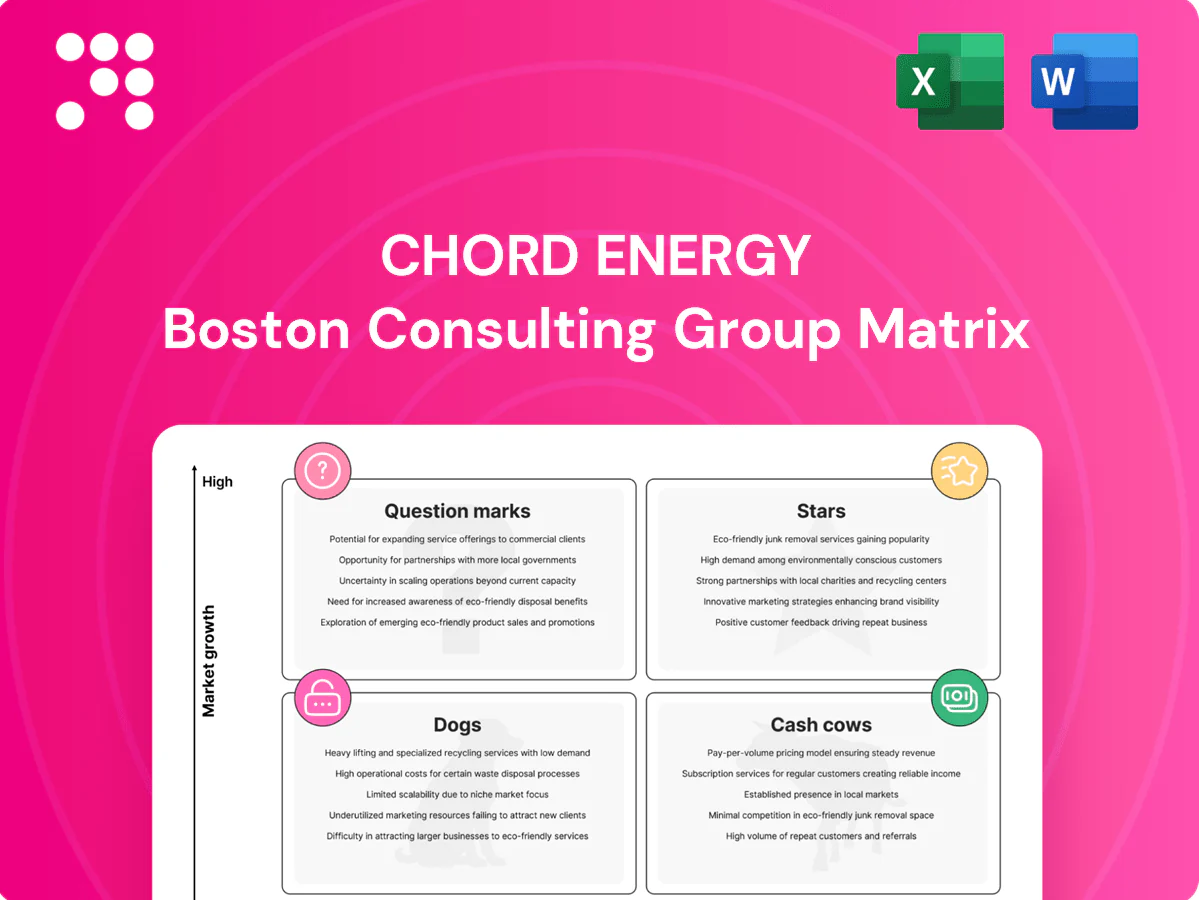

Want a sharp, investor-ready snapshot of Chord Energy? This preview shows the rough quadrant shapes, but the full BCG Matrix breaks down which assets are Stars, Cash Cows, Dogs or Question Marks—and why. Buy the complete report for quadrant-by-quadrant data, strategic moves tailored to Chord’s portfolio, and ready-to-use Word and Excel files that save you research time and point to where capital should flow next.

Stars

Core Williston oil program

Chord’s Core Williston oil program sits in high-growth Bakken/Three Forks windows where volumes and margins remain robust; pad development and long laterals sustain top-quartile per-well performance. The company holds leading operated acreage positions and reinvests significant capex to protect and grow share. Returns on that capital have historically outpaced cost of capital, justifying continued investment. Maintain funding to convert growth into durable cash flow.

Top-tier DSUs with repeatable type curves

Top-tier DSUs with repeatable type curves deliver consistent, above-basin EURs and lead a still-expanding Midland micro-market. Permian well productivity rose about 12% year-over-year in 2024 (EIA/Texas RRC), so these units command capital, crews and attention and repay through scale. Competitors benchmark against these wells; nurture them and they become cash engines as growth cools.

High-intensity completions and ops efficiency

Modern high-intensity completions and tight execution lift initial production rates and compress cycle times, giving Chord a competitive edge in a growth pocket. This approach demands upfront capital for fleets, proppant and logistics, pressuring near-term cash flow. The flywheel effect—higher IPs, faster payout and reinvestment—compounds returns. Stay capital-intensive while market momentum endures.

Oil-weighted barrels with premium differentials

Crude barrels that secure reliable takeaway and premium differentials deliver higher realizations, and in an expanding basin that uplift scales with volume; strong netbacks plus rising throughput drive star-category economics for Chord Energy in 2024. This is not set-and-forget but protect-and-expand: maintain takeaway capacity and keep capital aligned so share and realizations do not slip.

- reliable takeaway = better realizations

- scaling advantage with basin growth

- netbacks + rising volume = star behavior

- protect and expand capacity to defend share

Accretive bolt-on acquisitions

Consolidation in core townships increases Chord Energy working interest and inventory depth, delivering growth plus share through accretive bolt-on deals that strengthen returns if drilling inventory is high and contiguous.

Deals consume cash up front but fortify the operational moat; with disciplined integration these assets can transition from heavy investment to high-margin harvest over the life of the asset.

- Prioritize fit over flash: contiguous working interest and leasehold quality

- Integration control: centralize operations, capture synergies, protect margins

- Capex now, cashflow later: focus on IRR and acreage-level economics

Williston and Permian wells deliver top-quartile EURs and netbacks — reinvest to scale

Chord’s Williston and Permian stars deliver top-quartile per-well EURs and strong netbacks, justifying continued high reinvestment to protect acreage and takeaway. Modern completions and longer laterals lift IPs and compress cycle times, creating a payout flywheel. Prioritize takeaway capacity and contiguous bolt-ons to convert growth into durable cash engines. Maintain capital intensity while basin momentum persists.

| Metric | 2024 |

|---|---|

| Permian well productivity YoY | +12% (EIA/Texas RRC) |

| Core capex focus | High; protect & expand share |

What is included in the product

BCG analysis of Chord Energy’s units, pinpointing Stars, Cash Cows, Question Marks, Dogs and recommended invest/hold/divest actions.

One-page BCG matrix for Chord Energy — places each unit in a quadrant to pinpoint priorities and ease decisions.

Cash Cows

Base PDP production

Base PDP production provides low-decline barrels from mature benches that generate dependable cash — roughly 60% of Chord Energy’s operated volumes and funding over 80% of near-term debt service and dividends in 2024, with minimal promotional spend required; disciplined operations and maintenance keep decline low, feeding the next drillbit. Milk it, don’t starve it.

Mature Bakken/Three Forks pads

Mature Bakken/Three Forks pads sit squarely in cash cow territory: growth is past but operating margins remain strong against ~1.2 MMb/d Bakken basin output, with lease operating expenses roughly ~$6/BOE and predictable decline behavior. Infrastructure is in and learnings are banked, so modest completion or uptime tweaks typically boost cash flow more than large incremental capex. Classic low-growth, high-cash-return profile.

Midstream and takeaway arrangements

Established pipeline access stabilizes realizations and helped Chord lock in takeaway coverage for roughly 90% of 2024 volumes, reducing pricing differentials and lowering flaring-related penalties that previously cost operators millions annually. The asset is a cash cow: low growth but high utility, contributing steady midstream margin that underpins free cash flow. Keep contracts optimized and volumes steady to preserve ~$100–150 million of recurring EBITDA-equivalent cash generation. Quietly pays the bills.

Hedged production book

Hedged production book: not exciting, just effective — cushions price swings and supports planning. It doesn’t grow, it preserves; Chord entered 2024 with roughly half of forecast oil volumes hedged, stabilizing near-term cash versus volatile WTI. That reliable cash supports risk-taking elsewhere in the portfolio. Maintain discipline and roll hedges only when economics justify it.

- Cash reliability: funds capex and M&A

- Preservation not growth: stabilizes EBITDA

- Discipline: roll selectively

Water handling and reuse systems

Water handling and reuse systems are mature cash cows for Chord Energy, with existing infrastructure keeping operating costs low across legacy areas and delivering steady savings rather than growth.

Efficient handling per barrel improves free cash flow and supports capital-light operations; maintaining these systems preserves margin and funds upstream activity.

- Legacy infrastructure reduces unit Opex

- Stable savings, low growth

- Per-barrel efficiency boosts free cash flow

- Maintain assets to sustain margins

low-growth, high-cash: PDP ~60%, funds >80% debt/divs, EBITDA $100–150M

Base PDP supplies ~60% of operated volumes and funded >80% of near-term debt service and dividends in 2024; LOE ~ $6/BOE, recurring EBITDA ~$100–150M, ~50% oil volumes hedged and ~90% takeaway coverage—low-growth, high-cash generator that preserves free cash flow to fund capex and M&A.

| Metric | 2024 |

|---|---|

| Operated volumes from PDP | ~60% |

| Funds debt/dividends | >80% |

| Recurring EBITDA-equivalent | $100–150M |

| Lease operating expense | ~$6/BOE |

| Oil volumes hedged | ~50% |

| Takeaway coverage | ~90% |

What You’re Viewing Is Included

Chord Energy BCG Matrix

The Chord Energy BCG Matrix you're previewing is the exact, final file you'll receive after purchase. No watermarks, no demo placeholders—just a fully formatted strategic report ready for presentation. It’s crafted for clarity and editing, delivered instantly to your inbox with no surprises. Use it in decks, planning, or client meetings right away.

Actionable Strategy Starts Here

Want a sharp, investor-ready snapshot of Chord Energy? This preview shows the rough quadrant shapes, but the full BCG Matrix breaks down which assets are Stars, Cash Cows, Dogs or Question Marks—and why. Buy the complete report for quadrant-by-quadrant data, strategic moves tailored to Chord’s portfolio, and ready-to-use Word and Excel files that save you research time and point to where capital should flow next.

Stars

Core Williston oil program

Chord’s Core Williston oil program sits in high-growth Bakken/Three Forks windows where volumes and margins remain robust; pad development and long laterals sustain top-quartile per-well performance. The company holds leading operated acreage positions and reinvests significant capex to protect and grow share. Returns on that capital have historically outpaced cost of capital, justifying continued investment. Maintain funding to convert growth into durable cash flow.

Top-tier DSUs with repeatable type curves

Top-tier DSUs with repeatable type curves deliver consistent, above-basin EURs and lead a still-expanding Midland micro-market. Permian well productivity rose about 12% year-over-year in 2024 (EIA/Texas RRC), so these units command capital, crews and attention and repay through scale. Competitors benchmark against these wells; nurture them and they become cash engines as growth cools.

High-intensity completions and ops efficiency

Modern high-intensity completions and tight execution lift initial production rates and compress cycle times, giving Chord a competitive edge in a growth pocket. This approach demands upfront capital for fleets, proppant and logistics, pressuring near-term cash flow. The flywheel effect—higher IPs, faster payout and reinvestment—compounds returns. Stay capital-intensive while market momentum endures.

Oil-weighted barrels with premium differentials

Crude barrels that secure reliable takeaway and premium differentials deliver higher realizations, and in an expanding basin that uplift scales with volume; strong netbacks plus rising throughput drive star-category economics for Chord Energy in 2024. This is not set-and-forget but protect-and-expand: maintain takeaway capacity and keep capital aligned so share and realizations do not slip.

- reliable takeaway = better realizations

- scaling advantage with basin growth

- netbacks + rising volume = star behavior

- protect and expand capacity to defend share

Accretive bolt-on acquisitions

Consolidation in core townships increases Chord Energy working interest and inventory depth, delivering growth plus share through accretive bolt-on deals that strengthen returns if drilling inventory is high and contiguous.

Deals consume cash up front but fortify the operational moat; with disciplined integration these assets can transition from heavy investment to high-margin harvest over the life of the asset.

- Prioritize fit over flash: contiguous working interest and leasehold quality

- Integration control: centralize operations, capture synergies, protect margins

- Capex now, cashflow later: focus on IRR and acreage-level economics

Williston and Permian wells deliver top-quartile EURs and netbacks — reinvest to scale

Chord’s Williston and Permian stars deliver top-quartile per-well EURs and strong netbacks, justifying continued high reinvestment to protect acreage and takeaway. Modern completions and longer laterals lift IPs and compress cycle times, creating a payout flywheel. Prioritize takeaway capacity and contiguous bolt-ons to convert growth into durable cash engines. Maintain capital intensity while basin momentum persists.

| Metric | 2024 |

|---|---|

| Permian well productivity YoY | +12% (EIA/Texas RRC) |

| Core capex focus | High; protect & expand share |

What is included in the product

BCG analysis of Chord Energy’s units, pinpointing Stars, Cash Cows, Question Marks, Dogs and recommended invest/hold/divest actions.

One-page BCG matrix for Chord Energy — places each unit in a quadrant to pinpoint priorities and ease decisions.

Cash Cows

Base PDP production

Base PDP production provides low-decline barrels from mature benches that generate dependable cash — roughly 60% of Chord Energy’s operated volumes and funding over 80% of near-term debt service and dividends in 2024, with minimal promotional spend required; disciplined operations and maintenance keep decline low, feeding the next drillbit. Milk it, don’t starve it.

Mature Bakken/Three Forks pads

Mature Bakken/Three Forks pads sit squarely in cash cow territory: growth is past but operating margins remain strong against ~1.2 MMb/d Bakken basin output, with lease operating expenses roughly ~$6/BOE and predictable decline behavior. Infrastructure is in and learnings are banked, so modest completion or uptime tweaks typically boost cash flow more than large incremental capex. Classic low-growth, high-cash-return profile.

Midstream and takeaway arrangements

Established pipeline access stabilizes realizations and helped Chord lock in takeaway coverage for roughly 90% of 2024 volumes, reducing pricing differentials and lowering flaring-related penalties that previously cost operators millions annually. The asset is a cash cow: low growth but high utility, contributing steady midstream margin that underpins free cash flow. Keep contracts optimized and volumes steady to preserve ~$100–150 million of recurring EBITDA-equivalent cash generation. Quietly pays the bills.

Hedged production book

Hedged production book: not exciting, just effective — cushions price swings and supports planning. It doesn’t grow, it preserves; Chord entered 2024 with roughly half of forecast oil volumes hedged, stabilizing near-term cash versus volatile WTI. That reliable cash supports risk-taking elsewhere in the portfolio. Maintain discipline and roll hedges only when economics justify it.

- Cash reliability: funds capex and M&A

- Preservation not growth: stabilizes EBITDA

- Discipline: roll selectively

Water handling and reuse systems

Water handling and reuse systems are mature cash cows for Chord Energy, with existing infrastructure keeping operating costs low across legacy areas and delivering steady savings rather than growth.

Efficient handling per barrel improves free cash flow and supports capital-light operations; maintaining these systems preserves margin and funds upstream activity.

- Legacy infrastructure reduces unit Opex

- Stable savings, low growth

- Per-barrel efficiency boosts free cash flow

- Maintain assets to sustain margins

low-growth, high-cash: PDP ~60%, funds >80% debt/divs, EBITDA $100–150M

Base PDP supplies ~60% of operated volumes and funded >80% of near-term debt service and dividends in 2024; LOE ~ $6/BOE, recurring EBITDA ~$100–150M, ~50% oil volumes hedged and ~90% takeaway coverage—low-growth, high-cash generator that preserves free cash flow to fund capex and M&A.

| Metric | 2024 |

|---|---|

| Operated volumes from PDP | ~60% |

| Funds debt/dividends | >80% |

| Recurring EBITDA-equivalent | $100–150M |

| Lease operating expense | ~$6/BOE |

| Oil volumes hedged | ~50% |

| Takeaway coverage | ~90% |

What You’re Viewing Is Included

Chord Energy BCG Matrix

The Chord Energy BCG Matrix you're previewing is the exact, final file you'll receive after purchase. No watermarks, no demo placeholders—just a fully formatted strategic report ready for presentation. It’s crafted for clarity and editing, delivered instantly to your inbox with no surprises. Use it in decks, planning, or client meetings right away.

Description

Actionable Strategy Starts Here

Want a sharp, investor-ready snapshot of Chord Energy? This preview shows the rough quadrant shapes, but the full BCG Matrix breaks down which assets are Stars, Cash Cows, Dogs or Question Marks—and why. Buy the complete report for quadrant-by-quadrant data, strategic moves tailored to Chord’s portfolio, and ready-to-use Word and Excel files that save you research time and point to where capital should flow next.

Stars

Core Williston oil program

Chord’s Core Williston oil program sits in high-growth Bakken/Three Forks windows where volumes and margins remain robust; pad development and long laterals sustain top-quartile per-well performance. The company holds leading operated acreage positions and reinvests significant capex to protect and grow share. Returns on that capital have historically outpaced cost of capital, justifying continued investment. Maintain funding to convert growth into durable cash flow.

Top-tier DSUs with repeatable type curves

Top-tier DSUs with repeatable type curves deliver consistent, above-basin EURs and lead a still-expanding Midland micro-market. Permian well productivity rose about 12% year-over-year in 2024 (EIA/Texas RRC), so these units command capital, crews and attention and repay through scale. Competitors benchmark against these wells; nurture them and they become cash engines as growth cools.

High-intensity completions and ops efficiency

Modern high-intensity completions and tight execution lift initial production rates and compress cycle times, giving Chord a competitive edge in a growth pocket. This approach demands upfront capital for fleets, proppant and logistics, pressuring near-term cash flow. The flywheel effect—higher IPs, faster payout and reinvestment—compounds returns. Stay capital-intensive while market momentum endures.

Oil-weighted barrels with premium differentials

Crude barrels that secure reliable takeaway and premium differentials deliver higher realizations, and in an expanding basin that uplift scales with volume; strong netbacks plus rising throughput drive star-category economics for Chord Energy in 2024. This is not set-and-forget but protect-and-expand: maintain takeaway capacity and keep capital aligned so share and realizations do not slip.

- reliable takeaway = better realizations

- scaling advantage with basin growth

- netbacks + rising volume = star behavior

- protect and expand capacity to defend share

Accretive bolt-on acquisitions

Consolidation in core townships increases Chord Energy working interest and inventory depth, delivering growth plus share through accretive bolt-on deals that strengthen returns if drilling inventory is high and contiguous.

Deals consume cash up front but fortify the operational moat; with disciplined integration these assets can transition from heavy investment to high-margin harvest over the life of the asset.

- Prioritize fit over flash: contiguous working interest and leasehold quality

- Integration control: centralize operations, capture synergies, protect margins

- Capex now, cashflow later: focus on IRR and acreage-level economics

Williston and Permian wells deliver top-quartile EURs and netbacks — reinvest to scale

Chord’s Williston and Permian stars deliver top-quartile per-well EURs and strong netbacks, justifying continued high reinvestment to protect acreage and takeaway. Modern completions and longer laterals lift IPs and compress cycle times, creating a payout flywheel. Prioritize takeaway capacity and contiguous bolt-ons to convert growth into durable cash engines. Maintain capital intensity while basin momentum persists.

| Metric | 2024 |

|---|---|

| Permian well productivity YoY | +12% (EIA/Texas RRC) |

| Core capex focus | High; protect & expand share |

What is included in the product

BCG analysis of Chord Energy’s units, pinpointing Stars, Cash Cows, Question Marks, Dogs and recommended invest/hold/divest actions.

One-page BCG matrix for Chord Energy — places each unit in a quadrant to pinpoint priorities and ease decisions.

Cash Cows

Base PDP production

Base PDP production provides low-decline barrels from mature benches that generate dependable cash — roughly 60% of Chord Energy’s operated volumes and funding over 80% of near-term debt service and dividends in 2024, with minimal promotional spend required; disciplined operations and maintenance keep decline low, feeding the next drillbit. Milk it, don’t starve it.

Mature Bakken/Three Forks pads

Mature Bakken/Three Forks pads sit squarely in cash cow territory: growth is past but operating margins remain strong against ~1.2 MMb/d Bakken basin output, with lease operating expenses roughly ~$6/BOE and predictable decline behavior. Infrastructure is in and learnings are banked, so modest completion or uptime tweaks typically boost cash flow more than large incremental capex. Classic low-growth, high-cash-return profile.

Midstream and takeaway arrangements

Established pipeline access stabilizes realizations and helped Chord lock in takeaway coverage for roughly 90% of 2024 volumes, reducing pricing differentials and lowering flaring-related penalties that previously cost operators millions annually. The asset is a cash cow: low growth but high utility, contributing steady midstream margin that underpins free cash flow. Keep contracts optimized and volumes steady to preserve ~$100–150 million of recurring EBITDA-equivalent cash generation. Quietly pays the bills.

Hedged production book

Hedged production book: not exciting, just effective — cushions price swings and supports planning. It doesn’t grow, it preserves; Chord entered 2024 with roughly half of forecast oil volumes hedged, stabilizing near-term cash versus volatile WTI. That reliable cash supports risk-taking elsewhere in the portfolio. Maintain discipline and roll hedges only when economics justify it.

- Cash reliability: funds capex and M&A

- Preservation not growth: stabilizes EBITDA

- Discipline: roll selectively

Water handling and reuse systems

Water handling and reuse systems are mature cash cows for Chord Energy, with existing infrastructure keeping operating costs low across legacy areas and delivering steady savings rather than growth.

Efficient handling per barrel improves free cash flow and supports capital-light operations; maintaining these systems preserves margin and funds upstream activity.

- Legacy infrastructure reduces unit Opex

- Stable savings, low growth

- Per-barrel efficiency boosts free cash flow

- Maintain assets to sustain margins

low-growth, high-cash: PDP ~60%, funds >80% debt/divs, EBITDA $100–150M

Base PDP supplies ~60% of operated volumes and funded >80% of near-term debt service and dividends in 2024; LOE ~ $6/BOE, recurring EBITDA ~$100–150M, ~50% oil volumes hedged and ~90% takeaway coverage—low-growth, high-cash generator that preserves free cash flow to fund capex and M&A.

| Metric | 2024 |

|---|---|

| Operated volumes from PDP | ~60% |

| Funds debt/dividends | >80% |

| Recurring EBITDA-equivalent | $100–150M |

| Lease operating expense | ~$6/BOE |

| Oil volumes hedged | ~50% |

| Takeaway coverage | ~90% |

What You’re Viewing Is Included

Chord Energy BCG Matrix

The Chord Energy BCG Matrix you're previewing is the exact, final file you'll receive after purchase. No watermarks, no demo placeholders—just a fully formatted strategic report ready for presentation. It’s crafted for clarity and editing, delivered instantly to your inbox with no surprises. Use it in decks, planning, or client meetings right away.