Christie Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

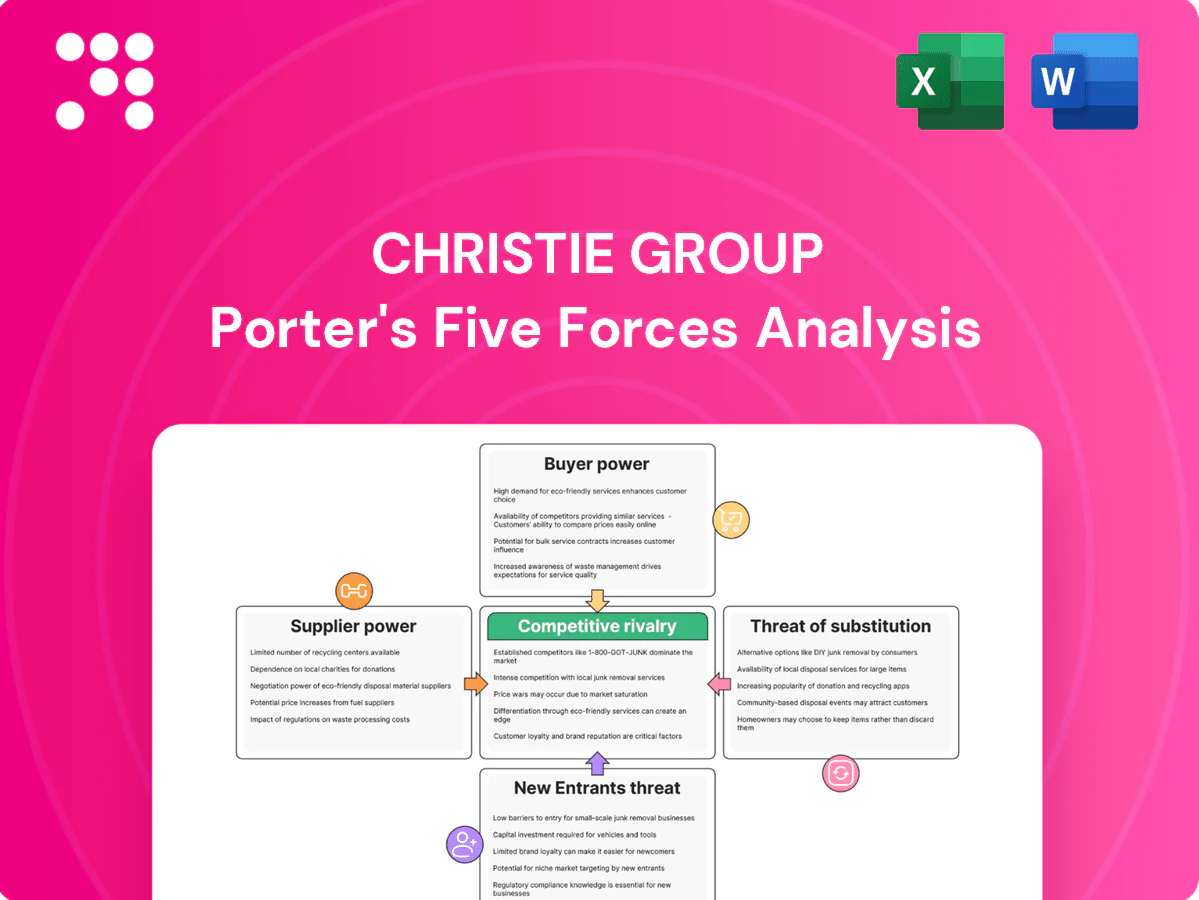

Christie Group faces moderate supplier power and intense buyer expectations, while barriers to entry and substitutes shape strategic choices; this snapshot highlights key pressures and competitive positioning. Unlock the full Porter's Five Forces Analysis to view force-by-force ratings, visuals, and actionable strategies to guide investment or strategy decisions.

Suppliers Bargaining Power

Specialist talent scarcity

Christie Group depends on scarce RICS-qualified valuers, sector experts and regulated agents, concentrating supplier power; RICS reports circa 140,000 members globally in 2024. Experienced professionals command premium pay and flexible terms, while retention and training investments raise switching costs. Tight UK labor markets (unemployment ~4.2% Apr–Jun 2024) amplify pressure.

Critical data and software inputs

Access to property, sales and sector datasets for Christie Group relies heavily on third-party vendors and proprietary platforms, with subscriptions commonly ranging from 10,000–100,000+ USD/year and cloud/analytics hosting often billed separately. In 2024 the top three cloud providers (AWS 32%, Azure 23%, GCP 11%) held about 66% of IaaS, increasing vendor leverage. Consolidation among data vendors amplifies pricing power, while multi-year contracts and integration costs create high switching barriers.

Regulatory and accreditation bodies

RICS (over 140,000 members worldwide in 2024) and the FCA (regulating over 58,000 firms) plus healthcare frameworks (eg CQC/NHS standards covering thousands of providers) act as suppliers of licensure and standards for Christie Group; their compliance costs and mandatory audits create non-negotiable terms. Frequent changes in standards raise operating complexity and implementation costs. Accreditation grants market credibility but increases dependency on these bodies.

Niche tech integrators

In 2024 niche tech integrators exert high supplier power for Christie Group: legacy inventory and sector-specific software require specialized integrators, limiting alternatives and increasing fees and timelines. Customization and ongoing maintenance create 3–5 year lock-ins and material switching costs. Vendor failure can halt operations and cause remediation expenses that often exceed project contingencies.

- Limited alternatives → higher fees, longer lead times

- 3–5 year customization/maintenance lock-ins

- Vendor failure risk → operational disruption, budget overruns

Outsourced field services

For inventory audits and site work, localized contractors and auditors can influence cost and availability; 2024 industry surveys show peak-season rate uplifts of about 18-22%, boosting supplier leverage. Quality variability shrinks the viable pool to under one-third of providers, and requirement for multi-country coverage typically limits options to a dozen or fewer vetted vendors.

- Localized premium: +18–22% (2024)

- Viable suppliers: <30% due to quality variance

- Multi-country vendors: ~12 or fewer

Supplier concentration: scarce RICS valuers, tight UK labour, cloud lock-ins, 18-22% uplift

Christie Group faces concentrated supplier power from scarce RICS-qualified valuers (RICS ~140,000 members in 2024) and tight UK labor markets (unemployment ~4.2% Apr–Jun 2024). Data and cloud vendors (AWS 32%, Azure 23%, GCP 11% IaaS share 2024) charge $10k–$100k+/yr with multi-year lock-ins (3–5 years). Niche integrators and localized auditors drive switching costs, peak-rate uplifts ~18–22%, viable suppliers <30%.

| Metric | 2024 Value |

|---|---|

| RICS members | ~140,000 |

| UK unemployment | ~4.2% (Apr–Jun) |

| Top-3 IaaS share | AWS32%/Azure23%/GCP11% |

| Data subscriptions | $10k–$100k+/yr |

| Contract lock-ins | 3–5 years |

| Peak-rate uplift | +18–22% |

| Viable suppliers | <30% |

| Multi-country vendors | ~12 |

What is included in the product

Tailored Porter’s Five Forces analysis for Christie Group, uncovering key drivers of competition, supplier and buyer power, entry barriers and substitutes, plus identification of disruptive threats and strategic levers to protect market share and pricing power.

A concise, one-sheet Porter’s Five Forces for Christie Group that turns complex market pressures into instant strategic clarity, ready to drop into pitch decks or board slides. Customize force levels, swap in your data, and generate a spider chart—no macros or finance expertise required.

Customers Bargaining Power

Fragmented yet informed clients

Hospitality, leisure, healthcare and retail clients remain numerous but by 2024 increasingly data-savvy. Comparable quotes and online intelligence—used by around 75% of buyers in 2024—enable tougher negotiations and compress fees on standardized tasks. Differentiation must rest on deep sector expertise and demonstrable outcomes.

Enterprise and public-sector tenders

Large chains, care groups and public entities run formal RFPs that concentrate volume and force price and service-level concessions; framework agreements, typically 3–5 years, intensify competition and limit supplier flexibility. Multi-year awards can anchor pricing and squeeze margins across the period. About 75% of long-term care beds in the UK are privately provided, amplifying buyer leverage.

Moderate switching costs

For brokerage and valuation, buyers can switch among accredited firms, yet 2024 industry reports show professional services client retention near 80%, reflecting relationship stickiness. Proprietary insights and pipeline knowledge create frictions that raise practical switching effort. In systems segments, embedded software and processes—often backed by 36-month enterprise contracts—materially lift switching costs. Performance SLAs, with penalties commonly up to 10% of contract value, further bind clients.

Cyclical budget sensitivity

Downturns increase buyer price sensitivity and project deferrals, with many clients trading down to limited-scope contracts or DIY solutions; conversely 2024 upcycles have improved demand, product mix and pricing, swinging buyer power materially over time.

- Buyer sensitivity: higher in downturns

- Trading down: limited-scope/DIY options rise

- Upcycles: better mix and pricing

- Net effect: cyclical swing in buyer power

Outcome-based expectations

Clients demand measurable value—faster deal cycles, pinpoint valuations, compliance assurance and shrinkage reduction—and 2024 contracts increasingly tie fees to those outcomes. Performance metrics create fee pressure when outcomes lag, while references and case studies materially boost customer bargaining leverage. Renewal terms in 2024 commonly hinge on demonstrated ROI and milestone delivery.

- Faster deals

- Accurate valuations

- Compliance assurance

- Shrinkage reduction

- Outcome-linked fees

- References drive leverage

- Renewal = ROI

Data-savvy buyers drive tougher deals; 75% use online intelligence

Buyers more data-savvy—about 75% used online intelligence in 2024—driving tougher price negotiations. Large chains use 3–5 year RFP frameworks; 75% of UK long-term care beds are private. Professional services client retention ~80% and 36-month enterprise contracts raise switching costs. Outcome-linked fees and SLAs (penalties ≤10%) increase buyer leverage.

| Metric | 2024 |

|---|---|

| Online intelligence use | 75% |

| UK private long-term care beds | 75% |

| Client retention (professional services) | ~80% |

| Typical enterprise contract | 36 months |

| SLA penalties | ≤10% |

What You See Is What You Get

Christie Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of the Christie Group you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is completed you’ll have instant access to this identical file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Christie Group faces moderate supplier power and intense buyer expectations, while barriers to entry and substitutes shape strategic choices; this snapshot highlights key pressures and competitive positioning. Unlock the full Porter's Five Forces Analysis to view force-by-force ratings, visuals, and actionable strategies to guide investment or strategy decisions.

Suppliers Bargaining Power

Specialist talent scarcity

Christie Group depends on scarce RICS-qualified valuers, sector experts and regulated agents, concentrating supplier power; RICS reports circa 140,000 members globally in 2024. Experienced professionals command premium pay and flexible terms, while retention and training investments raise switching costs. Tight UK labor markets (unemployment ~4.2% Apr–Jun 2024) amplify pressure.

Critical data and software inputs

Access to property, sales and sector datasets for Christie Group relies heavily on third-party vendors and proprietary platforms, with subscriptions commonly ranging from 10,000–100,000+ USD/year and cloud/analytics hosting often billed separately. In 2024 the top three cloud providers (AWS 32%, Azure 23%, GCP 11%) held about 66% of IaaS, increasing vendor leverage. Consolidation among data vendors amplifies pricing power, while multi-year contracts and integration costs create high switching barriers.

Regulatory and accreditation bodies

RICS (over 140,000 members worldwide in 2024) and the FCA (regulating over 58,000 firms) plus healthcare frameworks (eg CQC/NHS standards covering thousands of providers) act as suppliers of licensure and standards for Christie Group; their compliance costs and mandatory audits create non-negotiable terms. Frequent changes in standards raise operating complexity and implementation costs. Accreditation grants market credibility but increases dependency on these bodies.

Niche tech integrators

In 2024 niche tech integrators exert high supplier power for Christie Group: legacy inventory and sector-specific software require specialized integrators, limiting alternatives and increasing fees and timelines. Customization and ongoing maintenance create 3–5 year lock-ins and material switching costs. Vendor failure can halt operations and cause remediation expenses that often exceed project contingencies.

- Limited alternatives → higher fees, longer lead times

- 3–5 year customization/maintenance lock-ins

- Vendor failure risk → operational disruption, budget overruns

Outsourced field services

For inventory audits and site work, localized contractors and auditors can influence cost and availability; 2024 industry surveys show peak-season rate uplifts of about 18-22%, boosting supplier leverage. Quality variability shrinks the viable pool to under one-third of providers, and requirement for multi-country coverage typically limits options to a dozen or fewer vetted vendors.

- Localized premium: +18–22% (2024)

- Viable suppliers: <30% due to quality variance

- Multi-country vendors: ~12 or fewer

Supplier concentration: scarce RICS valuers, tight UK labour, cloud lock-ins, 18-22% uplift

Christie Group faces concentrated supplier power from scarce RICS-qualified valuers (RICS ~140,000 members in 2024) and tight UK labor markets (unemployment ~4.2% Apr–Jun 2024). Data and cloud vendors (AWS 32%, Azure 23%, GCP 11% IaaS share 2024) charge $10k–$100k+/yr with multi-year lock-ins (3–5 years). Niche integrators and localized auditors drive switching costs, peak-rate uplifts ~18–22%, viable suppliers <30%.

| Metric | 2024 Value |

|---|---|

| RICS members | ~140,000 |

| UK unemployment | ~4.2% (Apr–Jun) |

| Top-3 IaaS share | AWS32%/Azure23%/GCP11% |

| Data subscriptions | $10k–$100k+/yr |

| Contract lock-ins | 3–5 years |

| Peak-rate uplift | +18–22% |

| Viable suppliers | <30% |

| Multi-country vendors | ~12 |

What is included in the product

Tailored Porter’s Five Forces analysis for Christie Group, uncovering key drivers of competition, supplier and buyer power, entry barriers and substitutes, plus identification of disruptive threats and strategic levers to protect market share and pricing power.

A concise, one-sheet Porter’s Five Forces for Christie Group that turns complex market pressures into instant strategic clarity, ready to drop into pitch decks or board slides. Customize force levels, swap in your data, and generate a spider chart—no macros or finance expertise required.

Customers Bargaining Power

Fragmented yet informed clients

Hospitality, leisure, healthcare and retail clients remain numerous but by 2024 increasingly data-savvy. Comparable quotes and online intelligence—used by around 75% of buyers in 2024—enable tougher negotiations and compress fees on standardized tasks. Differentiation must rest on deep sector expertise and demonstrable outcomes.

Enterprise and public-sector tenders

Large chains, care groups and public entities run formal RFPs that concentrate volume and force price and service-level concessions; framework agreements, typically 3–5 years, intensify competition and limit supplier flexibility. Multi-year awards can anchor pricing and squeeze margins across the period. About 75% of long-term care beds in the UK are privately provided, amplifying buyer leverage.

Moderate switching costs

For brokerage and valuation, buyers can switch among accredited firms, yet 2024 industry reports show professional services client retention near 80%, reflecting relationship stickiness. Proprietary insights and pipeline knowledge create frictions that raise practical switching effort. In systems segments, embedded software and processes—often backed by 36-month enterprise contracts—materially lift switching costs. Performance SLAs, with penalties commonly up to 10% of contract value, further bind clients.

Cyclical budget sensitivity

Downturns increase buyer price sensitivity and project deferrals, with many clients trading down to limited-scope contracts or DIY solutions; conversely 2024 upcycles have improved demand, product mix and pricing, swinging buyer power materially over time.

- Buyer sensitivity: higher in downturns

- Trading down: limited-scope/DIY options rise

- Upcycles: better mix and pricing

- Net effect: cyclical swing in buyer power

Outcome-based expectations

Clients demand measurable value—faster deal cycles, pinpoint valuations, compliance assurance and shrinkage reduction—and 2024 contracts increasingly tie fees to those outcomes. Performance metrics create fee pressure when outcomes lag, while references and case studies materially boost customer bargaining leverage. Renewal terms in 2024 commonly hinge on demonstrated ROI and milestone delivery.

- Faster deals

- Accurate valuations

- Compliance assurance

- Shrinkage reduction

- Outcome-linked fees

- References drive leverage

- Renewal = ROI

Data-savvy buyers drive tougher deals; 75% use online intelligence

Buyers more data-savvy—about 75% used online intelligence in 2024—driving tougher price negotiations. Large chains use 3–5 year RFP frameworks; 75% of UK long-term care beds are private. Professional services client retention ~80% and 36-month enterprise contracts raise switching costs. Outcome-linked fees and SLAs (penalties ≤10%) increase buyer leverage.

| Metric | 2024 |

|---|---|

| Online intelligence use | 75% |

| UK private long-term care beds | 75% |

| Client retention (professional services) | ~80% |

| Typical enterprise contract | 36 months |

| SLA penalties | ≤10% |

What You See Is What You Get

Christie Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of the Christie Group you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is completed you’ll have instant access to this identical file.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Christie Group faces moderate supplier power and intense buyer expectations, while barriers to entry and substitutes shape strategic choices; this snapshot highlights key pressures and competitive positioning. Unlock the full Porter's Five Forces Analysis to view force-by-force ratings, visuals, and actionable strategies to guide investment or strategy decisions.

Suppliers Bargaining Power

Specialist talent scarcity

Christie Group depends on scarce RICS-qualified valuers, sector experts and regulated agents, concentrating supplier power; RICS reports circa 140,000 members globally in 2024. Experienced professionals command premium pay and flexible terms, while retention and training investments raise switching costs. Tight UK labor markets (unemployment ~4.2% Apr–Jun 2024) amplify pressure.

Critical data and software inputs

Access to property, sales and sector datasets for Christie Group relies heavily on third-party vendors and proprietary platforms, with subscriptions commonly ranging from 10,000–100,000+ USD/year and cloud/analytics hosting often billed separately. In 2024 the top three cloud providers (AWS 32%, Azure 23%, GCP 11%) held about 66% of IaaS, increasing vendor leverage. Consolidation among data vendors amplifies pricing power, while multi-year contracts and integration costs create high switching barriers.

Regulatory and accreditation bodies

RICS (over 140,000 members worldwide in 2024) and the FCA (regulating over 58,000 firms) plus healthcare frameworks (eg CQC/NHS standards covering thousands of providers) act as suppliers of licensure and standards for Christie Group; their compliance costs and mandatory audits create non-negotiable terms. Frequent changes in standards raise operating complexity and implementation costs. Accreditation grants market credibility but increases dependency on these bodies.

Niche tech integrators

In 2024 niche tech integrators exert high supplier power for Christie Group: legacy inventory and sector-specific software require specialized integrators, limiting alternatives and increasing fees and timelines. Customization and ongoing maintenance create 3–5 year lock-ins and material switching costs. Vendor failure can halt operations and cause remediation expenses that often exceed project contingencies.

- Limited alternatives → higher fees, longer lead times

- 3–5 year customization/maintenance lock-ins

- Vendor failure risk → operational disruption, budget overruns

Outsourced field services

For inventory audits and site work, localized contractors and auditors can influence cost and availability; 2024 industry surveys show peak-season rate uplifts of about 18-22%, boosting supplier leverage. Quality variability shrinks the viable pool to under one-third of providers, and requirement for multi-country coverage typically limits options to a dozen or fewer vetted vendors.

- Localized premium: +18–22% (2024)

- Viable suppliers: <30% due to quality variance

- Multi-country vendors: ~12 or fewer

Supplier concentration: scarce RICS valuers, tight UK labour, cloud lock-ins, 18-22% uplift

Christie Group faces concentrated supplier power from scarce RICS-qualified valuers (RICS ~140,000 members in 2024) and tight UK labor markets (unemployment ~4.2% Apr–Jun 2024). Data and cloud vendors (AWS 32%, Azure 23%, GCP 11% IaaS share 2024) charge $10k–$100k+/yr with multi-year lock-ins (3–5 years). Niche integrators and localized auditors drive switching costs, peak-rate uplifts ~18–22%, viable suppliers <30%.

| Metric | 2024 Value |

|---|---|

| RICS members | ~140,000 |

| UK unemployment | ~4.2% (Apr–Jun) |

| Top-3 IaaS share | AWS32%/Azure23%/GCP11% |

| Data subscriptions | $10k–$100k+/yr |

| Contract lock-ins | 3–5 years |

| Peak-rate uplift | +18–22% |

| Viable suppliers | <30% |

| Multi-country vendors | ~12 |

What is included in the product

Tailored Porter’s Five Forces analysis for Christie Group, uncovering key drivers of competition, supplier and buyer power, entry barriers and substitutes, plus identification of disruptive threats and strategic levers to protect market share and pricing power.

A concise, one-sheet Porter’s Five Forces for Christie Group that turns complex market pressures into instant strategic clarity, ready to drop into pitch decks or board slides. Customize force levels, swap in your data, and generate a spider chart—no macros or finance expertise required.

Customers Bargaining Power

Fragmented yet informed clients

Hospitality, leisure, healthcare and retail clients remain numerous but by 2024 increasingly data-savvy. Comparable quotes and online intelligence—used by around 75% of buyers in 2024—enable tougher negotiations and compress fees on standardized tasks. Differentiation must rest on deep sector expertise and demonstrable outcomes.

Enterprise and public-sector tenders

Large chains, care groups and public entities run formal RFPs that concentrate volume and force price and service-level concessions; framework agreements, typically 3–5 years, intensify competition and limit supplier flexibility. Multi-year awards can anchor pricing and squeeze margins across the period. About 75% of long-term care beds in the UK are privately provided, amplifying buyer leverage.

Moderate switching costs

For brokerage and valuation, buyers can switch among accredited firms, yet 2024 industry reports show professional services client retention near 80%, reflecting relationship stickiness. Proprietary insights and pipeline knowledge create frictions that raise practical switching effort. In systems segments, embedded software and processes—often backed by 36-month enterprise contracts—materially lift switching costs. Performance SLAs, with penalties commonly up to 10% of contract value, further bind clients.

Cyclical budget sensitivity

Downturns increase buyer price sensitivity and project deferrals, with many clients trading down to limited-scope contracts or DIY solutions; conversely 2024 upcycles have improved demand, product mix and pricing, swinging buyer power materially over time.

- Buyer sensitivity: higher in downturns

- Trading down: limited-scope/DIY options rise

- Upcycles: better mix and pricing

- Net effect: cyclical swing in buyer power

Outcome-based expectations

Clients demand measurable value—faster deal cycles, pinpoint valuations, compliance assurance and shrinkage reduction—and 2024 contracts increasingly tie fees to those outcomes. Performance metrics create fee pressure when outcomes lag, while references and case studies materially boost customer bargaining leverage. Renewal terms in 2024 commonly hinge on demonstrated ROI and milestone delivery.

- Faster deals

- Accurate valuations

- Compliance assurance

- Shrinkage reduction

- Outcome-linked fees

- References drive leverage

- Renewal = ROI

Data-savvy buyers drive tougher deals; 75% use online intelligence

Buyers more data-savvy—about 75% used online intelligence in 2024—driving tougher price negotiations. Large chains use 3–5 year RFP frameworks; 75% of UK long-term care beds are private. Professional services client retention ~80% and 36-month enterprise contracts raise switching costs. Outcome-linked fees and SLAs (penalties ≤10%) increase buyer leverage.

| Metric | 2024 |

|---|---|

| Online intelligence use | 75% |

| UK private long-term care beds | 75% |

| Client retention (professional services) | ~80% |

| Typical enterprise contract | 36 months |

| SLA penalties | ≤10% |

What You See Is What You Get

Christie Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of the Christie Group you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is completed you’ll have instant access to this identical file.