Christie Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our targeted PESTLE Analysis of Christie Group—uncover how political shifts, economic trends, social preferences, technological change, legal developments, and environmental pressures shape its outlook. Perfect for investors and strategists, this ready-to-use report turns external risks into actionable moves. Purchase the full analysis for detailed insights and downloadable templates.

Political factors

UK policy stability and public spending

Shifts in UK fiscal and industrial policy materially affect Christie Group’s hospitality, healthcare and retail pipelines; the standard VAT rate remains 20% and UK public services funding keeps NHS spending around £176bn in 2024/25, directly shaping healthcare transactions and consultancy demand. Reforms to business rates and investment incentives alter valuations and client capex plans, while political stability boosts agency deal flow and volatility stalls buyer decisions.

Post‑Brexit UK‑EU relations

Regulatory divergence since the 2020 Trade and Cooperation Agreement has increased trade frictions, raising compliance costs for UK‑EU transactions and complicating cross‑border deals. Automatic recognition of professional qualifications ended in January 2021, affecting advisory credentials and valuations across jurisdictions. Ending free movement and the points‑based system reduced EU labour flows; net migration was 606,000 (year to June 2023), straining hospitality and care staffing and deal margins. Market confidence depends on predictable UK‑EU arrangements.

Local planning and licensing regimes

Planning permissions, change‑of‑use and alcohol/gaming licences directly determine asset viability and deal timing; local variations across over 300 UK planning authorities require tailored consultancy and tight timeline management. Policy shifts toward town‑centre revitalisation—UK high‑street vacancy ~13% in 2023—can unlock retail and leisure opportunities, while tight regimes increase compliance complexity and due‑diligence workloads.

Tourism and regional development policies

Destination marketing and infrastructure investment shape leisure demand; UNWTO reported travel recovery to roughly 90% of 2019 levels by 2023, supporting higher hotel occupancy assumptions. Regeneration grants such as the UK Levelling Up Fund (£4.8bn) can catalyze transactions in secondary locations. Visa liberalization and digital visas materially affect inbound volumes while clear policy signals improve pipeline visibility for Christie Group agency and valuation services.

- Destination marketing: boosts demand and occupancy

- Regeneration grants (£4.8bn): catalyze secondary-market deals

- Visa policy: alters inbound volumes and RevPAR assumptions

- Policy clarity: improves agency/valuation pipeline visibility

Public health and crisis preparedness

Public health directives materially affect footfall and occupancy across client sectors; UNWTO reported international tourism arrivals reached about 88% of 2019 levels in 2023, underscoring sensitivity to health rules. Preparedness frameworks shape contingency plans in hospitality and care, while mandates accelerate digital adoption that Christie systems can serve; rapid policy shifts demand agile advisory responses.

- Health impact: footfall/occupancy volatility

- Preparedness: contingency-driven CAPEX planning

- Digital mandates: telemetry, contactless revenue ops

- Advisory need: fast policy-response services

VAT 20%, NHS £176bn, migration 606k squeeze staffing, drive secondary deals

UK fiscal policy (VAT 20%, NHS spend £176bn in 2024/25) and business‑rate reforms shape Christie Group deal flow and valuations; net migration 606,000 (yr to Jun 2023) tightens hospitality/care staffing. Levelling Up Fund £4.8bn and tourism recovery ~90% of 2019 by 2023 support secondary‑market transactions; planning/licensing complexity prolongs timelines.

| Factor | 2024/25 datapoint | Impact |

|---|---|---|

| Public spend | £176bn NHS | Healthcare demand, consultancy |

| Migration | 606,000 | Staffing pressure, margins |

| Regeneration | £4.8bn | Secondary deals |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Christie Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, the analysis offers forward-looking insights, detailed sub-points and practical implications ready for business plans or scenario planning.

A concise, visually segmented Christie Group PESTLE summary that relieves planning pain points by condensing external risks into an editable, shareable format for quick insertion into presentations, team alignment, or client reports.

Economic factors

Interest rates and cost of capital

Interest rate levels drive discount rates, valuation multiples and buyer affordability; 10-year government yields around 4.0–4.5% in H1 2025 compressed cap rates and lowered implied values. Higher yields slowed deal cycles and raised refinancing risk in hospitality and retail, prompting restructuring mandates. Rate cuts in late 2024–2025 began reviving transaction volumes and bid activity.

Inflation and consumer spending

Cost inflation continues to squeeze margins across restaurants, hotels and retailers — after headline inflation peaked at 9.1% in the US in 2022, rates fell but input costs and wage pressure persist, compressing EBITDA. Real income trends remain the main driver of discretionary spend and trading performance, influencing footfall and F&B spend. Indexation clauses and rising operating costs directly alter valuation inputs and capex planning. Inventory services gain relevance as operators control shrink and cash flow.

Property cycles and transaction liquidity

Capital flows into operational real estate in 2024 tightened but remained the primary driver of agency pipelines, while bid‑ask spreads widened in downturns, prolonging marketing periods; stabilized occupancy and RevPAR trends through 2024–25 supported pricing recovery, and counter‑cyclical advisory and restructuring demand helped offset slower sales activity for Christie Group.

Labour market and wage dynamics

Tight labour markets push Christie Group's hospitality and care wage bills higher; the UK National Living Wage rose to 11.44 per hour in April 2024, increasing baseline costs and compressing EBITDA margins. Persistent sector shortages raise operational risk and extend buyer diligence timelines, while productivity tools and inventory systems can offset 3–6% in labour-related cost pressure. Changes in wage policy reduce client P&L resilience and may force price or service adjustments.

- NLW 11.44 (Apr 2024)

- Labour-driven EBITDA compression 3–6%

- Staff shortages → higher buyer diligence

- Productivity tools mitigate wage impact

FX and European exposure

Sterling volatility drives translation risk for Christie Group’s EU operations, with GBP/EUR swings of roughly ±6% in 2024 increasing reported profit variability and affecting cross‑border pricing and investor appetite. Hedging and invoicing in local currency reduced margin erosion in 2024, while macro divergence across EU markets — ECB 2024 GDP ~0.8% vs UK 2024 ~0.5% — forces tailored country strategies.

- FX exposure: GBP/EUR ±6% (2024)

- Hedging: local‑currency invoicing stabilizes margins

- Macro split: EU GDP ~0.8% vs UK ~0.5% (2024)

VAT 20%, NHS £176bn, migration 606k squeeze staffing, drive secondary deals

Higher rates (10y ~4.0–4.5% H1 2025) raised cap rates and refinancing risk before late‑2024/25 cuts revived transaction volumes. Cost and wage inflation (UK NLW £11.44 Apr 2024) compress EBITDA by ~3–6% in hospitality/retail. Sterling volatility (GBP/EUR ±6% 2024) and divergent GDP (EU ~0.8% vs UK ~0.5% 2024) force tailored country strategies.

| Metric | Value |

|---|---|

| 10y yield H1 2025 | 4.0–4.5% |

| NLW (Apr 2024) | £11.44/hr |

| EBITDA squeeze | 3–6% |

| GBP/EUR 2024 | ±6% |

| GDP 2024 (EU vs UK) | 0.8% vs 0.5% |

Preview Before You Purchase

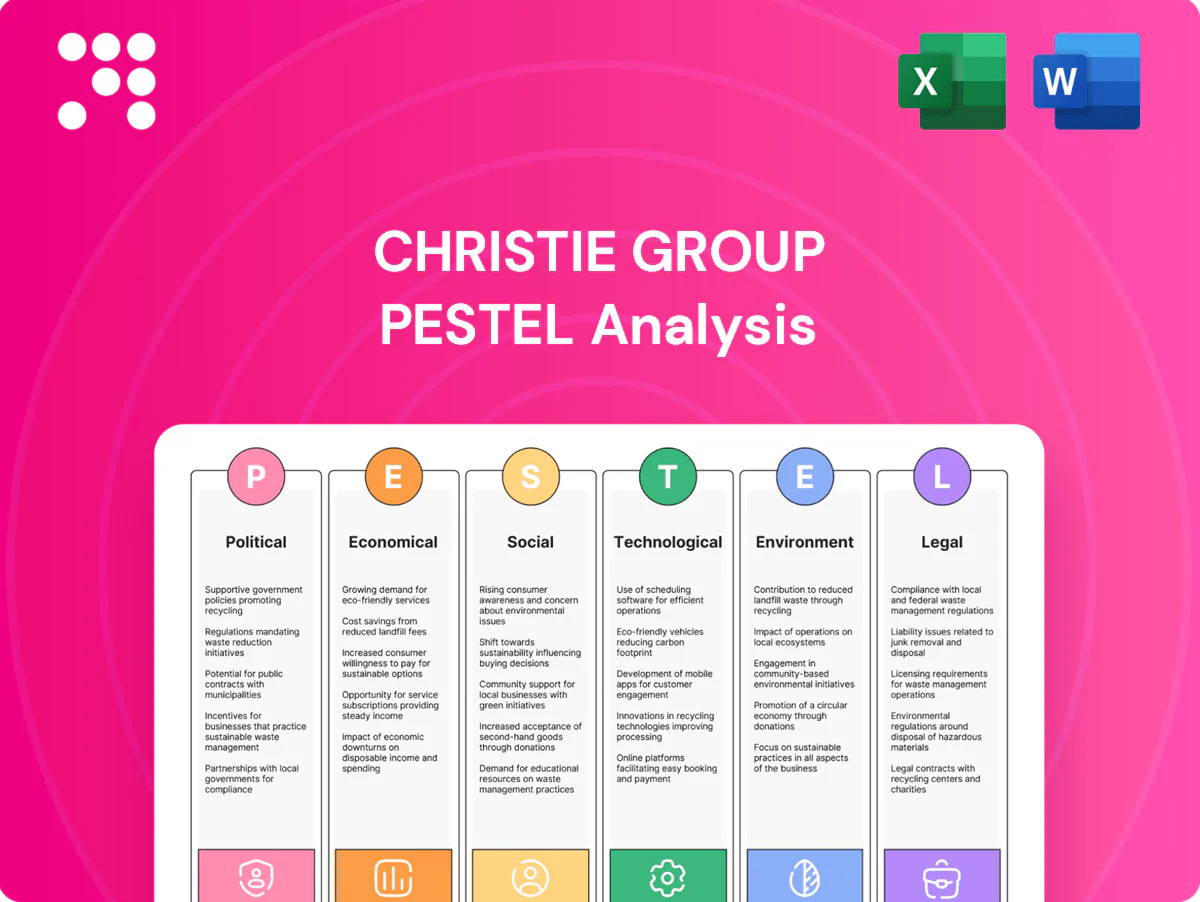

Christie Group PESTLE Analysis

The preview shown here is the exact Christie Group PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises. After checkout you'll instantly get this final, professionally structured document.

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our targeted PESTLE Analysis of Christie Group—uncover how political shifts, economic trends, social preferences, technological change, legal developments, and environmental pressures shape its outlook. Perfect for investors and strategists, this ready-to-use report turns external risks into actionable moves. Purchase the full analysis for detailed insights and downloadable templates.

Political factors

UK policy stability and public spending

Shifts in UK fiscal and industrial policy materially affect Christie Group’s hospitality, healthcare and retail pipelines; the standard VAT rate remains 20% and UK public services funding keeps NHS spending around £176bn in 2024/25, directly shaping healthcare transactions and consultancy demand. Reforms to business rates and investment incentives alter valuations and client capex plans, while political stability boosts agency deal flow and volatility stalls buyer decisions.

Post‑Brexit UK‑EU relations

Regulatory divergence since the 2020 Trade and Cooperation Agreement has increased trade frictions, raising compliance costs for UK‑EU transactions and complicating cross‑border deals. Automatic recognition of professional qualifications ended in January 2021, affecting advisory credentials and valuations across jurisdictions. Ending free movement and the points‑based system reduced EU labour flows; net migration was 606,000 (year to June 2023), straining hospitality and care staffing and deal margins. Market confidence depends on predictable UK‑EU arrangements.

Local planning and licensing regimes

Planning permissions, change‑of‑use and alcohol/gaming licences directly determine asset viability and deal timing; local variations across over 300 UK planning authorities require tailored consultancy and tight timeline management. Policy shifts toward town‑centre revitalisation—UK high‑street vacancy ~13% in 2023—can unlock retail and leisure opportunities, while tight regimes increase compliance complexity and due‑diligence workloads.

Tourism and regional development policies

Destination marketing and infrastructure investment shape leisure demand; UNWTO reported travel recovery to roughly 90% of 2019 levels by 2023, supporting higher hotel occupancy assumptions. Regeneration grants such as the UK Levelling Up Fund (£4.8bn) can catalyze transactions in secondary locations. Visa liberalization and digital visas materially affect inbound volumes while clear policy signals improve pipeline visibility for Christie Group agency and valuation services.

- Destination marketing: boosts demand and occupancy

- Regeneration grants (£4.8bn): catalyze secondary-market deals

- Visa policy: alters inbound volumes and RevPAR assumptions

- Policy clarity: improves agency/valuation pipeline visibility

Public health and crisis preparedness

Public health directives materially affect footfall and occupancy across client sectors; UNWTO reported international tourism arrivals reached about 88% of 2019 levels in 2023, underscoring sensitivity to health rules. Preparedness frameworks shape contingency plans in hospitality and care, while mandates accelerate digital adoption that Christie systems can serve; rapid policy shifts demand agile advisory responses.

- Health impact: footfall/occupancy volatility

- Preparedness: contingency-driven CAPEX planning

- Digital mandates: telemetry, contactless revenue ops

- Advisory need: fast policy-response services

VAT 20%, NHS £176bn, migration 606k squeeze staffing, drive secondary deals

UK fiscal policy (VAT 20%, NHS spend £176bn in 2024/25) and business‑rate reforms shape Christie Group deal flow and valuations; net migration 606,000 (yr to Jun 2023) tightens hospitality/care staffing. Levelling Up Fund £4.8bn and tourism recovery ~90% of 2019 by 2023 support secondary‑market transactions; planning/licensing complexity prolongs timelines.

| Factor | 2024/25 datapoint | Impact |

|---|---|---|

| Public spend | £176bn NHS | Healthcare demand, consultancy |

| Migration | 606,000 | Staffing pressure, margins |

| Regeneration | £4.8bn | Secondary deals |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Christie Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, the analysis offers forward-looking insights, detailed sub-points and practical implications ready for business plans or scenario planning.

A concise, visually segmented Christie Group PESTLE summary that relieves planning pain points by condensing external risks into an editable, shareable format for quick insertion into presentations, team alignment, or client reports.

Economic factors

Interest rates and cost of capital

Interest rate levels drive discount rates, valuation multiples and buyer affordability; 10-year government yields around 4.0–4.5% in H1 2025 compressed cap rates and lowered implied values. Higher yields slowed deal cycles and raised refinancing risk in hospitality and retail, prompting restructuring mandates. Rate cuts in late 2024–2025 began reviving transaction volumes and bid activity.

Inflation and consumer spending

Cost inflation continues to squeeze margins across restaurants, hotels and retailers — after headline inflation peaked at 9.1% in the US in 2022, rates fell but input costs and wage pressure persist, compressing EBITDA. Real income trends remain the main driver of discretionary spend and trading performance, influencing footfall and F&B spend. Indexation clauses and rising operating costs directly alter valuation inputs and capex planning. Inventory services gain relevance as operators control shrink and cash flow.

Property cycles and transaction liquidity

Capital flows into operational real estate in 2024 tightened but remained the primary driver of agency pipelines, while bid‑ask spreads widened in downturns, prolonging marketing periods; stabilized occupancy and RevPAR trends through 2024–25 supported pricing recovery, and counter‑cyclical advisory and restructuring demand helped offset slower sales activity for Christie Group.

Labour market and wage dynamics

Tight labour markets push Christie Group's hospitality and care wage bills higher; the UK National Living Wage rose to 11.44 per hour in April 2024, increasing baseline costs and compressing EBITDA margins. Persistent sector shortages raise operational risk and extend buyer diligence timelines, while productivity tools and inventory systems can offset 3–6% in labour-related cost pressure. Changes in wage policy reduce client P&L resilience and may force price or service adjustments.

- NLW 11.44 (Apr 2024)

- Labour-driven EBITDA compression 3–6%

- Staff shortages → higher buyer diligence

- Productivity tools mitigate wage impact

FX and European exposure

Sterling volatility drives translation risk for Christie Group’s EU operations, with GBP/EUR swings of roughly ±6% in 2024 increasing reported profit variability and affecting cross‑border pricing and investor appetite. Hedging and invoicing in local currency reduced margin erosion in 2024, while macro divergence across EU markets — ECB 2024 GDP ~0.8% vs UK 2024 ~0.5% — forces tailored country strategies.

- FX exposure: GBP/EUR ±6% (2024)

- Hedging: local‑currency invoicing stabilizes margins

- Macro split: EU GDP ~0.8% vs UK ~0.5% (2024)

VAT 20%, NHS £176bn, migration 606k squeeze staffing, drive secondary deals

Higher rates (10y ~4.0–4.5% H1 2025) raised cap rates and refinancing risk before late‑2024/25 cuts revived transaction volumes. Cost and wage inflation (UK NLW £11.44 Apr 2024) compress EBITDA by ~3–6% in hospitality/retail. Sterling volatility (GBP/EUR ±6% 2024) and divergent GDP (EU ~0.8% vs UK ~0.5% 2024) force tailored country strategies.

| Metric | Value |

|---|---|

| 10y yield H1 2025 | 4.0–4.5% |

| NLW (Apr 2024) | £11.44/hr |

| EBITDA squeeze | 3–6% |

| GBP/EUR 2024 | ±6% |

| GDP 2024 (EU vs UK) | 0.8% vs 0.5% |

Preview Before You Purchase

Christie Group PESTLE Analysis

The preview shown here is the exact Christie Group PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises. After checkout you'll instantly get this final, professionally structured document.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our targeted PESTLE Analysis of Christie Group—uncover how political shifts, economic trends, social preferences, technological change, legal developments, and environmental pressures shape its outlook. Perfect for investors and strategists, this ready-to-use report turns external risks into actionable moves. Purchase the full analysis for detailed insights and downloadable templates.

Political factors

UK policy stability and public spending

Shifts in UK fiscal and industrial policy materially affect Christie Group’s hospitality, healthcare and retail pipelines; the standard VAT rate remains 20% and UK public services funding keeps NHS spending around £176bn in 2024/25, directly shaping healthcare transactions and consultancy demand. Reforms to business rates and investment incentives alter valuations and client capex plans, while political stability boosts agency deal flow and volatility stalls buyer decisions.

Post‑Brexit UK‑EU relations

Regulatory divergence since the 2020 Trade and Cooperation Agreement has increased trade frictions, raising compliance costs for UK‑EU transactions and complicating cross‑border deals. Automatic recognition of professional qualifications ended in January 2021, affecting advisory credentials and valuations across jurisdictions. Ending free movement and the points‑based system reduced EU labour flows; net migration was 606,000 (year to June 2023), straining hospitality and care staffing and deal margins. Market confidence depends on predictable UK‑EU arrangements.

Local planning and licensing regimes

Planning permissions, change‑of‑use and alcohol/gaming licences directly determine asset viability and deal timing; local variations across over 300 UK planning authorities require tailored consultancy and tight timeline management. Policy shifts toward town‑centre revitalisation—UK high‑street vacancy ~13% in 2023—can unlock retail and leisure opportunities, while tight regimes increase compliance complexity and due‑diligence workloads.

Tourism and regional development policies

Destination marketing and infrastructure investment shape leisure demand; UNWTO reported travel recovery to roughly 90% of 2019 levels by 2023, supporting higher hotel occupancy assumptions. Regeneration grants such as the UK Levelling Up Fund (£4.8bn) can catalyze transactions in secondary locations. Visa liberalization and digital visas materially affect inbound volumes while clear policy signals improve pipeline visibility for Christie Group agency and valuation services.

- Destination marketing: boosts demand and occupancy

- Regeneration grants (£4.8bn): catalyze secondary-market deals

- Visa policy: alters inbound volumes and RevPAR assumptions

- Policy clarity: improves agency/valuation pipeline visibility

Public health and crisis preparedness

Public health directives materially affect footfall and occupancy across client sectors; UNWTO reported international tourism arrivals reached about 88% of 2019 levels in 2023, underscoring sensitivity to health rules. Preparedness frameworks shape contingency plans in hospitality and care, while mandates accelerate digital adoption that Christie systems can serve; rapid policy shifts demand agile advisory responses.

- Health impact: footfall/occupancy volatility

- Preparedness: contingency-driven CAPEX planning

- Digital mandates: telemetry, contactless revenue ops

- Advisory need: fast policy-response services

VAT 20%, NHS £176bn, migration 606k squeeze staffing, drive secondary deals

UK fiscal policy (VAT 20%, NHS spend £176bn in 2024/25) and business‑rate reforms shape Christie Group deal flow and valuations; net migration 606,000 (yr to Jun 2023) tightens hospitality/care staffing. Levelling Up Fund £4.8bn and tourism recovery ~90% of 2019 by 2023 support secondary‑market transactions; planning/licensing complexity prolongs timelines.

| Factor | 2024/25 datapoint | Impact |

|---|---|---|

| Public spend | £176bn NHS | Healthcare demand, consultancy |

| Migration | 606,000 | Staffing pressure, margins |

| Regeneration | £4.8bn | Secondary deals |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Christie Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, the analysis offers forward-looking insights, detailed sub-points and practical implications ready for business plans or scenario planning.

A concise, visually segmented Christie Group PESTLE summary that relieves planning pain points by condensing external risks into an editable, shareable format for quick insertion into presentations, team alignment, or client reports.

Economic factors

Interest rates and cost of capital

Interest rate levels drive discount rates, valuation multiples and buyer affordability; 10-year government yields around 4.0–4.5% in H1 2025 compressed cap rates and lowered implied values. Higher yields slowed deal cycles and raised refinancing risk in hospitality and retail, prompting restructuring mandates. Rate cuts in late 2024–2025 began reviving transaction volumes and bid activity.

Inflation and consumer spending

Cost inflation continues to squeeze margins across restaurants, hotels and retailers — after headline inflation peaked at 9.1% in the US in 2022, rates fell but input costs and wage pressure persist, compressing EBITDA. Real income trends remain the main driver of discretionary spend and trading performance, influencing footfall and F&B spend. Indexation clauses and rising operating costs directly alter valuation inputs and capex planning. Inventory services gain relevance as operators control shrink and cash flow.

Property cycles and transaction liquidity

Capital flows into operational real estate in 2024 tightened but remained the primary driver of agency pipelines, while bid‑ask spreads widened in downturns, prolonging marketing periods; stabilized occupancy and RevPAR trends through 2024–25 supported pricing recovery, and counter‑cyclical advisory and restructuring demand helped offset slower sales activity for Christie Group.

Labour market and wage dynamics

Tight labour markets push Christie Group's hospitality and care wage bills higher; the UK National Living Wage rose to 11.44 per hour in April 2024, increasing baseline costs and compressing EBITDA margins. Persistent sector shortages raise operational risk and extend buyer diligence timelines, while productivity tools and inventory systems can offset 3–6% in labour-related cost pressure. Changes in wage policy reduce client P&L resilience and may force price or service adjustments.

- NLW 11.44 (Apr 2024)

- Labour-driven EBITDA compression 3–6%

- Staff shortages → higher buyer diligence

- Productivity tools mitigate wage impact

FX and European exposure

Sterling volatility drives translation risk for Christie Group’s EU operations, with GBP/EUR swings of roughly ±6% in 2024 increasing reported profit variability and affecting cross‑border pricing and investor appetite. Hedging and invoicing in local currency reduced margin erosion in 2024, while macro divergence across EU markets — ECB 2024 GDP ~0.8% vs UK 2024 ~0.5% — forces tailored country strategies.

- FX exposure: GBP/EUR ±6% (2024)

- Hedging: local‑currency invoicing stabilizes margins

- Macro split: EU GDP ~0.8% vs UK ~0.5% (2024)

VAT 20%, NHS £176bn, migration 606k squeeze staffing, drive secondary deals

Higher rates (10y ~4.0–4.5% H1 2025) raised cap rates and refinancing risk before late‑2024/25 cuts revived transaction volumes. Cost and wage inflation (UK NLW £11.44 Apr 2024) compress EBITDA by ~3–6% in hospitality/retail. Sterling volatility (GBP/EUR ±6% 2024) and divergent GDP (EU ~0.8% vs UK ~0.5% 2024) force tailored country strategies.

| Metric | Value |

|---|---|

| 10y yield H1 2025 | 4.0–4.5% |

| NLW (Apr 2024) | £11.44/hr |

| EBITDA squeeze | 3–6% |

| GBP/EUR 2024 | ±6% |

| GDP 2024 (EU vs UK) | 0.8% vs 0.5% |

Preview Before You Purchase

Christie Group PESTLE Analysis

The preview shown here is the exact Christie Group PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises. After checkout you'll instantly get this final, professionally structured document.