Chubb Porter's Five Forces Analysis

Don't Miss the Bigger Picture

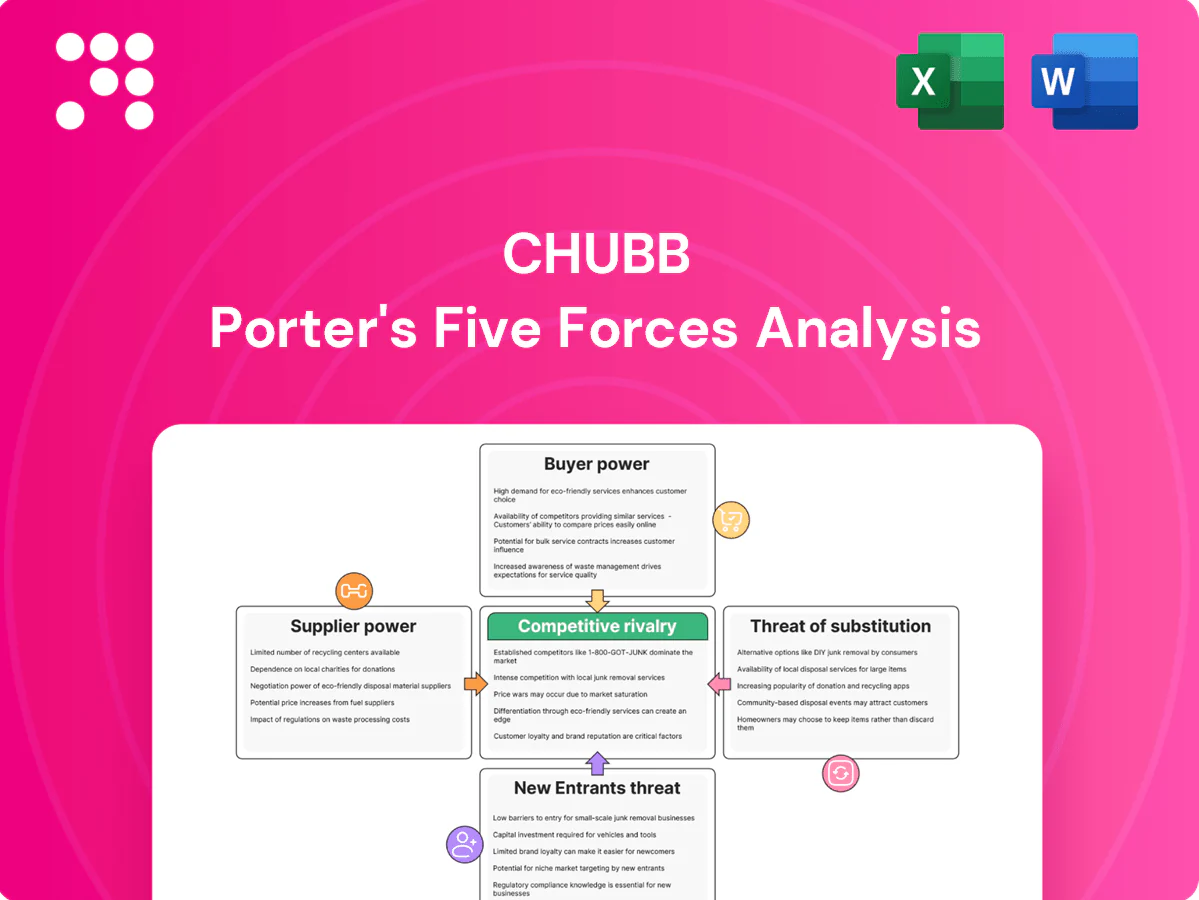

Chubb's Porter’s Five Forces snapshot highlights moderate buyer power, low supplier power, high competitive rivalry, limited substitute threat, and structural barriers to entry shaping pricing and underwriting margins. This brief preview hints at strategic risks and growth levers. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Reinsurer capacity cycles

Chubb depends on global reinsurers for peak-cat and large-limit protection, which gives reinsurers leverage during hard markets when capacity tightens; reinsurance pricing rose roughly 10–25% across major markets in 2023–24 per Aon and Swiss Re market notes. When catastrophe losses concentrate, capacity and terms worsen, but in softer phases—with capital replenishment—reinsurer power moderates. Chubb’s scale and long-term relationships enable multi-year, diversified treaties that dampen volatility.

Specialized data and models

Catastrophe modeling, data, and rating engines from a few vendors (RMS, AIR, CoreLogic) create vendor concentration and reliance on two to three dominant providers. Proprietary methodologies and integration into pricing systems generate meaningful switching costs. Dependence can skew underwriting assumptions and capital allocation. Chubb mitigates this by running multiple models, investing in internal R&D and maintaining robust model validation frameworks.

Technology and cloud vendors

Technology and cloud vendors hold moderate supplier power for Chubb because core systems, cloud, and cybersecurity integrations are complex and costly to replace. AWS (33%), Azure (23%) and GCP (11%) dominated the 2024 cloud market, increasing migration stickiness under regulatory scrutiny. Migration risks and audits elevate switching costs, while volume commitments and strict SLAs can secure favorable pricing and uptime. Adopting multi-cloud, modular architecture reduces dependence on any single provider.

Capital market alternatives

Insurance-linked securities and retro markets now act as alternative suppliers of risk capacity; the ILS market had about $60bn outstanding in 2024 and catastrophe bond issuance topped $8bn that year, which can reset reinsurance pricing and Chubb’s cost of risk transfer. Investor appetite shifts with catastrophe activity and interest rates, and Chubb taps diversified capital sources to optimize cost and flexibility.

- ILS market ~ $60bn (2024)

- Cat bond issuance > $8bn (2024)

- Pricing resets can lower Chubb’s reinsurance costs

- Investor appetite tied to catastrophe losses and rates

Talent and specialist services

Experienced underwriters, actuaries and claims experts are scarce, elevating supplier power; BLS data shows actuaries' median wage ~129,000 USD (2023) and Chubb employed ~34,000 people in 2023, concentrating hiring pressure. Compliance, legal and forensic vendors materially influence complex claim outcomes and fee structures. Wage inflation near 4% in 2024 and poaching raise costs; Chubb counters with targeted training, retention pay and global mobility programs.

- Scarcity: high salaries for specialists

- Vendors: legal/forensic shape claim resolution

- Cost pressure: ~4% wage inflation, increased poaching

- Chubb response: training, retention, global mobility

Hard reinsurance market, ILS growth and cloud concentration raise costs and retention pressure

Reinsurers gain leverage in hard markets (reins. pricing +10–25% in 2023–24), while ILS/retro ($60bn outstanding; cat bond issuance >$8bn in 2024) offer alternative capacity. Cat-model vendor concentration and cloud provider dominance (AWS 33%, Azure 23%, GCP 11% in 2024) create switching costs. Talent scarcity (actuary median wage ~$129k, Chubb ~34,000 employees) raises hiring/retention pressure; Chubb uses multi-year treaties, multi-model validation, multi-cloud and retention programs.

| Metric | 2024 figure |

|---|---|

| Reinsurance pricing | +10–25% |

| ILS market | $60bn |

| Cat bond issuance | >$8bn |

| Cloud share (AWS/Azure/GCP) | 33% / 23% / 11% |

| Actuary median wage | ~$129k |

| Chubb employees | ~34,000 |

| Wage inflation | ~4% |

What is included in the product

Tailored Porter's Five Forces analysis for Chubb that uncovers competitive pressures, supplier/buyer influence, entry barriers, substitutes, and emerging threats to its profitability.

A concise, one-sheet Porter's Five Forces summary for Chubb that clarifies competitive pressures and strategic risks at a glance—customizable for evolving market data and ready to drop into pitch decks or boardroom briefs.

Customers Bargaining Power

Brokers’ negotiating leverage

Independent brokers control access to large portions of commercial premiums; top four brokers account for over 50% of global commercial brokerage revenue in 2024, giving them clear price-discovery and program-structuring leverage that pressures insurers margins. Consolidated brokers increasingly demand enhanced terms and services. Chubb counters with differentiated coverages, elevated service levels, and long-term broker partnerships to protect margins.

Large corporate insureds

Multinationals with sizable, multi-line programs exert strong bargaining power, often driving down rates by soliciting global panels and layered towers across jurisdictions. They expect custom wording and embedded risk engineering as table stakes, leveraging procurement scale and centralized risk managers. Chubb operates in 54 countries and territories, and its multinational network and risk services help defend share and pricing against these sophisticated buyers.

Price transparency and switching

In personal lines and SME segments, widespread online comparison tools heighten price sensitivity and put downward pressure on premiums. Moderate switching costs—peaking at policy renewal—make customers responsive to offers, forcing competitors to cut rates. Chubb mitigates churn by emphasizing claims experience, digital service and bundling, leveraging its brand and service reputation to justify quality pricing.

Loss history and performance

Clients with favorable loss profiles secure lower premiums and broader terms; in 2024 Chubb reported a combined ratio near 93%, reflecting discipline that rewards low-loss business. Data sharing and telematics boost buyer leverage by proving risk reductions, while poorer risks face surcharges or limits. Chubb prioritizes profitability over volume when buyer power is excessive.

- Favorable loss profiles → better pricing

- Telematics/data → stronger buyer negotiating power

- Poor risks → surcharges/limits

- Chubb focus → underwriting discipline, ~93% combined ratio (2024)

Regulatory protections

Regulatory protections such as consumer fairness rules and filing requirements constrain Chubbs pricing flexibility by mandating rate justifications and pre-approvals, while dispute resolution and cancellation rules limit insurer leverage in claim and policy management. Standardized disclosures improve buyer comparability and bargaining power. Chubb addresses this through compliant filings, clear product documentation, and proactive customer communications.

- consumer fairness limits unilateral price changes

- filing requirements increase time-to-market

- dispute/cancellation rules reduce negotiation leverage

- standardized disclosures ease buyer comparison

- chubb mitigates via compliance, clarity, outreach

Global insurer fights broker consolidation with tailored programs, worldwide reach and underwriting

Chubb faces strong buyer power from consolidated brokers (top 4 >50% global commercial brokerage revenue, 2024) and multinational program buyers; digital comparison boosts retail price sensitivity. Chubb defends via differentiated products, global network (54 countries, 2024), underwriting discipline (combined ratio ~93% in 2024) and broker partnerships.

| Buyer | 2024 metric | Impact | Chubb response |

|---|---|---|---|

| Top brokers | >50% commercial brokerage rev | Price/program leverage | Partnerships, tailored programs |

| Multinationals | 54-country footprint | Demand custom global terms | Global network, risk services |

| Retail/SME | High online comparison | Rate sensitivity | Service, bundling |

Full Version Awaits

Chubb Porter's Five Forces Analysis

This preview shows the exact Chubb Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. The report delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes, with clear implications for strategy and risk. It’s fully formatted and ready for immediate download and use.

Don't Miss the Bigger Picture

Chubb's Porter’s Five Forces snapshot highlights moderate buyer power, low supplier power, high competitive rivalry, limited substitute threat, and structural barriers to entry shaping pricing and underwriting margins. This brief preview hints at strategic risks and growth levers. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Reinsurer capacity cycles

Chubb depends on global reinsurers for peak-cat and large-limit protection, which gives reinsurers leverage during hard markets when capacity tightens; reinsurance pricing rose roughly 10–25% across major markets in 2023–24 per Aon and Swiss Re market notes. When catastrophe losses concentrate, capacity and terms worsen, but in softer phases—with capital replenishment—reinsurer power moderates. Chubb’s scale and long-term relationships enable multi-year, diversified treaties that dampen volatility.

Specialized data and models

Catastrophe modeling, data, and rating engines from a few vendors (RMS, AIR, CoreLogic) create vendor concentration and reliance on two to three dominant providers. Proprietary methodologies and integration into pricing systems generate meaningful switching costs. Dependence can skew underwriting assumptions and capital allocation. Chubb mitigates this by running multiple models, investing in internal R&D and maintaining robust model validation frameworks.

Technology and cloud vendors

Technology and cloud vendors hold moderate supplier power for Chubb because core systems, cloud, and cybersecurity integrations are complex and costly to replace. AWS (33%), Azure (23%) and GCP (11%) dominated the 2024 cloud market, increasing migration stickiness under regulatory scrutiny. Migration risks and audits elevate switching costs, while volume commitments and strict SLAs can secure favorable pricing and uptime. Adopting multi-cloud, modular architecture reduces dependence on any single provider.

Capital market alternatives

Insurance-linked securities and retro markets now act as alternative suppliers of risk capacity; the ILS market had about $60bn outstanding in 2024 and catastrophe bond issuance topped $8bn that year, which can reset reinsurance pricing and Chubb’s cost of risk transfer. Investor appetite shifts with catastrophe activity and interest rates, and Chubb taps diversified capital sources to optimize cost and flexibility.

- ILS market ~ $60bn (2024)

- Cat bond issuance > $8bn (2024)

- Pricing resets can lower Chubb’s reinsurance costs

- Investor appetite tied to catastrophe losses and rates

Talent and specialist services

Experienced underwriters, actuaries and claims experts are scarce, elevating supplier power; BLS data shows actuaries' median wage ~129,000 USD (2023) and Chubb employed ~34,000 people in 2023, concentrating hiring pressure. Compliance, legal and forensic vendors materially influence complex claim outcomes and fee structures. Wage inflation near 4% in 2024 and poaching raise costs; Chubb counters with targeted training, retention pay and global mobility programs.

- Scarcity: high salaries for specialists

- Vendors: legal/forensic shape claim resolution

- Cost pressure: ~4% wage inflation, increased poaching

- Chubb response: training, retention, global mobility

Hard reinsurance market, ILS growth and cloud concentration raise costs and retention pressure

Reinsurers gain leverage in hard markets (reins. pricing +10–25% in 2023–24), while ILS/retro ($60bn outstanding; cat bond issuance >$8bn in 2024) offer alternative capacity. Cat-model vendor concentration and cloud provider dominance (AWS 33%, Azure 23%, GCP 11% in 2024) create switching costs. Talent scarcity (actuary median wage ~$129k, Chubb ~34,000 employees) raises hiring/retention pressure; Chubb uses multi-year treaties, multi-model validation, multi-cloud and retention programs.

| Metric | 2024 figure |

|---|---|

| Reinsurance pricing | +10–25% |

| ILS market | $60bn |

| Cat bond issuance | >$8bn |

| Cloud share (AWS/Azure/GCP) | 33% / 23% / 11% |

| Actuary median wage | ~$129k |

| Chubb employees | ~34,000 |

| Wage inflation | ~4% |

What is included in the product

Tailored Porter's Five Forces analysis for Chubb that uncovers competitive pressures, supplier/buyer influence, entry barriers, substitutes, and emerging threats to its profitability.

A concise, one-sheet Porter's Five Forces summary for Chubb that clarifies competitive pressures and strategic risks at a glance—customizable for evolving market data and ready to drop into pitch decks or boardroom briefs.

Customers Bargaining Power

Brokers’ negotiating leverage

Independent brokers control access to large portions of commercial premiums; top four brokers account for over 50% of global commercial brokerage revenue in 2024, giving them clear price-discovery and program-structuring leverage that pressures insurers margins. Consolidated brokers increasingly demand enhanced terms and services. Chubb counters with differentiated coverages, elevated service levels, and long-term broker partnerships to protect margins.

Large corporate insureds

Multinationals with sizable, multi-line programs exert strong bargaining power, often driving down rates by soliciting global panels and layered towers across jurisdictions. They expect custom wording and embedded risk engineering as table stakes, leveraging procurement scale and centralized risk managers. Chubb operates in 54 countries and territories, and its multinational network and risk services help defend share and pricing against these sophisticated buyers.

Price transparency and switching

In personal lines and SME segments, widespread online comparison tools heighten price sensitivity and put downward pressure on premiums. Moderate switching costs—peaking at policy renewal—make customers responsive to offers, forcing competitors to cut rates. Chubb mitigates churn by emphasizing claims experience, digital service and bundling, leveraging its brand and service reputation to justify quality pricing.

Loss history and performance

Clients with favorable loss profiles secure lower premiums and broader terms; in 2024 Chubb reported a combined ratio near 93%, reflecting discipline that rewards low-loss business. Data sharing and telematics boost buyer leverage by proving risk reductions, while poorer risks face surcharges or limits. Chubb prioritizes profitability over volume when buyer power is excessive.

- Favorable loss profiles → better pricing

- Telematics/data → stronger buyer negotiating power

- Poor risks → surcharges/limits

- Chubb focus → underwriting discipline, ~93% combined ratio (2024)

Regulatory protections

Regulatory protections such as consumer fairness rules and filing requirements constrain Chubbs pricing flexibility by mandating rate justifications and pre-approvals, while dispute resolution and cancellation rules limit insurer leverage in claim and policy management. Standardized disclosures improve buyer comparability and bargaining power. Chubb addresses this through compliant filings, clear product documentation, and proactive customer communications.

- consumer fairness limits unilateral price changes

- filing requirements increase time-to-market

- dispute/cancellation rules reduce negotiation leverage

- standardized disclosures ease buyer comparison

- chubb mitigates via compliance, clarity, outreach

Global insurer fights broker consolidation with tailored programs, worldwide reach and underwriting

Chubb faces strong buyer power from consolidated brokers (top 4 >50% global commercial brokerage revenue, 2024) and multinational program buyers; digital comparison boosts retail price sensitivity. Chubb defends via differentiated products, global network (54 countries, 2024), underwriting discipline (combined ratio ~93% in 2024) and broker partnerships.

| Buyer | 2024 metric | Impact | Chubb response |

|---|---|---|---|

| Top brokers | >50% commercial brokerage rev | Price/program leverage | Partnerships, tailored programs |

| Multinationals | 54-country footprint | Demand custom global terms | Global network, risk services |

| Retail/SME | High online comparison | Rate sensitivity | Service, bundling |

Full Version Awaits

Chubb Porter's Five Forces Analysis

This preview shows the exact Chubb Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. The report delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes, with clear implications for strategy and risk. It’s fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Chubb's Porter’s Five Forces snapshot highlights moderate buyer power, low supplier power, high competitive rivalry, limited substitute threat, and structural barriers to entry shaping pricing and underwriting margins. This brief preview hints at strategic risks and growth levers. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Reinsurer capacity cycles

Chubb depends on global reinsurers for peak-cat and large-limit protection, which gives reinsurers leverage during hard markets when capacity tightens; reinsurance pricing rose roughly 10–25% across major markets in 2023–24 per Aon and Swiss Re market notes. When catastrophe losses concentrate, capacity and terms worsen, but in softer phases—with capital replenishment—reinsurer power moderates. Chubb’s scale and long-term relationships enable multi-year, diversified treaties that dampen volatility.

Specialized data and models

Catastrophe modeling, data, and rating engines from a few vendors (RMS, AIR, CoreLogic) create vendor concentration and reliance on two to three dominant providers. Proprietary methodologies and integration into pricing systems generate meaningful switching costs. Dependence can skew underwriting assumptions and capital allocation. Chubb mitigates this by running multiple models, investing in internal R&D and maintaining robust model validation frameworks.

Technology and cloud vendors

Technology and cloud vendors hold moderate supplier power for Chubb because core systems, cloud, and cybersecurity integrations are complex and costly to replace. AWS (33%), Azure (23%) and GCP (11%) dominated the 2024 cloud market, increasing migration stickiness under regulatory scrutiny. Migration risks and audits elevate switching costs, while volume commitments and strict SLAs can secure favorable pricing and uptime. Adopting multi-cloud, modular architecture reduces dependence on any single provider.

Capital market alternatives

Insurance-linked securities and retro markets now act as alternative suppliers of risk capacity; the ILS market had about $60bn outstanding in 2024 and catastrophe bond issuance topped $8bn that year, which can reset reinsurance pricing and Chubb’s cost of risk transfer. Investor appetite shifts with catastrophe activity and interest rates, and Chubb taps diversified capital sources to optimize cost and flexibility.

- ILS market ~ $60bn (2024)

- Cat bond issuance > $8bn (2024)

- Pricing resets can lower Chubb’s reinsurance costs

- Investor appetite tied to catastrophe losses and rates

Talent and specialist services

Experienced underwriters, actuaries and claims experts are scarce, elevating supplier power; BLS data shows actuaries' median wage ~129,000 USD (2023) and Chubb employed ~34,000 people in 2023, concentrating hiring pressure. Compliance, legal and forensic vendors materially influence complex claim outcomes and fee structures. Wage inflation near 4% in 2024 and poaching raise costs; Chubb counters with targeted training, retention pay and global mobility programs.

- Scarcity: high salaries for specialists

- Vendors: legal/forensic shape claim resolution

- Cost pressure: ~4% wage inflation, increased poaching

- Chubb response: training, retention, global mobility

Hard reinsurance market, ILS growth and cloud concentration raise costs and retention pressure

Reinsurers gain leverage in hard markets (reins. pricing +10–25% in 2023–24), while ILS/retro ($60bn outstanding; cat bond issuance >$8bn in 2024) offer alternative capacity. Cat-model vendor concentration and cloud provider dominance (AWS 33%, Azure 23%, GCP 11% in 2024) create switching costs. Talent scarcity (actuary median wage ~$129k, Chubb ~34,000 employees) raises hiring/retention pressure; Chubb uses multi-year treaties, multi-model validation, multi-cloud and retention programs.

| Metric | 2024 figure |

|---|---|

| Reinsurance pricing | +10–25% |

| ILS market | $60bn |

| Cat bond issuance | >$8bn |

| Cloud share (AWS/Azure/GCP) | 33% / 23% / 11% |

| Actuary median wage | ~$129k |

| Chubb employees | ~34,000 |

| Wage inflation | ~4% |

What is included in the product

Tailored Porter's Five Forces analysis for Chubb that uncovers competitive pressures, supplier/buyer influence, entry barriers, substitutes, and emerging threats to its profitability.

A concise, one-sheet Porter's Five Forces summary for Chubb that clarifies competitive pressures and strategic risks at a glance—customizable for evolving market data and ready to drop into pitch decks or boardroom briefs.

Customers Bargaining Power

Brokers’ negotiating leverage

Independent brokers control access to large portions of commercial premiums; top four brokers account for over 50% of global commercial brokerage revenue in 2024, giving them clear price-discovery and program-structuring leverage that pressures insurers margins. Consolidated brokers increasingly demand enhanced terms and services. Chubb counters with differentiated coverages, elevated service levels, and long-term broker partnerships to protect margins.

Large corporate insureds

Multinationals with sizable, multi-line programs exert strong bargaining power, often driving down rates by soliciting global panels and layered towers across jurisdictions. They expect custom wording and embedded risk engineering as table stakes, leveraging procurement scale and centralized risk managers. Chubb operates in 54 countries and territories, and its multinational network and risk services help defend share and pricing against these sophisticated buyers.

Price transparency and switching

In personal lines and SME segments, widespread online comparison tools heighten price sensitivity and put downward pressure on premiums. Moderate switching costs—peaking at policy renewal—make customers responsive to offers, forcing competitors to cut rates. Chubb mitigates churn by emphasizing claims experience, digital service and bundling, leveraging its brand and service reputation to justify quality pricing.

Loss history and performance

Clients with favorable loss profiles secure lower premiums and broader terms; in 2024 Chubb reported a combined ratio near 93%, reflecting discipline that rewards low-loss business. Data sharing and telematics boost buyer leverage by proving risk reductions, while poorer risks face surcharges or limits. Chubb prioritizes profitability over volume when buyer power is excessive.

- Favorable loss profiles → better pricing

- Telematics/data → stronger buyer negotiating power

- Poor risks → surcharges/limits

- Chubb focus → underwriting discipline, ~93% combined ratio (2024)

Regulatory protections

Regulatory protections such as consumer fairness rules and filing requirements constrain Chubbs pricing flexibility by mandating rate justifications and pre-approvals, while dispute resolution and cancellation rules limit insurer leverage in claim and policy management. Standardized disclosures improve buyer comparability and bargaining power. Chubb addresses this through compliant filings, clear product documentation, and proactive customer communications.

- consumer fairness limits unilateral price changes

- filing requirements increase time-to-market

- dispute/cancellation rules reduce negotiation leverage

- standardized disclosures ease buyer comparison

- chubb mitigates via compliance, clarity, outreach

Global insurer fights broker consolidation with tailored programs, worldwide reach and underwriting

Chubb faces strong buyer power from consolidated brokers (top 4 >50% global commercial brokerage revenue, 2024) and multinational program buyers; digital comparison boosts retail price sensitivity. Chubb defends via differentiated products, global network (54 countries, 2024), underwriting discipline (combined ratio ~93% in 2024) and broker partnerships.

| Buyer | 2024 metric | Impact | Chubb response |

|---|---|---|---|

| Top brokers | >50% commercial brokerage rev | Price/program leverage | Partnerships, tailored programs |

| Multinationals | 54-country footprint | Demand custom global terms | Global network, risk services |

| Retail/SME | High online comparison | Rate sensitivity | Service, bundling |

Full Version Awaits

Chubb Porter's Five Forces Analysis

This preview shows the exact Chubb Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. The report delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes, with clear implications for strategy and risk. It’s fully formatted and ready for immediate download and use.